Dear Friend,

SpaceX is doing something no mega-IPO has ever done.

30% of shares reserved for retail investors. Through Robinhood. Fidelity. Schwab.

Sounds generous, right?

It's not.

At $1.75 trillion, you're buying the most expensive IPO in history — at 266 times earnings — on Day 1.

The institutions who got in at $800 billion need someone to sell to. That someone is you.

But there's another way.

One small company in Musk's supply chain is still trading at a fraction of its value. It builds the power infrastructure Colossus can't run without.

You don't need an IPO allocation. You need this ticker.

Dylan Jovine has it — free.

Skip the IPO trap. Get the backdoor ticker >>

“The Buck Stops Here,”

Kelly Maguire

Behind the Markets

5 Under-the-Radar AI Stocks to Watch in June

Written by Thomas Hughes. First Published: 5/31/2026.

Key Points

- Five AI-linked stocks across semiconductors, cybersecurity, and emerging tech present potential trading opportunities in June with specific catalysts ahead.

- Zscaler's May selloff is characterized as an overreaction, with analysts seeing up to 65% upside as AI-driven cybersecurity demand remains intact.

- Smaller-cap names such as Aeluma, AirJoule, and Everspin offer higher-risk exposure to AI infrastructure, cooling, and niche memory applications respectively.

- Special Report: Elon Musk: This Could Turn $100 into $100,000

Believe it or not, June is here, along with the summer trading season. That means lower trading volumes, the potential for volatility, and opportunities for savvy traders. The market rally is broadening, but it remains centered on tech. The stocks with the highest potential for movement and catalysts in play are smaller-cap tech names, though there are still some big moves ahead in mega-, large-, and mid-cap stocks as well. The unifying theme is AI; the only question is where in the ecosystem to invest and what the company-specific catalysts may be.

Aeluma: On Track for Commercialization—Deals Are in the Works

Aeluma (NASDAQ: ALMU) is an emerging tech play that is critical to AI, as its photonic and compound semiconductor technologies are game-changers for data centers. The photonic aspect is crucial for connectivity and networking, enabling high-speed, ultra-wideband, low-latency data transmission. Likewise, the company's manufacturing process enables faster, more efficient compound semiconductor fabrication. The combination promises to unleash AI capacity and power, helping alleviate bottlenecks throughout the system.

The #1 stock to buy BEFORE the June 12th filing (Ad)

When the SpaceX IPO launches, most retail investors will be locked out. The banks, funds, and insiders get in early - while everyone else waits on the sidelines.

But one small infrastructure supplier - a critical piece Musk can't scale the Colossus network without - is still trading well under institutional radar. A new briefing reveals the name and ticker at no cost.

Get the SpaceX infrastructure stock name and ticker hereA critical catalyst in June is the expectation of contracts. Aeluma is making small sales but has yet to secure a major original equipment manufacturer contract. Talks are in progress and are expected to yield results soon, if not in June, then in the months ahead.

At that time, the company will likely provide an update on government contracts and projects, as well as supply chain and capacity progress. Five analysts rate Aeluma as a Moderate Buy with a $25 price target. Technicals suggest more than 100% upside is possible, provided the expected bullish catalyst emerges.

AirJoule Technologies: Commercialization in Play

AirJoule (NASDAQ: AIRJ) is another emerging tech company with implications well beyond AI. The company harvests water directly from ambient air using waste heat—a process that simultaneously dehumidifies and cools. For data centers, this creates a compelling dual benefit: it reduces cooling load while producing the pure water those cooling systems need on-site. The result is lower operating costs, greater energy efficiency, and longer hardware life.

Catalysts for AirJoule in June include updates on partnerships and initial deployments, as well as news on when its commercial-scale product will be available. As it stands, the full rollout is expected in late Q4 this year. Five analysts rate this stock as a Moderate Buy and see it advancing by approximately 90% at the consensus.

Amprius Technologies: Ramping Capacity and Accelerating Growth

Amprius Technologies' (NYSE: AMPX) June catalysts include updates on its capacity, ecosystem, and order backlog. The Q1 report showed strength and set expectations for acceleration in the current quarter. Analysts forecast a 90% revenue gain and expect growth to persist at a hyper pace for at least the next 10 quarters.

The Q1 strength was widely expected, leading to a sell-the-news event compounded by the exchange. AMPX recently issued 2.7 million shares but retired more than 7 million warrants, creating a near-term headwind and potential leverage for a subsequent rally. MarketBeat data reveal that institutions bought the dip, short interest is down from its peak, and analyst sentiment is firming, pointing to upside above $20. AMPX’s next earnings report is due in early August.

Zscaler: Irrational Sell-Off Opens Door to Opportunity

Zscaler’s (NASDAQ: ZS) May price plunge was alarming. However, the cause was increased spending, which is tied to demand and AI. Not only is AI driving the need for cybersecurity, but it is also improving it, and Zscaler is doubling down. The company is a mission-critical component of the AI ecosystem, enabling easy-to-use, scalable, cloud-native security well suited to AI. Its zero-trust architecture means only qualified agents can access enterprise resources. The takeaway for investors is that Zscaler's results were solid and the AI flywheel is spinning.

Evidence from Zscaler and other AI-focused companies shows that AI spending drives greater demand for AI. ZS’s price should recover, and the rebound may not take long to gain traction. Analysts are lowering targets, but the market has overreacted, falling well below the low end of those targets, with potential for 65% upside at the consensus. The primary catalyst will be news about the sales team transition: good news will strengthen the outlook and put momentum back into Zscaler’s stock price.

Everspin Technologies: Persistent Memory for a Growing Market

Everspin Technologies (NASDAQ: MRAM) is a critical player in AI, not for its impact on data centers, but for its impact on AI applications. The MRAM memory technology offers numerous benefits for niche markets, including consumer wearables, aerospace, and defense, all of which benefit from AI infrastructure and the internet of things (IoT). Advantages include the speed of RAM and the persistence of Flash, combined with radiation and temperature resistance and lower power consumption. While MRAM requires more power to write, it requires no power to persist, making it essential in some use cases.

What the market gets wrong about Everspin is thinking it's another HBM or data center play, when in reality it's a play on long-term AI applications and physical AI. While revenue has been stagnant for years and has been slow to improve, the AI upcycle has only just begun. The likely outcome is that MRAM technology becomes more widely used over time. Near-term catalysts include a rebuttal to a short report and updates on government contracts.

TJX Companies Fires on All Cylinders With 9% Revenue Growth

Written by Thomas Hughes. First Published: 5/21/2026.

Key Points

- TJX Companies is on track to hit fresh highs and continue advancing as cash flow and capital returns underpin price action.

- Off-price business is hot, and TJX expects strength to persist this year.

- Analysts and institutions show high conviction and accumulated shares ahead of the Q1 earnings release.

- Special Report: Elon Musk: This Could Turn $100 into $100,000

TJX Companies' (NYSE: TJX) uptrend has limits, but those limits have yet to be reached. Accelerating business, dividends, and share buybacks suggest the rally will not only continue but may even accelerate in the second half.

The company recently boosted its share buyback program, giving investors added confidence in its future growth. As of the end of Q1, the company had repurchased only 20% of its new fiscal-year 2027 (FY2027) target, and the share count was down 1% year-over-year (YOY) and year-to-date. That is meaningful leverage for investors who already have several reasons to own this stock.

TJX Companies Is in Demand: Consumer Trends Are Strong for This Retailer

The #1 stock to buy BEFORE the June 12th filing (Ad)

When the SpaceX IPO launches, most retail investors will be locked out. The banks, funds, and insiders get in early - while everyone else waits on the sidelines.

But one small infrastructure supplier - a critical piece Musk can't scale the Colossus network without - is still trading well under institutional radar. A new briefing reveals the name and ticker at no cost.

Get the SpaceX infrastructure stock name and ticker hereTJX Companies had a solid quarter, with results reflecting both the strength of consumers and the pressures they continue to face. While inflation is limiting spending power for some retailers, consumers are flocking to off-price names, and TJX remains the leader. The company reported $14.32 billion in quarterly revenue, up more than 9% YOY and more than 200 basis points above expectations. Strength was broad-based across segments, led by a 9% gain at HomeGoods, a 7% increase in Canada, and a 6% gain in the core U.S. market. Comparable sales, a key indicator of organic growth, increased 6% across the network, well ahead of management's forecast.

The company’s merchandise mix and store traffic showed up in the margins. TJX widened gross margin by 180 basis points (bps), pretax margin by 170 bps, and GAAP earnings by 2,900 bps, or 1,900 bps better than MarketBeat’s reported consensus. Looking ahead, management expects those strengths to continue and raised guidance. The only issue is that Q2 and FY2027 guidance came in slightly below market expectations, but that does not appear to be worrying investors. Trends in comparable sales and store count suggest the guidance is conservative, leaving room for outperformance. Executives forecast 2.5% comparable sales growth in Q2.

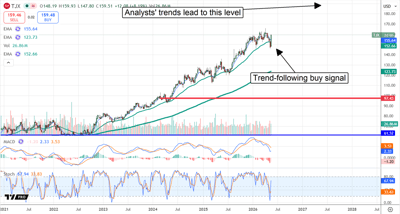

TJX price action surged more than 5% following the earnings release, reinforcing support at the $150 level. The move was strong, confirming a support target identified earlier this year and offering a trend-following entry for investors. The most likely outcome is that the stock will continue to move higher, potentially crossing a critical threshold by midyear. That threshold is the current all-time high, which could prompt many market participants to buy or add to positions. In that scenario, TJX shares could quickly move into the $170 range and continue trending higher in subsequent quarters. Long-term forecasts suggest as much as 100% upside over the next three to five years.

TJX Balance Sheet Strengthens in Q1: Shareholder Value Improved

TJX Companies' balance sheet reflects the strength of its market position and Q1 cash flow. The company’s cash, receivables, inventory, and assets all increased, while debt declined despite its aggressive capital return strategy.

The dividend is nearly as attractive as the buyback program, yielding approximately 1.2% as of late May and supported by expectations for further growth. The payout remains secure at just 35% of earnings, and dividend growth has compounded at a respectable double-digit pace in recent years. The pace of increases will likely slow in the coming years, but it should continue, keeping this Dividend Champion on track to eventually be crowned a Dividend King.

Institutions and analysts show high conviction in this investment. MarketBeat tracks 25 analysts who rate it a Buy with 100% bias, while institutions own more than 90% of the stock. The consensus forecast suggests only modest upside, but the revision trend is bullish and points toward $200, with room to continue as the year progresses. Institutions were selling shares early in 2026, helping cap gains, but shifted back to an accumulation stance in early Q2, supporting the stock at this critical price level.

TJX Fires on All Cylinders in Fiscal Year 2027

TJX Companies' biggest risks this year include rising fuel costs, higher inventory levels, and a stretched valuation. Rising fuel costs could pressure profitability, but that has not yet shown up in results or guidance. Higher inventory levels could also weigh on margins if markdowns increase, though that is not evident in the report or outlook. Valuation is the bigger concern, since execution will be critical. Even so, the stock’s 29X current-year earnings multiple is average for this market. The takeaway for investors is that TJX is firing on all cylinders in 2026, with signs of increasing momentum. It is taking share from competitors, including Target (NYSE: TGT), which continues to struggle with its turnaround efforts.

to bring you the latest market-moving news.

This message is a sponsored email from Behind the Markets, a third-party advertiser of TickerReport and MarketBeat.

Contact Us | Unsubscribe

Copyright 2006-2026 MarketBeat Media, LLC dba TickerReport. All rights reserved.

345 N Reid Place, Sixth Floor, Sioux Falls, South Dakota 57103-7078. United States..

No comments:

Post a Comment