|

Let’s get the naked self-publicity out of the way. A video from the day after Liberation Day, explaining the absurdity of the formula behind the “reciprocal” tariffs, has been nominated for a Webby award. It’s decided by public vote, which closes Friday, and we’d love your support. We’re currently running in second out of five nominees. You can vote here. And thank you!

Back in the 1950s, a young Peter Sellers got his first big break in The Goon Show on the BBC. An even younger King Charles III was one of the absurd radio program’s biggest fans. One episode, The Dreaded Batter Pudding Hurler (of Bexhill-on-Sea), included this immortal dialogue. Our heroes are navigating their warship, with Eccles keeping watch:

Eccles:

Mine ahead woohoowoo! Dirty big mine ahead!

Bloodnok:

Mine...?

Eccles:

Here, there's no need to worry fellas about the mine! It's one of ours!

FX:

[Explosion]

Eccles:

Oooh!

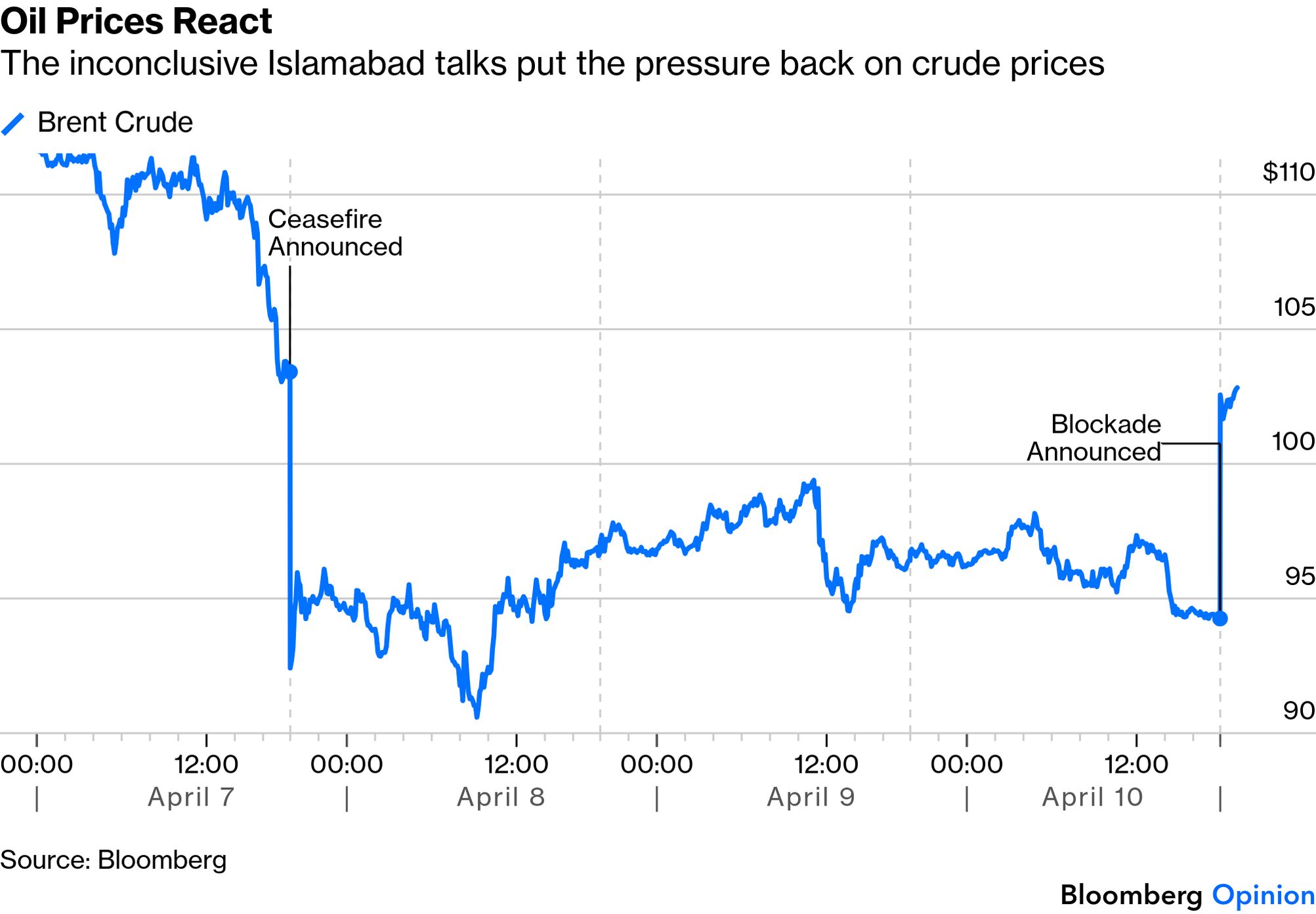

To my chagrin, I can’t find the audio for it. But the relevance is clear. This weekend, the US and Iran spent 21 hours in Islamabad negotiating to end their war without a deal. Iran’s control over the Strait of Hormuz, which has created a severe oil supply shock, was a critical stumbling block. In response, the US will itself blockade the Strait. This isn’t as absurd as the Goons. Iran has kept its own tankers moving through the bottleneck, and anything that changes that would be a serious blow to its already ailing economy. And in the longer run, with an agreement far off, the best hope for a reasonably swift resumption of the flow of oil is for the US to reopen the Strait by force. A blockade might hasten that. Andrew Bishop of Signum Global Advisors puts the strategic logic as follows:

If one thinks about the Strait of Hormuz (extremely simplistically) as currently being divided into two halves – the half controlled by Iran’s toll-booth system, and the half that is “mined” – the US’s plan seems to be to close off the former and work to reopen the latter (via demining, confidence-building, insurance backstops, navy escorts, etc.) until Iran concedes politically and the entire Strait can reopen without the need for artificial support.

This is not a dumb policy. It’s unlikely, however, to avert a resumption of hostilities. The war, and the interruption to supply, will likely escalate before they improve. In the short run, international markets are in a similar position to the Goons. It doesn’t much matter whose mines or warships are blocking the Strait; the point is that the oil isn’t coming through and supply remains interrupted. Hence the emphatic reaction of Brent crude prices once Asian trading reopened on Monday:

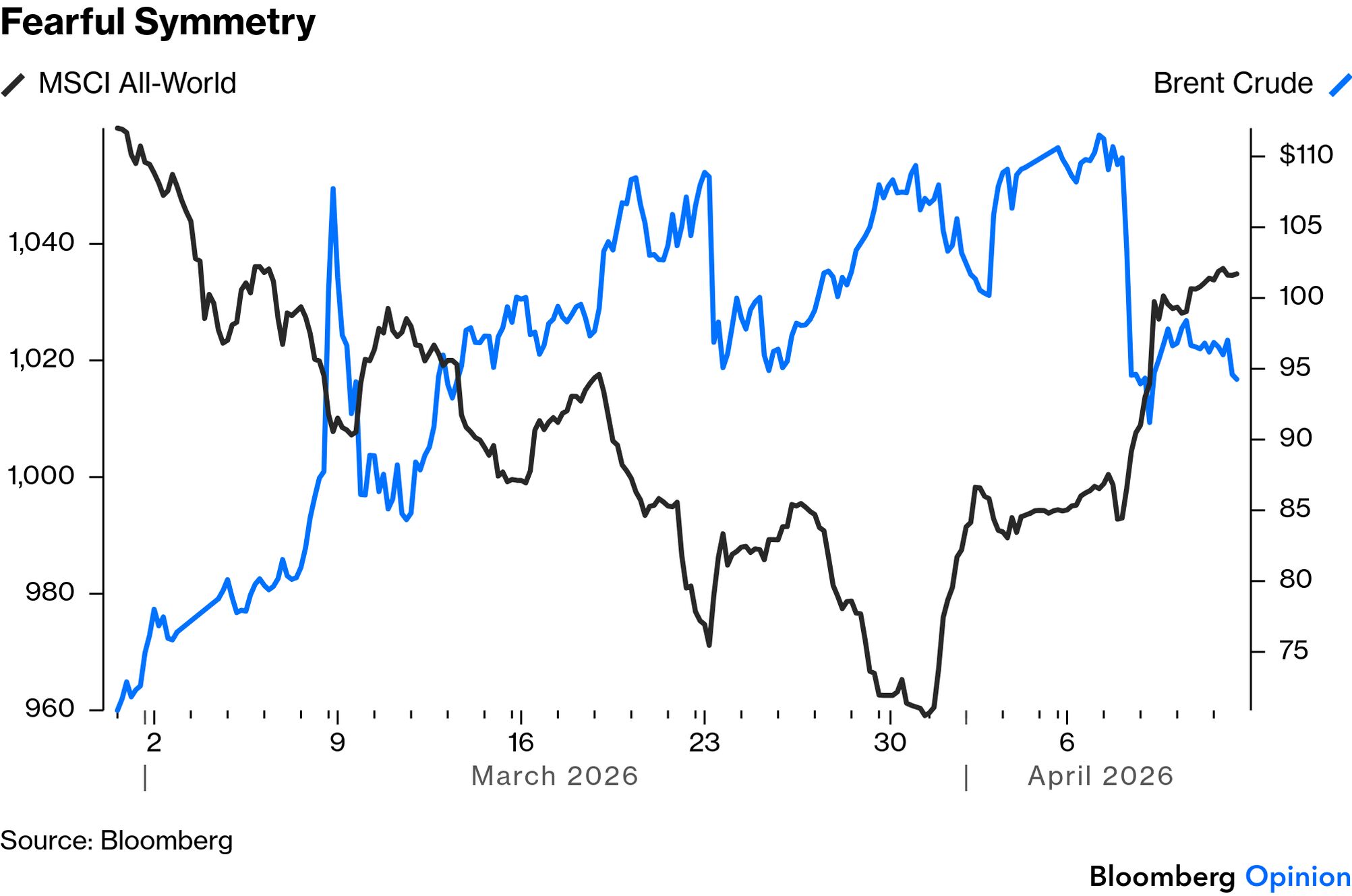

From this, it’s a fair bet that share prices will feel downward pressure once global bourses reopen. Since the war began, crude and equity indexes have been as symmetric as a Greek urn, with rises in oil driving falls in stocks and vice versa:

It’s not just stocks. With the interesting exception of Bitcoin, virtually all risk assets have had a significant negative correlation to the Brent price over the last six weeks. Some questions as another week dawns:

- How quickly and effectively can the US apply its blockade? (It’s an ambitious operation).

- Do US allies collaborate in the effort? (That improves chances of success but also escalates risk).

- Does Iran retaliate?

- Will China, which stands to be most affected by a block on Iranian oil exports, be moved to put pressure on the Iranians?

First-quarter earnings get started this week. There are plenty of other things that could move prices. But for now, the Iranian situation and the oil price still matter more than anything else. No matter whose mines are in the Strait.

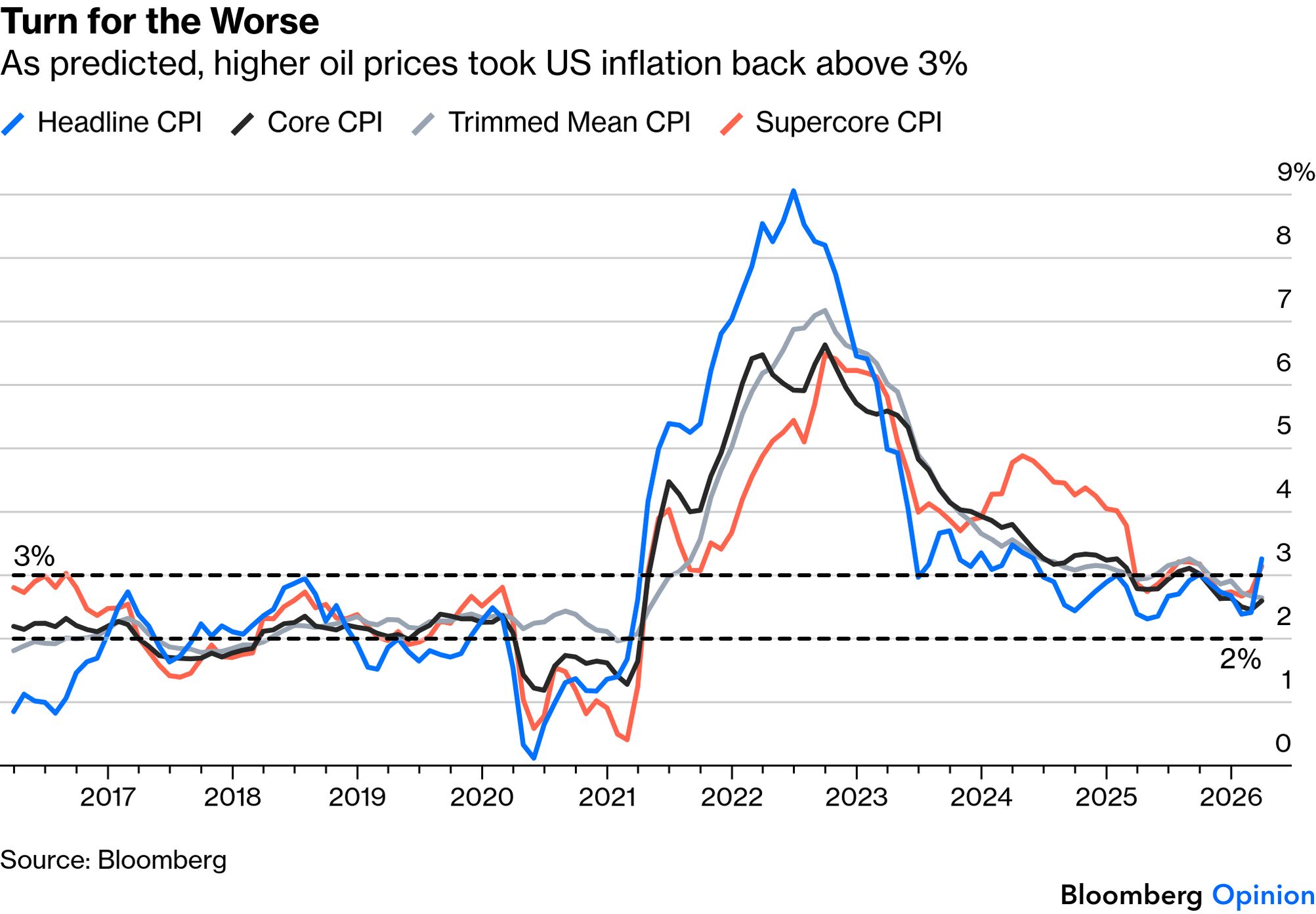

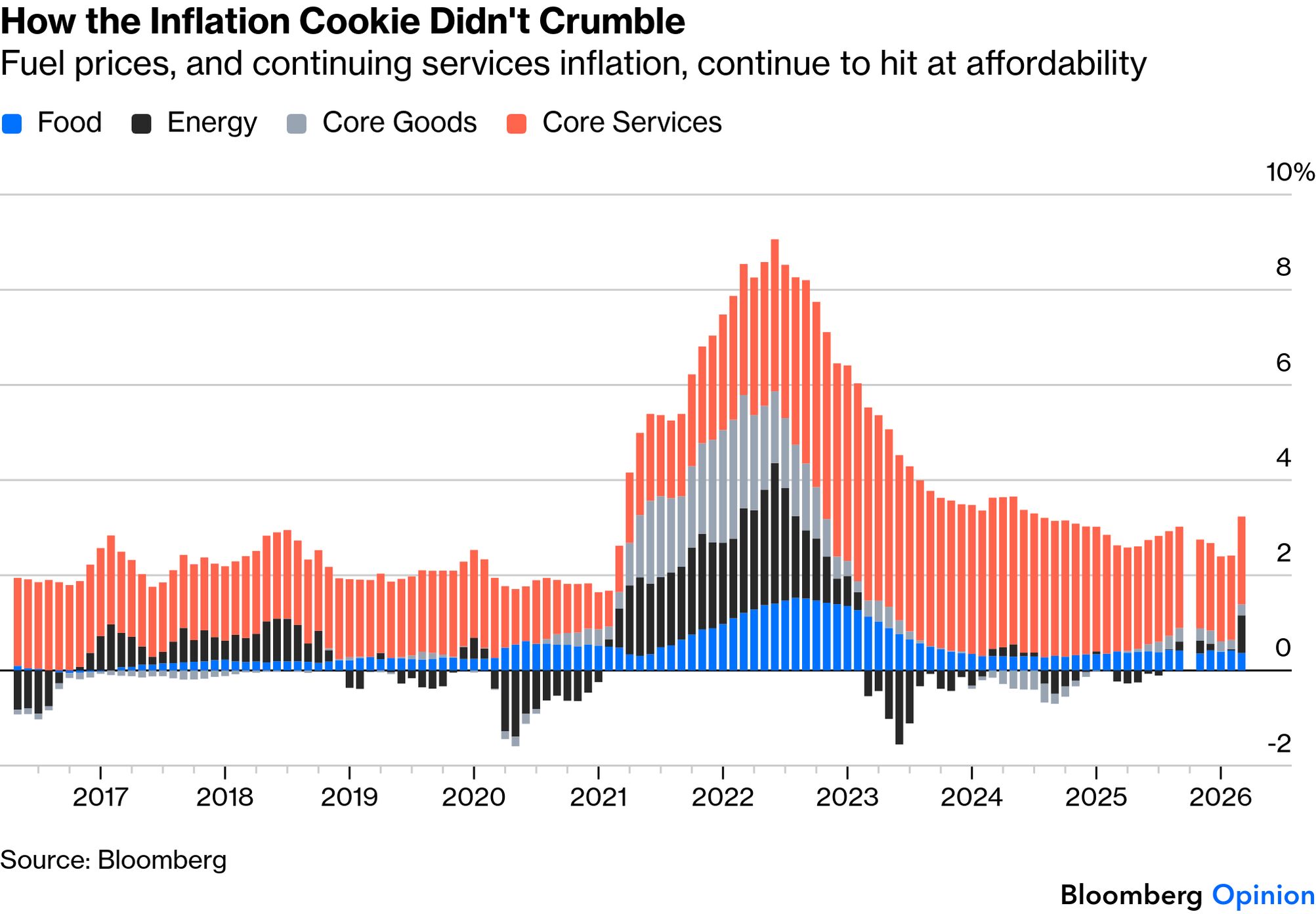

One critical factor limiting the US bargaining position: affordability. Unlike their Iranian opponents, they have voters to worry about who made it clear at the last election that high inflation was a serious problem for them. Publication of US consumer price inflation data for March has now confirmed that the spike in gasoline prices has indeed taken the headline to its highest level in more than two years, and back above the Federal Reserve’s upper-range target of 3%:

Neither the trimmed mean CPI (where the biggest outliers are stripped out and the rest are averaged) nor the core, excluding food and fuel, topped 3%. Tariffs are still not having anything like the severe effect on goods prices that many of us expected, and higher oil is not yet having a secondary impact on other prices. But the Fed’s own “supercore” (services inflation excluding shelter) has also ticked up, which is unwelcome. And a standard breakdown of inflation into its four main components reveals that all are rising. This isn’t disastrous, but it’s certainly not good:

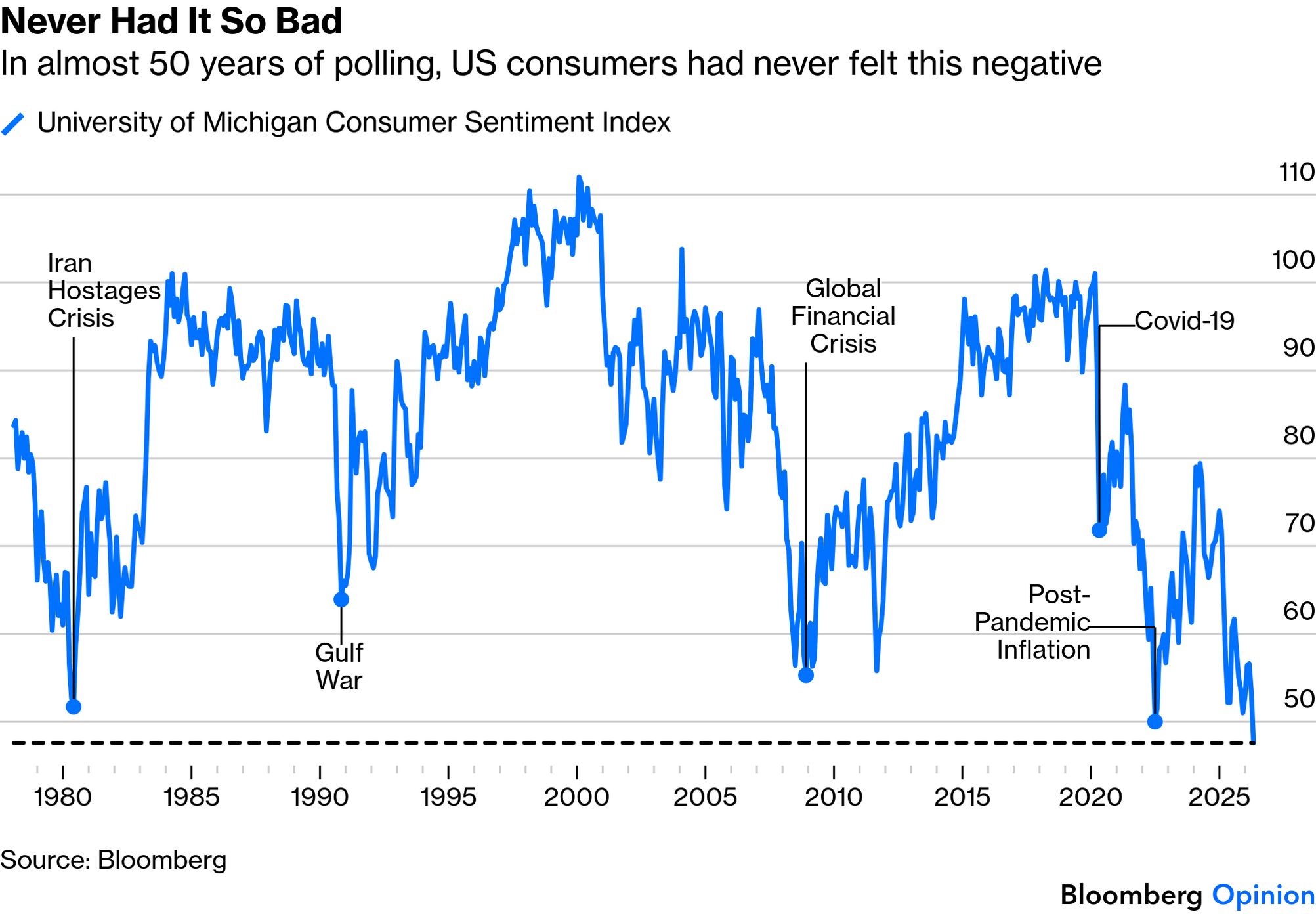

Further, it should be clear to politicians that this is making people really, really unhappy. The University of Michigan has been polling consumers on their sentiment since 1978. They have never before been as negative as they are now:

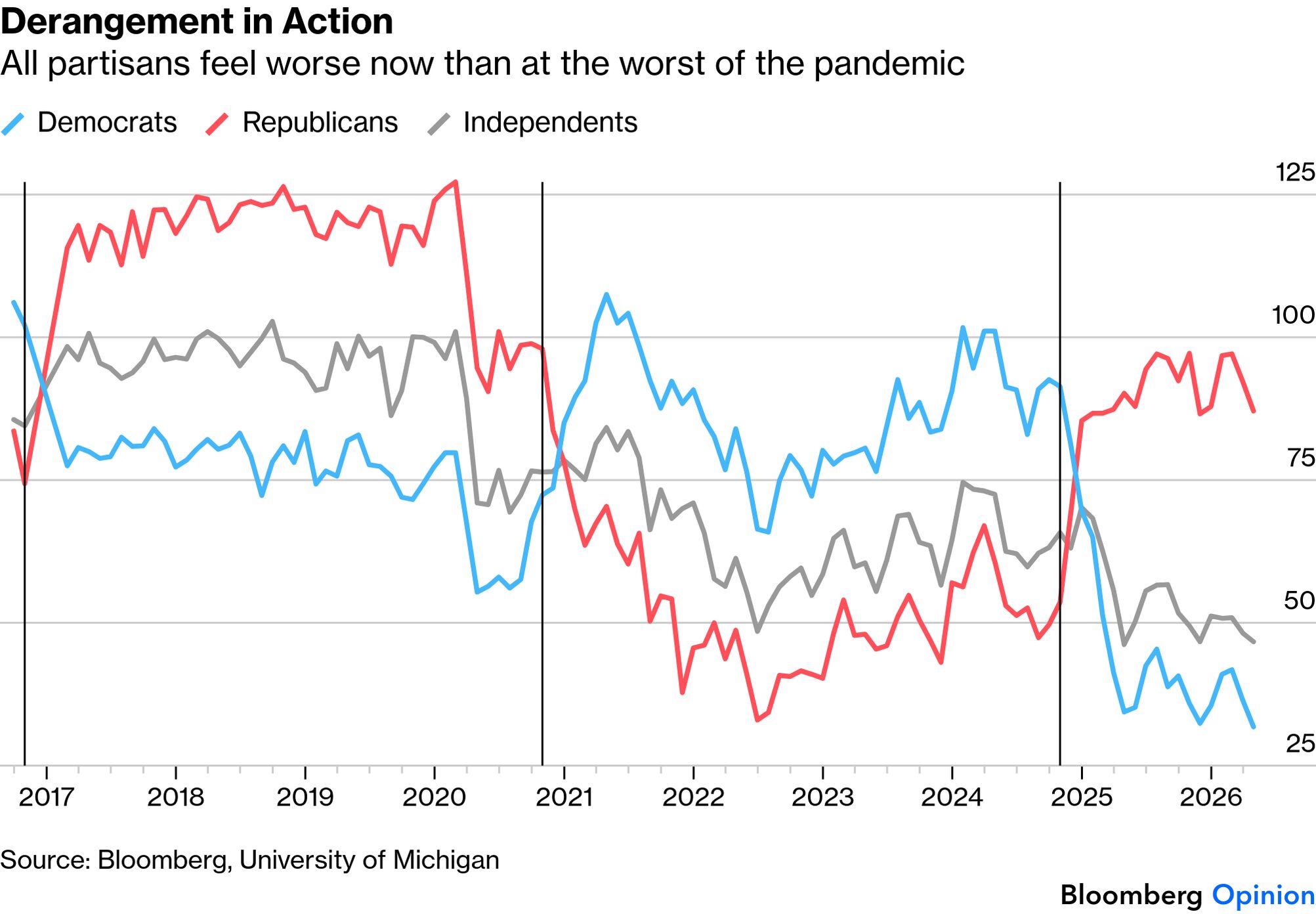

Despite many measures of the economy remaining robust, apparently people feel worse than they did during the hostage crisis of 1980 or the Iraqi invasion of Kuwait 10 years later, two previous occasions when the Gulf came to dominate debate. They’re more morose than at any time during the Covid pandemic. Some of this can be attributed to political polarization, the curse of the age. Michigan has been tabulating results by political identity since 2016, and both Democrats and Republicans obviously allow their ideology to color their assessment of the economy. The negativity is extreme among Democrats, but as Republicans say they feel worse than at any time during the pandemic — until Joe Biden won the 2020 election — there’s little comfort for the administration:

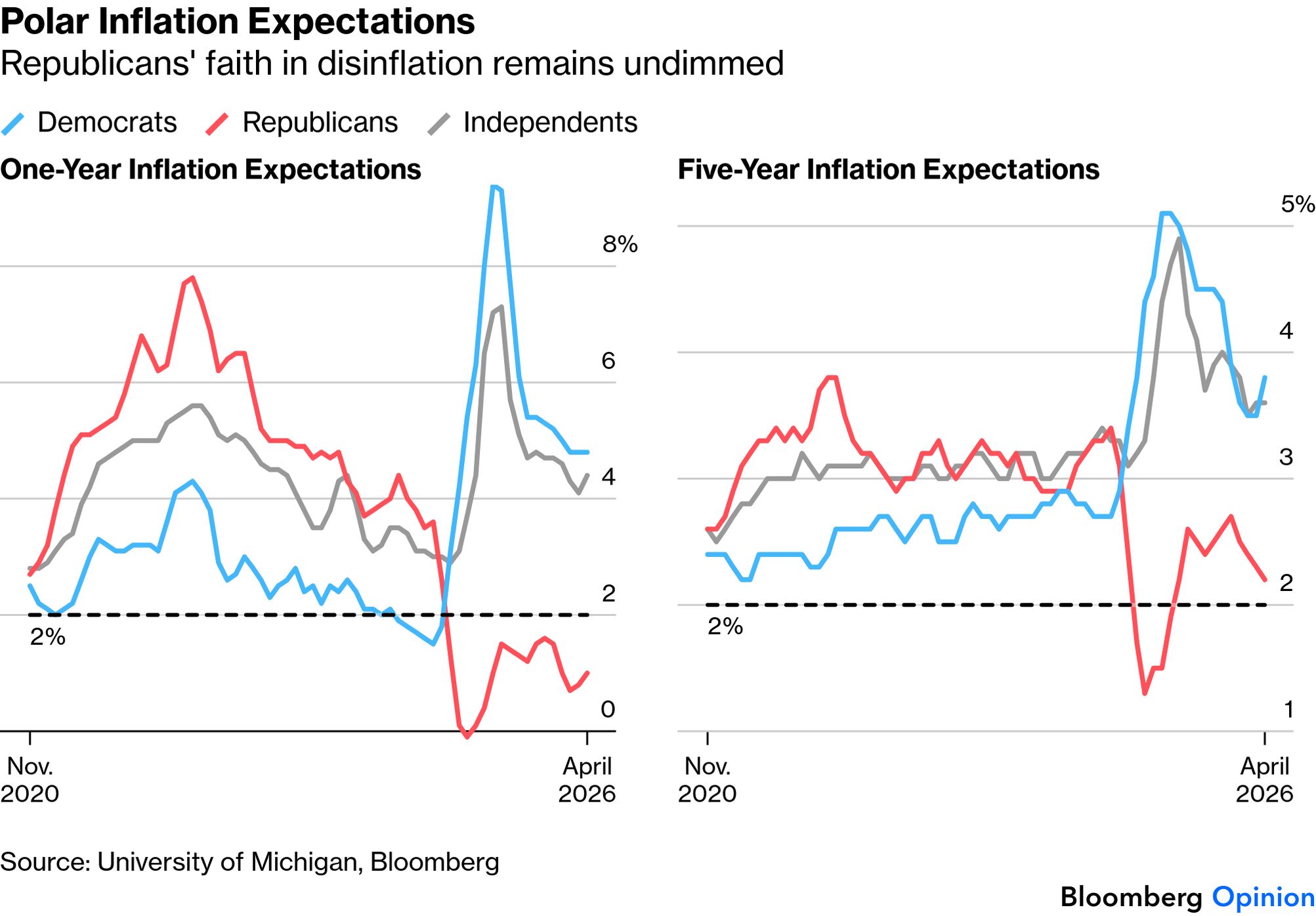

Inflation expectations are also hugely influenced by partisanship, although there is some encouragement from the way that the first month of the war has had little impact on forecasts either over the next year or the longer term:

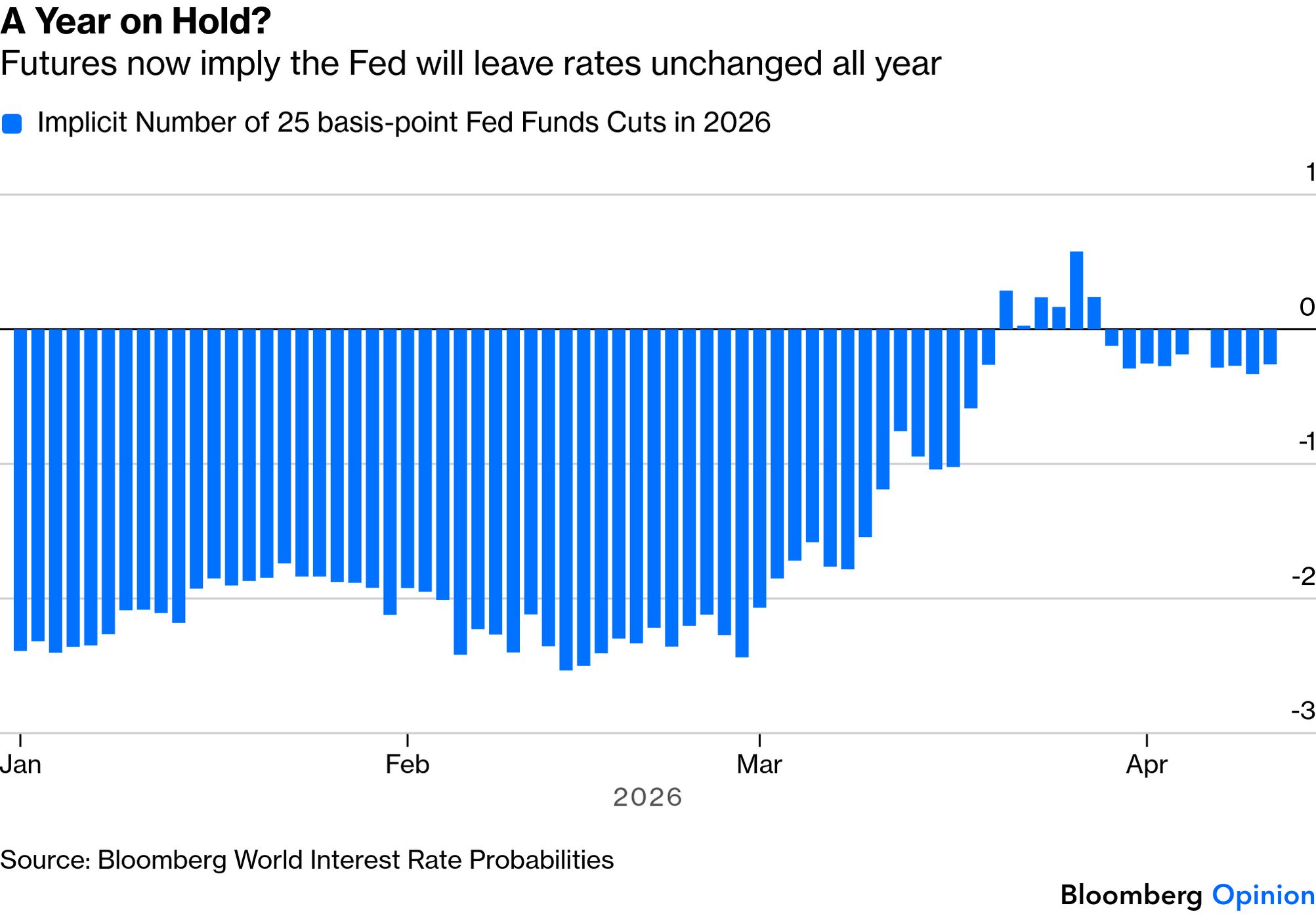

The critical question remains unanswered. Does the Strait remain blocked long enough to cause a spillover into higher prices in other products as companies pass on their higher energy bills? The chances of this dropped last week, and have risen again after the failed talks in Islamabad. For the Fed — due to have a new chairman next month, who is yet to be confirmed by the Senate — the expectation is that rates will be forced to stay on hold:

Seeing this, Washington will want to end the blockade quickly. The main reason is that it needs lower mortgage rates to make houses affordable.

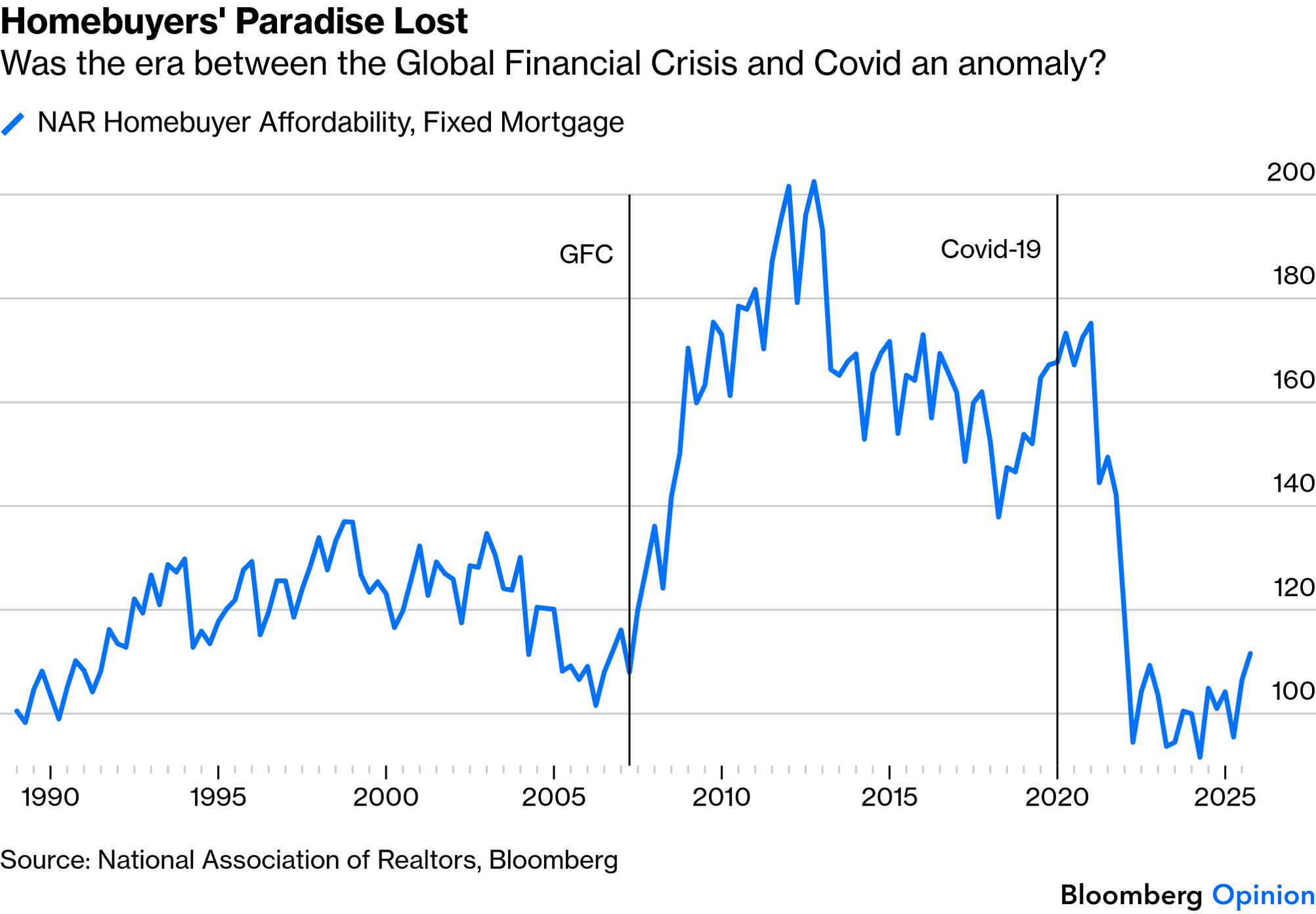

After the post-pandemic rate hikes, and then a Fed easing cycle disrupted by tariff brinkmanship, the war in Iran has offered homebuyers another reason for alarm by sending mortgage rates up again.

The question now is whether the low-rate environment before the pandemic, which allowed many to lock in rates that they don’t want to relinquish by moving house, was an anomaly. That would imply that higher rates are the new normal:

The fragile ceasefire helped last week’s slight decline in rates. But to unlock pent-up demand, they would have to trend downward sustainably, and it’s hard to see that happening while the fog of uncertainty remains. It’s not surprising that prospective homeowners are staying on the sidelines. A measure of mortgage applications throughout March fell by more than 10%. Treasury yields edged down slightly with the ceasefire, but Capital Economics’ Thomas Ryan sees little chance for a lasting relief :

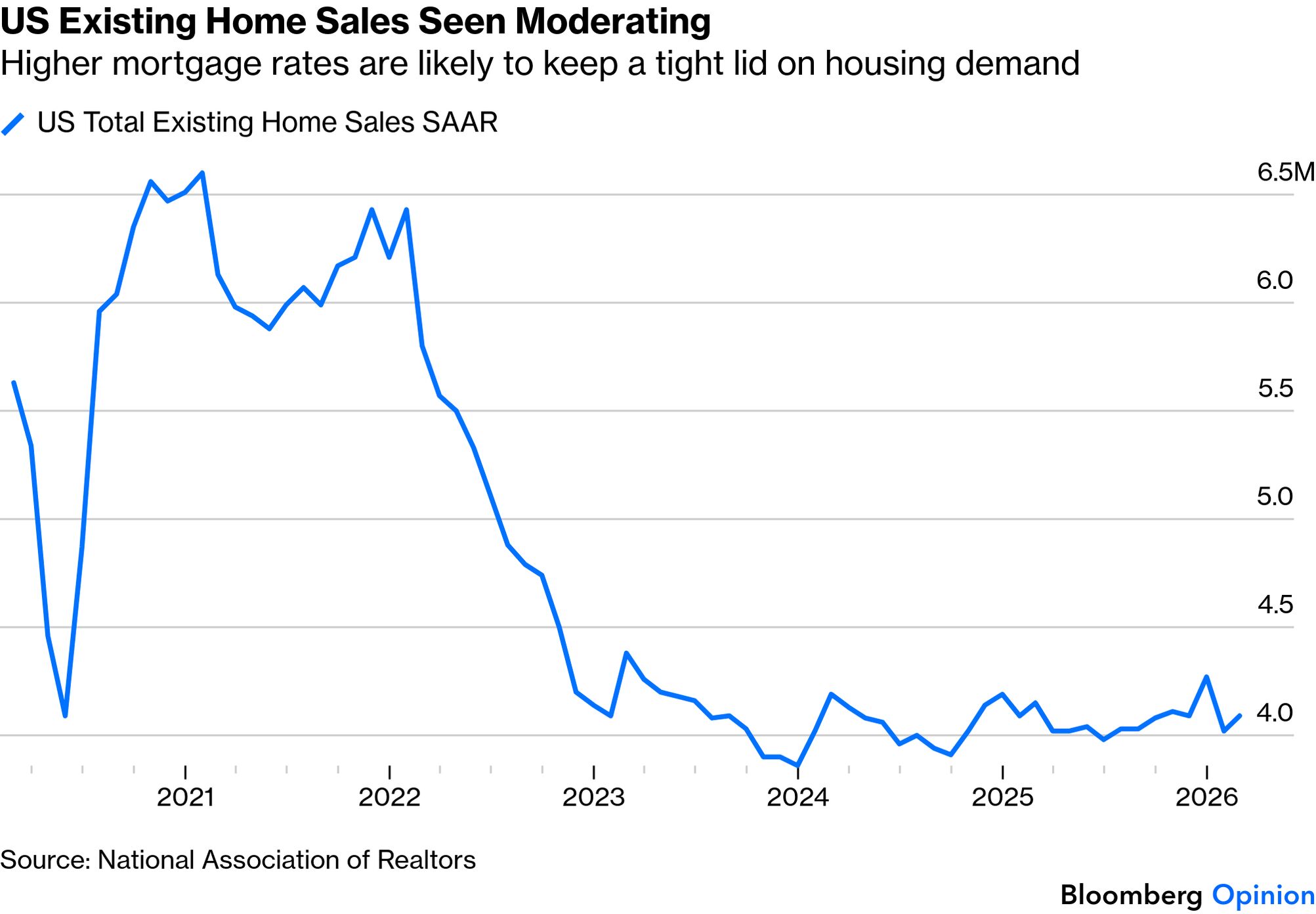

Seasonally adjusted purchase applications actually rose 5.7% in March compared to the previous month. But that reflected a rebound during the first two weeks following February’s depressed levels. Ryan points out that a sharp repricing of mortgage rates drove the broader slowdown through March, as fixed-income markets sold off amid inflation concerns tied to the war:

Weak mortgage activity in March suggests little relief for existing home sales, which have struggled to rise meaningfully above the 4 million annualized mark so far this year. This reinforces our view that existing home sales will remain roughly in line with last year at 4.1 million.

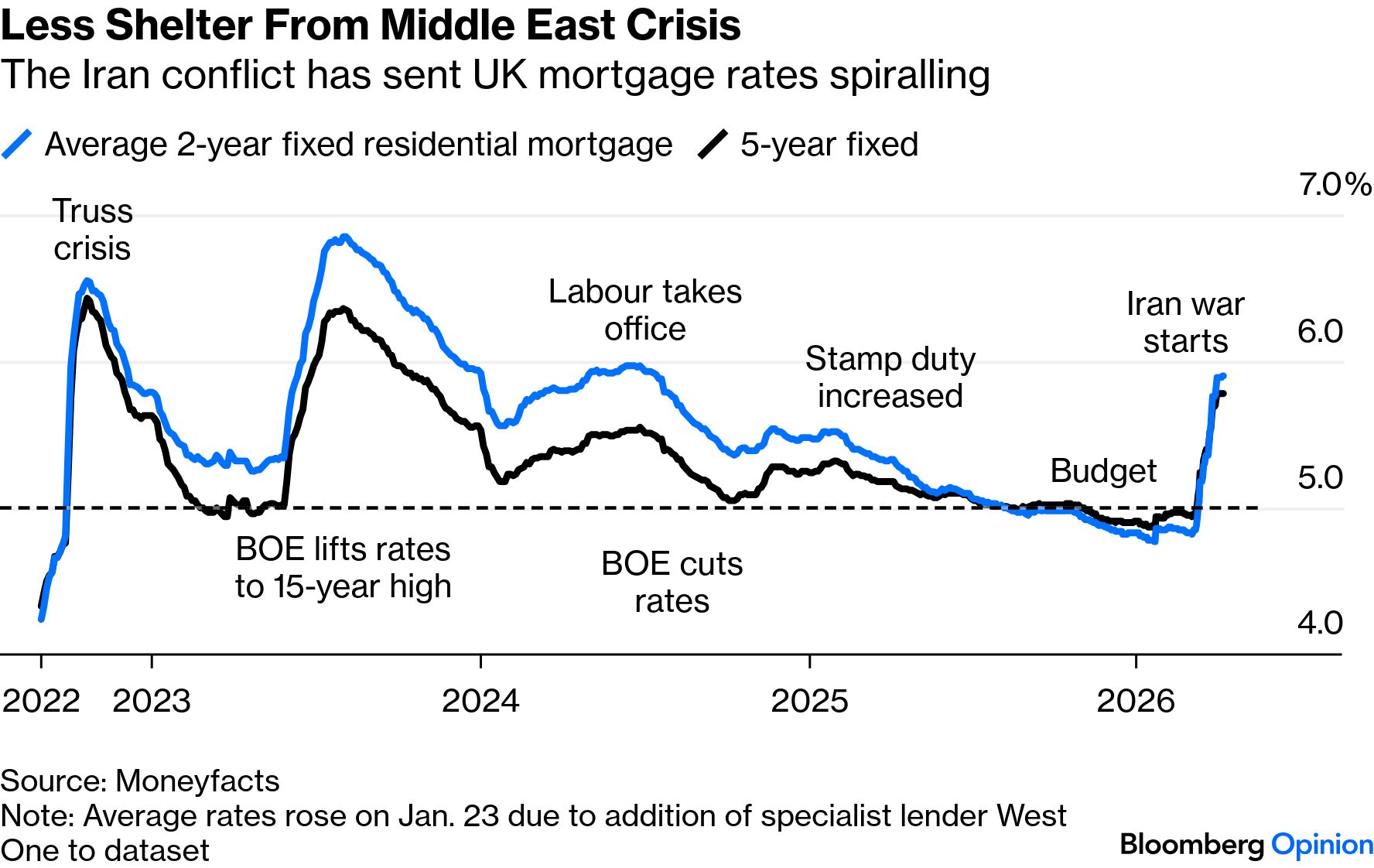

Across the Atlantic, Britons aren’t finding the housing market any more favorable. The Royal Institution of Chartered Surveyors’ gauge of homebuyers’ appetite plunged to the lowest since August 2023, with agreed sales mirroring the deterioration:

Estate agents expect reduced sales and declining house prices over the coming months. The conflict, we can now see, upended the housing market’s strong start to the year. Many lenders rushed to withdraw mortgage products and raise rates last month amid speculation that the Bank of England would hike rates to deal with the supply shock. These concerns may be exaggerated. But life for prospective homebuyers would have been a lot easier without war. —Richard Abbey |

No comments:

Post a Comment