| Welcome to Next Africa, a twice-weekly newsletter on where the continent stands now — and where it's headed. Sign up here to have it delivered to your email. US President Donald Trump's trade war has effectively locked African nations out of global debt markets yet again. Sovereign bonds across the continent were hammered by a selloff of riskier assets after Trump announced "reciprocal" tariffs on imports from across the world after accusing other nations of exploiting America's openness while protecting their own economies from fair competition.  Containers at the Cape Town port. Photographer: Dwayne Senior/Bloomberg Bond yields have spiked from Nigeria to Kenya and South Africa. That makes it all but unaffordable for governments to raise money internationally, especially as collapsing commodity prices simultaneously hit their tax revenue. Oil exporters like Nigeria, Angola and Gabon will be particularly hard hit. To complicate matters, African currencies rank among the worst-performing against the dollar this month. That's a double-edged sword for commodity producers: While depreciation will boost export earnings in local-currency terms, it will also increase the cost of repaying loans. African governments have been testing the waters after being shut out of foreign markets in 2022, when rates rapidly rose as the Federal Reserve led central banks in fighting rampant inflation. Borrowers including Ivory Coast, Benin and Kenya subsequently returned to the market. That window now appears to have shut. There aren't many African nations that have foreign bonds maturing this year, meaning most governments could wait the turmoil out. Some, including Kenya and Ivory Coast, have already refinanced maturing debt. South Africa, however, finds itself in a tight spot.  South African rand banknotes at a vendor's stall in Johannesburg. Photographer: Leon Sadiki/Bloomberg It has a $2 billion eurobond due in September, the premium it pays to borrow has spiked to an 18-month high and the rand has slumped to the weakest level in more than a year. The country's Treasury says it's confident it can execute its foreign-borrowing strategy — but it's hoping for conditions to stabilize before returning to the market. Trump has offered little clarity on what he's seeking in exchange for lowering tariffs and his officials have signaled that negotiations with trading partners will take time. That means the squeeze is unlikely to abate any time soon. — Robert Brand Key stories and opinion:

Specter of Bond-Market Lockout Returns for African Governments

Trump Keeps Investors on Edge With Clashing Tariff Comments

Ecobank Says Local African Trade Crucial to Avert Tariff Fallout

Trump Has Unveiled Reciprocal Tariffs. What Are They?: QuickTake

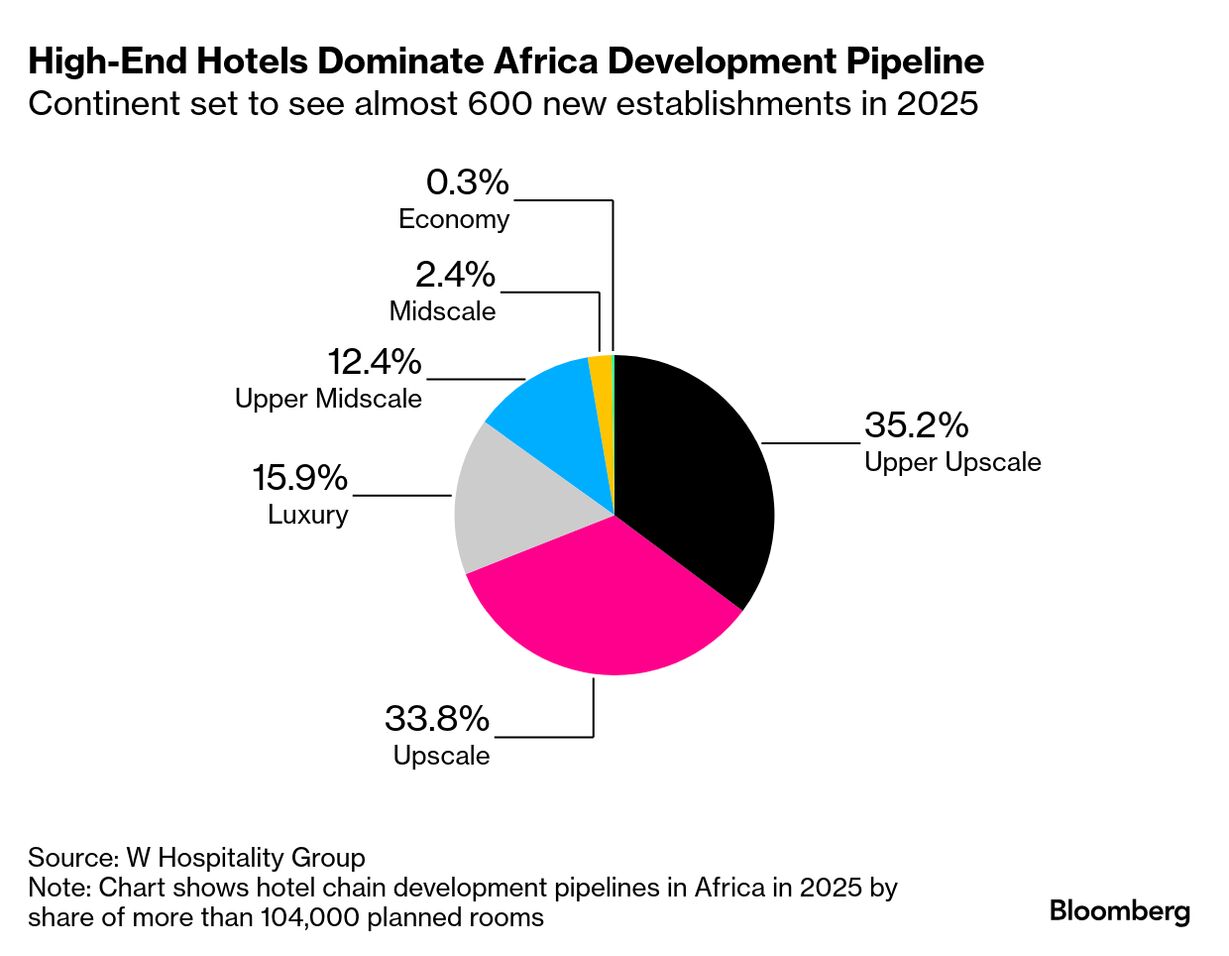

There's No Sign That Markets Have Had Enough Yet: John Authers South Africa's second-largest political party is deeply divided about whether to remain in the country's ruling coalition following a standoff over the budget. The Democratic Alliance voted against a key piece of legislation after its economic policy proposals were shot down. A group within the DA has always opposed being part of the so-called government of national unity and are now pushing to walk away, sources say. The party's Federal Executive met to discuss the issue on Monday, but no decision was taken. The biggest party, the African National Congress, hasn't decided whether to exclude any group from the government.  DA supporters at a rally in Pretoria ahead of last year's elections. Photographer: Waldo Swiegers/Bloomberg The African Union's public-health agency said governments will need to turn to taxes and the private sector to fill the hole left by the cancellation of billions of dollars of American aid. The Africa Centres for Disease Control and Prevention warned that an unprecedented financing crisis threatens to undermine pandemic preparedness, maternal- and child-health services and disease-control programs. "We know that never again will we get what we had in the past," said Jean Kaseya, the agency's director-general. Africa is on track for a boom in high-end hotels and resorts, with top chains such as Marriot International and Hilton backing new developments. There are 104,444 rooms under construction, the most in at least four years, a report that covers 54 countries by Lagos, Nigeria-based W Hospitality Group shows. High-end developments account for more than three-quarters of the pipeline.  Mali summoned Algeria's ambassador and recalled its own envoy from Algiers after one of its army drones was shot down near their shared border. The military lost contact with the drone around April 1 and an investigation found it had likely been hit by a missile. Mali's military ruler Assimi Goita called the incident an act of aggression and said allies Burkina Faso and Niger, which are also ruled by juntas, would also recall their ambassadors. Algeria's defense ministry said it had shot down an armed surveillance drone.

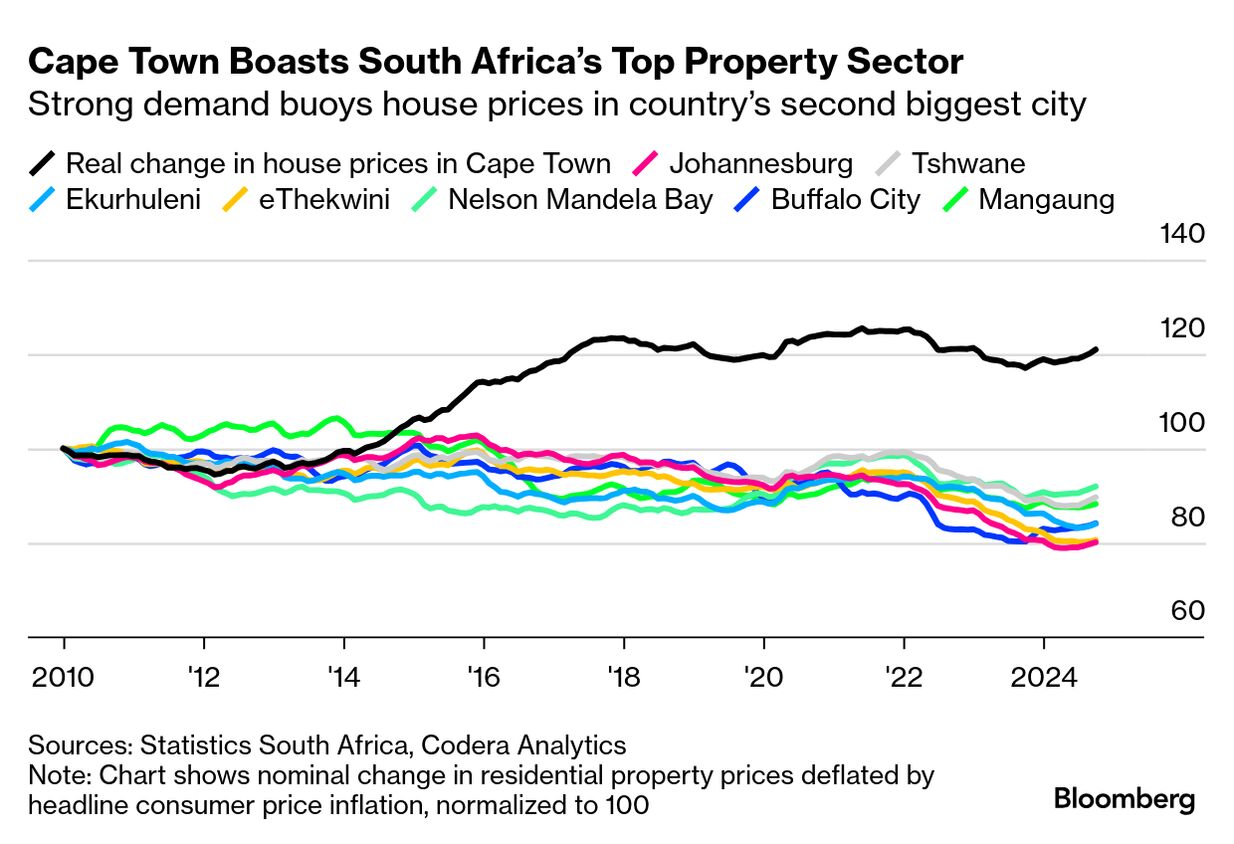

Gold and foreign-currency reserves backing the ZiG, Zimbabwe's bullion-linked currency, have more than doubled since its introduction, according to the central bank's governor. The reserves stood at $629 million at the end of last month, John Mushayavanhu said. Short for Zimbabwe Gold, the ZiG started trading a year ago, replacing the defunct Zimbabwe dollar, which was in freefall. The authorities want it to supersede the US dollar, which has been used as a dual transacting currency since 2009.  Mushayavanhu holds up ZiG notes. Photographer: Cynthia R Matonhodze/Bloomberg The World Bank said it will unlock further financing for Kenya on condition the government implements wide-ranging economic reforms. The East African nation received $1.2 billion of World Bank budget financing last year, and pledged to pursue fiscal consolidation and achieve a new debt anchor set at 55% of gross domestic product by 2029. Treasury Secretary John Mbadi has said the country is in negotiations for another $750 million from the lender. Kenya failed to meet the conditions of a four-year International Monetary Fund program in March, forgoing about $850 million in financing. Thank you for your responses to our weekly Next Africa Quiz and congratulations to Daniel Sodimu, who was first to correctly respond that there are no permanent inhabitants on the Heard Island and McDonald Islands, which Trump subjected to a 10% tariff. Cape Town, which has Africa's priciest real estate, plans to make it easier to develop homes as thousands flocking to the city put pressure on its $64 billion residential property market. Wedged between the iconic Table Mountain and the sea, South Africa's second-biggest and best-run metropolis has long been a favorite base for the wealthy seeking warm weather and an outdoor lifestyle. That's pricing locals out of the market.

Thanks for reading. Watch out for news from our inaugural Next Africa seminar with South African Trade Minster Parks Tau in our next edition on Friday. Send any feedback to mcohen21@bloomberg.net. |

No comments:

Post a Comment