| Welcome to the Weekly Fix, the newsletter that's always trying to get smarter. I'm cross-asset reporter Katie Greifeld. If you had an entire 90 minutes with four of the world's most powerful central bankers, it's probably a safe bet that artificial intelligence would come up at least once. Towards the end of a star-studded panel with the heads of the Federal Reserve, the European Central Bank, the Bank of England and the Bank of Japan — the main event in Sintra, Portugal this year — we heard Jerome Powell's thoughts on this year's biggest buzzwords.  Jerome Powell on June 28. Photographer: Horacio Villalobos/Corbis News/Getty Images "On AI, we're doing what everyone else is going. We're trying to get smart about it and it obviously has huge possibilities. Technologies tend to propagate through the economy fairly slowly and this may be the exception, maybe not," Powell said Wednesday. "It's something that we're spending a lot of time on. It's way too early for conclusions." It's easy to brush off that comment as lip service — it's on our radar, too soon to tell — but it raises an interesting question: how does a central bank go about factoring in an emerging technology with potentially enormous labor-force implications into their economic models? According to someone who's been in the room, it's not a black-and-white answer. "Even if AI becomes a big deal, it's not at all clear whether or not the net effect would be to push up or push down neutral policy rates. So I think the Fed is to be commended by trying to get ahead of this," former Fed vice chair Richard Clarida, now a global economic advisor at Pacific Investment Management Co., told Matt Miller and I on Bloomberg Television. "I would imagine they're looking at both sides of the AI coin if you will — the potential for disinflation in terms of labor cost reductions but faster growth and I think they'll probably be looking at both those dimensions." AI aside, the message from Powell and peers in Sintra was extremely clear: the inflation fight is far from over. This week brought the Fed's stress tests for the biggest US banks, and as expected, all 23 lenders sailed through the exam. While it's always easy to criticize the annual assessment for testing the wrong things, a potential issue this year is that duration risk — the bogeyman behind March's banking crisis — may have flown under the radar. The criteria for this year's exam was set before the regional bank turmoil. The severely adverse scenario was a toxic mix that included US unemployment surging to 10%, commercial real estate prices plunging 40% and the dollar jumping. Also included was the Fed's policy rate plunging back to zero. In the eyes of Ironsides Macroeconomics's Barry Knapp, a bigger hurdle for the banks would be the Fed hiking rates meaningfully higher from here. "The real adverse scenario is the Fed can't get inflation under control, decides they need to get to 2% right away," Knapp said on Bloomberg Television. "If the Fed becomes intent on trying to drive it to 2% right away, takes the front rate to 6% and the curve is 200 basis points inverted, there's no alternate for small community banks other than to shrink assets. And that's the lifeline of credit to the small business sector, which we have the least information about." Rewinding back to the dark days of March, the embedded irony in the banking crisis was that the world's safest asset sparked it after banks such as Silicon Valley Bank loaded up on long-maturity Treasuries in an ultra-low interest rate world. Against that backdrop, while the Fed did conduct an exploratory market shock on the trading books of the largest banks, testing them against greater inflationary pressures and rising interest rates, it would have been useful to see how everyone fared more broadly under the weight of substantially higher rates. Former New York Fed president and current Bloomberg Opinion columnist Bill Dudley made waves on Thursday with a big call: ten-year Treasury yields might be heading to 4.5%. The entire column is well worth reading, but for newsletter purposes, here's the meat of Dudley's argument: Suppose the Fed's short-term interest-rate target, adjusted for inflation, averages about 1% over the next decade. Inflation averages 2.5%, and the bond risk premium is one percentage point. In sum, this suggests a 10-year Treasury note yield of 4.5%. And that's a conservative estimate: Given historical neutral short-term rates, the recent persistence of inflation and the troubling US fiscal trajectory, all three elements could easily go higher.

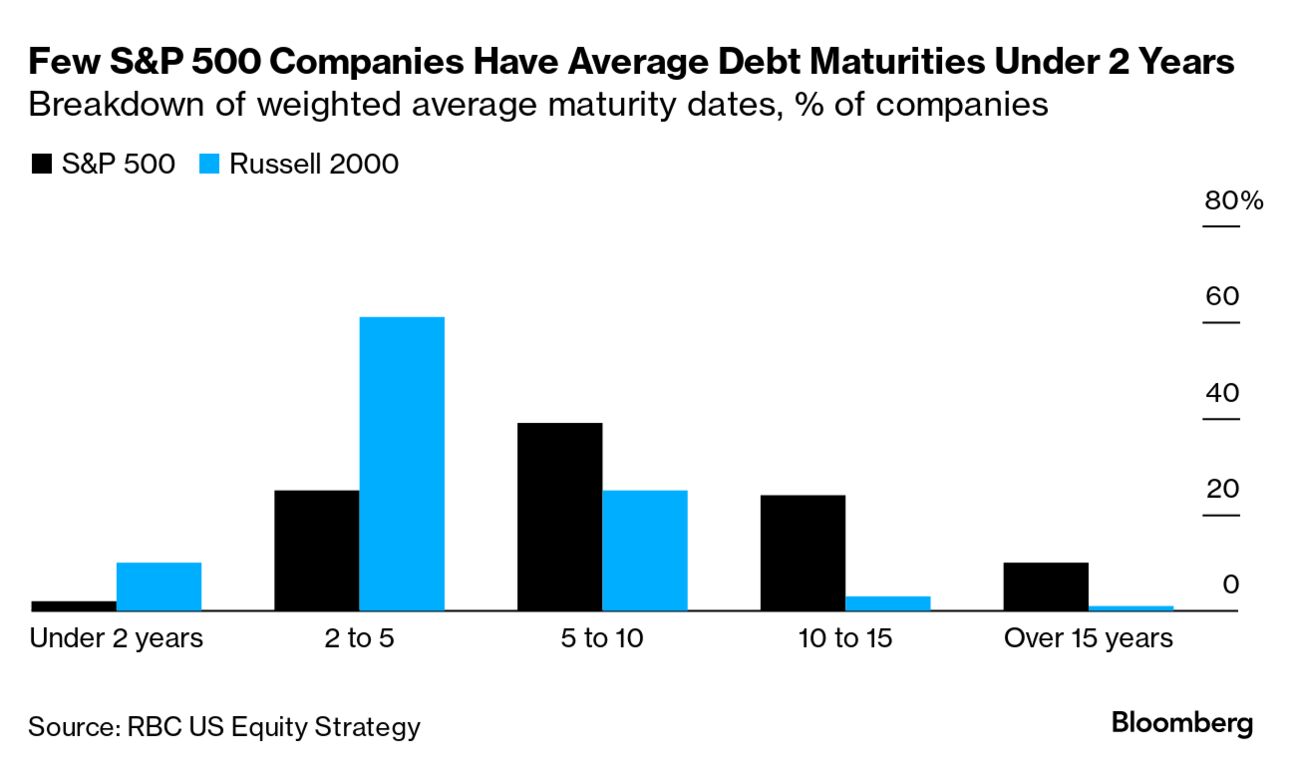

For context, 10-year Treasury yields haven't seen 4.5% since 2007. They're currently hovering near 3.83%, well below this cycle's high of 4.33% reached in October. Dudley's call stands outside the Wall Street consensus, with many money managers making the case that now is the time to start extending duration. Firmly on the other side of the the trade is Morgan Stanley's Matthew Hornbach, who wrote in mid-June that he expects 10-year yields to end 2023 at 3.5% — a full percentage point below Dudley's call. As fate would have it, Hornbach joined Bloomberg Television hours after Dudley's column published and walked through his forecast. It centers on the argument that federal fiscal support — once a wrench in the Fed's inflation fight — will pullback this year, turning into a tailwind for the central bank's campaign to stamp out price pressures. "We do think inflation will decelerate more meaningfully than the Fed is expecting," Hornbach, Morgan Stanley's global head of macro strategy, said on Bloomberg Television. In the same way that the debt ceiling spooks the Treasury market every couple of years, a looming maturity wall surfaces in bear cases for the corporate credit market. Here's the bogeyman this time around: about $88 billion of junk bonds are maturing through the end of next year, and overall, the high-yield market has the shortest average time to maturity on record. But how big of a threat are those upcoming maturities and rising debt service costs to the stock market? Lori Calvasina of RBC Capital Markets had some soothing statistics in a note this week: very few companies in the S&P 500 and the Russell 2000 have weighted average maturities in the 2-year-or-sooner timeframe. Specifically, that comes to just 2% of firms in the S&P 500, and 10% among small-cap companies, according to RBC. "Overall, we continue to see balance sheets as manageable," wrote Calvasina, the firm's head of US equity strategy. "Higher interest rates are clearly a headwind, but from a public company balance sheet perspective this issue appears to be one that companies have some time to deal with, particularly if the Fed starts cutting in 2024." According to RBC, the weighted average maturity in the small cap index is roughly 4.6 years, versus 8.5 years for the big benchmark, leaving the larger companies better equipped to navigate through any upcoming maturity hurdles. Not to mention, the S&P 500's weighted average interest expense as a percent of sales has dropped to about 2%, comfortably below the gauge's long-term average just below 3%. - The Air Jordan drop so hot it blew up an alleged $85 million Ponzi Scheme

- Citadel Securities is muscling its way into credit market-making

- Libor fades into history after 50 years of benchmark dominance

|

No comments:

Post a Comment