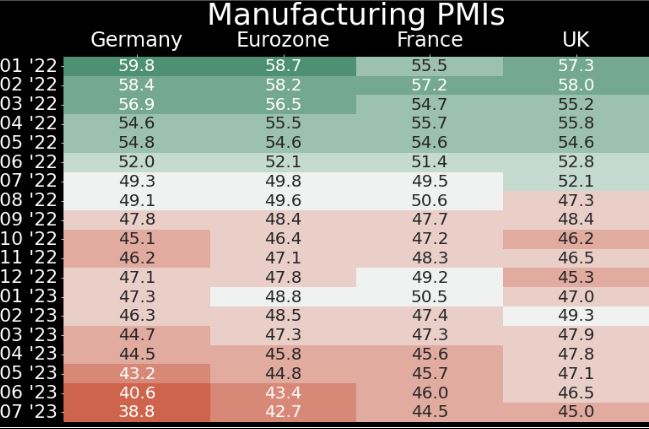

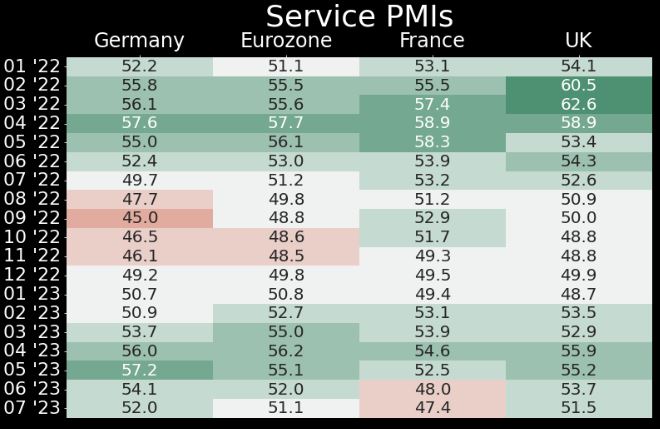

| Good morning. Wild weather may dampen tourism, China's markets throw off gloom and London's pay gap grows. Here's what people are talking about. Summers are getting more intense in southern Europe. Greek wildfires have forced evacuations of thousands of holiday-goers, while tourists wilted in Sardinia's near-record heat last week. Climate change is set to make tourist-friendly weather in some European destinations unrecognizable, sparking a tectonic shift for Europe's travel and tourism industry, which contributed $2.1 trillion to the regional economy last year. It could also remap travel patterns in a way that will likely deal a blow to some countries. For the day at least, optimists are driving China's markets on bets Beijing is finally adopting a more aggressive growth policy, and will soon unveil a series of supportive measures. The Politburo statement on Monday is spurring rallies in Chinese stocks, the yuan and the dollar bonds of developers after weeks of doubts. The question for many investors though is whether measures will follow through, and be able to tackle daunting challenges from local government debt to a slumping housing market and high youth unemployment. London's highest earners have reaped the biggest pay raises since the start of the pandemic, widening the gap between the richest and poorest people in the UK for the first time in two decades, the Institute for Fiscal Studies found. Average earnings for workers in the capital have increased 5% to £4,400 ($5,646) a month before tax since February 2020, almost double the 2.7% national average. The highest pay raises went to those working in business services including finance, accounting and law, which are concentrated in London. Global asset managers such as KKR and Allianz are partnering with Australia's $2.4 trillion pension fund industry on private market deals. The big attraction: Inflows of more than $676 million a week that need to find an investment destination. The industry's assets are forecast to as much as triple by 2040, and KPMG expects that the nation's two largest funds could each cross the trillion-dollar mark in that time. European equity futures dipped as traders brace for key central bank decisions this week. EU agriculture ministers meet in Brussels. Expected data include business confidence in Germany, the UK and Belgium. LVMH, Unilever and DSV are among a slew of companies scheduled to report earnings. Do you think the AI rally resembles the dotcom bubble? Will Nvidia become the world's largest company? Are you planning to increase your exposure to tech stocks? Share your views on big tech and ChatGPT in the latest MLIV Pulse survey. This is what's caught our eye over the past 24 hours Europe's manufacturing sector is now deep in the red, with services threatening to go the same way. This slowdown will impact traders' assumptions about central bank decisions beyond this week. The data is damaging for the soft-landing narrative, and may yet become part of the evidence that sees risk appetite dwindle across markets. Germany, France, the UK and euro-zone PMIs ticked lower. For the euro-area, commentators noted that business output fell at the fastest rate in eight months. What's worse, forward-looking future output expectations and new order inflows suggest further weakness, including in the labor market. That's incredibly damaging for the soft-landing narrative doing the rounds (and yes, I'm still a believer, but these numbers are pretty hard to ignore.) Now, as the table above shows, manufacturing has been bad for a while. And while it isn't getting any better, alone it probably won't be enough to shift policy. The slowdown in services is much more important. France, which relies heavily on this sector, saw the second consecutive sub-50 contractionary reading. Ok, but with a flurry of upcoming central bank meetings, it's fair to ask if any of this will shift matters on the policy front? And the short answer is that it will probably impact decisions more down the line than for anything that happens at the ECB or Fed this week. The key question is whether a soft economy would lead to a more dovish policy, which would then be positive for markets. But the likely answer is that this would only be the case if inflation softens too. The good news on that front is that the report noted price pressures moderated further. Eddie van der Walt is Deputy Managing Editor of the Markets Live blog on the Bloomberg Terminal, based in London. Follow him on Twitter at @EdVanDerWalt. |

No comments:

Post a Comment