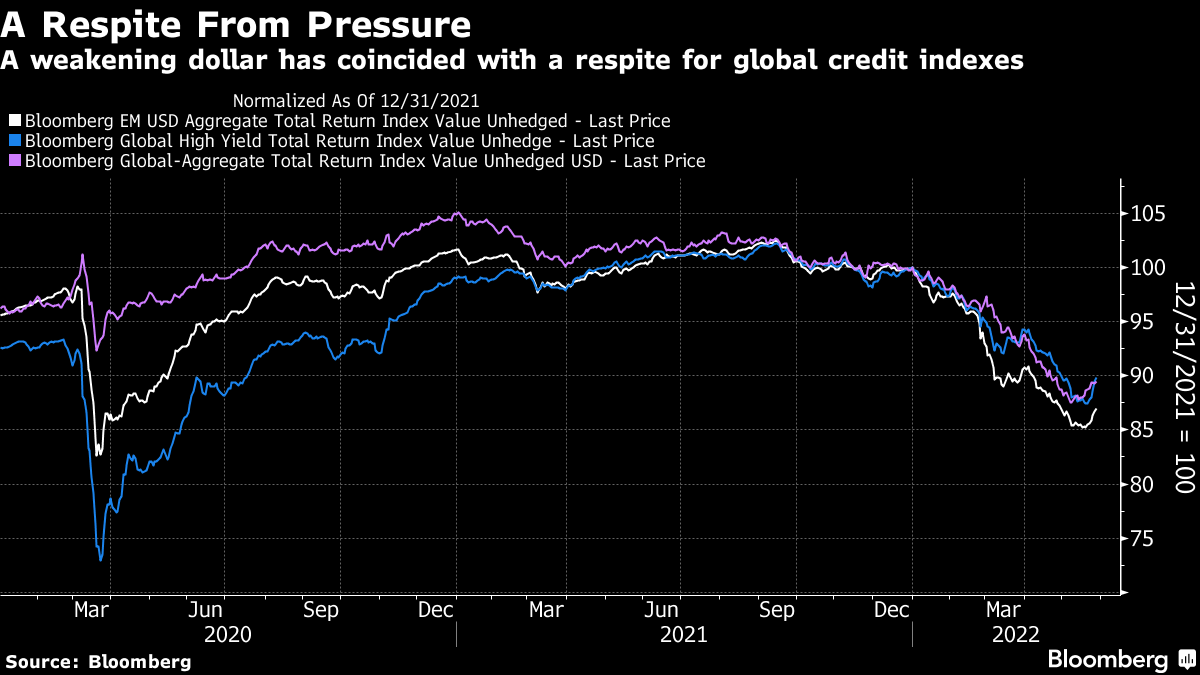

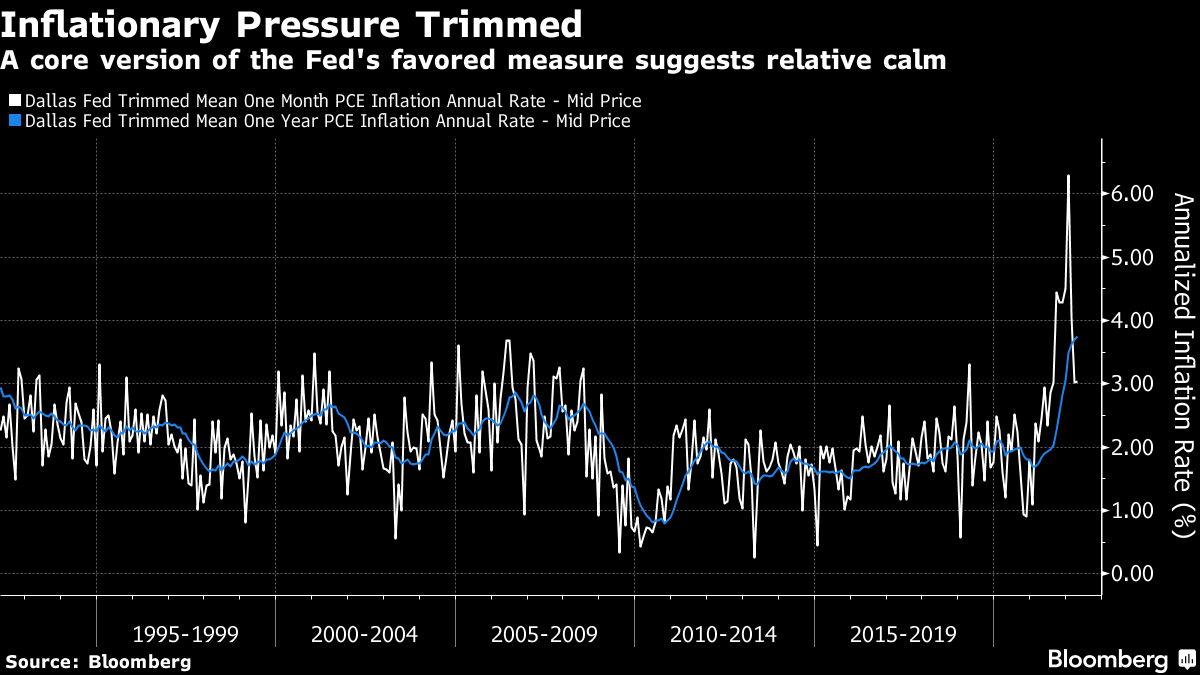

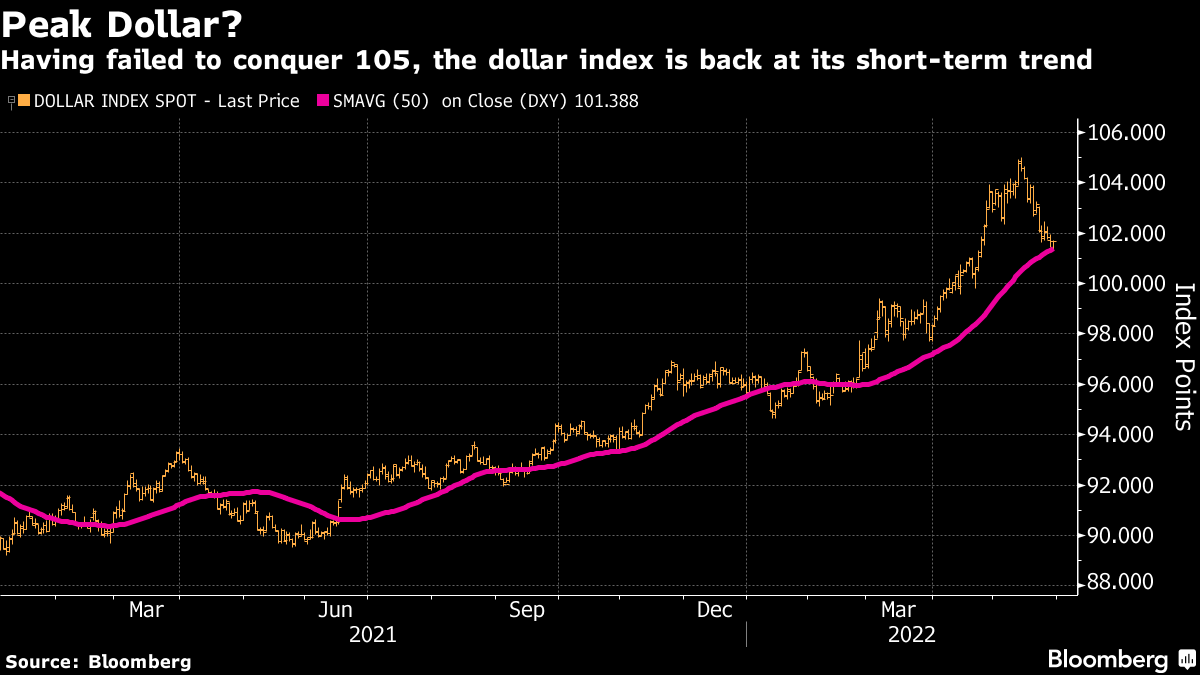

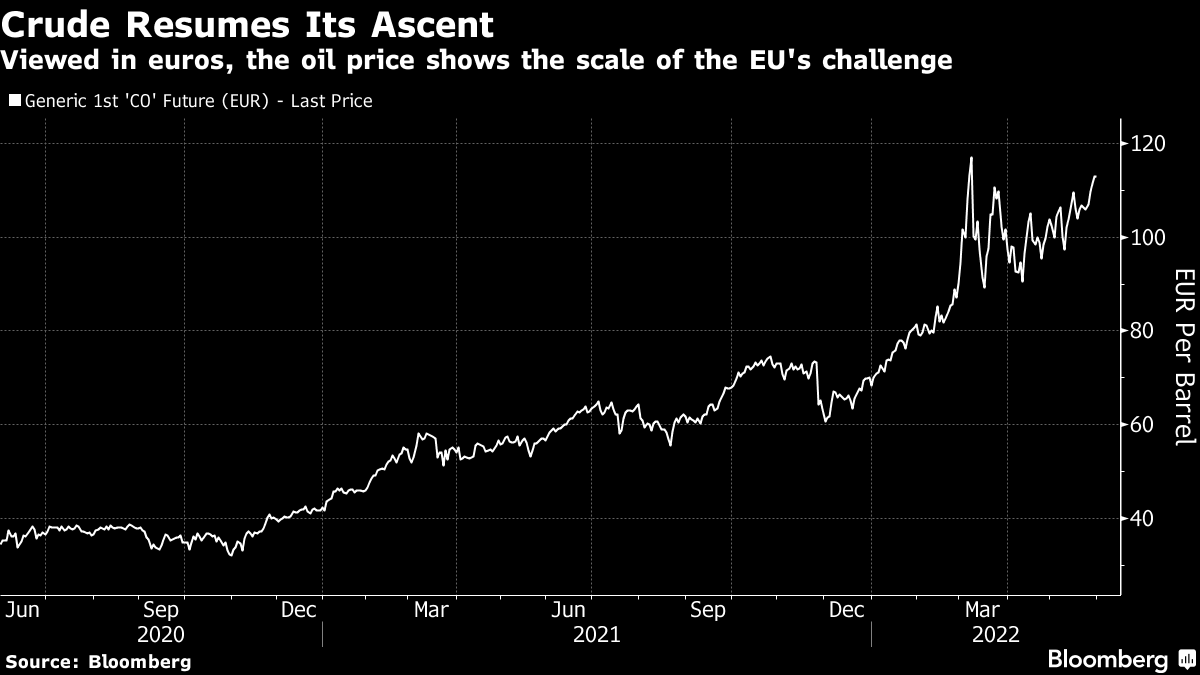

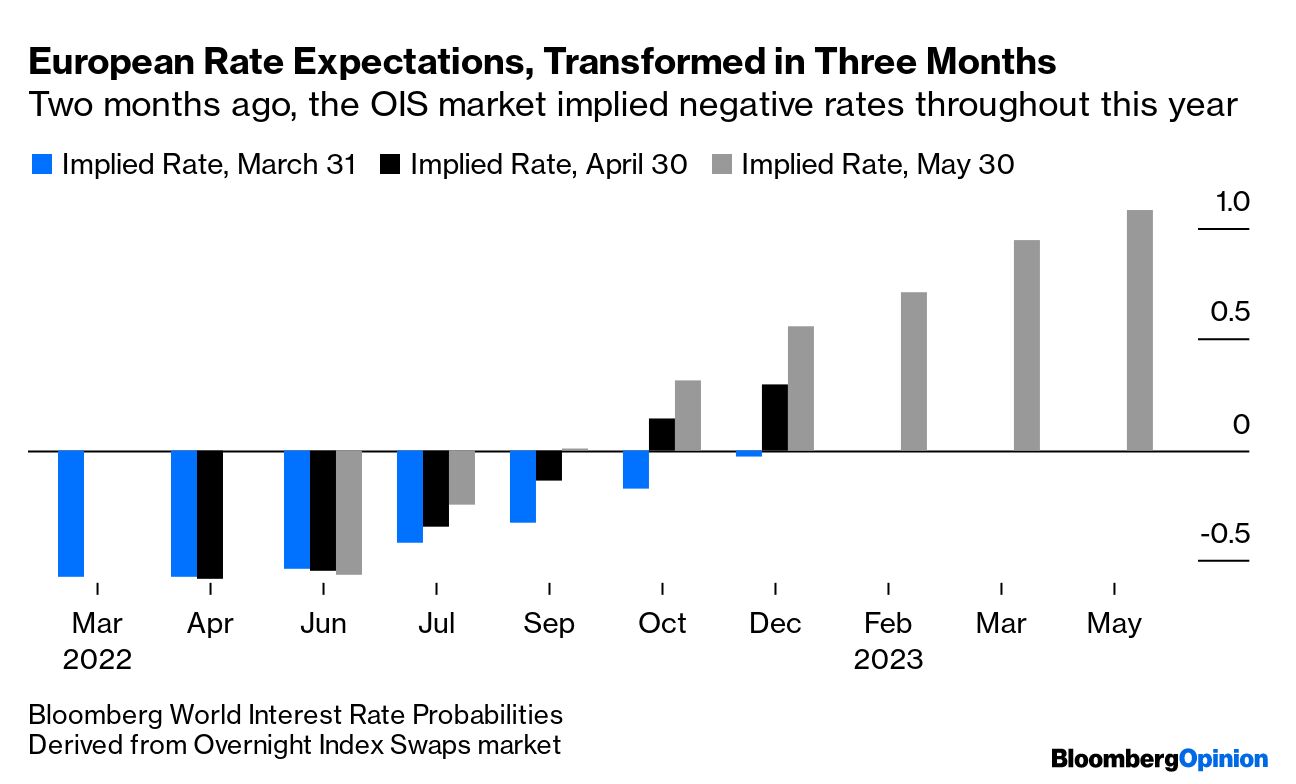

| As Americans return for a shortened week, it looks like they only missed more of the same. US stocks gained last week, breaking a losing streak, and the enthusiasm has continued. Can this be justified as anything more than a trading bounce of the kind that comes along in all bear markets? There's a way to do that (just about), but the news flow provides as many new reasons for concern as it does to relax. A key measure of risk is the dollar. When people are risk-averse, they tend to pile into the US. That makes them a little safer, but in turn makes life even worse for anyone needing to buy dollar-denominated commodities or repay US currency debt. The broad dollar index is beginning to look as if it is turning. For the first time since the initial week of the Ukraine invasion it has dipped below its short-term (50-day) moving average. So that's something: The easing pressure on debt, particularly in emerging markets, is already noticeable. Global credit indexes are still sitting on serious losses for the year so far, but Bloomberg's index of dollar-denominated emerging market debt, particularly hurt by the selloff of the first five months of this year, has recovered a little. The slackening of dollar strength is also soothing fear of risks to solvency:  More or less every other measure of bonds' price performance has also risen this month. Meanwhile, the latest inflation data are basically positive for anyone who doesn't want to see base rates move much higher than they are now. The end of last week saw publication of the Personal Consumption Expenditure inflation rate for April — the Federal Reserve's favored measure of inflation. The Dallas Fed provides a "trimmed mean" version of this gauge, which excludes the biggest outliers in either direction and takes the average of the rest. This is arguably a purist's best indicator of core price pressures in the economy. On a year-on-year basis it edged up very slightly. For the second month in a row, price rises were relatively contained at an annualized rate of only 3% month on month:  This certainly doesn't prove that the inflationary wave is over or that we have nothing more to worry about. It does provide some fairly good reason to hope that the Fed won't have to hike rates too far, and that inflation fears may have been overdone. It also provides a good excuse for a risk-on respite after a brutal start to the year, which is what we're seeing. However, there may be a limit to how far this can go. An inflation scare can easily morph into a growth scare, as central banks do more than enough to keep price rises under control. This raises hopes that both stocks and bonds can rise together (as they have done recently), but it's not greatly helpful for the future. And what would normally be positive signals for growth can easily tip over into reasons to fear more inflation. One critical problem remains unresolved; even excluding all the imponderables from the huge injections of cash two years ago that must be steadily withdrawn, there are two big geopolitical issues that need to be resolved. How will Russia's invasion of Ukraine be concluded and with what impact on future trade flows? And how will China emerge from its shutdowns to combat Covid-19, and with what permanent impacts on its economy? Either could quite conceivably tip the balance into either inflation or deflation. China's latest news is positive, as the government announces both that it is rolling back restrictions on movement and that it is trying to stimulate the economy. That augurs well for the future, although backward-looking data make plain that lockdowns slowed the country significantly. The May manufacturing Purchasing Managers' Index, released Tuesday morning in Asia, improved to 49.6 though remained below the 50 level that divides expanding from contracting conditions. There is a downside to economic recovery, which is that it adds to the demand pressure on commodities, most significantly oil. Speculation that China would soon be back to buying and burning oil at its old clip helped buoy the price of crude. Brent is now back to its highest level since the first few days of the Ukraine invasion. Viewed in euros, oil's rise in the last two years is spectacular: That is profoundly unwelcome because oil matters a lot to consumers. Energy and food prices are hard for central banks to control, which is why the core measures that policy makers often monitor exclude them. But it is the "headline" inflation rate, including both, which is most politically salient. And the latest headline inflation numbers in Germany must be dreadful for politicians to read. Increases in both food and energy prices are far above anything seen before: Numbers like this intensify the pressure to do something. That shows up in a transformation of expectations for the European Central Bank's likely path. The following chart is generated using the Bloomberg World Interest Rate Probabilities function (WIRP <GO> on the terminal), and shows the predictions for euro-zone base rates at each of the next ECB meetings, as produced by the overnight index swaps market on May 30, April 30, and March 31: Two months ago, the ECB was expected still to be stuck with negative rates at the end of this year. No longer. Markets have sped to price in an aggressive tightening campaign. That in turn helps strengthen the euro, and weaken the dollar, as U.S. rate expectations have been stable for a month now. That does help those who want to get risk "on" again. But it is driven by decidedly risky developments. Most importantly of all, the week starts with news that the European Union is getting its act together for what looks likely to be a far more effective and painful boycott of Russian energy imports than many had expected. At the time of writing, the latest news is that the EU would prohibit "the purchase of crude oil and petroleum products from Russia delivered to member states by sea but include a temporary exemption for pipeline crude." This was from the president of the European Council, Charles Michel. If the EU goes through with this, which would be its sixth separate package of sanctions since the invasion, it would hurt the Russian economy, but also resume the upward drive in the oil price. If growth is slowing, that generally spells problems for commodity prices, as Gary Shilling pointed out in Bloomberg Opinion last week. Artificially tightened supply could yet push prices up further even as the economy slips into the doldrums. May has seen a reset, as investors factor in the strong chance that the Fed will be unable to tighten as much as it wants. That has eased pressure on currencies and credit around the world. This can have its own self-reinforcing reflexivity. But let's not take things too far, ahead of a short week with plenty of macro data. If the reason we needn't worry about inflation is slowing growth, that's not great. And if exogenous political factors keep the oil price high, one of the concerns that got the inflation scare going in the first place, then stagflation is a real possibility. Risk-on rallies are fun, and they hurt those who are bearishly positioned; but they create the opportunity to lose yet more money when the next risk-off wave comes along. I have a reading recommendation, which is only about two years late. For a book club, I'm reading The Plague by Albert Camus, and it's brilliant. During the first weeks of the pandemic, it became very popular, for obvious reasons. Reading it now, it's startlingly prophetic about exactly the reasons that would lead mankind to make a mess of dealing with the worst global pandemic in a century. This section caught my eye: "The public's reaction was not immediate. The announcement, in the third week, that the plague's death toll had reached 302, actually seemed inconceivable. On the one hand, perhaps not all of them had died of plague. And, on the other hand, no one in the city knew, in ordinary times, how many people died per week. The city had 200,000 residents. People didn't know if this rate of deaths was normal. It was the exact kind of detail that no one ever bothered with, despite the obvious interest it presented. The public lacked, so to speak, any point of comparison."

Camus has far more profound topics in mind than problems in understanding statistics. But it's still fascinating that comprehending the problem, and the need to use to statistics to do so, rears its head early in his novel. And of course, this sounds exactly like the debates that split society two years ago. For light on how difficult it was for us all to find a point of comparison in the spring of 2020, I recommend this excellent podcast, in which Michael Lewis enlists the help of Columbia University's brilliant statistics professor Andrew Gelman and others to pull apart the early statistical offerings from experts when the coronavirus began to spread. There has been much attention for those who overestimated the potential toll in March 2020 — mostly for forecasters like Neil Ferguson of Imperial College, London who were held to have exaggerated the threat. His team predicted that even with measures to flatten the curve, the UK would have 250,000 fatalities. The latest official total is 179,000. That had a huge impact on British policy, but has subsequently been labeled alarmist. Meanwhile, Lewis and Gelman concentrate on John Ioannidis of Stanford University, who counseled caution on data, including this fateful paragraph, in the spring of 2020: If we assume that case fatality rate among individuals infected by SARS-CoV-2 is 0.3% in the general population — a mid-range guess from my Diamond Princess analysis — and that 1% of the U.S. population gets infected (about 3.3 million people), this would translate to about 10,000 deaths. This sounds like a huge number, but it is buried within the noise of the estimate of deaths from "influenza-like illness." If we had not known about a new virus out there, and had not checked individuals with PCR tests, the number of total deaths due to "influenza-like illness" would not seem unusual this year. At most, we might have casually noted that flu this season seems to be a bit worse than average. The media coverage would have been less than for an NBA game between the two most indifferent teams.

The latest confirmed death toll in the U.S. is now 1.005 million. On the face of it, this is a far more serious underestimate than Ferguson's overestimate. There is a fascinating debate over how statistics should be presented at times of great stress, and both the Ioannidis and Ferguson estimates, hugely influential over future policy, appeared defensible at the time they were made. But they show that Camus was right that the public lacks any point of comparison in the early stages of a pandemic, making uncertainty all the greater. And Gelman, who was able to find significant flaws in a research paper produced by Ioannidis and 16 Stanford colleagues, suggests that they should have directly admitted to making a mistake. And for something a little lighter, you could also try listening to the greatest Camus-inspired song ever recorded, The Cure's Killing An Arab, which is based on L'Etranger. It's also the only Camus-inspired song I'm aware of, and I'm happy to hear of others, but it does sound great live. Have a great week everyone. More From Other Writers at Bloomberg Opinion: Want more from Bloomberg Opinion? Terminal readers head to {OPIN <GO>}. |

No comments:

Post a Comment