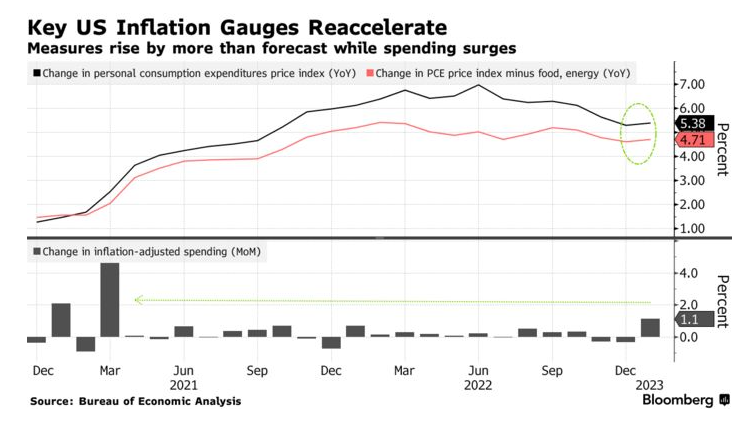

| Hello. Today we look at how some one-off factors might have distorted US economic data in January, the week ahead and a new study suggesting the Fed may need to do a whole lot more than markets expect. When it comes to the economic narrative, February has been something like a reverse of the old adage about March: it came in like a lamb and is going out like a lion. The story early on was that price pressures were coming down even as recessions looked less likely, amid still-solid growth. On Feb. 1, Federal Reserve Chair Jerome Powell crowed about how it was possible to say "for the first time that the disinflationary process has started." Things were then quickly upended by a slew of US reports showing the economy wasn't just doing OK, but was if anything running too hot. As Reade Pickert put it, the US was unseasonably hot in January, and data for the month showed it wasn't just the weather. But she notes how that strength came to some degree from a confluence of one-off factors: - Weather: Temperate weather boosted demand for things like restaurants and also drove an increase in hours worked. That likely bolstered the wages and salaries metric as well as overall consumer spending.

- Shifting shopping patterns: Many Americans did holiday shopping earlier, likely contributing to the back-to-back declines in consumer spending and retail sales in the final two months of 2022, setting the stage for a January bounce-back.

- Annual COLA: the annual cost-of-living adjustment for Social Security and Supplemental Security Income boosted incomes in January by the most in four decades. About 70 million Americans were affected, though a drop in other transfer payments worked in the opposite direction.

- Tax accounting: Incomes and savings in January were helped by a large decline in personal taxes. That drop "somewhat reflects" Bureau of Economic Analysis accounting, "rather than the true household experience," Wells Fargo economists said.

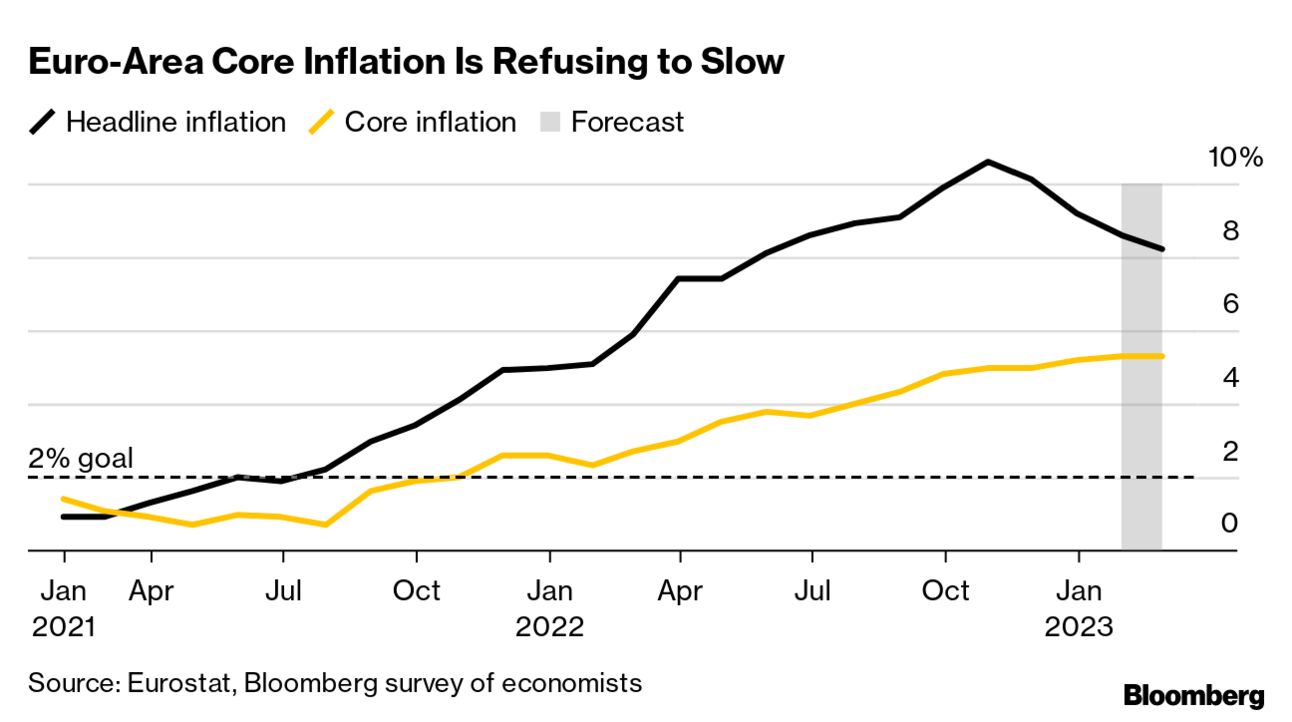

Some economists are warning a sharp reversal is still possible. Former Treasury Secretary Lawrence Summers, a paid contributor to Bloomberg TV, talks of a "Wile E. Coyote" moment — alluding to how the legendary cartoon character plunges all of a sudden into a canyon below. Summers pointed to bloated inventories among other signs. Mohamed El-Erian, the former Pimco CEO who's a Bloomberg Opinion contributor, agrees there is "evidence that the economy is slowing" amid the hot run of numbers. "This is a really tough environment both to predict and to invest," he said. The question now turns to how the February data look. The monthly purchasing manager indexes for manufacturing and services will offer an early read later this week. —Chris Anstey Fresh data from the euro zone are set to highlight why European Central Bank officials are maintaining their hawkish tone, even as the region's worst-ever spike in prices recedes. Economists polled by Bloomberg reckon headline inflation eased for a fourth month in February after warm winter weather sent natural gas costs tumbling. But the core gauge that strips out such volatile items will probably hold at a record 5.3% — its stickiness resembling the worrying picture in the US. The reading, scheduled for Thursday, will remain significantly above the ECB's 2% target. Alongside national data from the bloc's top economies earlier in the week, it will frame comments by half the Governing Council due to speak this week. Elsewhere, investors will be watching US sentiment gauges and global manufacturing PMI readings. Hungary and Sri Lanka are among the few central banks with scheduled rate decisions. See here for the rest of the week's economic events. - ECB bets | Traders are betting for the first time that the European Central Bank will extend its rate-hiking cycle into 2024, leading to a selloff in German debt.

- Continuity candidate | Kazuo Ueda said monetary easing should continue in support of Japan's recovery, a comment that suggests he won't seek an immediate change in policy if he is approved to helm the central bank.

- No statement | The world's top finance chiefs failed to agree on a consensus statement at meetings in Bengaluru due to an impasse over language on Russia's war in Ukraine.

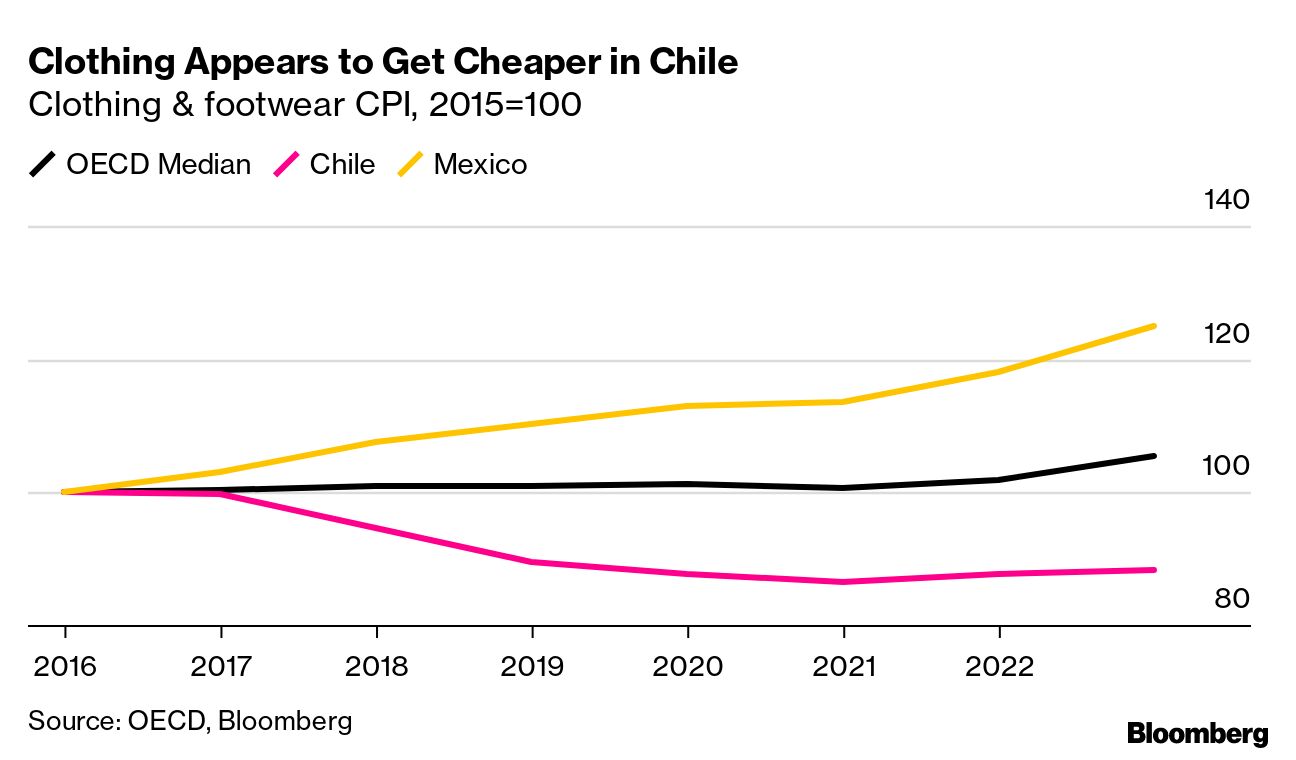

- Apparel puzzle | In Chile, economists are puzzled by a drop in clothing costs that contrasts with surging overall inflation. The disparity is reviving memories of a spat in 2013 over data methodology.

- Cost of koshary | Egypt's national dish is getting significantly more expensive to make, with the price of ingredients up almost 60%.

- Recession risk | Reserve Bank of Australia chief Philip Lowe's expectation of further interest-rate rises ahead has prompted economists and money markets to narrow the odds of a recession.

While futures pricing suggests the Fed will stop raising rates when it reaches about 5.4%, policymakers may in fact need to hike to as high as 6.5% to defeat inflation, according to a study by a coterie of well-known central bank watchers. The 55-page study included a series of simulations to predict likely paths for the Fed's benchmark rate. The computer models suggested a peak at either 5.6%, 6% or 6.5% in the second half of 2023. "In the current circumstances that already involve significant policy tightening (and a prospect for further restraint), an 'immaculate disinflation' would be unprecedented," the quintet of economists concluded.

Revisiting "voodoo economics"? Read more reactions on Twitter |

No comments:

Post a Comment