|

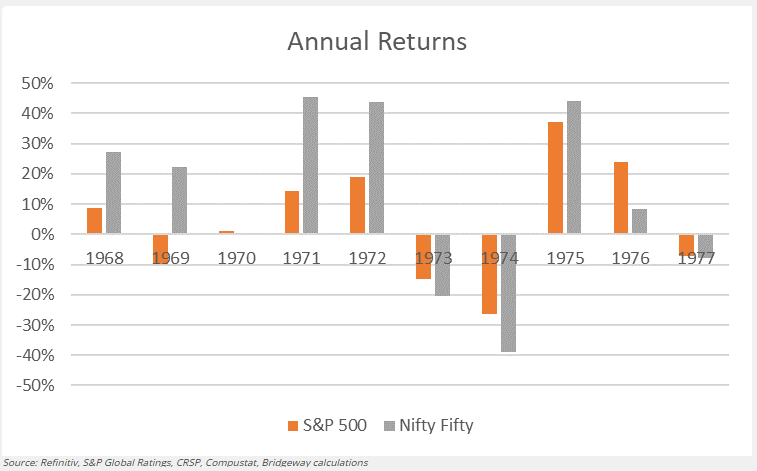

It has been more than 50 years since the high-flying Polaroid Corp. fell back to earth during the collapse of the famed Nifty Fifty bubble. At its peak, Polaroid controlled nearly two-thirds of the instant-camera market and traded at earnings multiples exceeding 90x. Other Nifties enjoyed similarly extreme multiples, beyond anything in today’s AI-driven rally. When the bubble burst, the Nifties brought the whole markets down with them, underperforming along the way. This chart is from Bridgeway Capital, produced as long ago as 2021 when the post-pandemic surge in tech stocks had set off another bubble alarm:

Naturally, this drives comparisons between the two eras. The Nasdaq 100 closed Wednesday at yet another record — but could its momentum ultimately unravel? The prevailing investor enthusiasm bears striking resemblance to the optimism around the Nifty Fifty half a century ago, even as market breadth appears considerably narrower now than it did then.

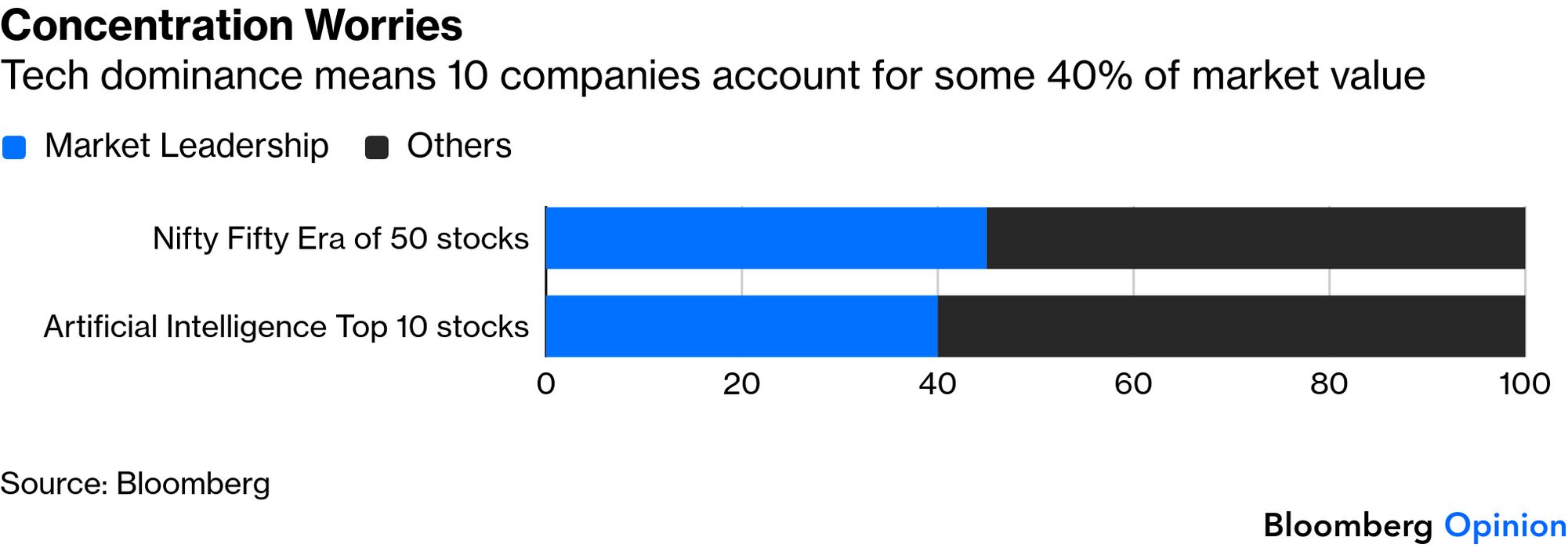

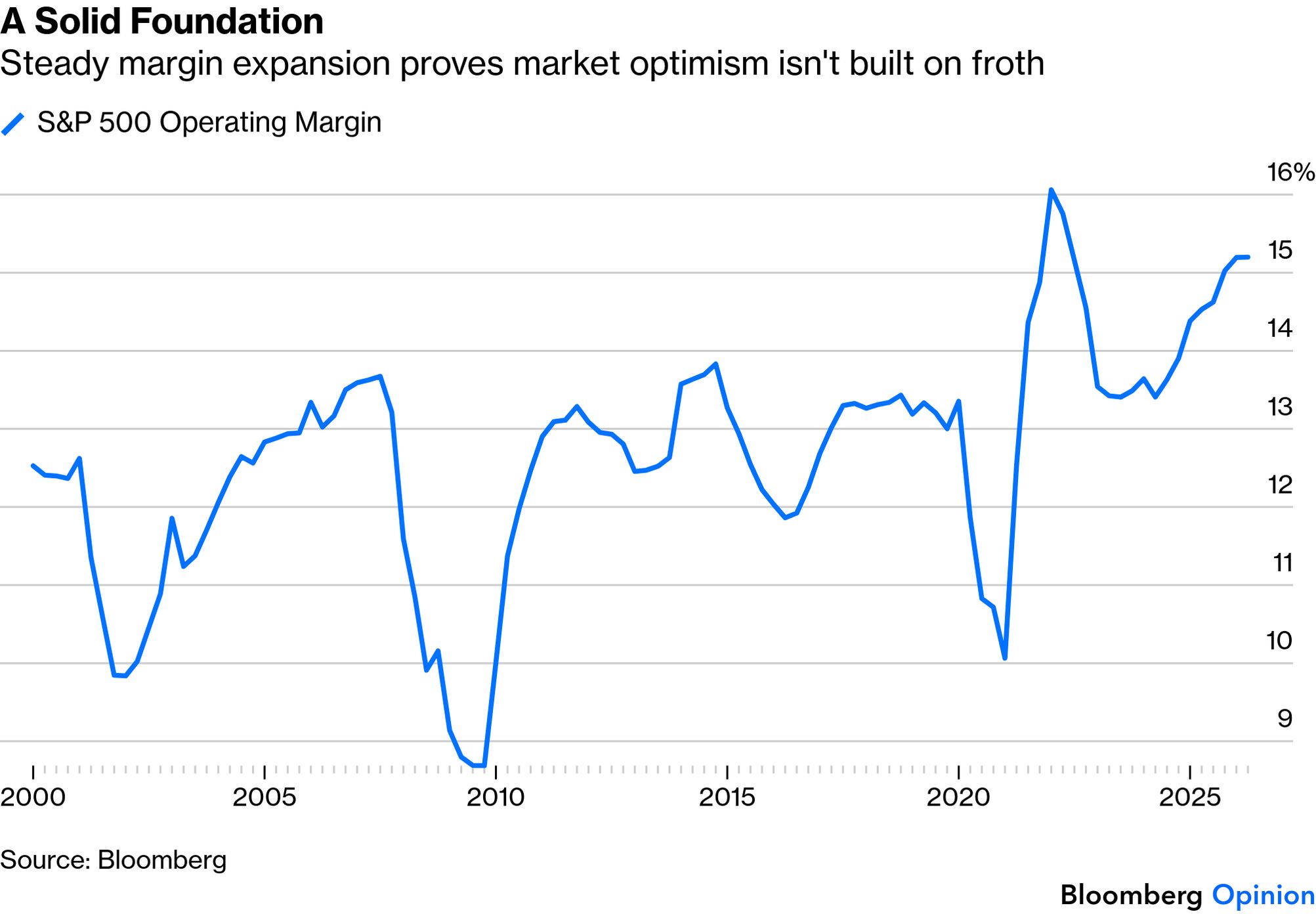

In recent months, robust earnings across the board have led to a slight diversification away from the mega caps. But concentration is much greater now than in 1972. Such levels, coupled with unrestrained spending on AI data-center buildouts, make it difficult to dismiss the possibility that the trade could unravel in a painful way. At the peak of what felt like an unassailable dominance in the early 1970s, the Nifty Fifty, a group of 50 stocks, accounted for roughly 45% of the S&P 500 value, though market leadership at the time was spread across a more diverse mix of industries. Meanwhile, as of May 13, 2026, just the top 10 — all tech groups apart from Berkshire Hathaway — account for roughly 40% of the index. There are fundamental justifications for this. As Points of Return has documented, earnings are on a record tear, particularly for semiconductors. Margins are remarkable. But previous bubbles were not entirely speculative either; Polaroid, Kodak, Xerox and the others exerted similar dominance from their wide economic moats.

Seth Cogswell of Running Oak Capital compares the two eras’ spending cycles, and questions the economics of hyperscale infrastructure spending:

Right now, it doesn’t make sense. Nvidia handing customers money to buy their products doesn’t make sense. That's not the way that business works, unless you’re in a position where that’s the only way to keep it going. The ecosystem right now is all being subsidized in a whole lot of ways.

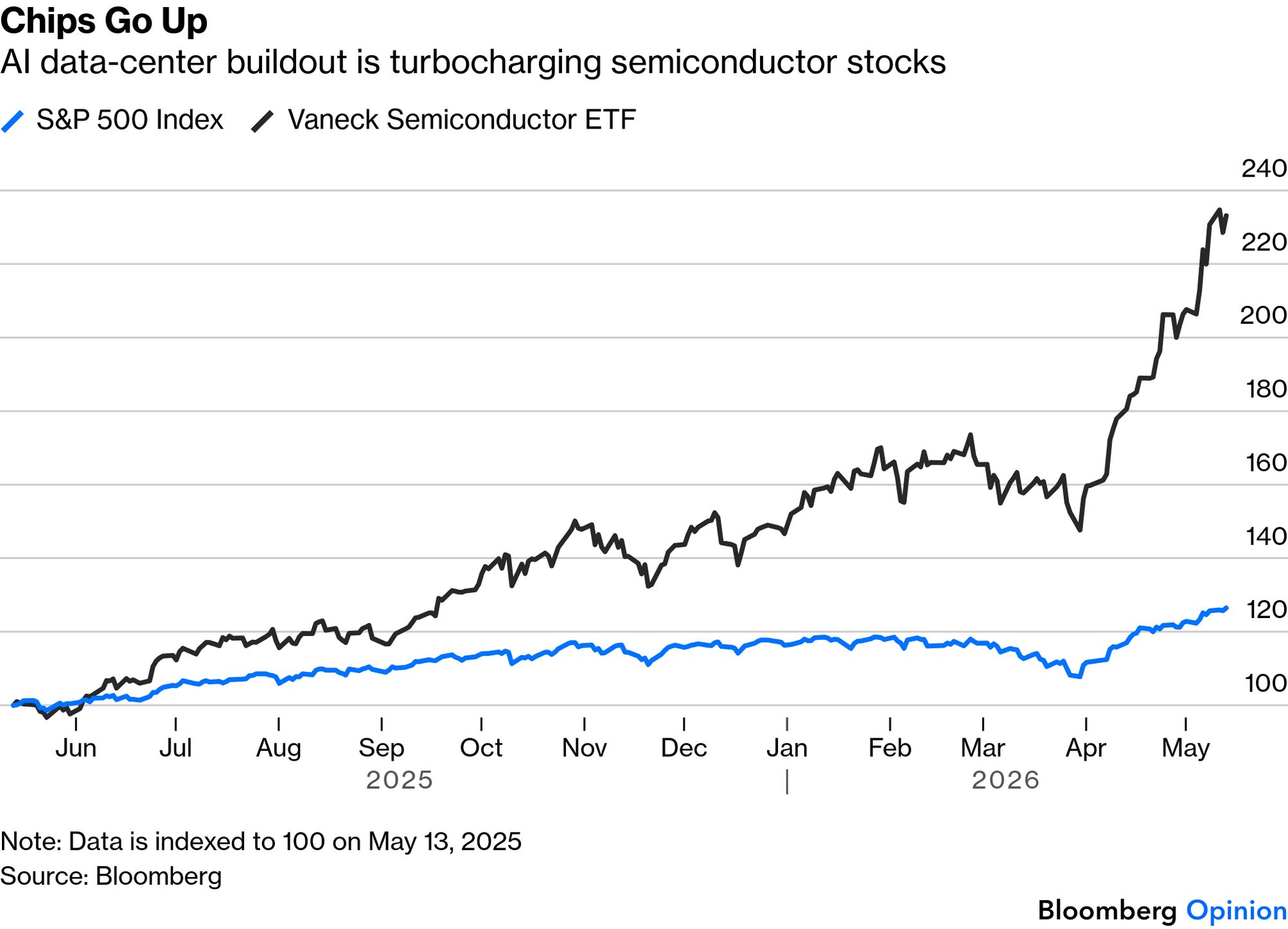

Jeremy Grantham, the founder of the GMO fund management group who famously warned about the dot-com bubble, argues that the profitability of today’s market leaders isn’t as impregnable as investors assume. In this interview, he notes that “earnings are not sacred.” He argues that mega-cap profits could soon feel pressure from the enormous costs of the data-center buildout, and then from the fact that the AI monsters now being built will ultimately compete against one another. Head-to-head competition, while good for consumers, is all but certain to damage profits. It’s also hard to ignore the obvious dangers lurking beneath what Bob Elliott of Unlimited Funds describes as a “macro mania” unfolding in plain sight. He points to the VanEck Semiconductors Exchange-Traded Fund, which has risen roughly 60% since its late-March trough.

Even though proponents cite fundamentals to justify current pricing, he says it’s hard to make a common-sense case that the outlook has swung so swiftly for a sector of such size:

It’s one thing to bid a single stock. Even spot gold is a pretty tiny market all things considered, where even a 10 or 20 billion incremental bid from the $100 trillion equity markets can create a squeeze. It’s a whole other dynamic to expect global equity earnings to surge 10% on the back of the sector at the center of speculation.

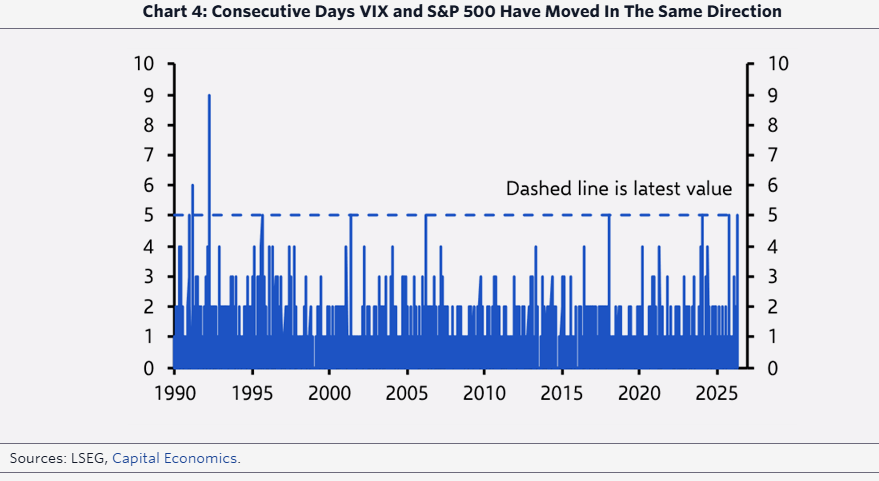

Over-pricing increases the risk of a correction, but says nothing about when it might happen, or how big the pullback could be. Capital Economics’ James Reilly points to the unusual lockstep movement between the VIX and S&P 500 over the past week. Usually they have an inverse relationship, with investor anxiety rising as stock prices fall. The current pattern has happened only a handful of times in recent decades, notably just before the “Volmageddon” selloff in early 2018 and around the start of the software stock selloff late last year.

The bear case, Reilly argues, is that this is an unstable rally, just as on those two occasions. Investors are chasing the market higher, having been caught out by the size of the rally, but feel the need to buy more downside protection amid heightened tail risks. He adds:

The VIX is driven by demand for calls, too, and retail buying has reportedly risen to Covid-era extremes lately. The bigger picture is that these developments are odd and, alongside extreme dispersion in performance, means this equity rally comes with a bit of a health warning.

When such dynamics emerge, Elliott argues they’re far more likely to end badly than culminate in remaking the global economy. Questioning today’s optimism can sound almost Luddite, but market history suggests that caution is warranted. — Richard Abbey

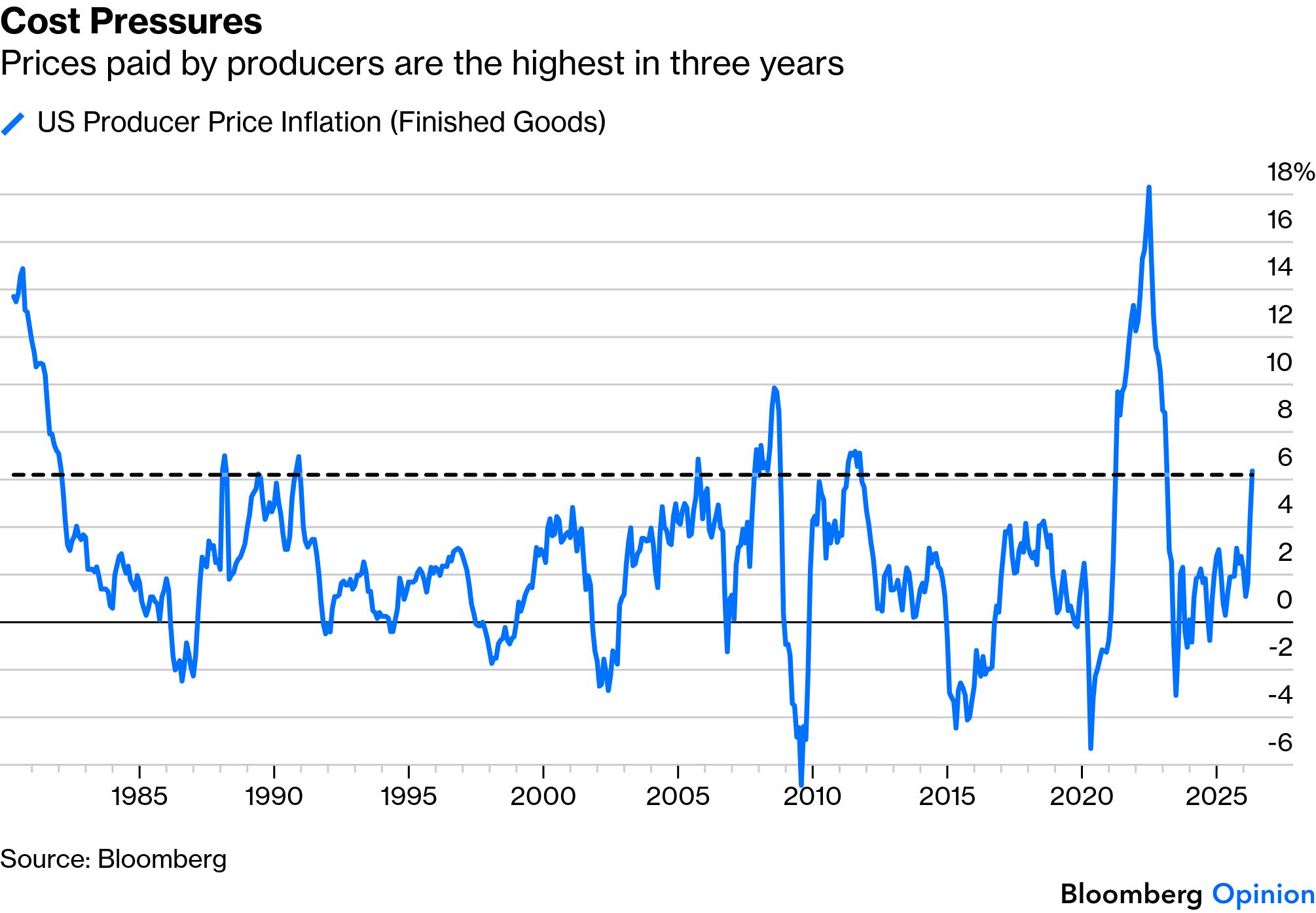

US producer prices brought fresh evidence that the oil supply shock is beginning to ripple through into other prices. The producer price index is always more prone to big swings than consumer prices, but an outcome above 6% topped estimates and brings it right to the heights of its historical range since the 1980s — excluding the post-pandemic surge.

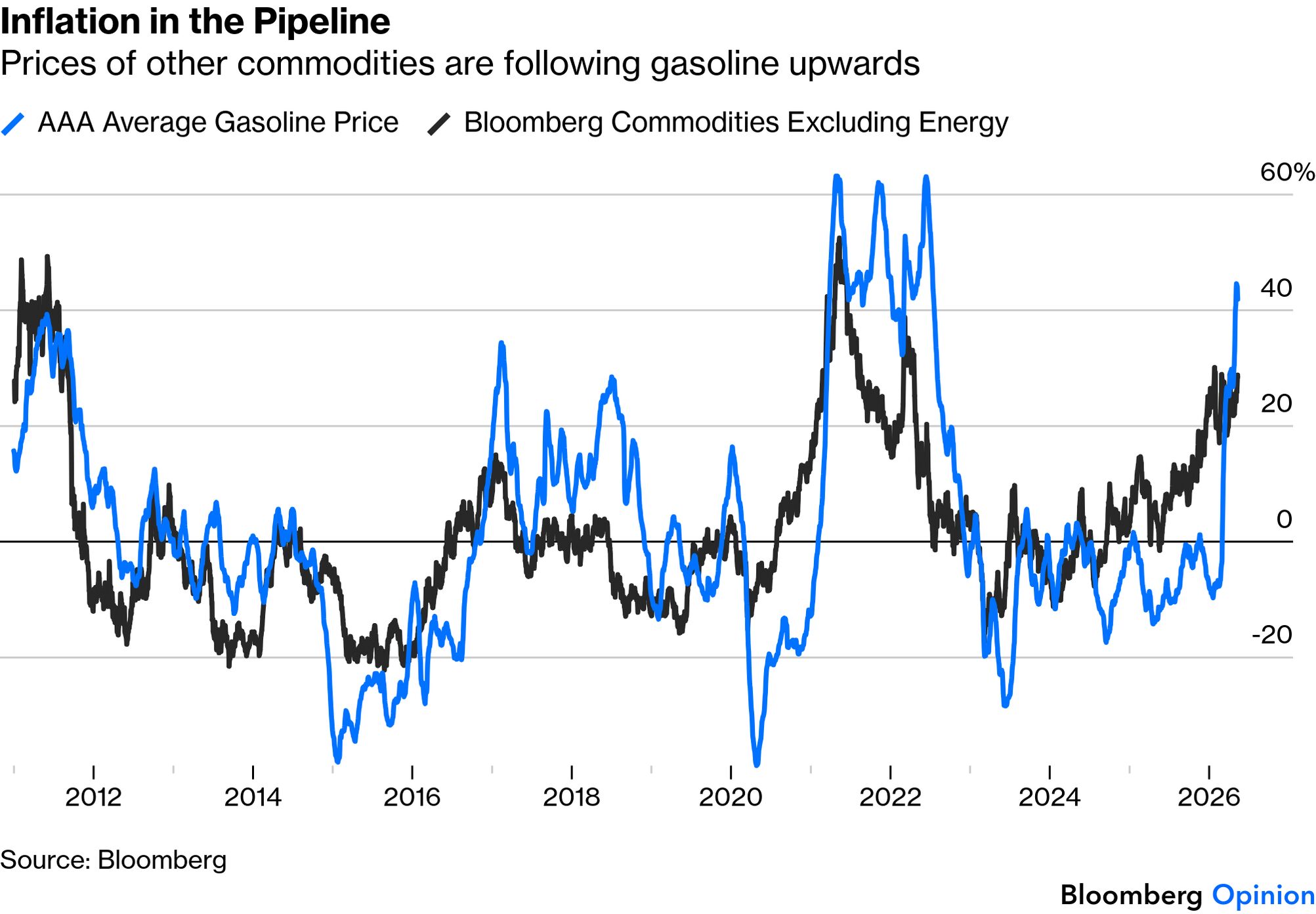

There are other signs of building pressures. While gasoline prices naturally hog attention, Bloomberg’s index for all non-energy commodities is also now at an all-time high — even though precious metals, an important component, are down about 15% since their peak in January.

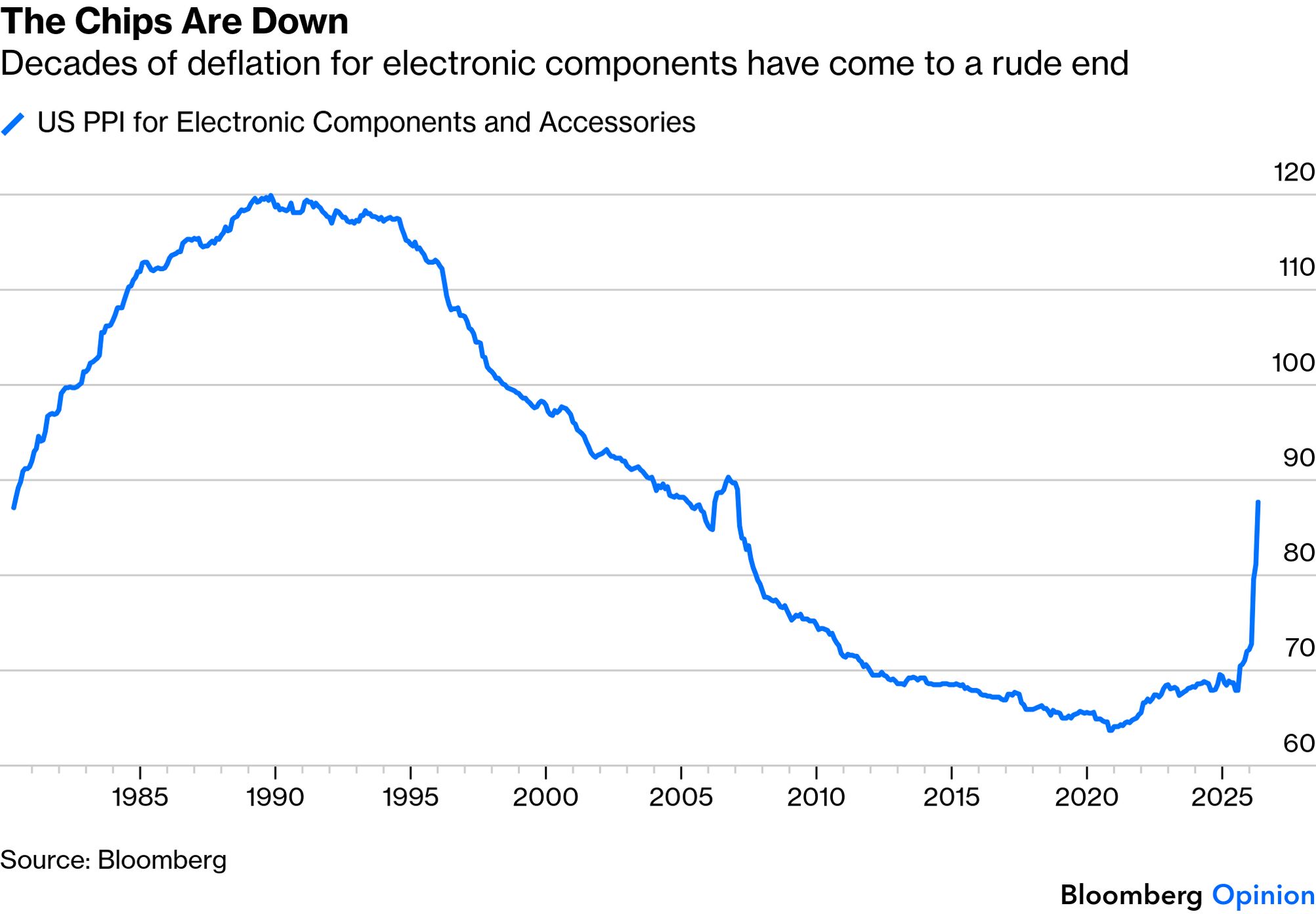

But the price rises aren’t just a function of the oil shock. Grace Zwemmer, US economist at Oxford Economics, argues that these numbers should push the headline Personal Consumption Expenditure deflator, the Fed’s preferred inflation indicator, to 3.8% — its hottest reading since May 2023 and far too high to permit rate cuts. Beyond oil, she pointed out that prices of electronics components and accessories had risen by 8% month-on-month, as AI demand has created a shortage of memory chips. Electronic components inflated by 27% year-on-year, ending decades of persistent reducing costs. This could throw many companies’ assumptions badly awry.

Until now, as we’ve seen, the sole market reaction to this development has been to send the share prices of chip manufacturers into the stratosphere. It might be wise to guard against some of the potential adverse consequences as well.

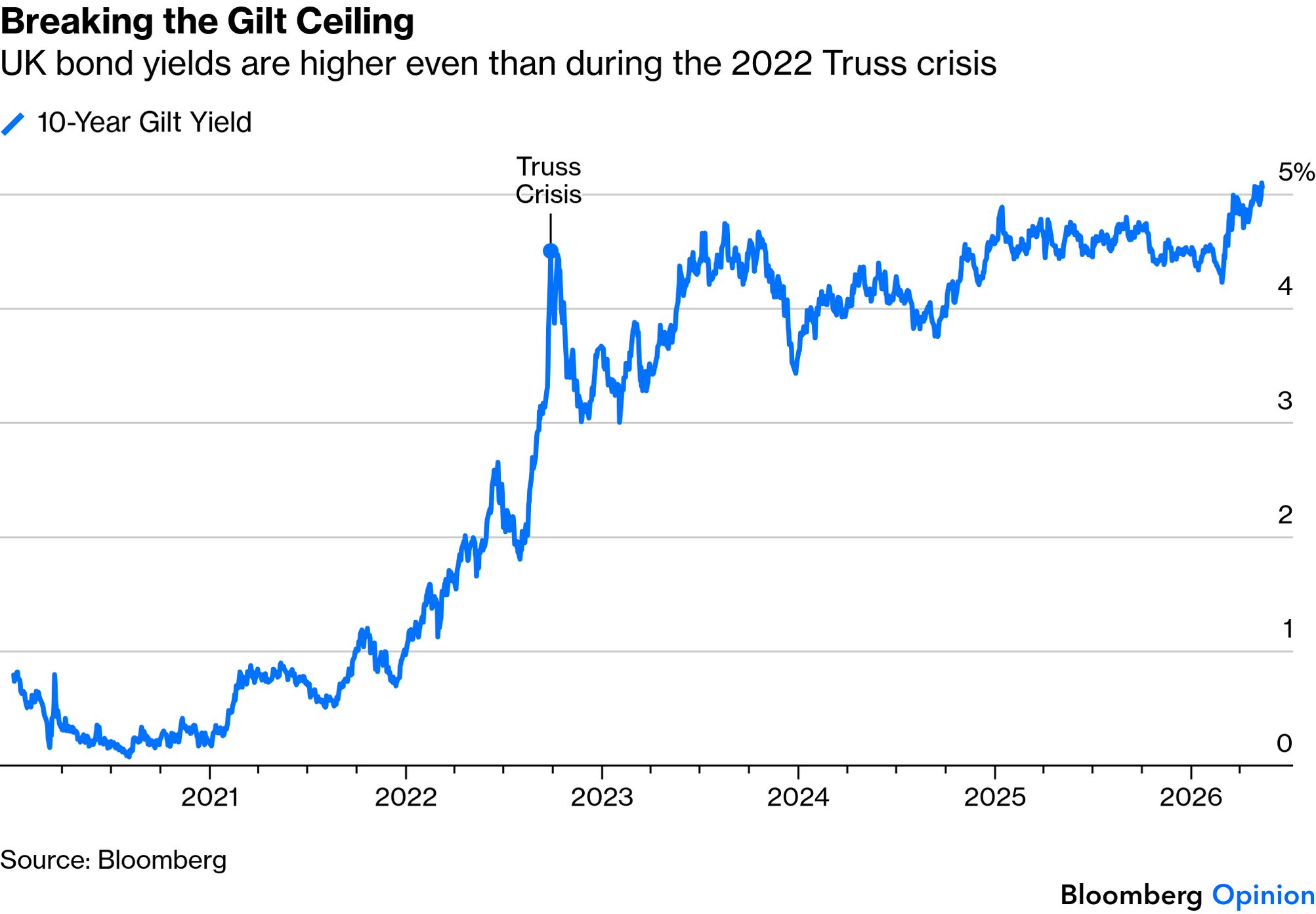

Keir Starmer, the UK’s prime minister, is in awful political trouble. This isn’t new for the country. Since 2010, which saw the end of 13 years of Tony Blair/Gordon Brown center-leftism, which had followed directly from 18 years of free-market right-wing policies under Margaret Thatcher/John Major, political intrigue and uncertainty has become the norm. Starmer is the sixth prime minister since then, in a period that has been characterized by either unstable coalitions or fierce internal battles whenever one party has a strong majority in Parliament. In a long-term perspective, it’s obvious that the UK’s political instability has been economically harmful. It’s also wrought havoc with financial markets. As bond market investors are already alarmed about fiscal stability, and any replacement for Starmer would almost certainly worsen the problem (in their eyes) by trying to loosen fiscal spending, this is a dangerous situation. Gilt yields are now slightly higher than they were when a bond market revolt forced the ejection of Liz Truss in 2022:

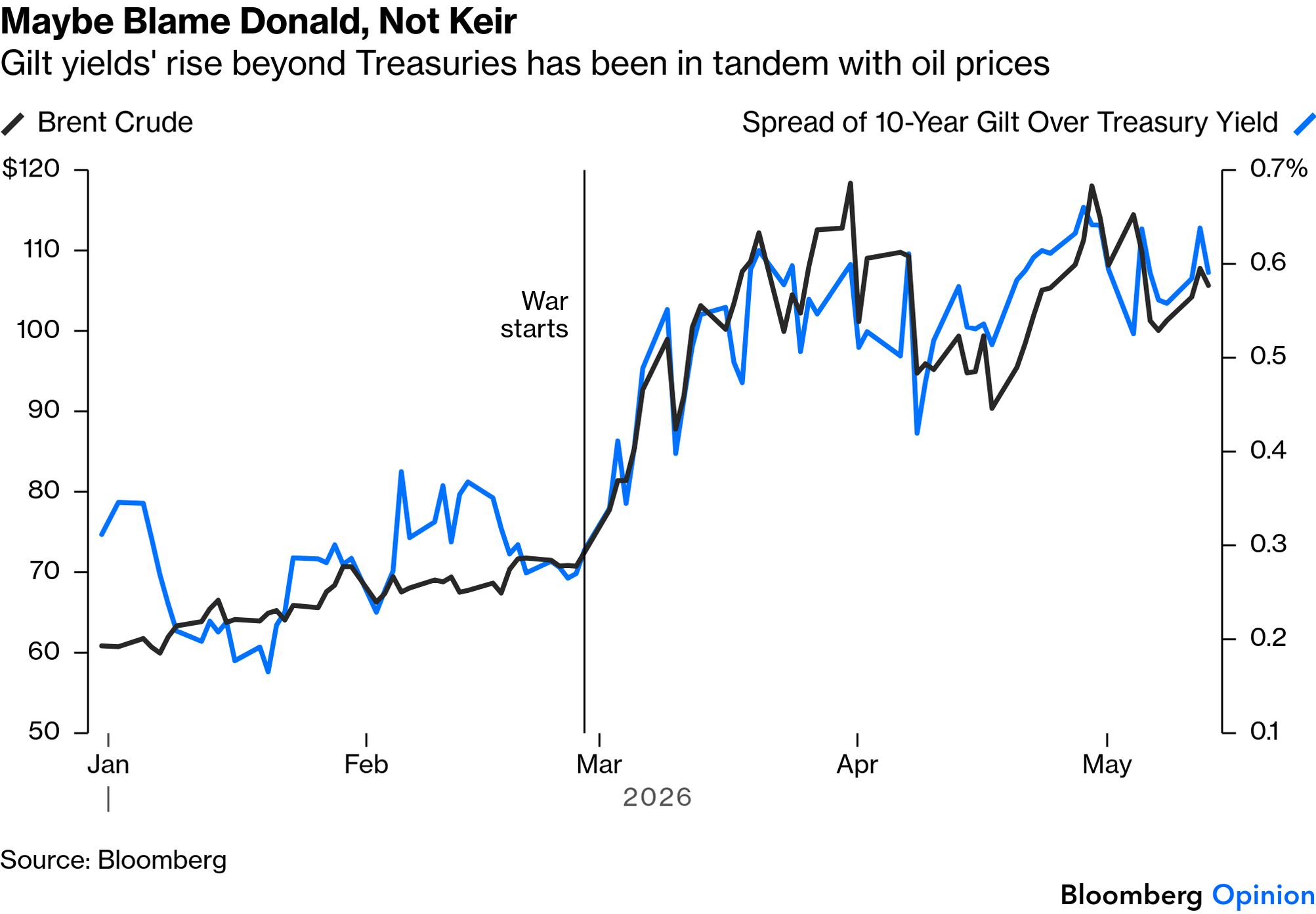

But while Starmer, like Truss before him, appears to be in terminal difficulties, it’s not clear that his political problems have had any great impact on bonds just yet. The UK is more economically exposed than the US to the Iran war, and the extra spread on gilt yields compared to Treasuries has moved almost directly in line with the oil price since the outbreak of hostilities.

Why, then, is the Starmer effect muted? In part because he has evidently been in trouble for a while, and markets have long been priced on the assumption that he probably won’t last beyond the end of this year. Polymarket’s contract on Starmer to leave his job by Dec. 31 was initiated six months ago, and it has almost put the odds at more than 50%. The mess around choosing a successor doesn’t add significantly to the financial damage for the UK, as the market in general doesn’t think any of the alternative candidates would be an improvement.

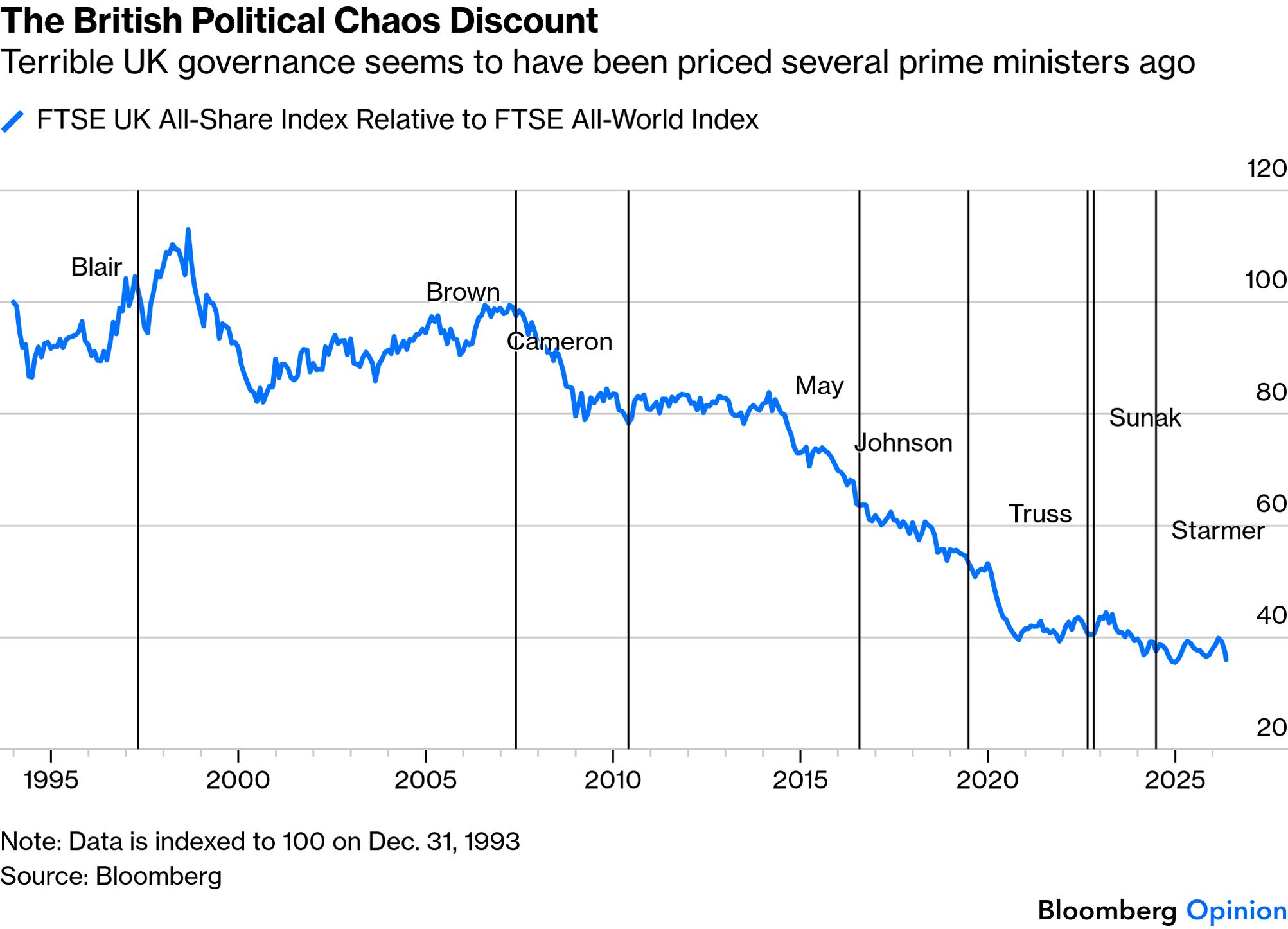

In stocks, Britain’s underperformance has endured for years. The slide started long before the 2016 Brexit referendum, although that certainly made things worse. After seven successive prime ministers who oversaw a stock market that underperformed the rest of the world, the market seems satisfied that it’s priced in British political dysfunction. There were no great expectations of improvement under Starmer, and there is no disappointment now that his premiership is panning out as badly as investors expected.

Lousy UK political governance, it would appear, is already in the price. There’s no prospect of that changing. That’s miserable for the country’s prospects. It also explains why the century-old Labour-Conservative duopoly seems finally to have been broken, as Britons have had enough. But in the shorter term, it probably means that the market downside from Starmer’s agonies isn’t as severe as it might appear. |

No comments:

Post a Comment