Dear Reader,

Pull up Tesla's most recent SEC filing. Page 5.

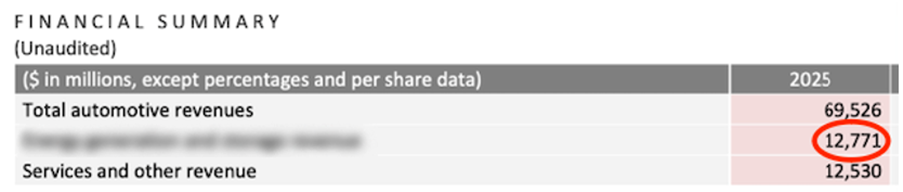

And you'll see a single line showing $12 billion in revenue from a brand-new "super startup" Elon Musk has been quietly incubating inside Tesla.

This new "super startup" has nothing to do with cars, or robots, or space or AI…

But it sits at the center of what Blackstone calls "a $23 trillion investment opportunity."

And on July 22, Elon is expected to pull back the curtain and reveal exactly what he's building.

But former hedge fund manager Adam O'Dell already knows… and he reveals it all in this urgent video.

Adam believes this will go down as Elon's greatest ever invention, and his biggest ever disruption…

And that investors who position themselves before this becomes front-page news could walk away wealthier than they ever thought possible.

Go here to watch Adam's full briefing now... And he'll even give you the name and ticker of one of his top picks to play it — completely free.

Regards,

Adam O'Dell

Chief Investment Strategist, Money & Markets

The Great SPR Arbitrage: An Oil Market Glitch Fuels Sector Gains

By Jeffrey Neal Johnson. Article Posted: 5/14/2026.

Key Points

- Pure-play refiners are positioned to capture expanding margins created by lower input costs and elevated global refined product prices.

- Recent operational upgrades at key facilities have prepared downstream assets for maximum utilization during this period of high demand.

- Integrated energy majors can leverage vast downstream refining capacity to absorb discounted crude and enhance corporate free cash flow.

- Special Report: Elon Musk’s $1 Quadrillion AI IPO

A diplomatic stalemate in the Middle East has effectively taken the Strait of Hormuz offline, removing a critical artery for global crude and refined product flows.

With Brent crude forecasts targeting $95 per barrel, Washington has authorized a 172-million-barrel exchange from the Strategic Petroleum Reserve (SPR) to temper prices ahead of the peak summer driving season. However, this policy move is creating a powerful side effect: a historic arbitrage opportunity for U.S. oil refiners, positioning them for a period of exceptional profitability.

TENGU: The No. 1 AI Tech of the Decade? (Ad)

Starting June 16, This AI Lab Could Take Off Dramatically

Time magazine recently named this lab "the most disruptive company in the world." It's not SpaceX or OpenAI. In fact, its annualized revenues have already surpassed both of these firms. And this 60-year Wall Street legend believes it's gearing up for a watershed product launch that could send its sales soaring even higher starting June 16.

Click here to learn how you can access a "pre-IPO backdoor" into this firm for just $40 a share.The government action gives domestic refiners access to artificially discounted crude inputs. At the same time, geopolitical turmoil has sent the prices of refined products like gasoline and diesel soaring on global markets. This dislocation between input costs and output pricing is dramatically expanding refining margins, creating a powerful tailwind for highly efficient downstream operators.

Cracking the Spread: Crude Into Cash

The core of this opportunity lies in the crack spread, the price differential between a barrel of crude oil and the petroleum products refined from it. With the Hormuz chokepoint disrupting the global supply of middle distillates, these spreads have exploded. Ultra-low sulfur diesel margins recently crested at a record $86.25 per barrel, while the benchmark 3:2:1 gasoline crack spread expanded by nearly 35% through April.

The SPR release amplifies this dynamic. The program is structured as an exchange, loaning oil to refiners who must return it later with a premium. This floods the domestic market with immediate supply, depressing feedstock costs for companies like Valero Energy (NYSE: VLO) and Marathon Petroleum (NYSE: MPC). These businesses are now processing deeply discounted crude and selling the resulting products into a global market defined by scarcity and elevated prices. While integrated majors also benefit, pure-play independent refiners are best positioned to capture this direct margin expansion.

Valero Energy: Primed for Peak Performance

Valero Energy has demonstrated strong operational leverage, with its stock price rising nearly 50% year to date.

The refiner posted first-quarter earnings per share (EPS) of $4.22, beating the $3.16 consensus estimate.

This performance underscores Valero Energy's ability to capitalize on favorable market conditions.

Management's confidence in sustained cash flow is evident in its recent capital allocation decisions. Valero Energy raised its quarterly dividend by 6% to $1.20 per share, signaling an optimistic outlook.

Further enhancing its potential, Valero Energy is on track to complete a significant optimization project at its St. Charles refinery's fluid catalytic cracking (FCC) unit in the third quarter. This upgrade is timed to expand the output of high-value products just as global fuel inventories remain under severe pressure. The market appears to be pricing in this sustained earnings power, with Valero Energy's forward price-to-earnings (P/E) ratio compressing sharply from a trailing multiple of about 17.6 to 8.7.

Marathon Petroleum: Ready for the Ramp-Up

Marathon Petroleum has been another key beneficiary of the current environment, delivering a 55% year-to-date return for shareholders.

Its first-quarter results included a significant EPS beat, reporting $1.65 against a consensus of just 74 cents.

An active $5 billion share repurchase authorization further supports the stock's downside, reflecting Marathon Petroleum's commitment to returning capital to shareholders.

Crucially, Marathon Petroleum recently completed a major overhaul of its hydrotreater at its massive 631,000-barrel-per-day Galveston Bay refinery. With this extensive maintenance now complete, the facility is positioned for maximum utilization.

This operational readiness enables Marathon Petroleum to fully leverage discounted SPR barrels and process them into high-margin distillates for a supply-starved global market. Similar to its peer, Marathon Petroleum's valuation reflects market expectations for windfall profits, with its forward P/E ratio tightening to 8.6 from a trailing P/E of 16.2. Options market data reinforces this bullish sentiment, showing a distinct skew toward out-of-the-money call volumes for June and July contracts.

ExxonMobil: Scale as a Strategic Weapon

While pure-play refiners offer the most direct exposure to expanding crack spreads, ExxonMobil's (NYSE: XOM) integrated model provides a more diversified, though still potent, way to leverage the trend.

ExxonMobil's stock price is up over 25% year to date, supported primarily by the strength in its upstream exploration and production business, which directly profits from higher baseline crude prices.

However, its downstream operations represent a significant and underappreciated asset in the current landscape. The recently expanded Beaumont, Texas, refinery owned by ExxonMobil now processes over 630,000 barrels per day.

The Beaumont refinery's enormous capacity acts as a strategic sponge, allowing ExxonMobil to absorb vast quantities of cost-advantaged SPR crude. This downstream leverage provides a powerful hedge, bolstering corporate free cash flow and insulating earnings even if macro headwinds were to slow the appreciation in benchmark crude prices.

ExxonMobil's 2.72% dividend yield adds another layer of stability for risk-averse investors.

From Boom to Bust? What Could Derail the Rally

The bullish thesis for refiners is tied directly to the persistence of current geopolitical and supply chain dynamics. A sudden diplomatic breakthrough reopening the Strait of Hormuz would quickly deflate the geopolitical risk premium baked into refined product prices, normalizing crack spreads.

Furthermore, investors should consider macroeconomic risks. Should aggressive inflation-fighting measures trigger a sharper-than-expected economic slowdown, the resulting demand destruction for transportation fuels could pressure margins from the top down, offsetting some of the benefits of lower feedstock costs.

Finally, if gasoline prices remain elevated at the pump, refiners could face policy risk in the form of a potential windfall profits tax, which could be debated in Washington as a measure to appease consumers.

A Unique Market Dislocation Opportunity

The combination of a geopolitical supply shock and a strategic government inventory release has created a rare and powerful earnings catalyst for the U.S. refining sector. The data indicates that operators with significant, efficient, and operationally ready downstream assets are in a prime position to convert this market dislocation into substantial free cash flow.

Investors looking for direct exposure to this arbitrage opportunity might consider adding the operational leverage of pure-play refiners Valero Energy and Marathon Petroleum to their watchlists. Those who prefer a more diversified approach that still captures the downstream tailwinds while also benefiting from strong upstream performance may find ExxonMobil's integrated scale a compelling alternative.

Why Trump’s Amazon Stock Sale May Not Matter at All

By Sam Quirke. Article Posted: 5/19/2026.

Key Points

- President Trump recently disclosed selling Amazon stock earlier this year, but the move likely says far more about portfolio reallocation than a worsening outlook for Amazon’s prospects.

- The stock’s core investment thesis continues strengthening thanks to AWS reacceleration and growing AI demand.

- With shares holding near their recent all-time highs and analysts still calling for major upside, the case for buying and holding is hard to ignore.

- Special Report: Elon Musk’s $1 Quadrillion AI IPO

While shares of Amazon.com Inc (NASDAQ: AMZN) have cooled slightly over the past two weeks after an explosive rally through April, they’re still holding onto most of those gains and remain just below their recent all-time high.

That resilience comes despite a headline last week that might have rattled many investors at first glance: Donald Trump recently disclosed that he sold Amazon stock back in February.

TENGU: The No. 1 AI Tech of the Decade? (Ad)

Starting June 16, This AI Lab Could Take Off Dramatically

Time magazine recently named this lab "the most disruptive company in the world." It's not SpaceX or OpenAI. In fact, its annualized revenues have already surpassed both of these firms. And this 60-year Wall Street legend believes it's gearing up for a watershed product launch that could send its sales soaring even higher starting June 16.

Click here to learn how you can access a "pre-IPO backdoor" into this firm for just $40 a share.On the surface, that naturally raises questions. Whenever a high-profile public figure reports selling a major stock like this, investors are right to wonder whether it signals fading confidence or some deeper concern about the company’s outlook. In Amazon’s case, however, the evidence suggests they probably shouldn’t read too much into the move.

In fact, when you zoom out and focus on the underlying business fundamentals rather than the headline itself, Amazon still looks like one of the strongest mega-cap setups in the market today. The question now is whether investors should pay attention to the disclosure at all, or whether Amazon’s improving outlook matters far more. Let’s jump in and take a closer look below.

The Trump Sale Looks Dramatic, But Context Matters

The first thing investors need to understand is that Amazon was not the only stock involved in the disclosure. Reports showed that Trump’s transactions from last quarter included both sales and purchases across a broad range of equities, including other large-cap tech stocks.

That context matters because it makes the transactions look far less like a targeted bearish call against Amazon specifically and far more like general portfolio management. For example, he also unloaded part of his position in Meta Platforms, Inc (NASDAQ: META), while buying the likes of ServiceNow (NYSE: NOW), NVIDIA Corp (NASDAQ: NVDA) and Broadcom Inc (NASDAQ: AVGO).

While the stock had been selling off around the same time, spooking investors with its rising capital expenditure plans, there’s little evidence that the sale from last February reflected a worsening view from Trump on Amazon’s longer-term prospects. If anything, he may be wishing he’d held onto the stock a little longer, as it’s only gone from strength to strength since then.

Last month’s report largely silenced concerns about soaring capex, and investors are increasingly convinced that the company’s aggressive spending plans will pay off.

AWS Is Becoming the Main Driver Again

One of the most obvious ways this is playing out right now is in AWS. Sure, for a period last year, there were concerns about AWS’s growth trajectory and the increasing competition in the AI infrastructure race. However, those concerns now appear increasingly outdated.

Recent commentary from Jefferies suggests AWS is still in the early stages of a reacceleration as additional capacity comes online and long-term AI partnerships start delivering revenue. That’s exactly the kind of commentary investors want to hear because it reinforces the idea that all of Amazon’s AI spending, and there is a lot of it, is beginning to translate into real results.

The Stock Still Has Many Tailwinds

Importantly, while the recent cooling in Amazon shares might make Trump’s selling look justified, there’s a stronger argument that it’s actually healthy. Having surged sharply through April and into the start of May, the stock was technically in extremely overbought territory. That made it difficult to chase an entry, as there’s always a risk a rally becomes unsustainable without some volatile profit-taking.

With that pressure now easing, the technical setup has improved considerably for those thinking about getting involved. In other words, Amazon appears to have digested its recent rally while still holding onto most of its gains.

The broader market backdrop also remains supportive. While equities in general have been cooling over the past week, investor appetite for high-quality AI and cloud infrastructure names remains extremely strong. As we’ve been highlighting, Amazon has done well to position itself directly in the center of those themes.

Wall Street’s outlook reinforces that optimism. The folks at TD Cowen reiterated their bullish stance last week with a fresh $350 price target, implying as much as another 30% upside. This echoed similarly bullish ratings earlier this month from the likes of BNP Paribas and New Street Research.

Should Investors Follow Trump and Sell?

Right now, there is little evidence suggesting they should. Trump’s disclosed Amazon sale from last February may generate headlines, but a lot has happened since then—almost all of it positive.

AWS growth is improving, AI demand remains robust, the stock’s technical setup has normalized, and Wall Street still sees considerable upside from current levels.

Of course, risks remain. Amazon’s valuation is no longer cheap, expectations are high, and any slowdown in AI infrastructure demand could pressure sentiment quickly. Until that starts happening, however, investors have far more important things to focus on than who happened to sell some shares three months ago.

to bring you the latest market-moving news.

This email message is a sponsored message provided by Banyan Hill Publishing, a third-party advertiser of TickerReport and MarketBeat.

If you would like to unsubscribe from receiving offers for Strategic Fortunes, please click here.

Contact Us | Unsubscribe

© 2006-2026 MarketBeat Media, LLC dba TickerReport.

345 N Reid Place, Sixth Floor, Sioux Falls, S.D. 57103-7078. U.S.A..

No comments:

Post a Comment