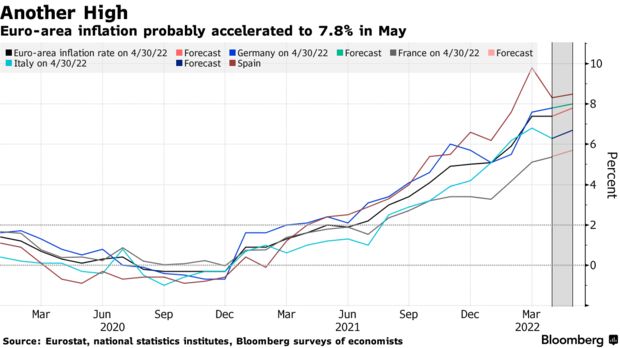

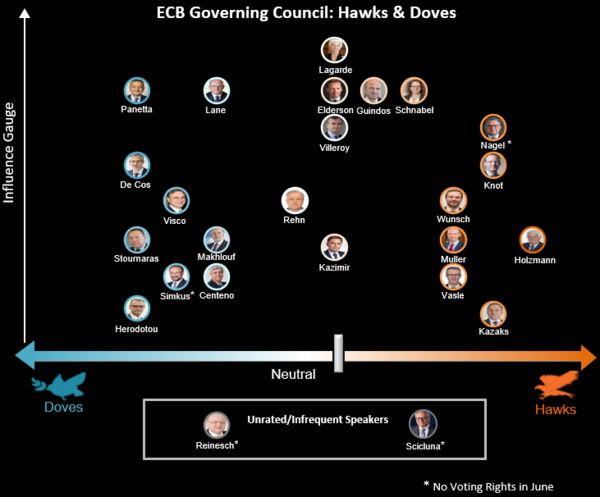

| Hello. Today we look at the inflation outlook for the euro area, the week's coming economic events and what prices are surging in the UK. Euro-zone inflation isn't as fast as in the US, but it's getting there — and so is the argument over whether to start hiking interest rates just as quickly. Annual consumer-price growth in May is likely to have hit yet another record in the history of the currency area, with the median forecast of economists now at 7.8% for the region's data due on Tuesday. Setting the scene later today will be inflation in Europe's biggest economy, Germany, which is seen jumping to 8.1% — close to the 8.3% level seen in the US in April. Meantime, data already out today showed Spanish inflation unexpectedly quickened, denting hopes that the euro area's record price surge is peaking. As Alessandra Migliaccio explains here, such numbers are likely to intensify the discussion on how fast the European Central Bank should raise rates. With a hike now penciled in for July, hawkish policy makers are saying that a half-point move — just like the Federal Reserve delivered earlier this month — can't be ruled out. "Everything else risks being seen as soft," Austria's Robert Holzmann told Bloomberg last week.

His Dutch colleague Klaas Knot, who is also wondering aloud about such a hike, points to inflation and associated underlying indicators as key data to watch. "These new numbers are extremely important to determine the speed at which rate hikes will need to happen," said Giorgio di Giorgio, a professor at Luiss University in Rome. "There's a real tangle of factors that have come together to complicate the picture, from the pandemic to supply bottlenecks, then the war in Ukraine, now China's zero Covid policy and its fallout." The risk is that inflation driven primarily by such forces won't dissipate in due course. "Even when supply shocks fade, the disinflationary dynamics of the past decade are unlikely to return," ECB President Christine Lagarde has warned.

Her timetable signals quarter-point moves in July and September — a scenario that Bloomberg Economics reckons is likely to transpire, rather than any half-point increase. Whatever the ECB ends up deciding, officials received a message of sympathy last week from veteran UK economist Charles Goodhart. "It's a very, very difficult situation for the ECB — it's harder in many ways for the ECB than it is for the Fed," he told a conference in Madrid. "Dealing with a supply shock is a great deal more difficult than dealing with a demand shock."

And it could turn out that the ECB doesn't ultimately hike as much as the Fed, creating a transatlantic divide, according to economists at HSBC: "For the ECB, fears about rising peripheral bond spreads might limit the pace of tightening. Europe might also have a lower long run 'neutral' rate."

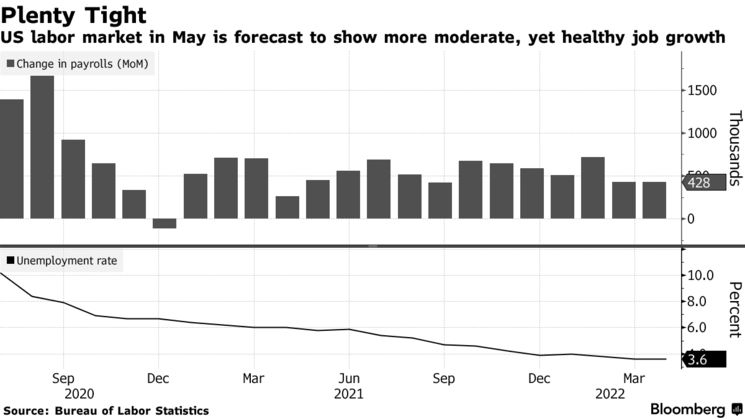

—Craig Stirling This week's US jobs report is projected to show the labor market, while still tight, may be starting to transition to more moderate payrolls growth from outsized monthly advances. Payrolls probably increased by about 325,000 in May after rising 428,000 in each of the previous two months, according to the median estimate in a Bloomberg survey of economists ahead of Friday's report. While still robust, the projected advance would be the smallest in just over a year. Fed policy makers will probably take the data in stride as they prepare to keep boosting rates and wait for a more-sustained cooling in job growth to help moderate wage gains and inflation. Elsewhere, a prospective half-point rate increase in Canada and slowing Brazilian growth may be among highlights. Read about the full week here.  | - Outbreak wanes | Chinese authorities are moving to stimulate the economy and ease some of its strictest virus controls as the number of new local Covid-19 cases fell to the lowest level in almost three months.

- US outlook | Firmer consumer spending and a decisive narrowing of the merchandise trade deficit show the US economy is emerging in short order from a first-quarter pothole.

- Kiwi confidence | New Zealand's central bank is confident it can guide the economy to a "soft landing" even as it raises interest rates aggressively to tame inflation.

- UK jubilee | The bank holiday to celebrate Queen Elizabeth II's 70 years on the throne may tip the UK economy into contraction but growth into subsequent months will save it from a recession.

- Reducing the gap | The US merchandise-trade deficit shrank in April by the most since 2009 as imports fell amid lockdowns in China while exports increased to a record. The shortfall narrowed by 15.9% to $105.9 billion last month, following a record level in March.

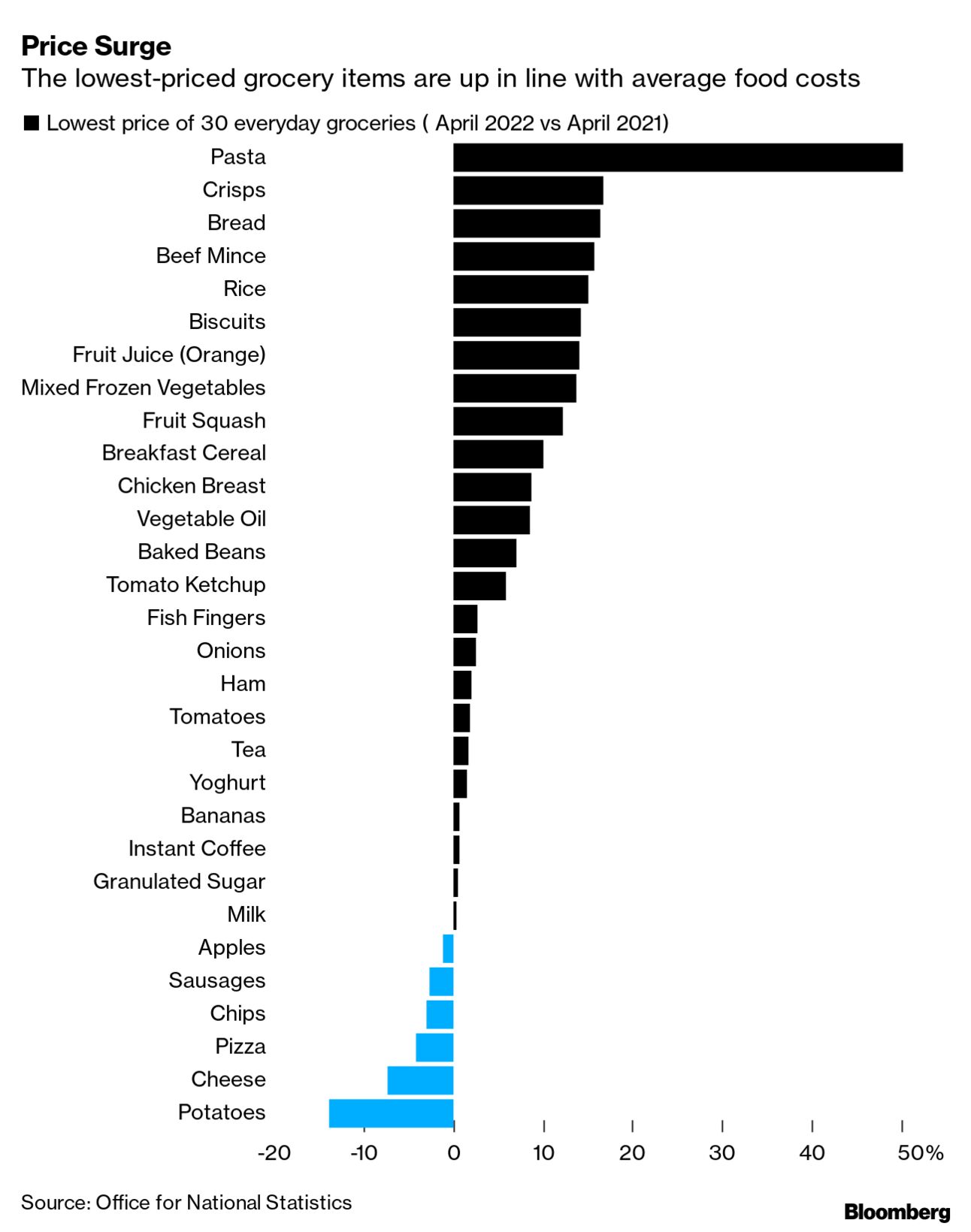

The price of the lowest-cost pasta soared 50% in the past year, and other cheap staples have also seen double-digit increases, according to UK data that highlights the growing difficulty of managing household budgets through the cost-of-living crisis. The Office for National Statistics, which called the figures "highly experimental," found that low-cost crisps, bread, minced beef and rice had all seen prices jump by more than 15% in the 12 months through April. In cash terms, the biggest increases for a single item were a 32 pence rise in the price of a 500-gram packet of beef mince, and an extra 28 pence for 600 grams of chicken breasts. See here for more. Read more reactions on Twitter |

No comments:

Post a Comment