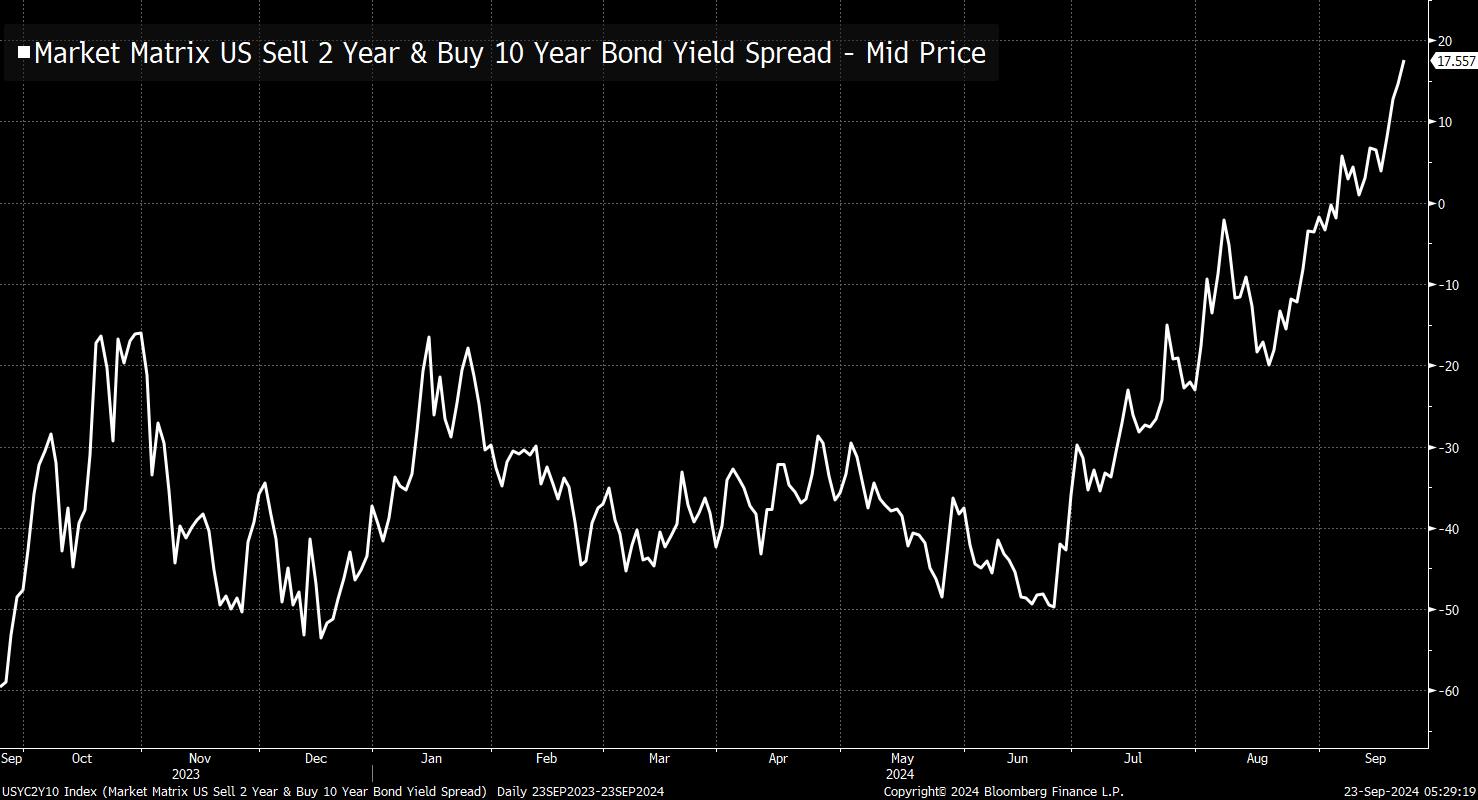

| Good morning. US markets are waiting for signs of what's next from the Fed after last week's rate cut, while in Europe and China expectations are mounting for further central bank action. And Intel is said to have received a multi-billion dollar investment offer from Apollo. Here's what markets are talking about today. — Morwenna Coniam Want to receive this newsletter in Spanish? Sign up to get the Five Things: Spanish Edition newsletter. US stock futures pointed to a slightly higher open with indexes hovering near record highs after the Federal Reserve's outsized rate cut last week and as traders look forward to speeches from Fed officials for fresh insight on the pace and scope of further easing. The euro retreated and German bond yields fell after a lower-than-expected French services PMI reading, while in Asia, stock benchmarks climbed after China announced plans for a rare economic briefing Tuesday and cut a short-term policy rate. Gold touched a record high ahead of US data this week, including the personal consumption expenditures gauge and jobless claims, that may offer clues on whether the Federal Reserve's 50-basis-point rate reduction will be the first in a series of aggressive cuts. The precious metal later pared the move due to escalating tensions in the Middle East. The euro area's private-sector economy shrank for the first time since March, with the end of France's Olympic boost and a deepening manufacturing downturn heightening concerns that the recovery has run out of steam. A key segment of the German yield curve normalized after the release as traders bet that the European Central Bank will need to accelerate the pace of rate cuts to underpin the 20-nation economy. Meanwhile, China announced plans for a rare briefing on the economy just as it cut one of its short-term policy rates, fueling speculation officials are preparing to ramp up efforts to revive growth. The moves bolster expectations for the PBOC to lower rates after the Fed's cut eased pressure on China to defend its currency. After disappointing data in August, there are concerns that the world's second-largest economy could miss its annual growth target of around 5% without more support. Intel shares rose in premarket trading after Apollo offered to make an equity-like investment of up to $5 billion, according to a person familiar — a move that would be a vote of confidence in the chipmaker's turnaround strategy. It comes just days after Qualcomm was said to have floated a friendly takeover, raising the prospect of one of the biggest-ever M&A deals. The chipmaker is considering Apollo's proposal. This is what's caught our eye over the past 24 hours. Hello and welcome to the week after Fed week. As of the time that I'm typing this, stock futures are up a little bit. And the 2-10 spread continues to steepen. Here's a chart of the 2-10 spread.  The 10-year yield has gone up a touch since the Fed decision last week, and what's important to remember is that this is perfectly consistent with Fed easing. Some people get confused by this. They think the Fed easing and lower rates are synonymous. But to some extent this is a misconception. The simplest thing to think about it is that if we had some kind of massive shock tomorrow, harming the economy, you'd almost certainly expect the 10-year yield to collapse. Or think about the 2010s, after the Great Financial Crisis. Inflation was very mild. Employment growth was mediocre, and rates fell through most of the decade. Just going on the economic targets alone, the implication is that for many of those years, the Fed was too tight. And that's why yields at the long end of the curve kept falling. Anyway, it'll be a decent week for economic data. Nothing too massive. But today we get the S&P Services and Manufacturing PMIs. Tomorrow, we get Philly Fed Non-Manufacturing, Richmond Fed, and the Conference Board confidence data. Later this week we'll also get Initial Jobless Claims, the latest reading of Q2 GDP, and then also Core PCE, which we know matters a lot to the Fed. Should be another interesting week. Follow Bloomberg's Joe Weisenthal on X @TheStalwart |

No comments:

Post a Comment