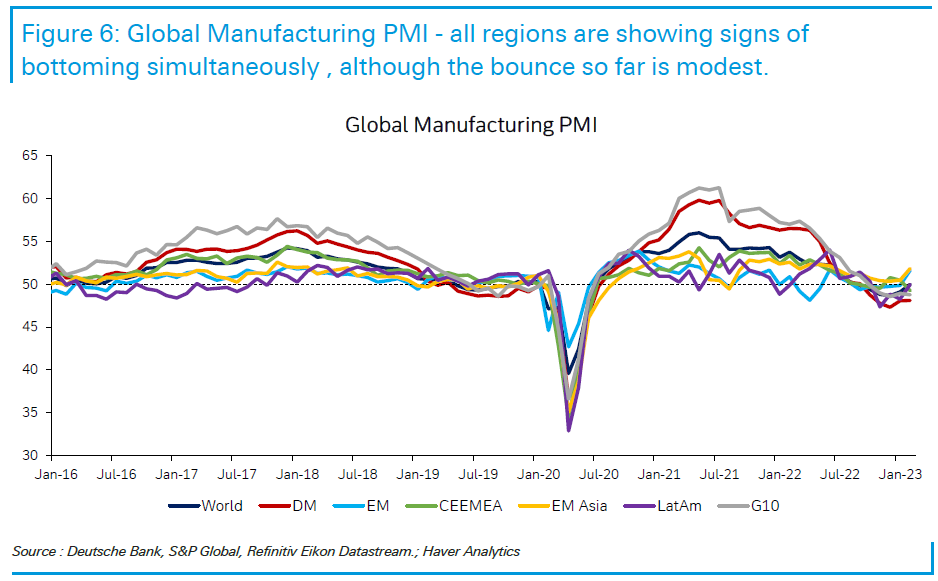

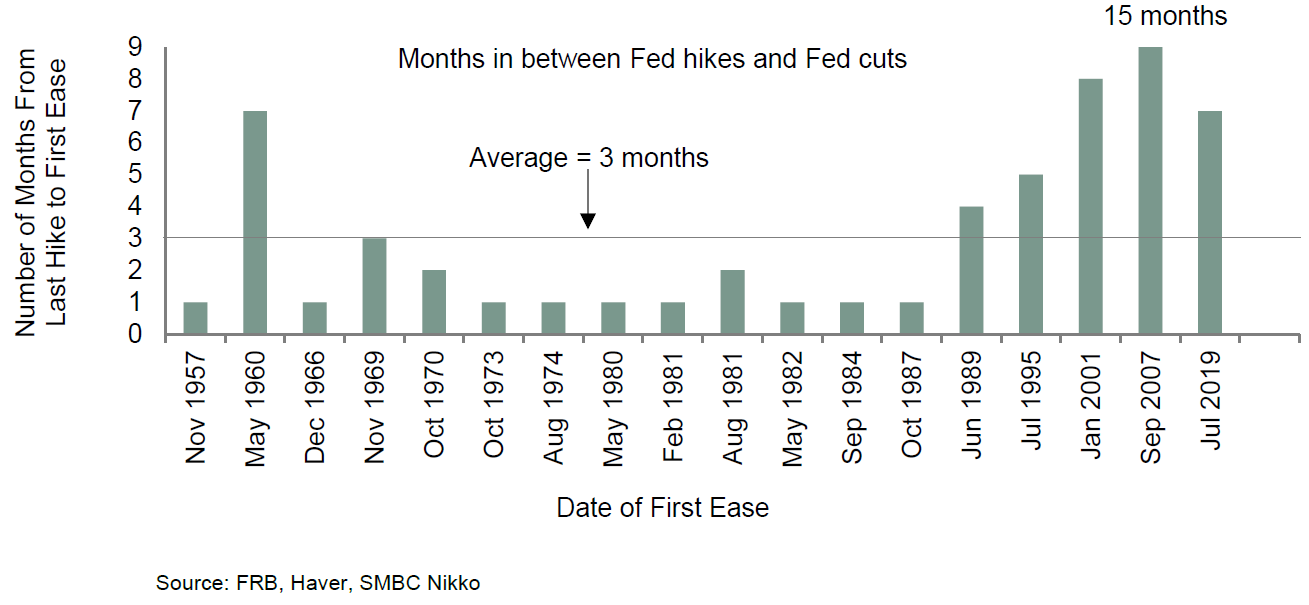

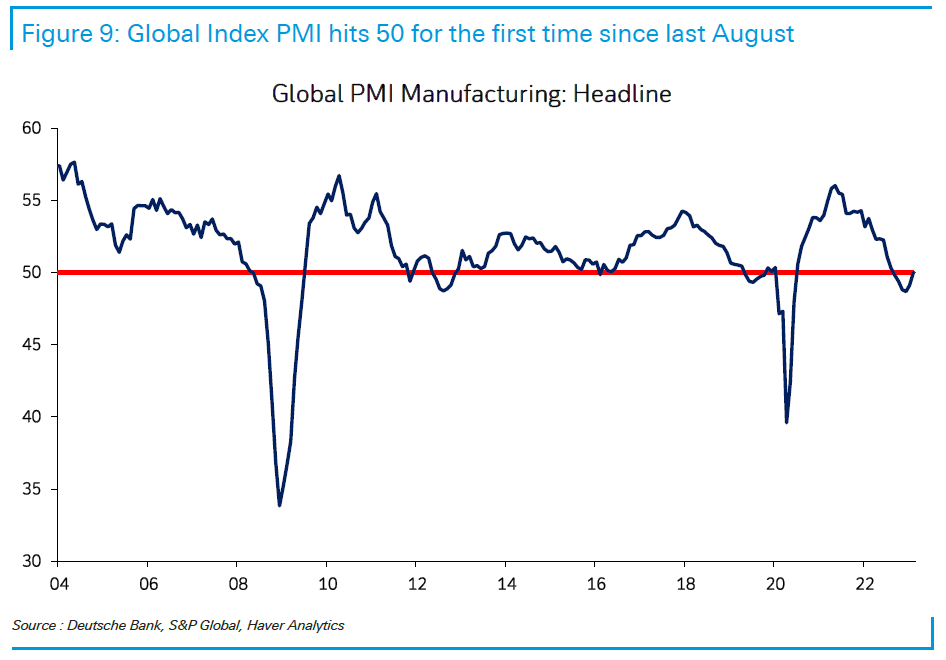

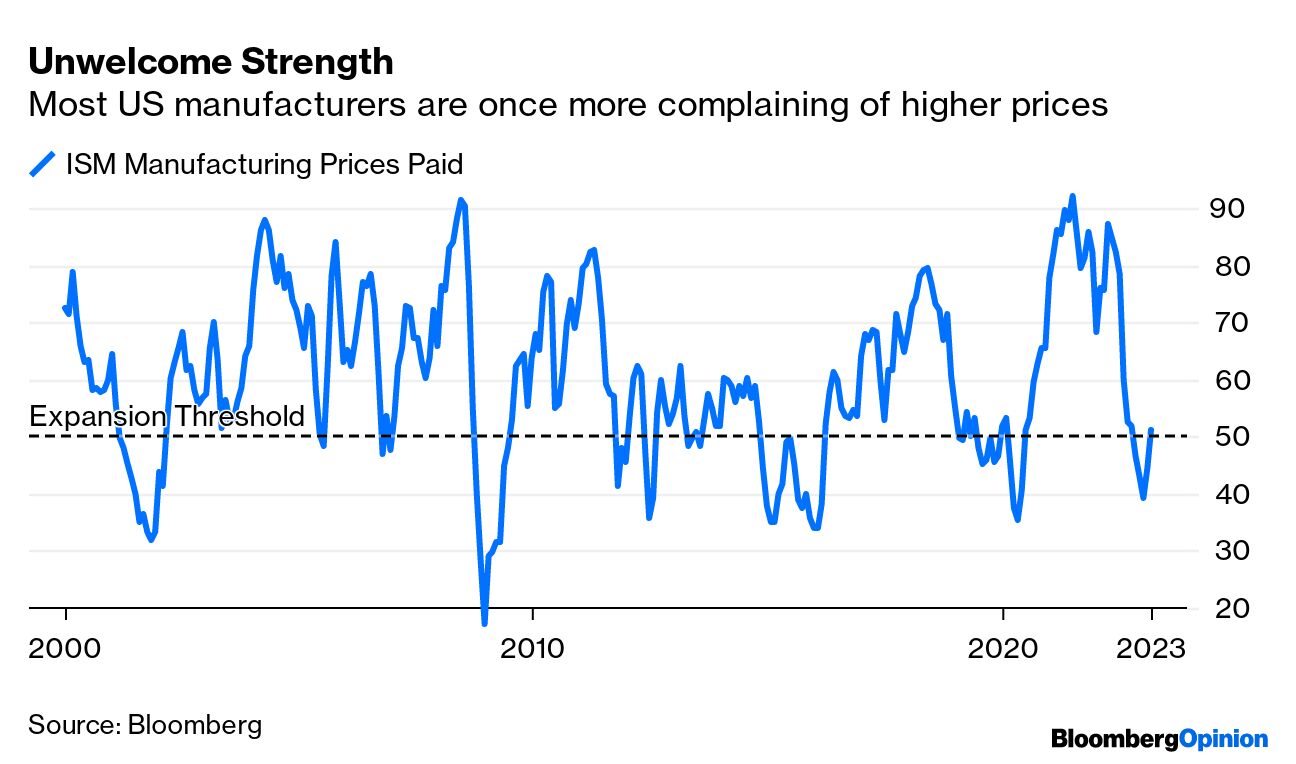

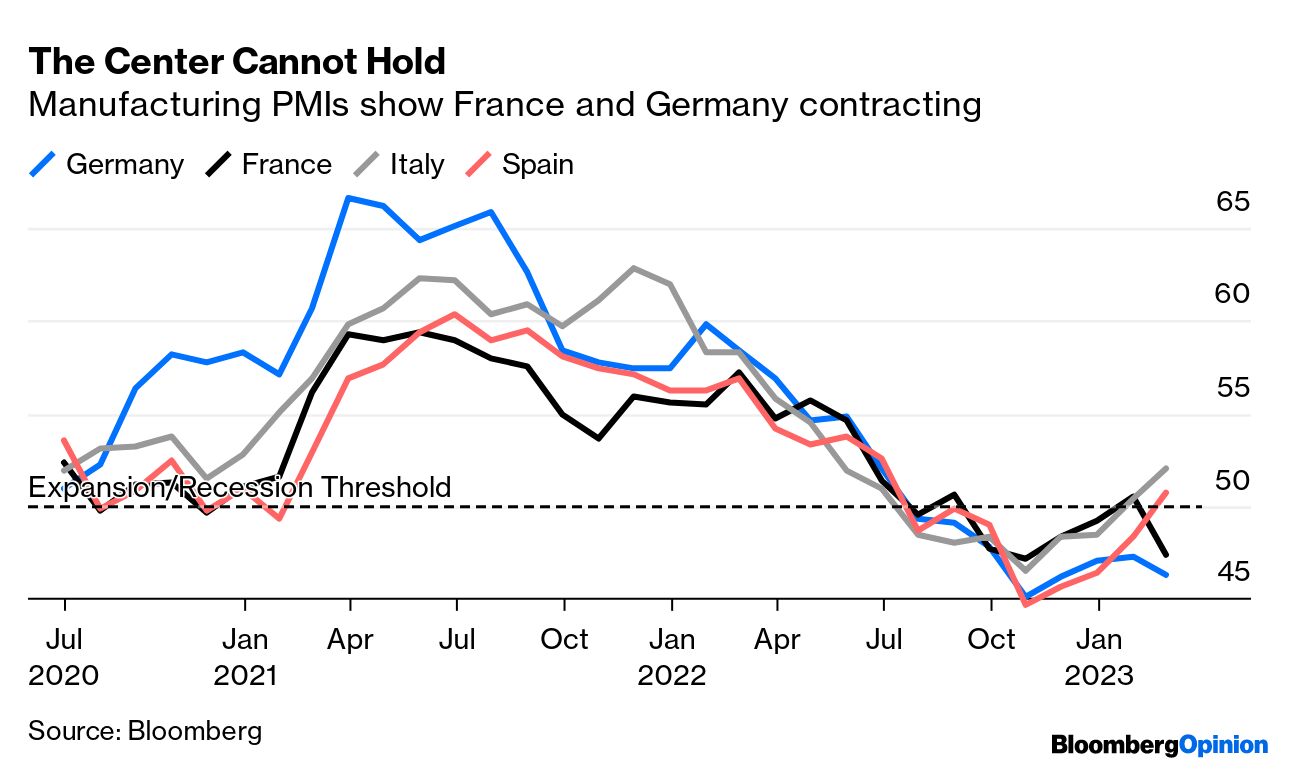

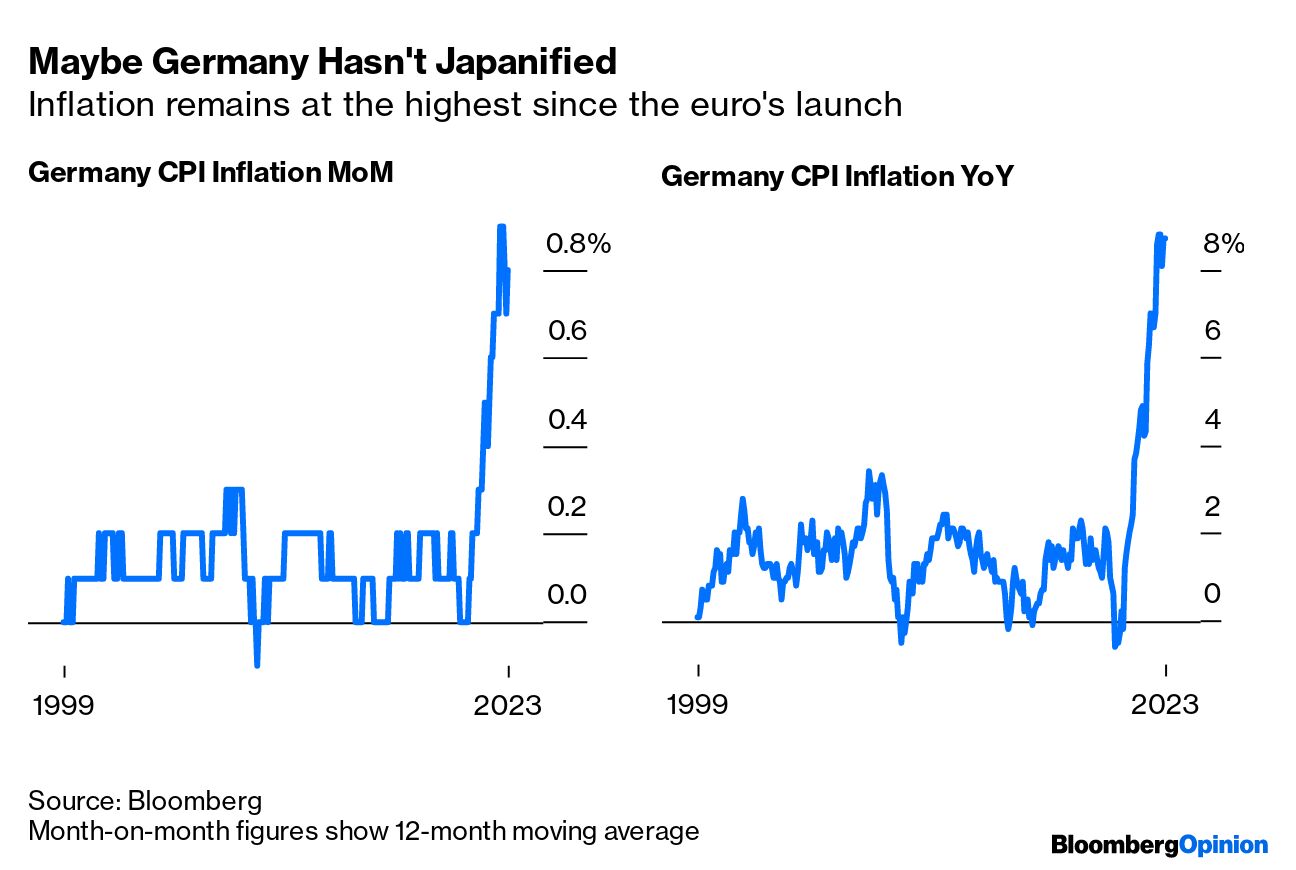

| March, like every month, has started with a wave of surveys updating us on the health of the economy around the world, and this download could make you as mad as a March hare. It suggests that global manufacturing is picking up a bit (good news), but that is leaving higher price pressures (bad news). Global purchasing manager indexes, charted here by Deutsche Bank AG, are back above the 50 level — the threshold between recession and expansion — for the first time in six months: An air of caution remains, possibly because managers are over-learning the lessons from the pandemic. Bill Adams, chief economist at Comerica Bank, commented that US businesses are adding to inventories more cautiously "to avoid being caught offsides as the broader economy cools." He said: "The precautionary purchases that businesses made during the shortages and supply chain turmoil of the last few years are things of the past." That means less of a rebound in activity, which appears to apply mostly to Europe and North America. As the regional breakdown shows, it does look as though the world made something like a coordinated low late last year, but the rebound is not too impressive so far, and distinctly being led by emerging Asia:  This adds ballast to the notion emerging from the data over the preceding weeks that a recession is not yet imminent. From this encouraging news, however, it follows that the drastic hiking campaign has failed, so far, to rein in prices. This shows up most dramatically if we look at the "prices paid" component of the survey. At one point, more than 90% of US manufacturers in the survey complained that their input prices were rising. That number collapsed as supply-chain problems eased — but there has now been a disconcerting rebound. The problem is nowhere near as severe as it was, but it adds to evidence that inflationary pressure isn't going away: Within the euro zone, the surveys demonstrated weakness for the central economies of France and Germany, while the "peripheral" countries, led by Spain and Italy, moved back into expansion territory. Germany has looked very weak on this measure for a while: That is a shame, because Germany also released inflation data, which remains distressingly high — indeed, it is the most elevated since the 1999 inception of the euro. If there is a positive to be gleaned from this, it's that the widespread belief in "Japanification" — that Germany had fallen into a deflationary slump like Japan's — appears to have been exaggerated. The bad news is that interest rates, which will have to be applied to all the countries of the euro zone, will probably have to keep rising to deal with the worst price pressures in a generation: That translated into a dramatic day in fixed-income markets. German two-year yields have broken above 3%. Having been negative for much of the last decade, they are now at their highest since the eve of the financial crisis of 2008. The post-crisis regime has been decisively broken: In terms of the calculus that matters most, the ISMs were strong enough to convince investors to raise their assumptions for rate hikes further, with a top fed funds rate of 5.5% now almost fully priced in. In Europe, overnight index swaps imply that the European Central Bank will have moved its policy rate above 4% by the end of the year, sharply higher than previous predictions. Have rate expectations over-compensated? Possibly. Joe Lavorgna, chief US economist at SMBC Nikko, argues that, historically, the Federal Reserve has tended to wait only three months between its last hike and its first cut. It's only in the low inflationary environment of the last three decades that rates have tended to be left at their highs for much longer than that. The difference is that none of those hiking cycles were anything like as aggressive as the current one. He said: "The past five episodes did not experience the rapid tightening of the current tightening cycle, which leaves us highly doubtful the Fed can keep rates in restrictive territory for as long as policymakers proclaim."  Overnight index swaps suggest that traders expect the Fed to take their time at the top. They imply reaching a peak in June, or possibly July, with an ensuing cut not fully priced in until January 2024. That would be a swift turnaround by the standards of this century, far slower than was typically seen over the decades before. If the economy has transitioned back to a regime where inflation is a constant concern, then perhaps it would also make sense for the Fed to revert toward speedier changes of course (or even, dare we say, "pivots"). The market was driven until recently by a narrative that the great tightening would be over by now, with rate cuts imminent. Now that that has been proved wrong, it's just possible it has over-compensated. At the beginning of the year, the most popular bet on Wall Street was to go long emerging markets. And it made sense, particularly due to the weakening dollar, which historically tends to push assets in the developing world higher. But after a February of rising rates largely canceled out the risk-on month of January, the question arises: Are markets back to where they started? They just might be. Emerging-market equities tumbled in February, with the FTSE Emerging Index losing more than 7%. China, despite the optimism surrounding its reopening, also lost ground — the Nasdaq Golden Dragon China Index fell 11%. As UBS strategists led by Mark Haefele wrote in a March 1 note, emerging markets are especially vulnerable to the risk of an extended series of Fed rate rises. The recent strength of the greenback also adds to the burden of dollar-denominated debt and tightens financial conditions. But if anything, China's February purchasing managers' index showed signs of a stronger rebound than expected after Covid restrictions were abandoned. The PMI, which Points of Return discussed briefly Wednesday, posted its biggest improvement in more than a decade with services activity climbing and the housing market stabilizing. This was not a given, as many had expected a wave of cases after the end of Covid Zero to weaken the economy. It looks like that hasn't happened: The data offered the first comprehensive insight into the economy's recovery after restrictions were dropped. It nicely dovetails with other signs of a rebound and put Chinese policymakers in a good position ahead of next week's National People's Congress, where a new growth target will be disclosed. And it's not just China. Deutsche Bank's Alan Ruskin points to a notable gap between a solid improvement in PMIs for EM as a whole, at 51.6, compared to only 48.1 for developed economies. The chart below shows the ratio between the FTSE Emerging Index and the FTSE Developed Index, which represents the performance of the large and mid-cap stocks from developed countries. The emerging index has just enjoyed its best day of outperformance since September. After a rout in mid-January, at least for the day — and despite higher rate expectations in the West — the EM trade is back on: Could this be a one-off reaction? Haefele expects a "renewed period of emerging market outperformance:" The broader EM rally looks likely to resume after a risk-off move in February. Within Chinese equities, we like the direct beneficiaries of reopening, including sectors such as consumer, materials, and transportation. Within currencies, we remain positive on the Chinese yuan as well as China reopening beneficiaries like the Australian dollar and the Thai baht.

While China will be the big driver, it should also benefit its neighbors in North and Southeast Asia as well as several commodity-sensitive emerging economies such as those in the Middle East, Africa and Latin America. On the corporate front, UBS also sees some earnings momentum and estimate revisions bottoming, both in absolute terms and in relation to developed markets. Here's a clearer picture of Wednesday's one-day gain, which was the biggest since November: Emily Leveille, portfolio manager at Thornburg Investment Management, also sees China's reopening as the key catalyst for EM optimism: That has legs and will play out this year in really interesting ways. We estimate that there's somewhere between 3 and 6 trillion renminbi in additional savings that were accumulated during the Covid crisis in China. So I think there's a potential for there to be a really strong reopening impact on names that are exposed to domestic consumption.

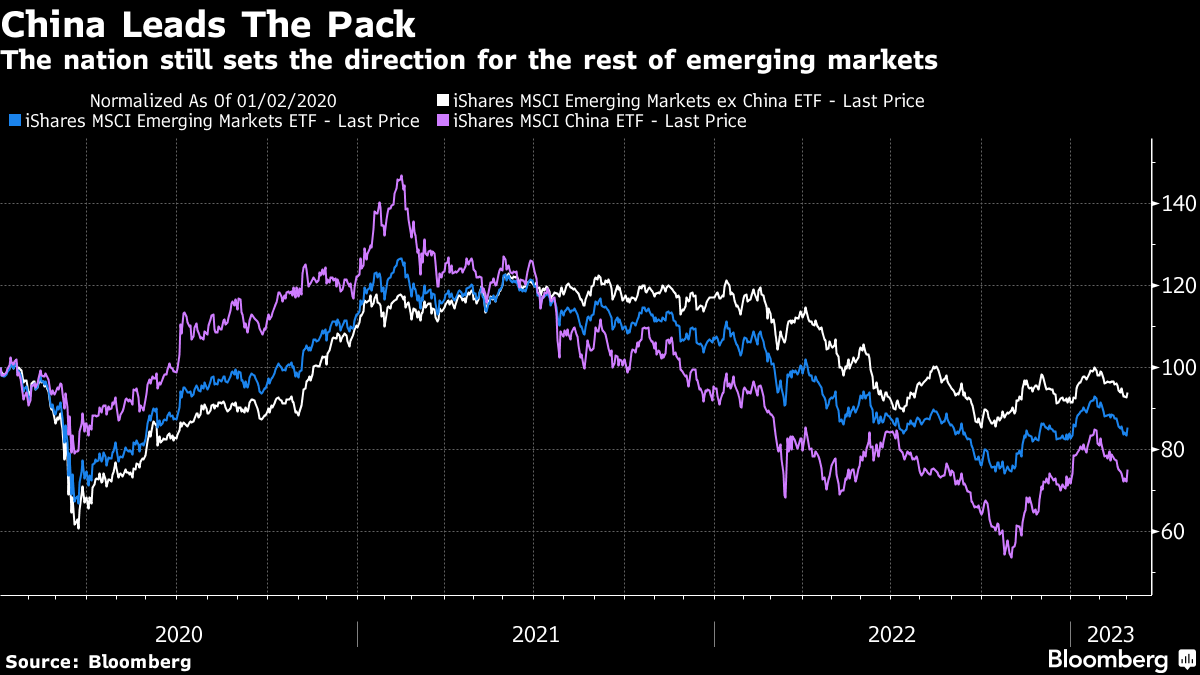

Even though China is increasingly treated as a separate entity from the emerging world, it continues to be pivotal, leading EM up when it is rallying, and acting as a lead weight when times are bad. This has held true throughout the pandemic era, despite the widely varying effects of Covid-19 on different countries. The following chart compares China to EM excluding China, and to EM as a whole, using exchange-traded funds based on MSCI indexes: Another critical point is that the March 1 jolt came just in time to rally emerging currencies against the dollar. After a brutal period of depreciation, JPMorgan's Emerging Market Currency Index had perked up and moved above its 200-day moving average, until the renewed fear about rates in February. It now appears to have bounced off that 200-day moving average. Technical patterns like these matter a lot in foreign exchange, and this might bolster EM currencies despite the pressure from higher rates in the west: All that to say, the annual NCP kicks off on March 5. Officials throughout China's system will unveil the major economic and social policies for the year. Michael Hirson of 22V Research said this meeting will have "added importance" as it's the first after the 20th Party Congress: Xi Jinping and his new leadership team are eager to use the meeting to boost confidence in China's recovery and longer-term outlook. However, there are trade-offs between Xi's broad priorities and what markets and the private sector would most like to hear, including guarding against financial risks vs. increasing stimulus, and consolidating Party control and "economic security" vs. pursuing liberalizing reforms. There is more room for the NPC to surprise to the upside on growth and stimulus than when it comes to reforms and governance.

Chinese assets tend to inflict a roller-coaster ride on their investors. The political obstacles have not gone away, and neither have concerns about corporate governance and shareholder rights under the increasingly autocratic Xi administration. But if enthusiasm survives next week's congress, China is ready for another sustained rally. — Isabelle Lee Far more important than ISM Day, March 1 is St David's Day, an opportunity to celebrate the patron saint of Wales. The Welsh have a singing tradition like nobody else; so you might try listening to Tom Jones, Stereophonics, Manic Street Preachers, The Alarm, or Feeder. Or for the really great stuff, in Welsh, try the great Bryn Terfel singing Calon Lan, or the Welsh national anthem Hen Wlad Fy Nhadau. Dewch ymlaen Cymru! Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. More From Bloomberg Opinion: Want more Bloomberg Opinion? OPIN <GO>. Or you can subscribe to our daily newsletter. |

No comments:

Post a Comment