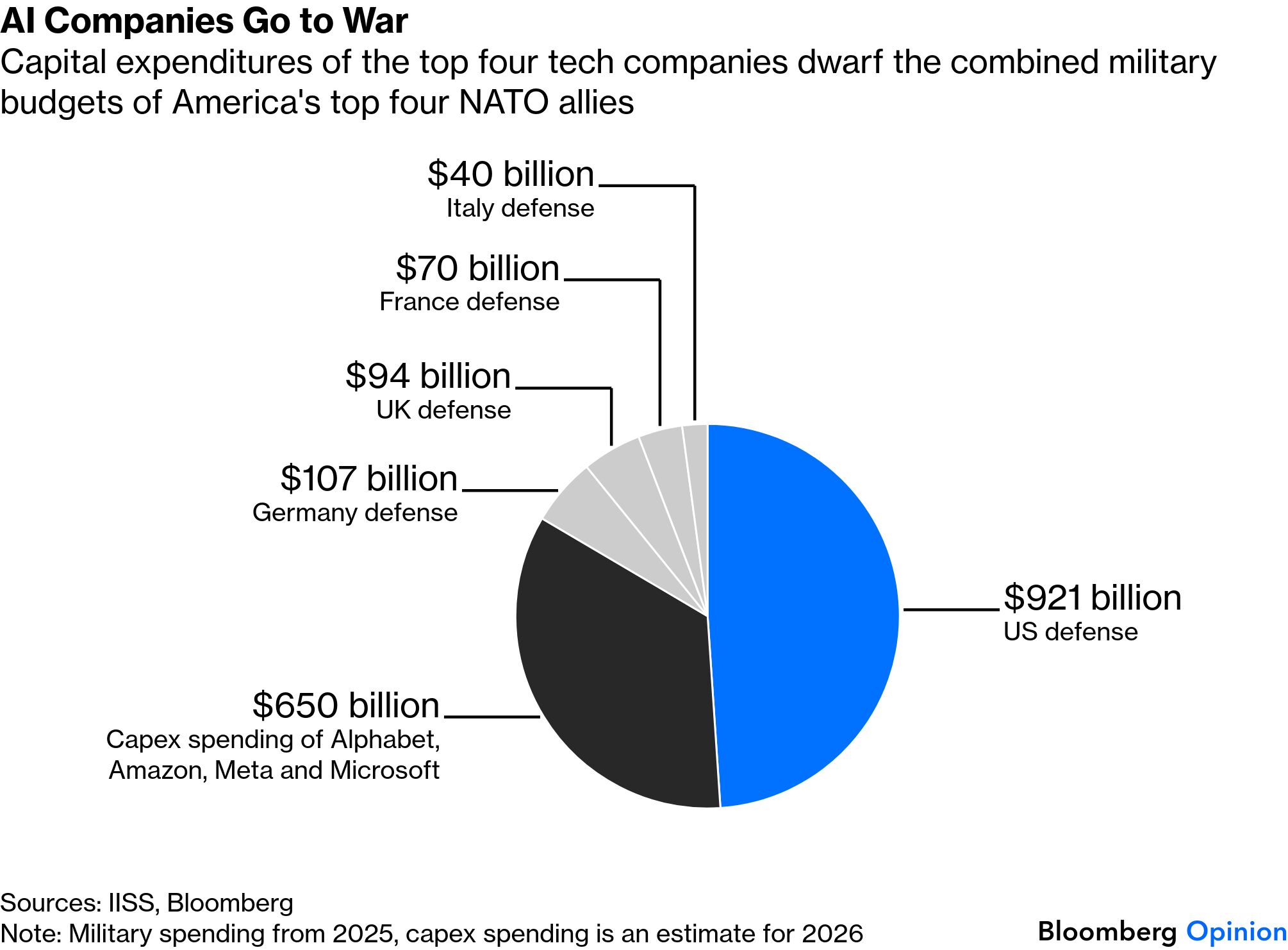

| This is Bloomberg Opinion Today, an insurmountable structural roadblock of Bloomberg Opinion's opinions. On Sundays, we look at the major themes of the week past and how they will define the week ahead. Sign up for the daily newsletter here. I'm not going to lie to you: $650 billion is a lot of money. How much, exactly, makes my head hurt. I mean, as a six and a five and a handful of zeros after them, it's not particularly impressive, or visceral. It's like when you are told the tonnage of a cruise ship — it seems like a really big amount, but what does it really mean? You can go ahead and tell me that $650 billion is the equivalent of 434 million iPhone 17 Pros or 123 billion Big Macs or 72 billion mass-market yo-yos or 8.6 billion professional yo-yos or 6.5 million ultraluxury jewel-encrusted yo-yos. But I can't really visualize any of those, either. I asked ChatGPT to make an image of those $100,000 blinged-out yo-yos in a pile, and while it's cute, it's not helpful. And it's not like I don't spend a certain amount of time thinking about unimaginably vast numbers: Military spending is kinda my day gig. So when I hear over and over that Big Tech's Big Four AI firms — Alphabet, Amazon, Meta and Microsoft — are going to spend $650 billion on capital expenditures this year, my mind goes here: [1] Here's how Dave Lee visualizes that $650 billion: "Nvidia will get a lot of it." Why? Hello, margins. "Adjusted gross margin in the November-January period was 75.2%, the highest it has been since the second half of 2024," Dave reports. "The company forecasts that number to be roughly the same in the current quarter. What's unclear is just how long Nvidia can maintain this extraordinary profitability as the AI landscape matures." So I guess my retirement nest egg is going straight to Jensen Huang, right? Jonathan Levin thinks I should wait out the "SaaSpocalypse" — in which investors dumped enterprise software purveyors that manage accounts and workflows. "As one argument went, who needs expensive software subscription platforms when AI coding tools could spin up made-to-order new software in hours? Who needs insurance brokers or wealth managers when AI chatbots can guide consumers on their financial journeys?" writes Jonathan. [2] "Sure, some of those fears will be validated, making bottom-fishing in individual stocks a bit of a minefield. But from the standpoint of diversified S&P 500 Index investors, these episodes of volatility may be a blessing in disguise — a sign that market psychology is shifting and the air is coming out of the AI bubble." Um, do you think? The problem may run deeper than stock prices. Gautam Mukunda cites the warnings of his mentor, the management guru Clayton Christensen. "Successful companies improve their products faster than most customers require. Their cost structures are built to serve their most demanding users. And then they get eaten from below by cheaper alternatives that serve everyone else," writes Gautam. "The frontier AI companies are building exactly the kind of cost structure Christensen warned about at a scale he could never have imagined." If Big Tech is overplaying its hand, the world's biggest nation is underutilizing its talent. "India is fast becoming one of the world's biggest AI user bases. The question now is how it can turn that scale into superpower status rather than just training Silicon Valley for free," writes Catherine Thorbecke. "The three main building blocks of AI are talent, compute (including high-end chips and infrastructure), and data. India doesn't lack engineers, but it currently doesn't have foundational research training at scale or enough advanced processors at public labs and universities. What it does have, in abundance, is data. It should start treating this like a strategic asset rather than leaking it out as a free export." What India also has in abundance is people, and more and more on the way. "In the past, investors inclined to be more bullish on countries with young and growing populations, such as India and Indonesia, betting that better demographics would underpin more vibrant consumer spending," writes Shuli Ren. "By comparison, aging populations, as seen in China, Japan and South Korea, were presented as an insurmountable structural roadblock. The adoption of AI technology will transform that dated mindset. Driven by labor shortages, North Asia will only double down on robotics." And if a machine can't do your job for you, at least it can make your restaurant reservations — thanks to OpenClaw and its new owner, OpenAI. "The broad possibilities of AI agents flip the idea, popularized by venture capitalist Marc Andreessen, that 'software is eating the world.' Now AI might just eat software," Parmy Olson writes. "How long that disruption takes depends on how quickly [Sam] Altman and entrepreneurs like Gavriel Cohen can make agents both secure and idiot-proof. As any cyber security expert will tell you, the latter problem is the hardest to solve." Well, so long as OpenClaw can get this idiot reservations at One Madison Park, I'm all for disruption. [3] Bonus Welcome to the Machine Reading: What's the World Got in Store ? - UK Spring Statement, March 3: Green Triumph Is Catastrophic for Starmer, Terrible for Farage — Rosa Prince

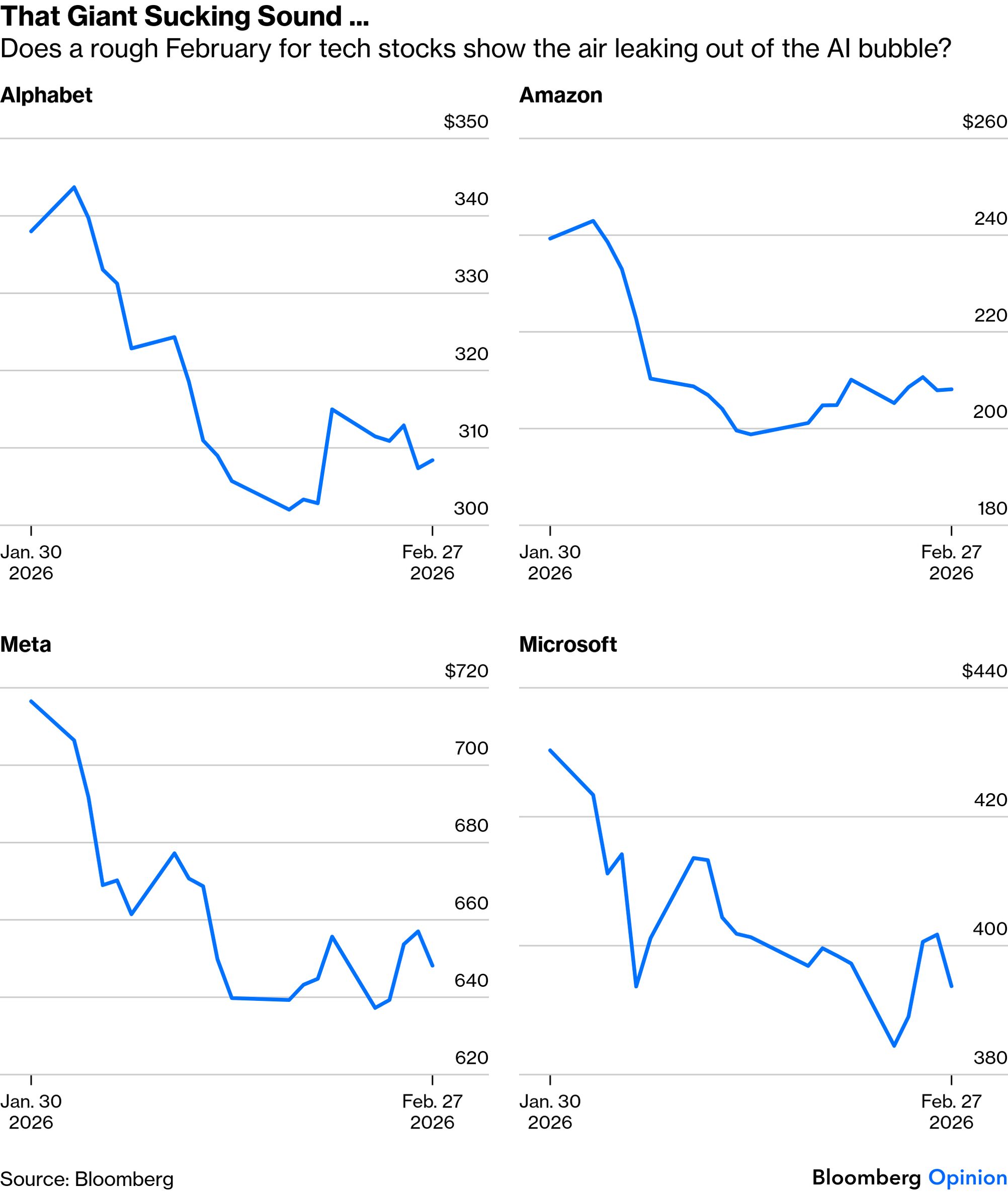

- China's National People's Congress starts, March 5: Want to Counter China? Stop Tariffing Your Friends — Karishma Vaswani

- US jobs report, March 5: Factories Can Come Back to the US. Jobs, Not So Much — Thomas Black

OK, let's say the AI bubble is here to stay. The robots will clean all our bathrooms, OpenClaw will snag that four-top at Ha's Snack Bar and we'll get to retire early and drink from a sea made of lemonade. Charles Fourier's eyes would have lit up at the prospect, but that excitement isn't universal. In his 1930 essay, Economic Possibilities for Our Grandchildren, John Maynard Keynes asked himself the question, "what would life be like a hundred years hence?" The answer is my greatest dream, but possibly our grandchildren's nightmare. 'The combination of innovation and compound interest would solve the problem that had dogged humanity since Adam and Eve: how to make ends meet," writes Adrian Wooldridge. "Our grandchildren would be able to meet all their material needs by working 15 hours a week. But this would leave what Keynes called 'the permanent problem of the human race.' How to use the resulting freedom from economic necessity to live a good life — or as Keynes put it 'how to live wisely and agreeably and well.'" A century later, Adrian worries that AI is proving the great economist prescient. "Perhaps the biggest problem with job destruction is that jobs are not merely ways of making a living," he writes. "Jobs provide people with a combination of psychological benefits: social connections, pride and self-worth, a sense of accomplishment and, not to put too fine a point on it, meaning." Well, a world of nothing but leisure time might become deprived of meaning, but think of all the yo-yo tricks you could master. Note: Please send yo-yo tricks and feedback to Tobin Harshaw at tharshaw@bloomberg.net |

No comments:

Post a Comment