| Read in browser | |||||||||||||||||

Quite rightly, global markets have switched from fretting over an inflationary shock from the war in Iran to worrying about growth. The pivot can support investors if a recession is avoided. It also increases the risk that the global economy tips the wrong way.

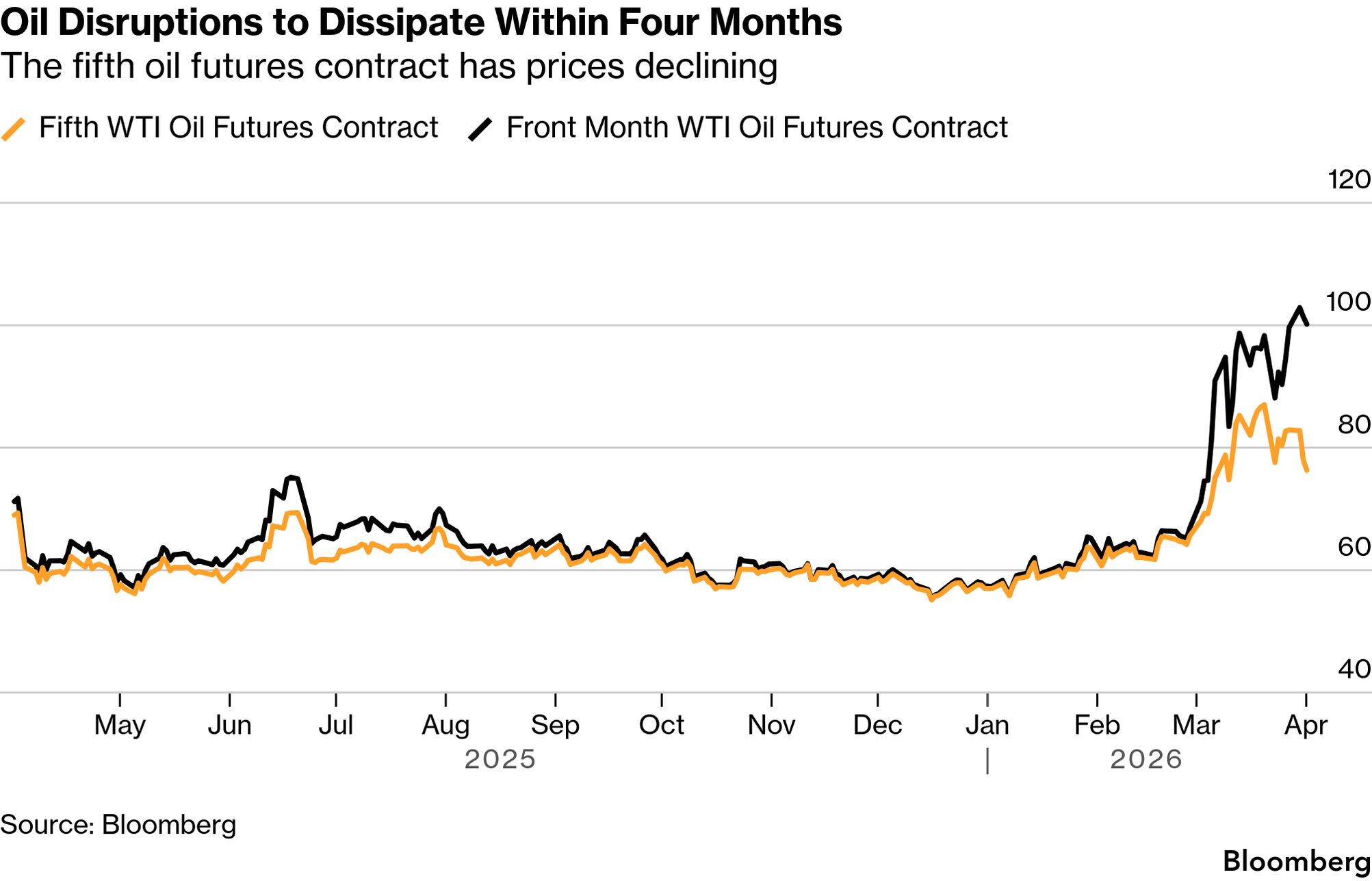

Bond investors can breathe easier nowThe risk for higher yields has been eclipsed by investors recalibrating to focus on growth. It's a justified shift because sky-high oil prices typically end in recession causing central banks to cut interest rates, not raise them.  Once Powell confirmed that view, rate hike fears evaporated. With rate cuts back into view, expect the market to price in even more easing, driving short-dated bond yields lower. We're back in a traditional situation where the bond side of your portfolio benefits from any economic weakness that hurts growth and lowers corporate earnings and equity prices. In a Goldilocks scenario, growth slows just enough to cause the Fed to ease policy, benefitting bonds while not enough to hurt stocks. Who will unblock the shipping straits?The core message from last week's newsletter was that the US economy is doing well enough to overcome a temporary increase in bond yields. The latest forecast from the Atlanta Fed for growth in the quarter ended this week was 2%. Moreover, retail sales remain firm and the latest labor metrics indicate the economy is still adding jobs. A US recession isn't a near-term worry. Things of course could slow from here as high oil prices and inflation crimp growth. But a slowdown of 1% to 2% wouldn't be enough to trigger a pullback on capital investment, layoffs and a wave of bond defaults. That's my baseline for now. There are worse outcomes, though, and their probability is rising. The contours of an end to the war where President Donald Trump can claim to have achieved his objectives are coming into view. He's now saying he's ousted the previous Iranian regime, eliminated their nuclear threat and crushed their navy. He gave a timeline of two or three weeks for hostilities to last, helping the S&P 500 to its best performance in 10 months. Oil futures prices, while still high, also saw a marked decline in the September contracts.  There is one wrinkle to this scenario though. Trump is reportedly telling aides he may not be able to restore the flow of shipping traffic through the Strait of Hormuz. With the Houthis involved in this conflict, there might even be a second chokepoint at Bab-al Mandeb, the strait through which ships must travel to leave ports on the other side of the Middle East. If Iranians and the Houthis remain the gatekeepers of these narrow passageways, the economic impact will be greatest in Asia and to a lesser degree in Europe. It's an outcome that would keep oil prices elevated, raising the risk of a global recession. It's all about oilNobel Laureate Economist Paul Krugman modeled the situation in a recent newsletter and found the lowest reasonable case for world benchmark Brent crude oil at $99 a barrel, just under where it sits today. His middling case showed Brent at $152, with an extreme disruption case as high as $372. After seeing Krugman's model and listening to Bloomberg columnist Javier Blas talk to colleagues Tracy Alloway and Joe Weisenthal, I realized that Trump's mooted solution doesn't remove economic pain. Ending the military conflict alone won't bring oil price relief. The Iranian regime knows by now that's where their biggest leverage lies. An oil price overhang while the supply routes remain blocked or the threat of destructive strikes on infrastructure is still in place is no longer a tail risk. It's a reality that could last longer than the economy can sustain. Buffett's warningDespite relative insulation from the price shocks emanating from the Middle East, this is where the US becomes more economically vulnerable. Warren Buffett recently cautioned that he sees emerging signs of fragility in the US banking system because of its interconnectedness to non-bank financial institutions in private markets. Banks' hidden ties to private credit would come into full view in a weakening economy. Spending on artificial intelligence, that's been the backbone of recent earnings, could also slow down. Or companies could cite AI to justify more layoffs. All of this makes government bonds look very attractive, especially at the shorter maturity spectrum where inflation concerns are less problematic and where the benefit from rate cuts is greatest. Longer-duration bonds look less attractive because of stagflation risks. The positive near-term outlook for earnings growth still supports equities. And if Iran stands down, we will have a massive relief rally to boot. Still, the overhang of a potentially enduring oil shock tempers the optimism, as the probability of that outcome has increased. Things on my radar

More from BloombergEnjoying The Everything Risk? Check out these newsletters:

You have exclusive access to other subscriber-only newsletters. Explore all newsletters here to get most out of your Bloomberg subscription.  We're improving your newsletter experience and we'd love your feedback. If something looks off, help us fine-tune your experience by reporting it here. Follow us You received this message because you are subscribed to Bloomberg's The Everything Risk newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.

|

Wednesday, April 1, 2026

Markets are right to worry about growth

Subscribe to:

Post Comments (Atom)

‘They don’t get paid unless they win’

Plus: Scammers supercharge fraud with AI | ...

-

Bloomberg Evening Briefing Americas View in browser Who's paying for Donald Trum...

-

PLUS: Dogecoin scores first official ETP ...

No comments:

Post a Comment