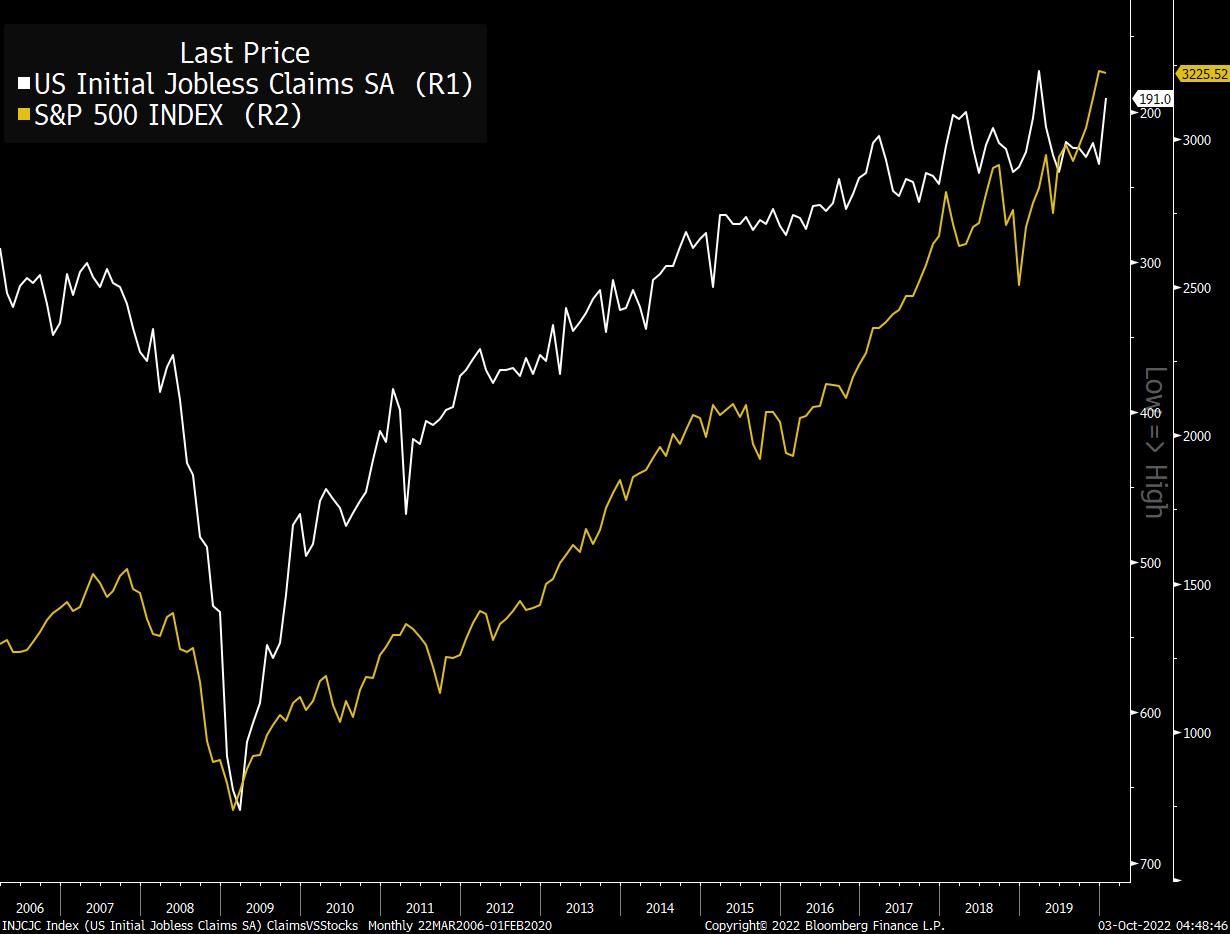

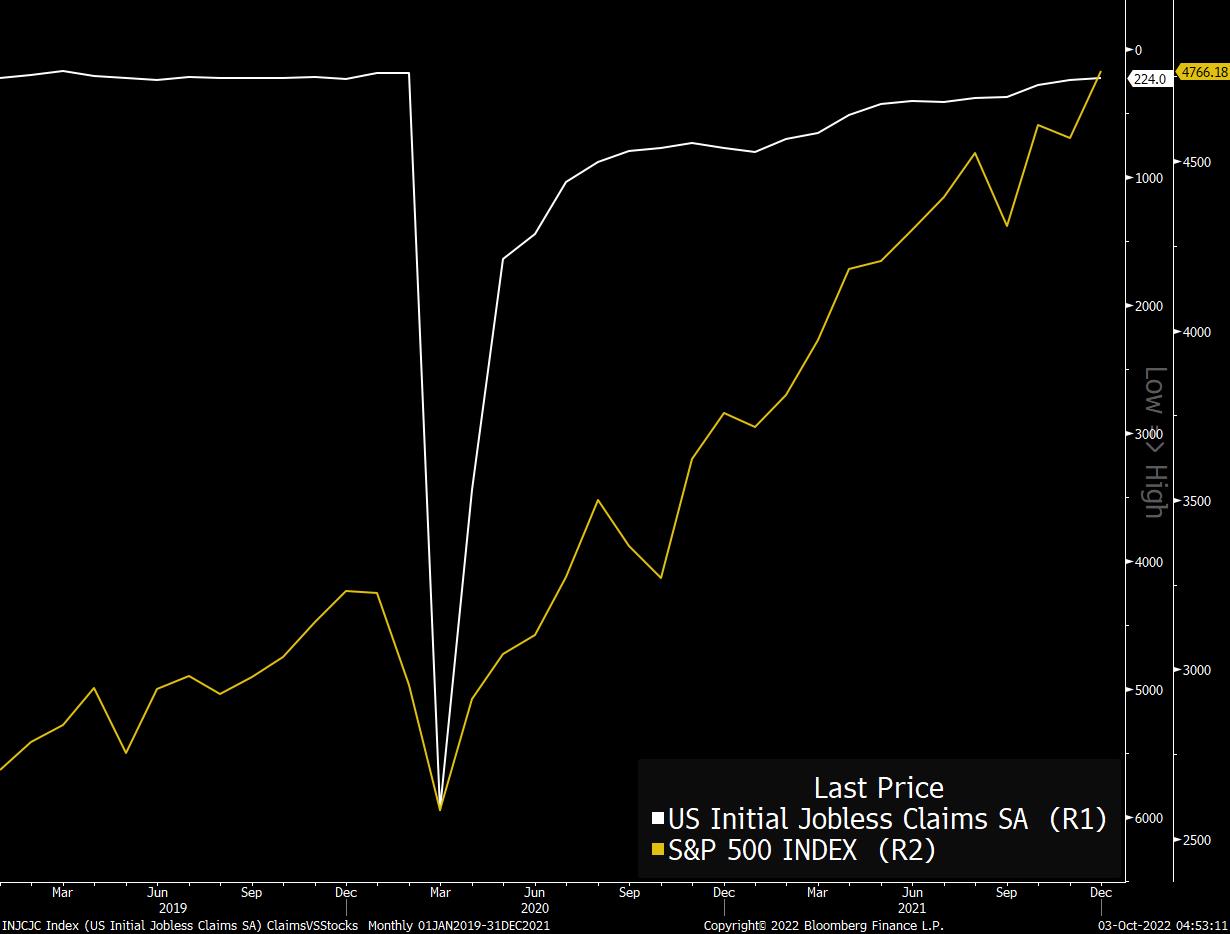

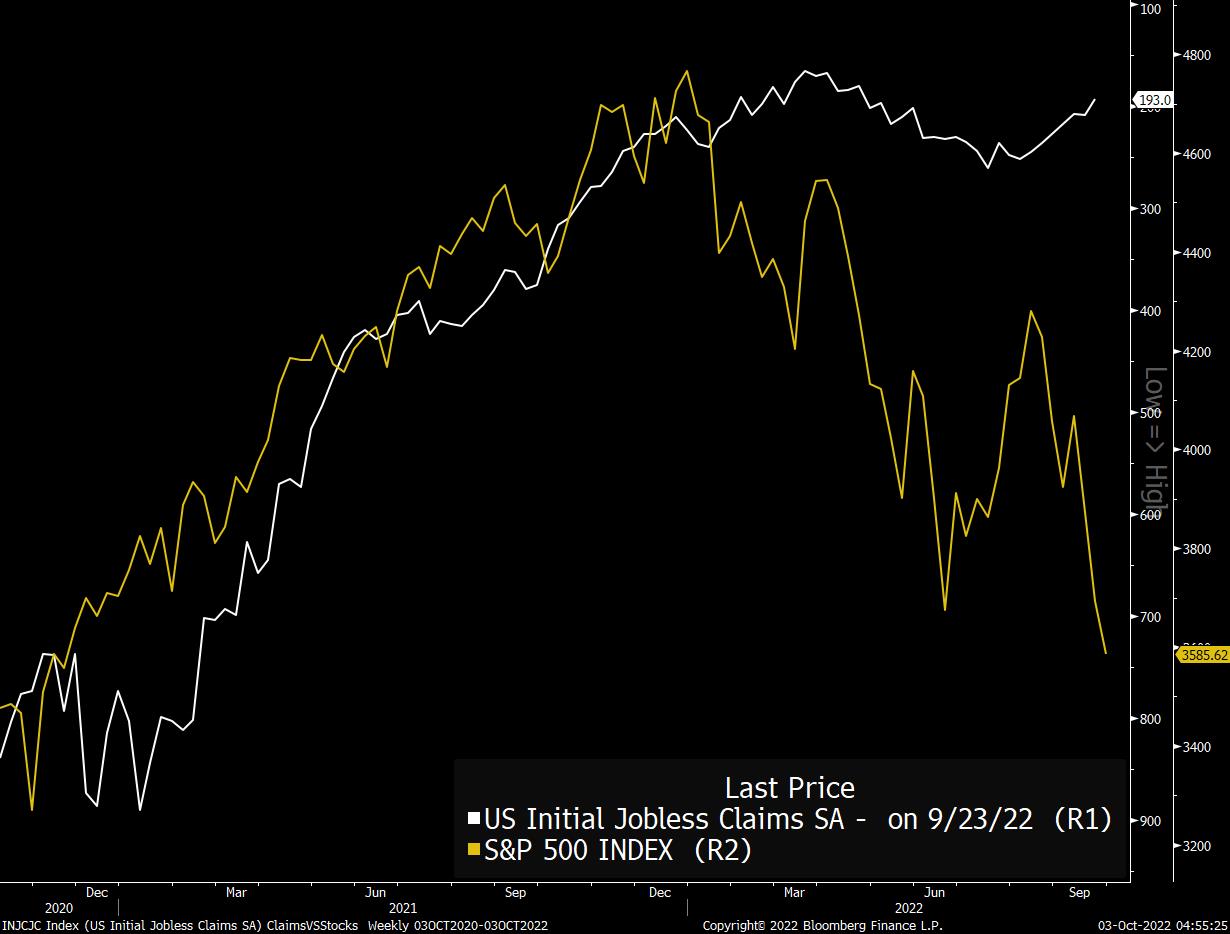

| Credit Suisse woes deepen, the UK makes a u-turn and stocks are upbeat to start the week. Credit Suisse's five-year credit default swaps — a gauge of credit risk — rose to a record while its stock hit a fresh low after the bank's attempts to reassure markets on its financial stability backfired. Chief Executive Officer Ulrich Koerner had sought to calm employees and the markets over the weekend only to see his carefully-worded memo have the opposite effect. While touting the bank's capital levels and liquidity, he acknowledged that the firm was facing a "critical moment" as it worked toward its latest overhaul. The bank sent around talking points to executives dealing with clients who brought up the swaps, according to people with knowledge of the matter. Credit Suisse declined to comment via a company spokesman. Prime Minister Liz Truss dropped a plan to cut taxes for the UK's highest earners just 10 days after it formed a key part of the mini-budget that sent markets into a tailspin. Investors initially welcomed the news, with the pound and government bonds climbing, but those moves quickly unwound. The future is looking uncertain too --options markets are still showing bearish bets, and "the market continues to view the government having something of a fiscal credibility deficit," according to CIBC's Jeremy Stretch.  | The incessant rise in the dollar has increased speculation that there will be a global coordinated effort to weaken it. Almost half of respondents in the MLIV Pulse survey believe central banks around the world will conjoin to curtail a rally that has taken the dollar 13.9% higher this year. Meanwhile, two-thirds of respondents believe the Bloomberg Dollar Spot Index will climb to yet new highs over the next month. Japan has already intervened to try to stem the fall in its currency versus the dollar, with 42% of survey respondents expecting the country to intensify its unilateral intervention efforts. The dollar's ascent is also expected to squeeze US earnings, with almost 90% expecting this to become apparent in third quarter results. European stocks and US futures have bounced off session lows yet soured sentiment dominates as the fourth quarter begins. S&P 500 futures trade about 0.1% higher while tech-heavy Nasdaq 100 contracts slip about 0.3% as of 6:15 a.m. New York time. In Europe, Stoxx 600 declined about 0.8% as tech, industrial goods and financial services lagged while energy outperformed. Treasuries across the curve rallied, led by the short-end. The Bloomberg Dollar Spot Index is 0.1% firmer. Oil rallied on prospects of an OPEC+ oil production cut. Manufacturing data is in focus today, with the S&P Global print at 9:45 a.m. and ISM at 10 a.m. The ISM data include prices paid and new orders. Canada also has S&P Global manufacturing PMI. The Fed's Raphael Bostic and John Williams speak. There's also light vehicle sales. Here's what caught our eye over the weekend: Hello, and welcome to Jobs Week. This Friday we get the September Non-Farm Payrolls report, where 250K jobs are expected to have been added. And also this week we'll get a JOLTS number and initial jobless claims. So a big week for labor data all around. But let's talk about initial claims for a second. For years after the Great Financial Crisis, this was one of my favorite charts. It shows the S&P 500 vs. weekly initial jobless claims (reversed, so that up is fewer). And while no two lines are ever perfect, they broadly moved in the same direction at the same time. As claims improved, stocks improved. And both had some rough patches at the same time. 2011 there was a significant weakening of jobless claims (lots of double dip recession talk that year) and a selloff in the stock market. Similar story with 2018 and 2019. Some hiccoughs at the same time in the same direction. The relationship even held during the 2020/2021 craziness, with the S&P 500 bottoming the same week as initial claims hit their worst point. But now the relationship is gone. Initial jobless claims have been improving ever since the middle of the summer, and yet the market has been tanking. In fact last Thursday was a particularly brutal day for the market, right after initial jobless claims came in sub-200K, stocks fell by roughly 2%. In the post-GFC environment, good news was good news. As the labor market continued to heal, stocks went up in a fairly straightforward manner. In 2022, labor market strength is simply seen by the market (in part because of Fed messaging) as simply worsening the inflation picture. And so "good news" (on the jobs front) is no longer a welcome development for investors. Follow Bloomberg's Joe Weisenthal on Twitter @TheStalwart |

No comments:

Post a Comment