|

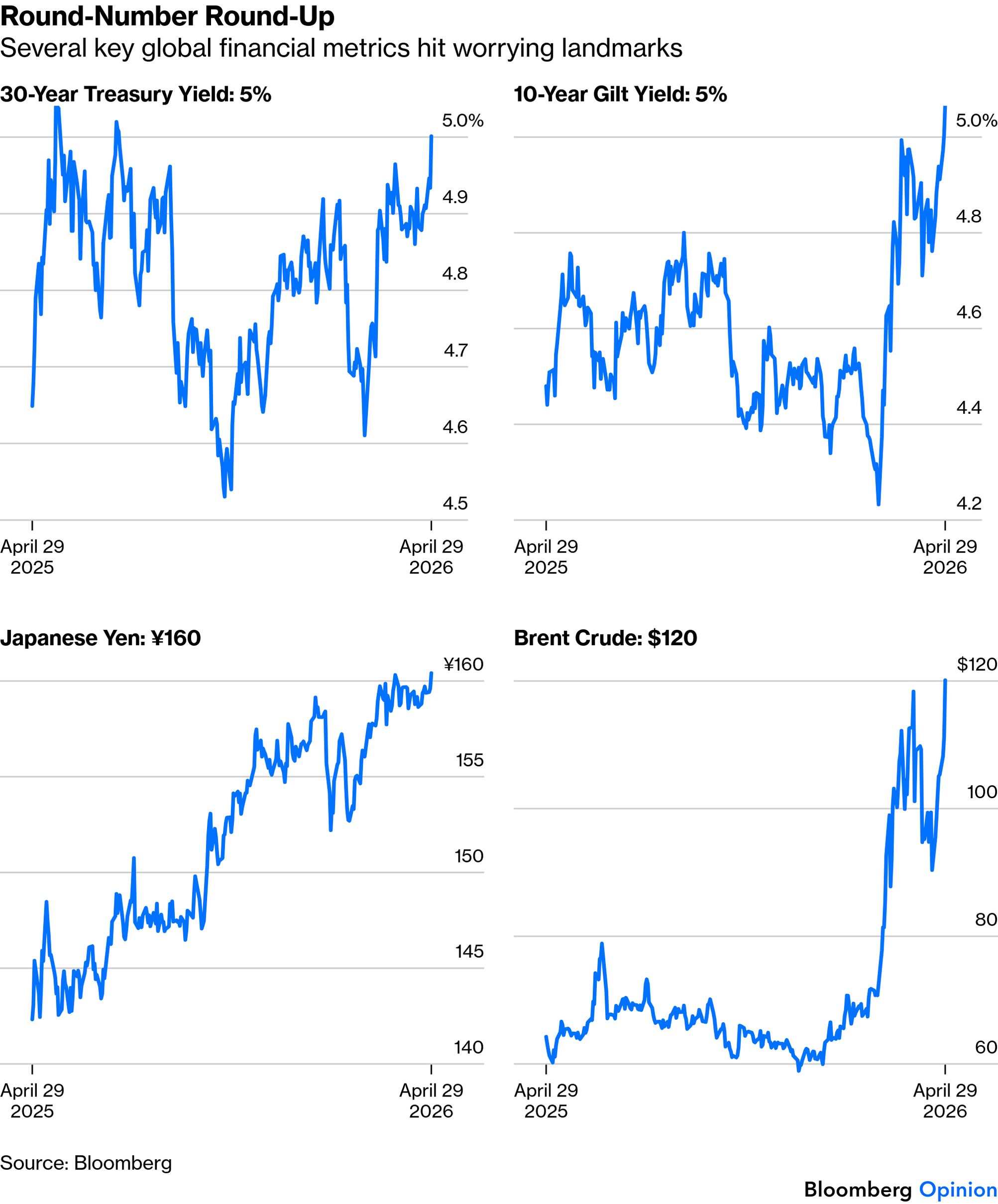

The story seems clear. The Strait of Hormuz is still closed, there’s no longer any pretense of serious negotiations to open it, and oil prices have reacted by blasting upward. Helped along by the United Arab Emirates’ withdrawal from OPEC+, Brent crude — the world’s most followed benchmark — topped $120 per barrel on Wednesday and closed higher than at any time during the conflict. That drove a series of classic alarm bells across global markets, taking out closely watched landmarks. Bond yields surged, with 10-year gilts topping 5% for the first time since 2008; 30-year Treasury yields hitting 5% for the first time this year; and the Japanese yen over 160 to the dollar. These all suggest alarm about inflation. The war is at a tipping point where markets accept that it will seriously damage the global economy:

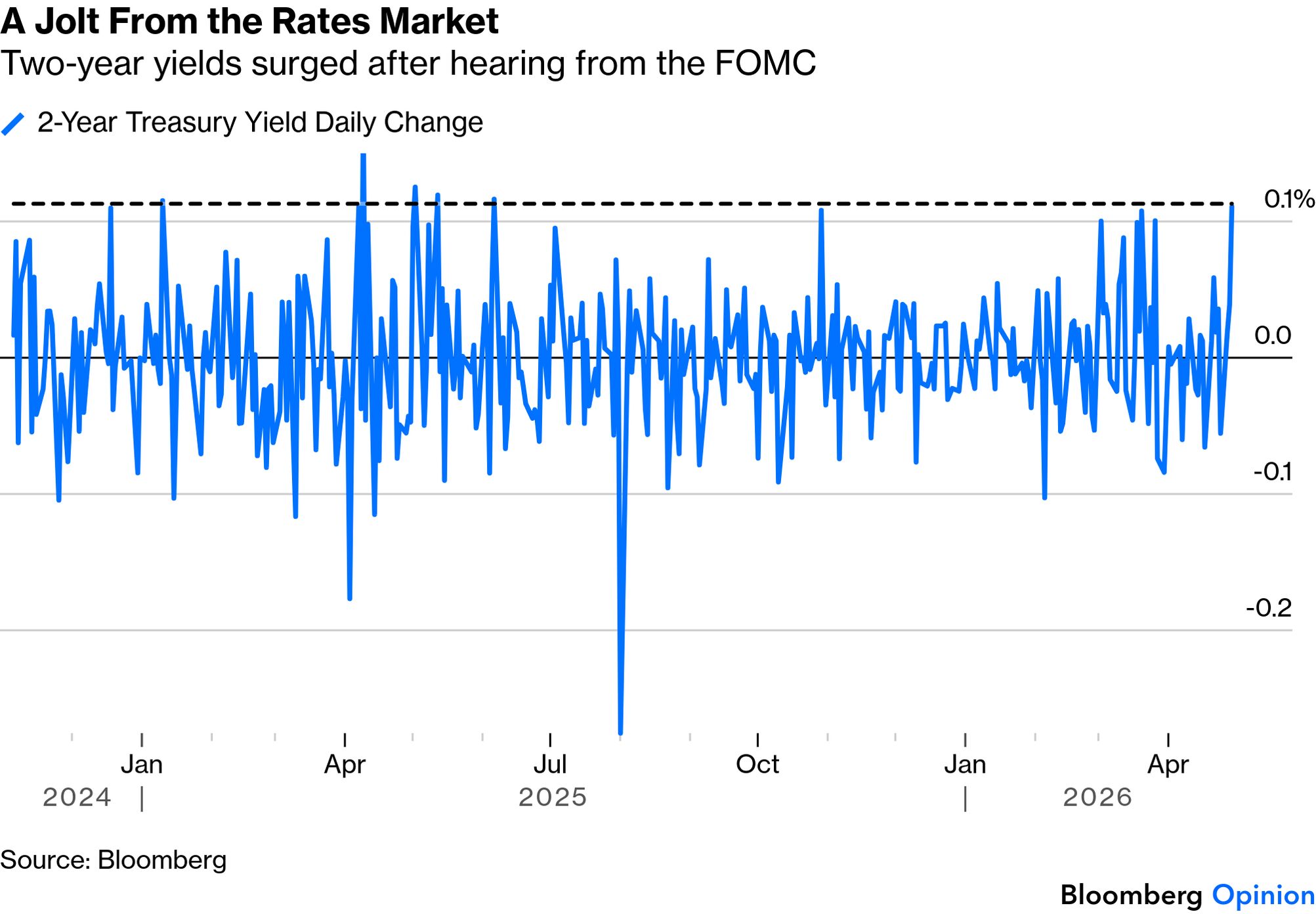

They also had to absorb news of a more hawkish Federal Reserve than had been expected (we’ll cover below), which made two-year Treasury yields jump by 11 basis points, their biggest rise in more than six months:

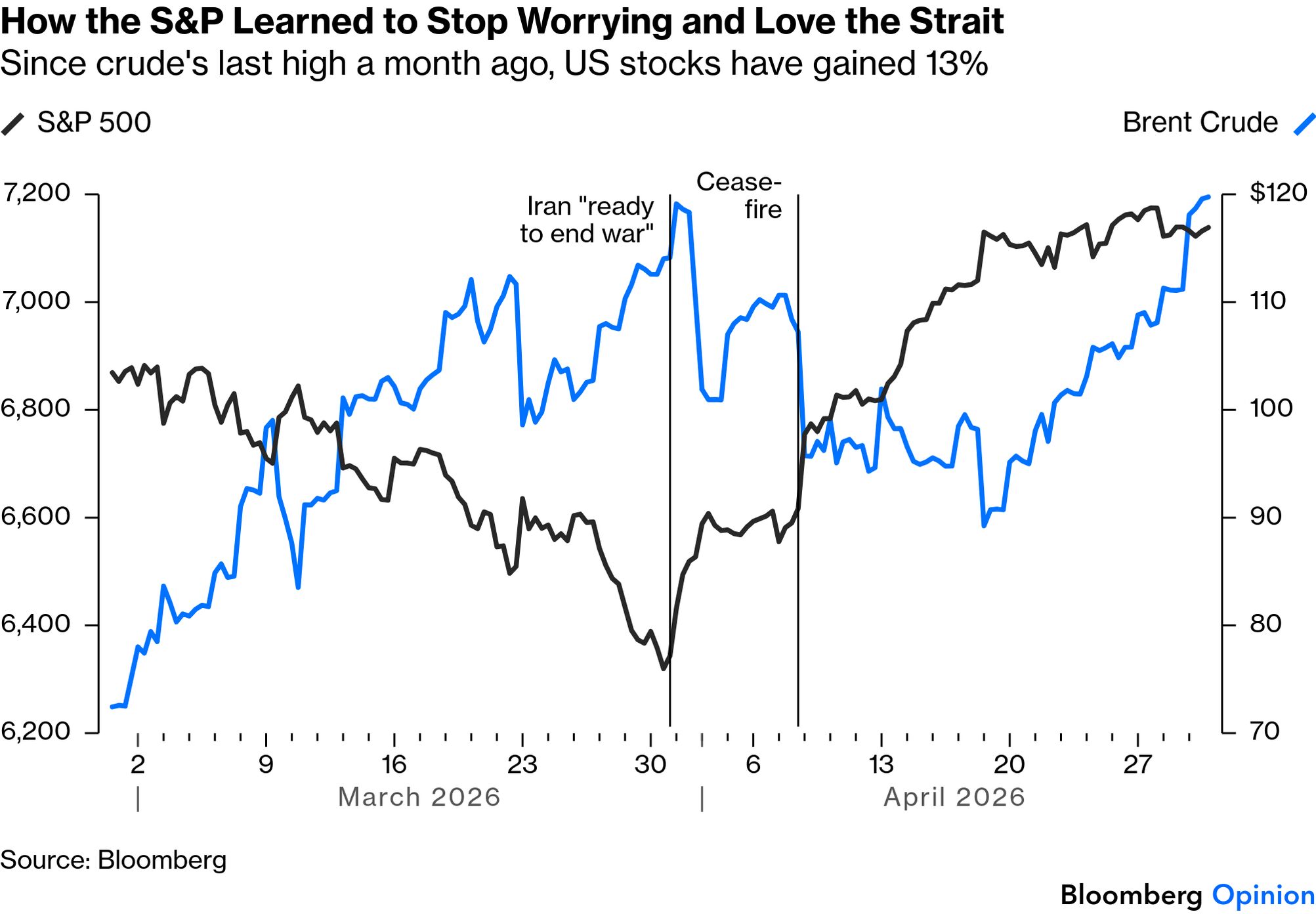

So what happened to the stock market? The Nasdaq 100 gained for the day, while the S&P 500 was flat. During the war’s first month, crude and the S&P 500 had a perfectly inverse relationship. During the second just ended, they rose together. The S&P hit a low when Brent logged its previous high on March 30. Since then, oil has reclaimed its peak, while the S&P rallied by 13%:

The war isn’t over, and many of the world’s most important markets are behaving as though it’s getting more damaging. But for US stocks, they think it’s over. Measures of volatility show that the amount people are paying to hedge future price moves in both equities and bonds are back where they were before the attack on Iran:

Polymarket now puts odds of only 52% on the Strait reopening by the end of June — implying we’re not even half way through the blockage. A protracted stalemate that creates shortages now looms as the likeliest outcome. Two months ago, when the war was supposed to end in a matter of days, that would have been an unrealistically doom-laden scenario implying a bear market for stocks. Now it’s the base case. And stocks are up. How to explain this? As Points of Return has covered, earnings expectations are behaving like a force of nature, and that is more important than anything else when pricing the stock market. Knowledge that all the biggest hyperscaler groups were announcing results after the close (which we’re also coming to) would make people reluctant to exit from the market. The way markets managed to keep on track as the Ukraine war bogged down into a stalemate, and dealt with last year’s tariff war, has also made traders confident. And if inflation is rising, stocks can be a good place to shelter. That said, it’s hard to believe they’re not over-confident.

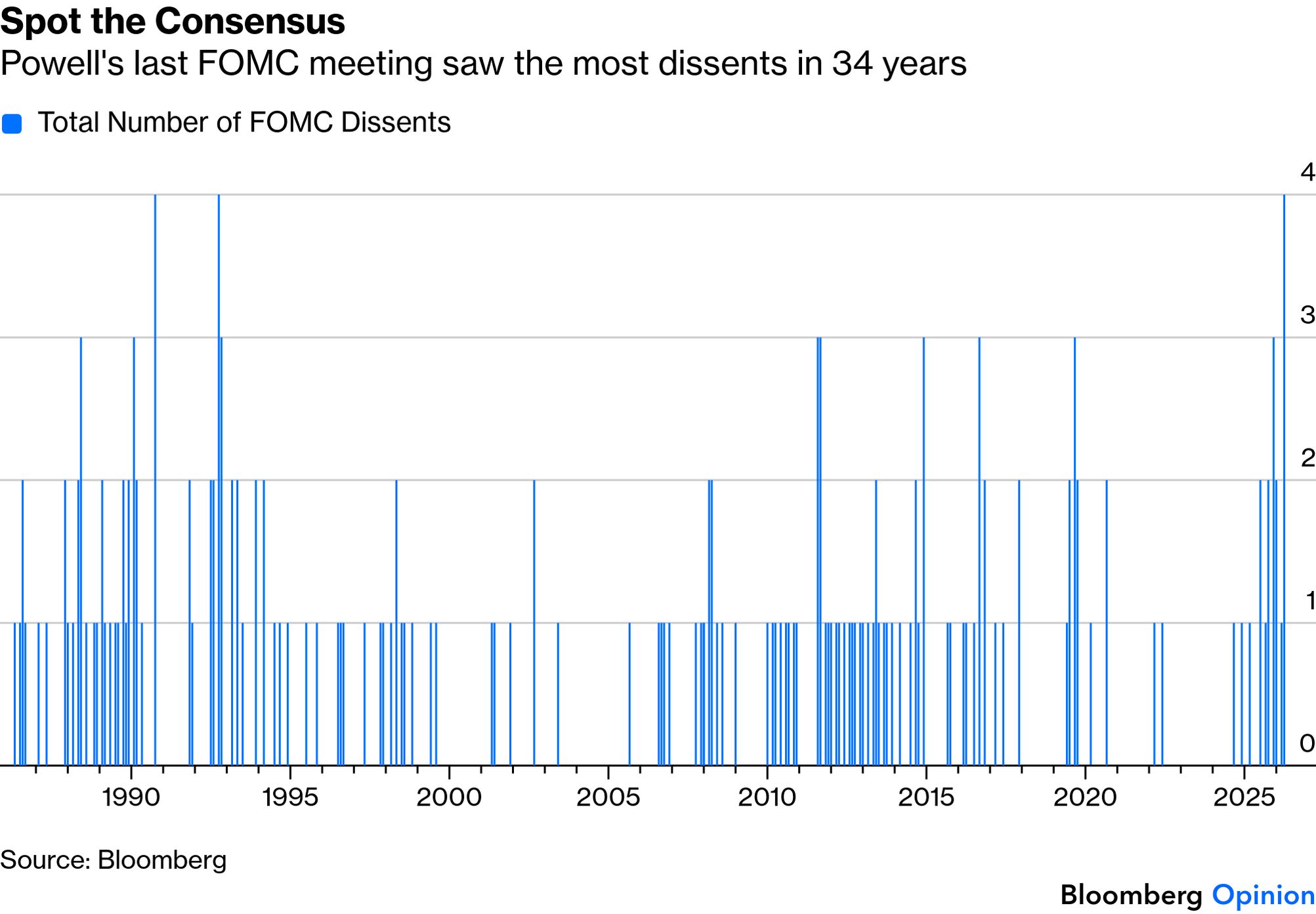

As non-event meetings go, Jerome Powell’s final session chairing the Federal Open Market Committee was spectacular. Rates are unchanged, and so is guidance. But four of the committee’s 12 voters dissented from that decision. Such lack of consensus hasn’t been seen since October 1992, the last FOMC before Bill “It’s the economy stupid” Clinton won the presidency.

So unfazed was Powell by all this dissension that he announced that he’d stay on as a mere governor and member of the committee under successor Kevin Warsh until “it’s appropriate for me to leave.” He isn’t looking to a be a “high-profile dissident”:

My intention isn’t to interfere. I was a governor for almost six years. The tradition is that you work with the chair and you try to collaborate. That’s the attitude I will take.

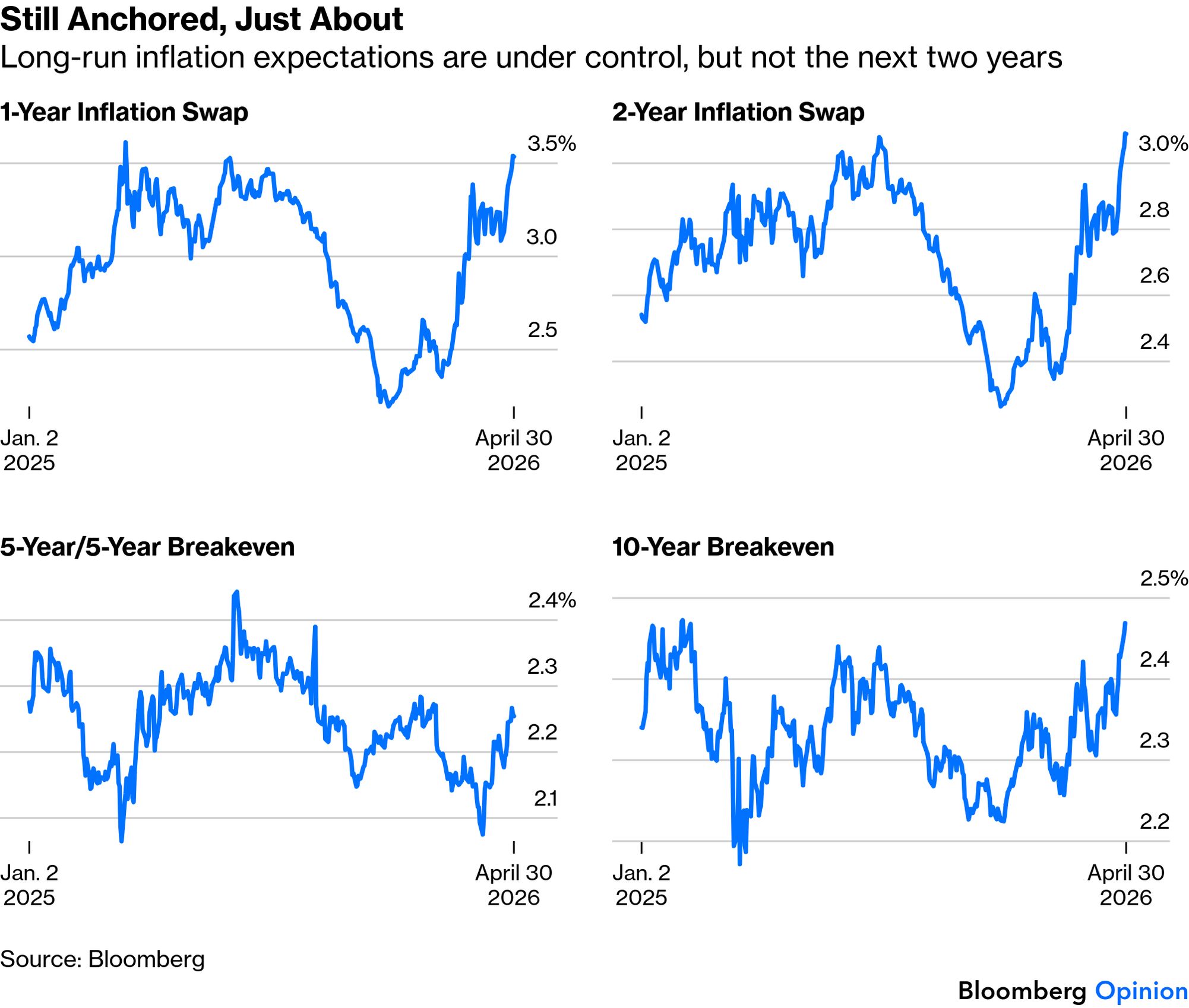

He has two years left in his term as governor, and won’t stand down until the Justice Department’s investigation into his handling of the Fed’s building renovations is “well and truly over, with transparency and finality.” He will judge when that’s appropriate. The thread binding the dissents and Powell’s decision to stay is a determined effort to exert the independence not only of the Fed, but also of the committee’s individual voting members, most of whom now have terms that extend longer than Warsh’s four years as chairman. It will be his job to thrash out a consensus, and that is arguably easier now his new colleagues have shown their positions. If he cannot deliver rate cuts as President Donald Trump wants, he can blame them. Powell defended Fed independence by pointing out that markets trust it to control inflation. Longer-term expectations have indeed remained remarkably stable throughout the shocks of the last few years. However, while the five-year/five-year forecast — reflecting inflation from five to 10 years’ hence and the Fed’s favored measure — remains at only 2.25%, shorter term swaps forecasts are surging upward:

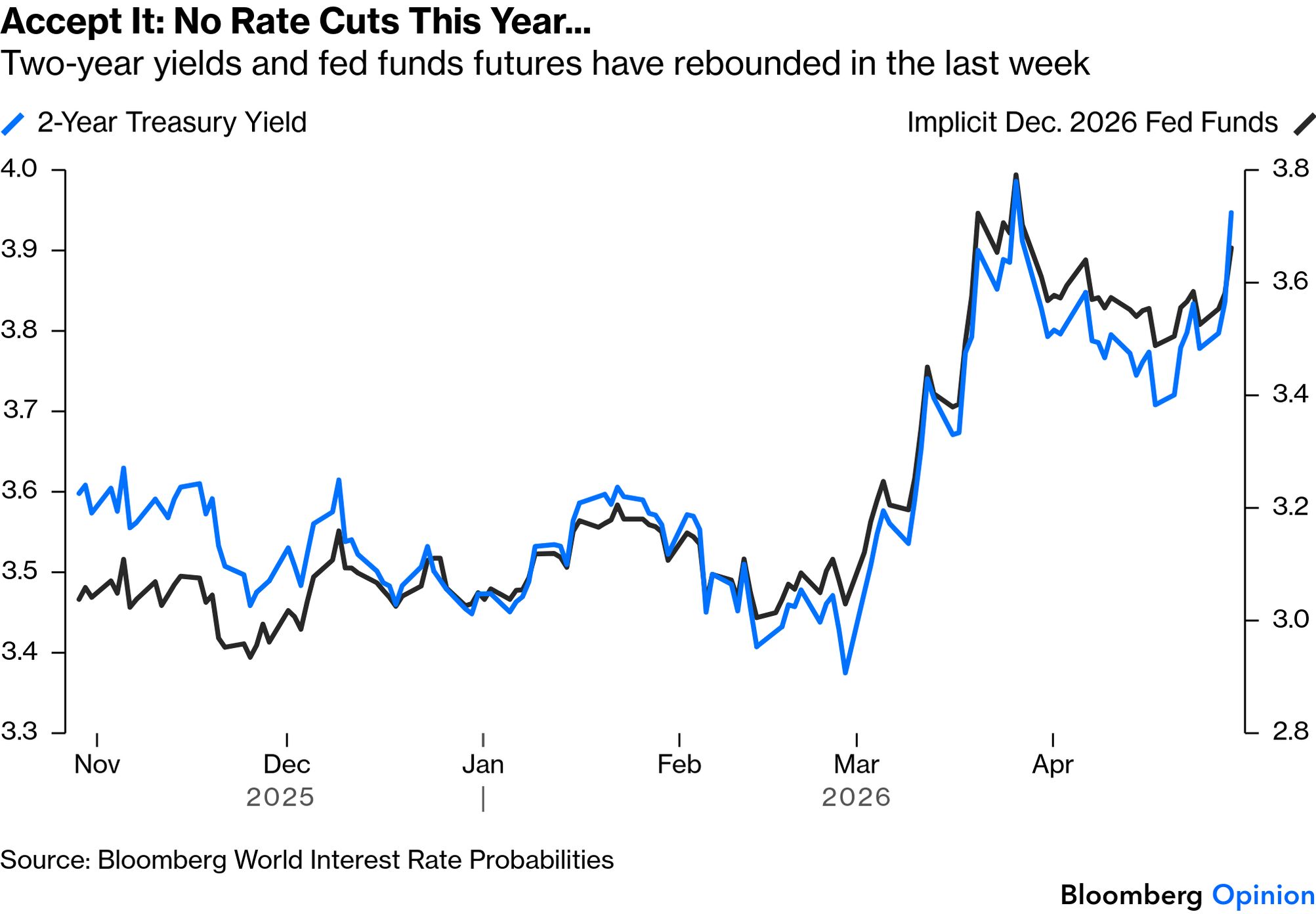

Any discussion of cutting rates this year is moot. Futures markets no longer expect it, while the rate-sensitive two-year yield has surged with rate expectations:

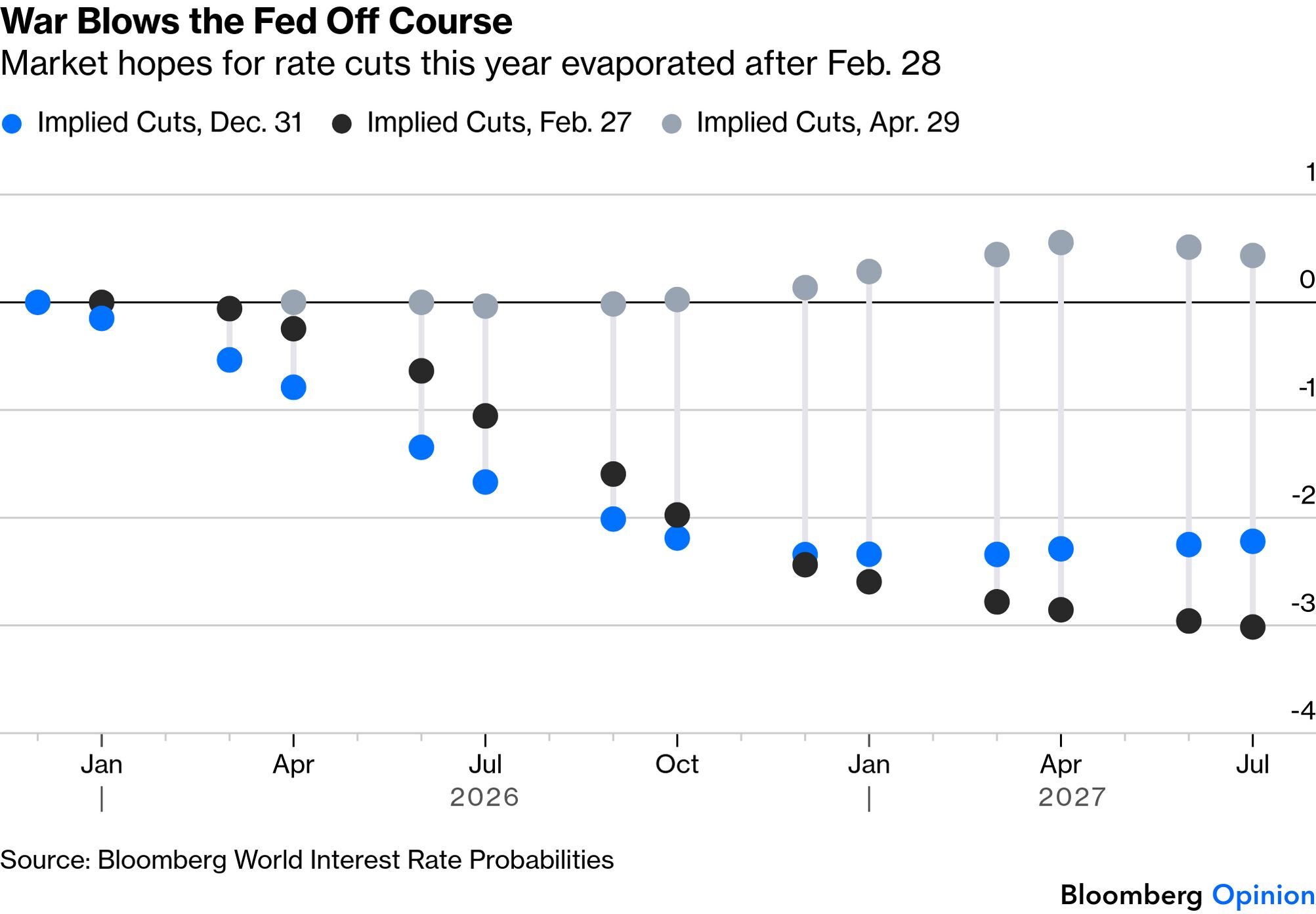

Bloomberg’s World Interest Rate Probabilities function shows how drastically the war blew the Fed off course. On the war’s eve, three cuts were penciled in for 2026:

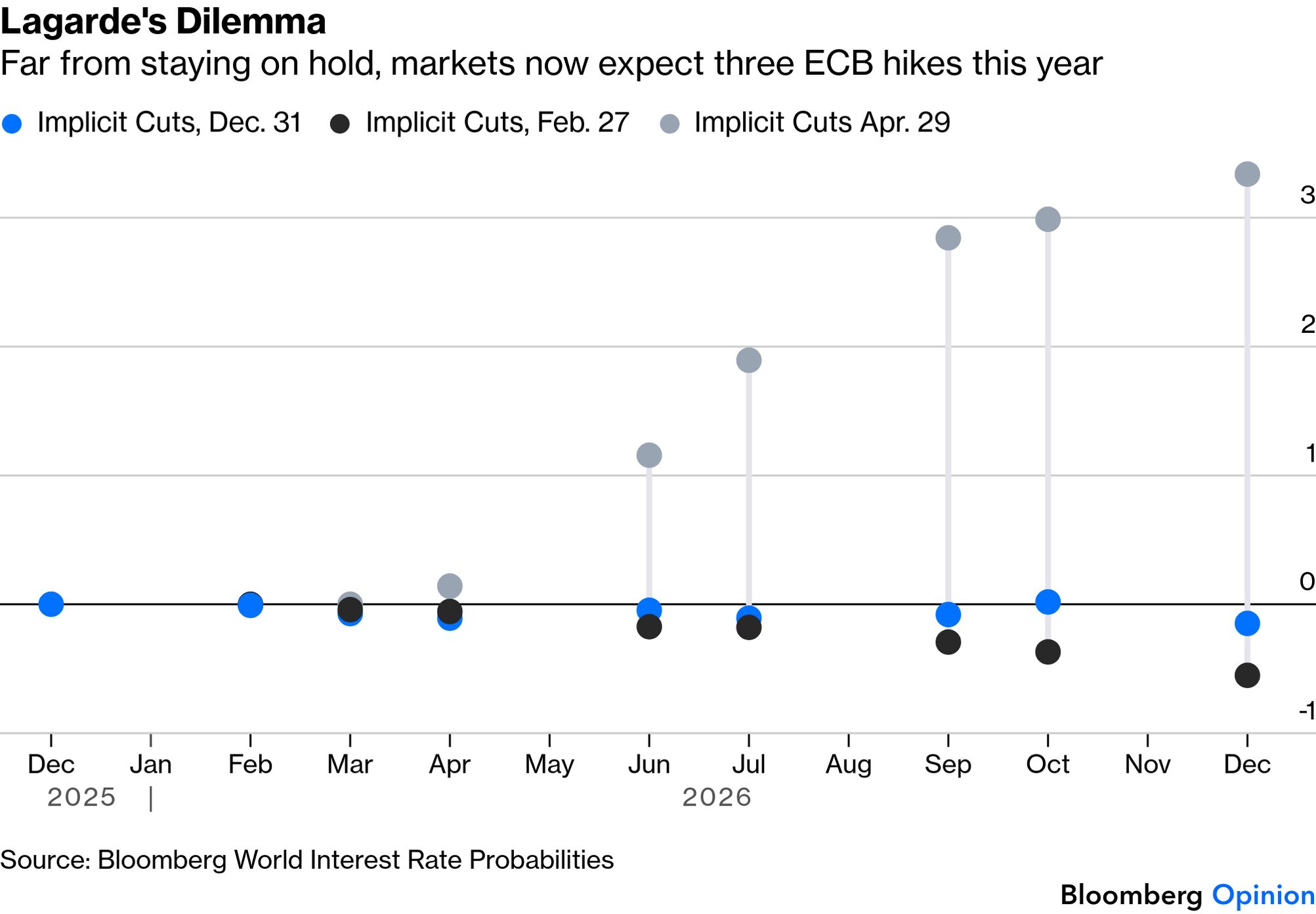

Meanwhile, the European Central Bank, due to make its own announcement shortly after you receive this, is in a tougher spot as Europe is more directly exposed to the conflict. In February, it was expected to leave rates unchanged all year. Now, traders are expecting three hikes, starting in June:

Trump wants rate cuts, but it’s hard to feel sorry. The impasse in the Strait has thwarted any chance of that, while his administration’s brutish attempts to interfere with the central bank appear to have robbed it of the chance to replace Powell with someone more amenable. The committee is now setting out its stall to behave like the Bank of England, where decisions come down to narrow majorities and the governor is sometimes in the minority. That’s not how the Fed has typically operated, but it’s a model that works elsewhere, and the bullying tactics are chiefly responsible. Underscoring the point, Treasury Secretary Scott Bessent attacked Powell for staying on:

It’s highly unusual for someone who says he’s an institutionalist and cares about norms at the Fed. This is a violation of all Federal Reserve norms.

It’s hard to take this seriously. Weaponizing the prosecution system to to get rid of Fed governors you don’t like is a much greater violation of such norms. And the Fed’s building, currently being renovated so controversially, bears the name of Marriner Eccles — a highly respected chairman who stayed on as a governor once he left the chair, just as Powell is planning.

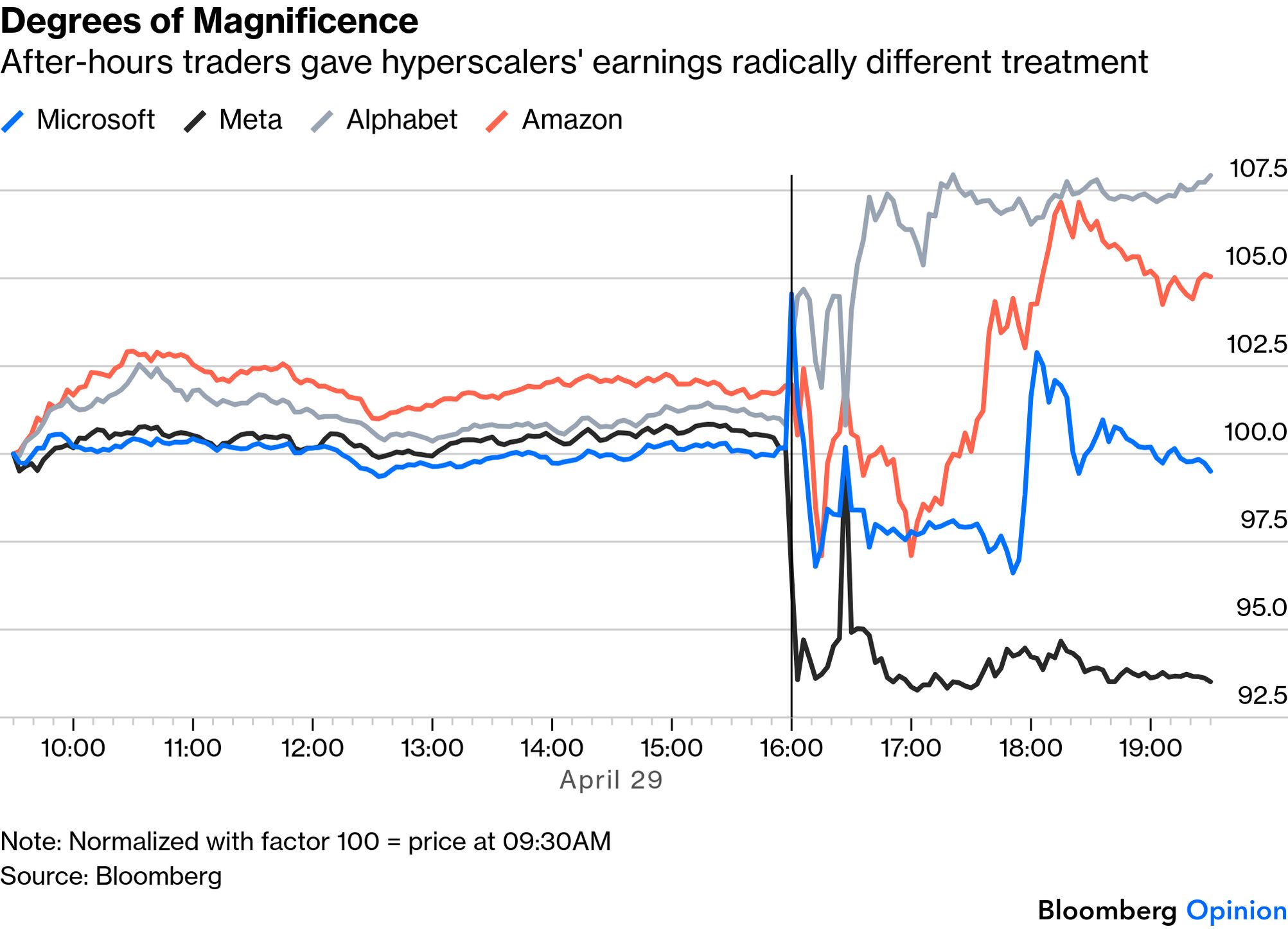

Wednesday’s mega-cap earnings delivered a familiar verdict: margins matter. Investors’ intolerance for unchecked AI-driven capital spending proved a consequential force as the after-hours reports from Meta Platforms Inc., Alphabet Inc., Microsoft Corp. and Amazon.com Inc., together worth nearly $12 trillion, offered a clearer read on the strength and the durability of the AI-driven rally. Alphabet was the biggest winner, after delivering revenues and profits ahead of estimates. It soared by more than 7%, while others weren’t so lucky:

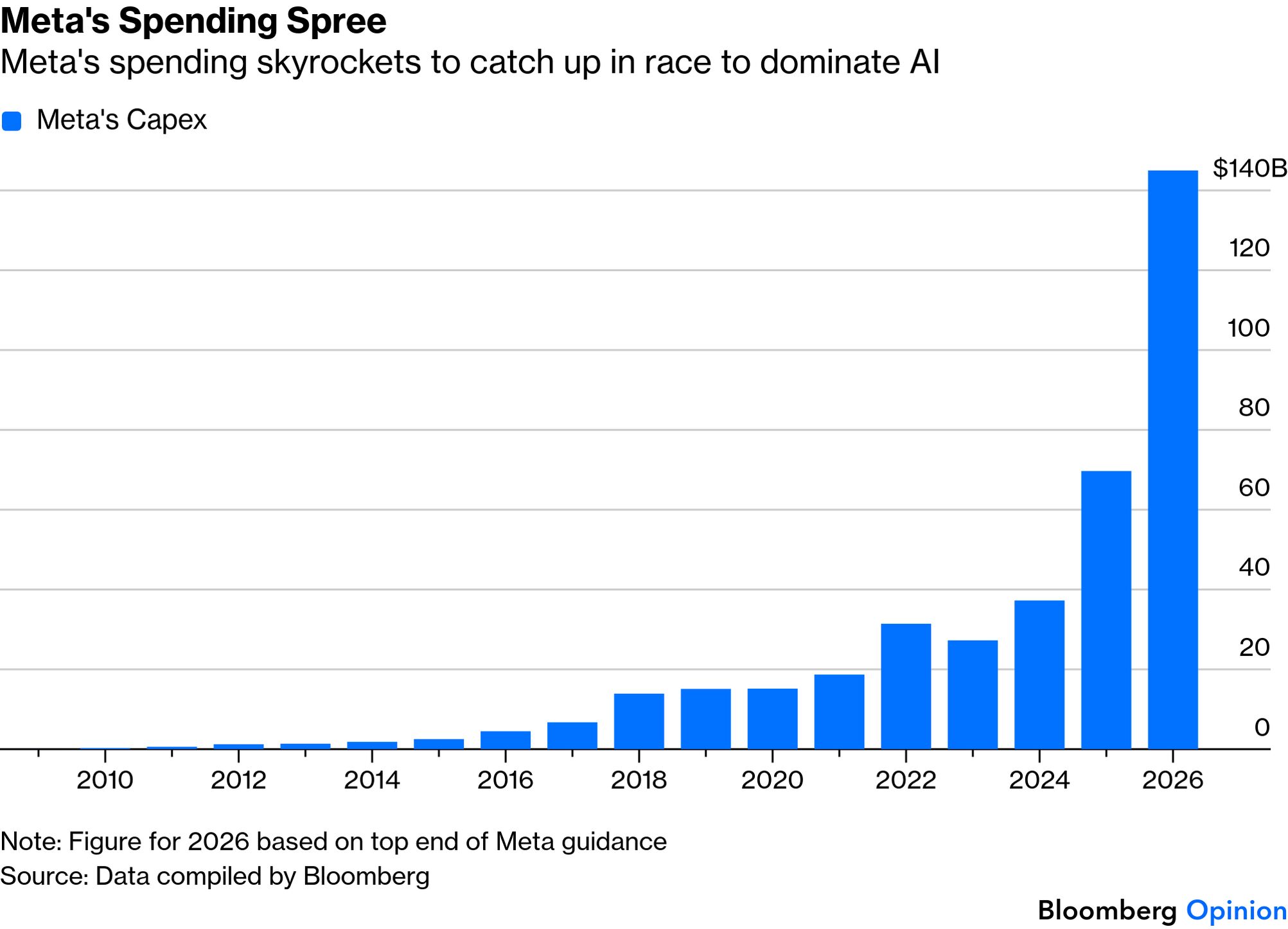

Behind this performance is the conviction that the company’s new generation of custom-designed chips, known as tensor processing units or TPUs, should provide additional tailwind to its artificial intelligence offering. Not only is Alphabet’s flagship AI model, Gemini, powered by these relatively lower-cost chips, but it’s also betting that broader adoption will put it in a position to challenge dominant chipmaker Nvidia Corp. For context, Jensen Huang’s GPUs are designed for general-purpose model training, whereas Alphabet’s chips are optimized for more targeted AI inference tasks like chatbots and agents. The significance of Alphabet’s pivot is underscored by the market reaction to Meta. It has raised spending on the back of “more expensive” components for building out its AI data centers, and now projects capex could top $145 billion this year. That’s up $10 billion from its estimates from three months ago:

This immense splurge didn’t go down well with investors, sending its shares tumbling by almost 7% in after-hours trading. That was despite sales of $56.3 billion, ahead of Wall Street’s estimate of $55.51 billion. To quote Hargreaves Lansdown’s Matt Britzman, “You can't tell from the market reaction, but Meta delivered another very strong quarter, with advertising momentum clearly accelerating.” The key was that the solid results didn’t dispel concern that sustaining growth will come at a rising cost that eats into margins. Whether investors are being too harsh on Meta is difficult to judge. Britzman argues it’s been treated unfairly:

In context, this feels like an overreaction. The increase [in capex] is modest relative to Meta’s existing investment plans, comes alongside unchanged cost guidance, and sits against a backdrop of strong revenue growth and healthy margins.

Other companies received a more nuanced welcome. Take Amazon. It reported $151 billion in property and equipment expenses over the 12 months through March 31, $57.9 billion more than in the same period a year earlier. But investors viewed this favorably because Amazon’s cloud computing business needs to scale up if it’s to make more money. Sales at Amazon Web Services, which make up roughly a fifth of the company’s revenue and most of its operating profit, shot up 28% to $37.6 billion. As the chart above suggests, traders weren’t sure what to make of Amazon. And their varying tolerance for huge spending plans suggests the demand for semiconductors may not be as limitless as the rally in chip stocks implies. We’ll find out soon enough whether these results are enough to keep the rally going in the face of so many headwinds. |