| Shanghai's residents are finally getting a real taste of freedom.

After a three-month lockdown — including half-hearted easing measures that only served to torment the city's population of 25 million — Shanghai re-opened June 1. No longer do people have to request permission to leave their residential compounds, nor are they swabbed for Covid on a daily basis. Trains are running again, shops are re-opening and ride-hailing services can pick up passengers.

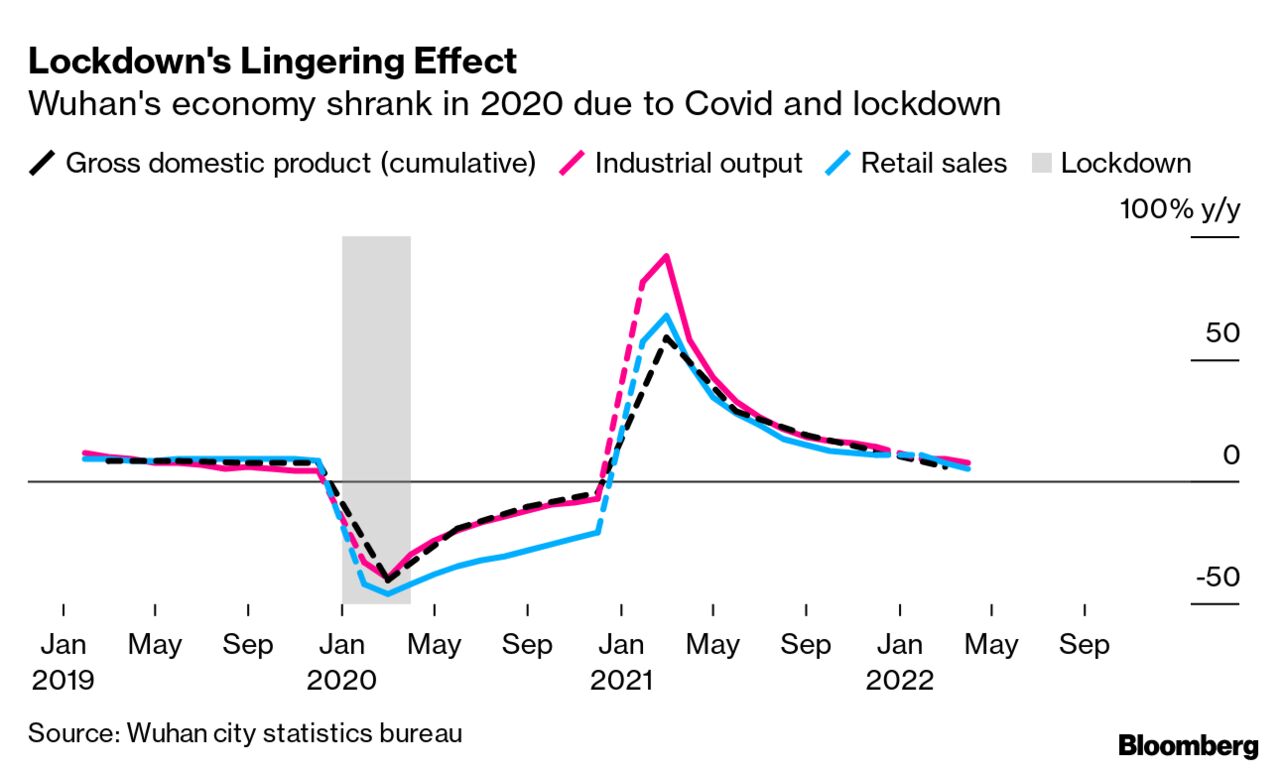

It's not all smooth sailing. Some 10% of the population in high-risk areas are still locked in, gyms and cinemas remain shut, and residents need to hustle to get a negative Covid test result within the past 72 hours to enter public spaces. Even so, reaction to the good news was swift. The newly released cheered their freedoms with fireworks and parties in their housing compounds. Some fled to Hong Kong. Investors bid up stocks. Bloomberg's Allen Wan marked his first day of freedom with a celebratory beer at a Family Mart and a trip to the barber. He took the subway to Lujiazui, China's version of Wall Street, to see what obstacles he and other residents would continue to face on their return to the office. His journey can be viewed here. While the government is finally relaxing its strict curbs as cases plunge, Shanghai faces weeks, if not months, of slow recovery until economic activity can fully bounce back from the crippling lockdown that began in March. Based on the experiences of other cities like Wuhan in 2020 and Jilin earlier this year, it will take time for shops to reopen or factories to secure supplies and ramp up production. Several companies said they can't fully restart their operations despite the easing because of supply chain issues. "We're talking about long supply chains that have been disrupted for more than eight weeks so it will take some time to stabilize," said Eric Zheng, president of the American Chamber of Commerce in Shanghai. And while truck traffic in Shanghai has started to gradually pick up as the city relaxes Covid restrictions for drivers, it's still less than 30% of the weekly average in 2019. For thousands of small and midsize companies, the reckoning has just begun. Gracell Biotechnologies is one such firm. The lockdown made it impossible for the Nasdaq-listed drugmaker to export sophisticated components intended for cancer therapies, and complicated a clinical trial of a drug for late-stage cancer patients. Some larger manufacturers including Tesla are telling workers they need to stay in a so-called closed loop — where they can't leave the factory and must be tested regularly — until June 10 as a buffer to ensure production stability. Millions of twentysomethings, meanwhile, are struggling to find jobs as the pandemic and government regulatory crackdowns upend their career ambitions. Perhaps they should look to Covid testing. Companies are dangling monthly salaries exceeding 10,000 yuan ($1,487) to recruit staff to work the network of tens of thousands of lab testing booths being set up across the country's largest cities, with the goal of having residents just a 15-minute walk away from a swabbing point. This will allow cities to require tests as often as every 48 hours, with negative results needed to get on the subway or even enter a store.  A permanent PCR testing booth in Shanghai on May 31. The Shanghai government issued a thank you letter to its citizens, pledging to "spare no effort to promote the full restoration" of normal life and to "do our best to recover the time and losses caused by the epidemic." Money would help, but like most of the financial aid China has rolled out, much of Shanghai's recovery plan is focused on businesses and production. Households haven't been given direct financial support, like the cash handouts that have cushioned consumers from the blow of Covid lockdowns in the US and in Europe. The letter, which trended on China's Twitter-like Weibo, received criticism online, with people saying it should have been an apology, and calling for punishment of the experts who led the virus response. The Tom Cruise blockbuster "Top Gun: Maverick" raked in a cool $124 million in its opening weekend in North America. Too bad it probably won't make a dime in China. That's because the movie, which follows Cruise's character as he trains a group of young fighter pilots, likely won't get a release in the world's biggest film market. Tencent had signed on to co-finance the film in 2019 but pulled out over concerns the movie glorifies the US military, according to the Wall Street Journal. Another no-no for Beijing: Cruise's character wears a bomber jacket with the Taiwanese flag, something considered an independence symbol by China, which views the island as part of its territory.  Tom Cruise in "Top Gun: Maverick." The flag was either missing or couldn't be seen properly in a trailer for the film in 2019, prompting some people to wonder whether it had been removed to satisfy demands from China's censors. But when the full movie recently hit theaters, keen observers noted that the flags had made a comeback. Similarly, the Japanese flag was reinstated. The decision to keep the flag on the back of the jacket worn by protagonist Captain Pete "Maverick" Mitchell suggests that at least some Hollywood executives might be turning a new page when it comes to Chinese censorship. "Hollywood is now pushing back," said Chris Fenton, a former movie executive. "The market is simply not worth the aggravation anymore in attempting to please Chinese censors." Hollywood and foreign film studios are facing growing challenges in China as authorities tighten control over content. Walt Disney's Marvel film "Eternals" wasn't screened in the country after comments made by Chinese director Chloe Zhao almost a decade ago were deemed critical of the nation. It would be a shame if Chinese audiences can't go to the movies to see the sequel to the 1986 hit. The new film, which waxes nostalgic and signals a return to normalcy as audiences return to theaters in the age of the pandemic, scored a 97% critical approval rating on RottenTomatoes.com. It's also a tough time for Chinese movie stars in China. Jing Tian, an actress in several Hollywood movies such as "The Great Wall" with Matt Damon and "Kong: Skull Island," was slapped with a million-dollar fine for breaching the nation's advertising law by touting candies as a weight-loss drug.  Jing Tian. In the ads, which have since been pulled from e-commerce sites such as Alibaba's Taobao and JD.com, the 33-year-old actress said that people could keep in shape by taking two "candies" after eating a meal. The local regulator imposed a 7.22 million yuan ($1.1 million) fine, saying ordinary food can't be claimed to have therapeutic effects under the advertising law. Jing is the latest celebrity to be caught up in a year-long crackdown on the entertainment industry. Regulators have targeted what state media outlets have characterized as "improper" idol worship, excessive wealth held by some and dubious tax practices. The Chinese cyberspace regulator last year told social media platforms to remove all rankings of celebrities. One of China's most popular film stars, Zhao Wei, was blacklisted from the nation's internet, and actress Zheng Shuang was ordered to pay 299 million yuan in overdue taxes, late fees and fines. Jing, who raked in 2.6 million yuan in "illegal income" from the endorsement, apologized on Weibo, saying she didn't do enough due diligence when she signed her contract. You think? It's shaping up to be another rough year for startups seeking Chinese moolah. China is leading the global decline in venture capital investments, with the value of deals in the country tumbling 44% from a year earlier to $24.7 billion in the first four months of the year, according to research firm Preqin. That's almost twice the rate of decline in the US and nearly four times the pace of the global slide. There are several reasons for the turnaround. After more than a decade of surging valuations, the broader tech sector has been taking a beating, with companies like Amazon and Tesla tumbling and venture investors pulling back from high-risk deals. China's regulatory crackdown on the industry and lockdowns in cities like Shanghai also dampened the mood. Sequoia Capital warned founders and chief executives that the good times are gone. "Rates are rising, money is no longer free, and that has massive implications for valuations and fundraising," it said. When there is investment, it's often going to sectors favored by the Chinese government, including renewable energy and electric vehicles. Under President Xi Jinping, Beijing has prioritized key industries, including semiconductors and artificial intelligence. The biggest deals so far this year include an $800 million Series B round for a supply chain technology unit of JD.com driven by Hillhouse Capital and Warburg Pincus, and a 5 billion yuan ($750 million) bet on chipmaker Guangdong Fenghua Advanced Technology from investors including UBS, according to Preqin. The situation isn't much better for companies seeking to IPO in Hong Kong, where only one company sold shares for the first time in May. The proceeds raised were the lowest for that month in 10 years. Yunkang Group, a Chinese company that offers diagnostic services including Covid tests, raised $139 million in its IPO.

Sometimes it feels like Covid testing is the only surefire growth industry. Finally, a few other stories that caught our attention: - This is the space station China is building to challenge the US

- Activists say UN rights chief's China trip whitewashed abuse

- Communist Party expels ex-Nanjing chief for faking economic data

- Taiwan pilot dies in third military jet crash this year

- China mocks Biden's economic pact for failing to lower tariffs

- A photographer records Shanghai's final days before lockdown

|

No comments:

Post a Comment