We Need to Talk to Kevin... |

Kevin Warsh is about to face the Senate in confirmation hearings that will determine whether he is appointed to chair the Federal Reserve and becomes the most powerful figure in the global economy. It’s not being treated as that big of a deal. That’s because:

- Nothing Warsh says will affect the single greatest obstacle to his confirmation, which is Senator Thom Tillis’s stance that he won’t allow the nomination to proceed unless the case against incumbent Jerome Powell over spending on the Fed’s renovations is abandoned. The assumption is that this will be resolved eventually and Warsh will get the job, but nothing that happens Tuesday will likely affect this.

- Nothing any nominee says in confirmation hearings tends to matter much in the long run. Warsh, like his predecessors, has a long paper trail of decisions and opinions, including a stint as a Fed governor during the Global Financial Crisis. He has been a vocal critic at times. But Alan Greenspan was an acolyte of Ayn Rand, who opposed the existence of central banks, and that didn’t stop him from taking many activist policies in office.

Beyond that, a still-possible prolonged oil spike would rule out any chance of interest rate cuts. It also, probably, gives Warsh a get-out clause to avoid committing himself when he faces inevitable questions about President Donald Trump’s pressure for rate cuts. On the Fed’s role, under attack from the administration over the last 12 months, Warsh can only say that he will safeguard independence while being duly polite to the president who nominated him. This is a needle he threaded quite well in his preliminary remarks, which were leaked on Monday.

For Tillis, it’s all about Powell. Photographer: Alex Kent/Bloomberg

After the crisis, Warsh will say, he witnessed “an institution that was tempted to play a larger role in the economy and society... to extend its reach and stretch its hard-earned credibility, often with the best intentions, to the very edge of, if not beyond, the Fed’s statutory responsibilities.” He then lays out a view that monetary policy should be independent of political interference, while the rest of the Fed’s remit is fair game for politicians:

Fed independence is at its peak in the operational conduct of monetary policy. That degree of independence does not extend to the full range of its congressionally mandated functions. Fed officials are not entitled to the same special deference in their stewardship of public monies... or in bank regulatory and supervisory policy... or in areas affecting international finance, among other matters. And the Fed must stay in its lane.

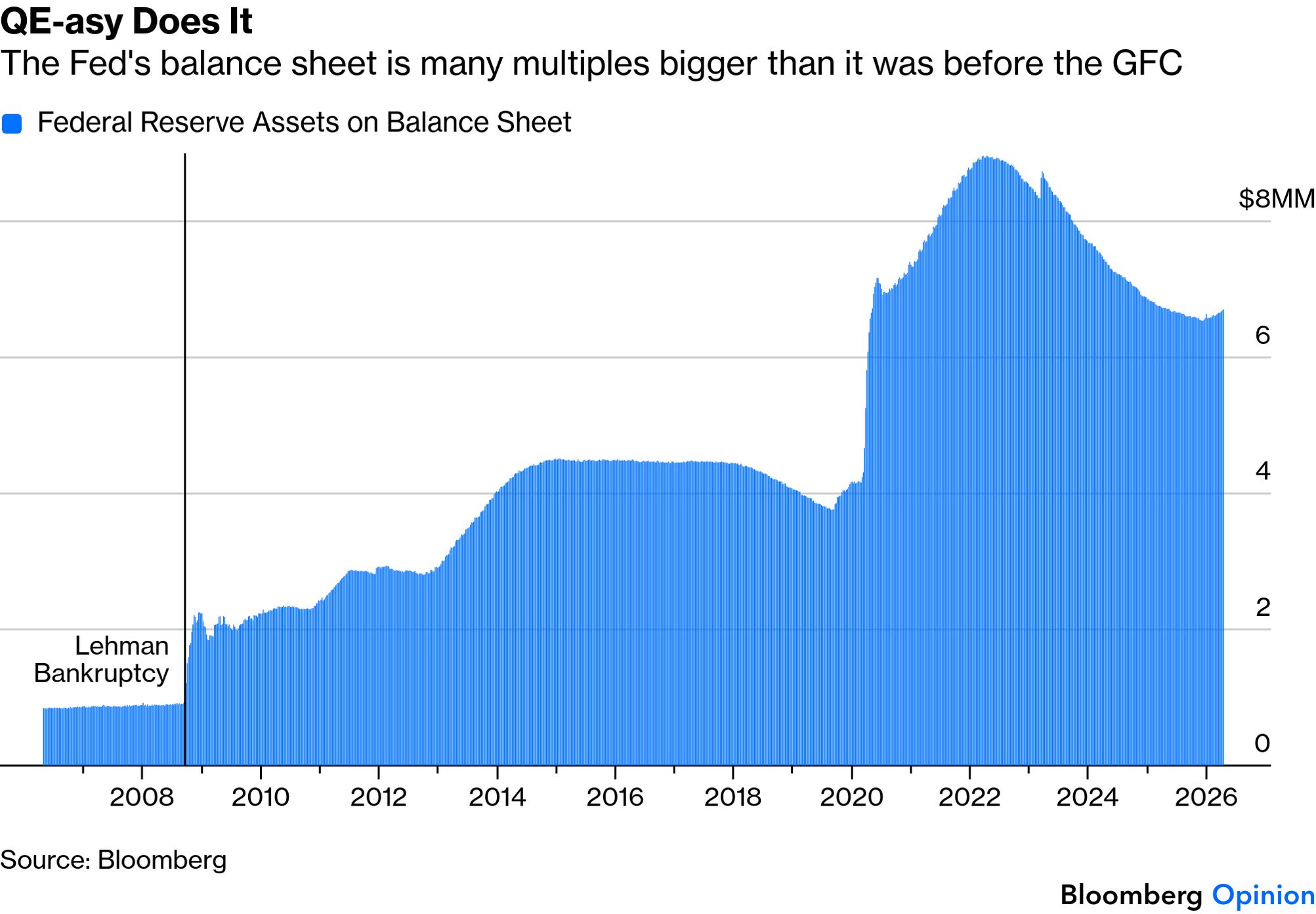

Without offering examples, he says Fed independence is at greatest risk “when it strays into fiscal and social policies” and the bank should “not act as some general-purpose agency of the US government.” That should be independent enough to keep the markets happy, while bolshy enough to keep Trump onside. Warsh’s most interesting views, which potentially bring him into conflict with politicians and the markets, concern the Fed’s balance sheet. He is loudly on record that it should be smaller — meaning that the Fed should sell down some of the huge portfolio of bonds it took on to deal with the GFC and then the pandemic. At the margin, that would mean less liquidity in the market, and higher bond yields. And the balance sheet has begun to enlarge a little once more. Senators are bound to ask him about this, and his answers could have a market effect:

Powell’s first black eye from the markets came in late 2018, when he said he would shrink the balance sheet “on auto-pilot.” An immediate selloff forced him into what became known as the Powell Pivot. Anything that risks pushing up bond yields in the current environment risks a similar outcome. There’s no mention of the balance sheet or QE in Warsh’s five-page opening statement. But that’s not surprising. Here are some words never mentioned during Ben Bernanke’s confirmation hearing in 2005:

- QE (or Quantitative Easing)

- Balance Sheet

- Subprime

- CDOs

- Lehman

Bernanke’s chairmanship would be dominated by just these issues as he battled the crisis, but nothing in that hearing gave any guide as to how he would deal with the challenges of 2008. Warsh is a smart enough operator to avoid saying anything important on the key financial issues of the moment — and the chances are that nobody will ask him about the key issues that he will in fact have to face over the next four years. It should still make for good entertainment.

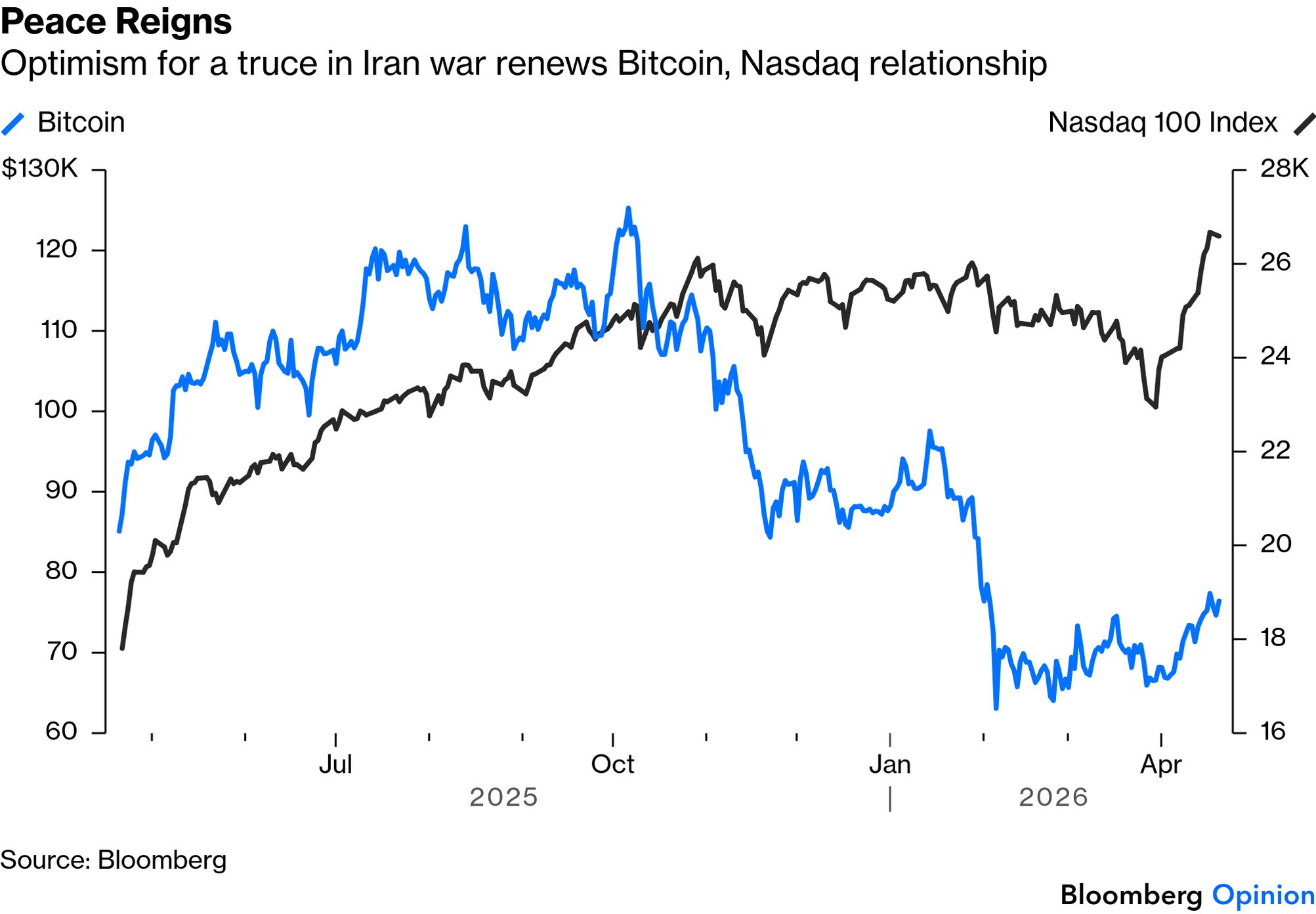

Bitcoin investors’ troubles aren’t over, but they’re probably feeling a little better. A confluence of favorable fundamentals is supporting the cryptocurrency’s best run in almost a year, up nearly 10% this month. It partially owes its decent rally to the Middle East peace talks: quite the irony for the so-called haven asset. Bitcoin is still down for the year, but it has trimmed its losses to about 14%:

Whether the rally will hold rests on the fundamentals, and there’s a sense in a corner of the market that it will be short-lived. K33’s Vetle Lunde notes:

Traders are actively building short positions and betting against a breakout, creating conditions where a short squeeze becomes more likely if upward momentum persists.

Since its spectacular collapse from October’s peak, short rallies have often been followed by pullbacks, suggesting investors are selling at every opportunity to pare losses. Thus, traders betting on a similar snapback are understandable, but the fundamentals will have the final say. Regarding the tailwinds, the ceasefire brokered a fortnight ago proved instrumental, suggesting that renewed talks for a more meaningful pause in hostilities are likely to have a similar effect. Of course, investors may already have priced in an extension, though the weight of concessions either side must make in any final deal could alter their resolve. Bitcoin’s rally has coincided with a great run for the tech-heavy Nasdaq, perhaps re-establishing a relationship that appeared broken. Continuing rallies for both now depend on the broader AI story. Meanwhile, Michael Saylor’s digital asset treasury company, Strategy, bought more than $2.5 billion in Bitcoin last week, its biggest buy since 2024, and prompting a modest rally in the share price. Doubling down like this shows confidence, but Strategy’s investors need Bitcoin to rally a while longer if they are to recoup their losses:

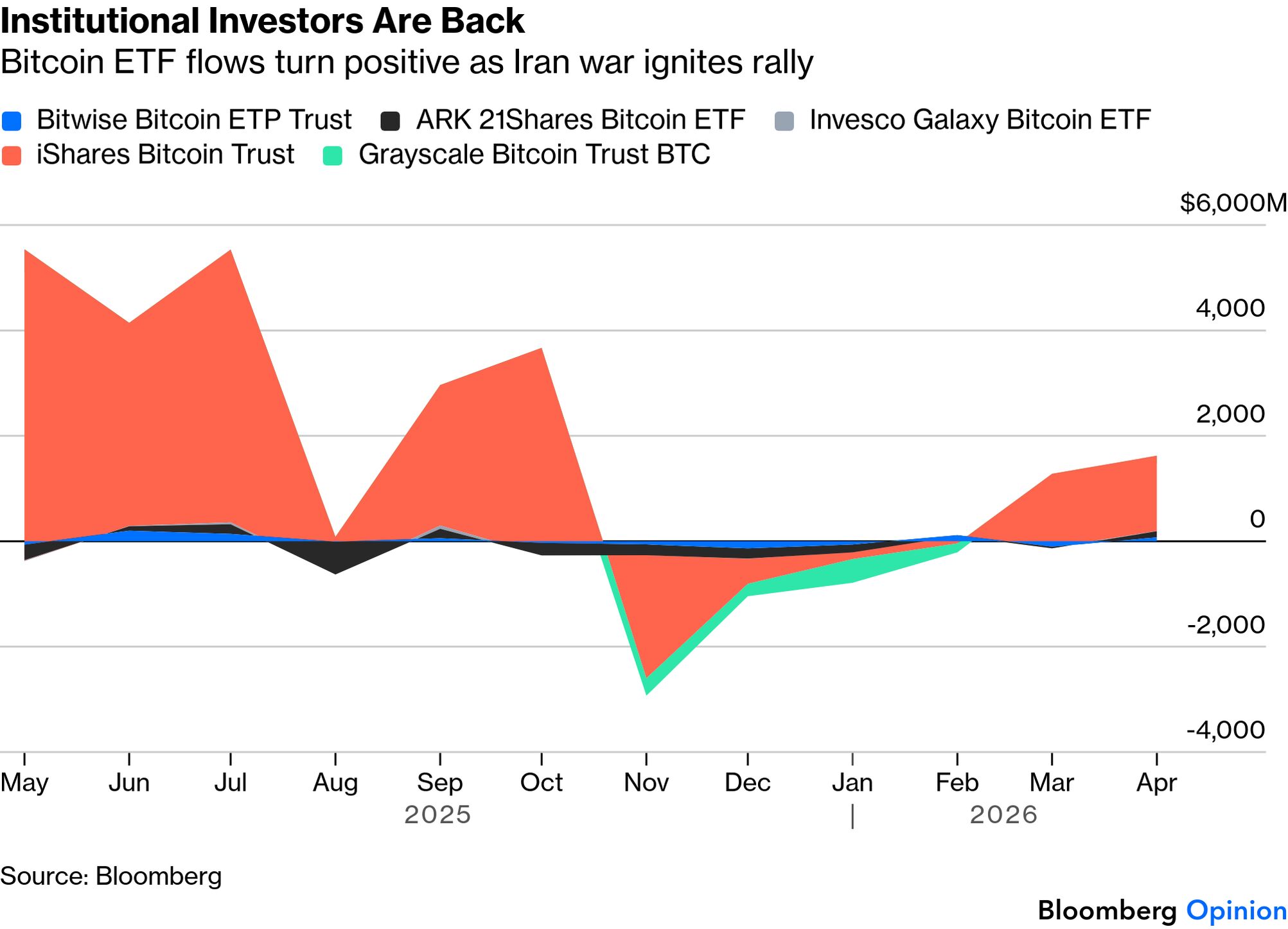

Bitcoin has also just survived a test. The loss of almost $300 million in a hack of the Aave decentralized finance (DeFi) platform over the weekend prompted more than $10 billion in outflows, but this hasn’t spilled into the broader digital assets universe. Bitcoin gained 2.1% on Monday, even as the stock market took a pause. Further, institutional investors last week poured in almost $1 billion via exchange-traded funds, and the resurgence rests on persuading them to keep investing. Last week, Goldman Sachs filed for a Bitcoin ETF, joining Morgan Stanley and BlackRock:

Goldman’s is aiming to provide exposure to Bitcoin while also generating an income by selling options tied to it. That would sacrifice some upside during market rallies, but could deal with one of the cryptocurrency’s biggest disadvantages by offering a yield. It’s getting ever further from the decentralized and libertarian vision of Satoshi Nakomoto (whoever he is), but investors sitting on losses will be only too happy to get some help from the Wall Street establishment. —Richard Abbey

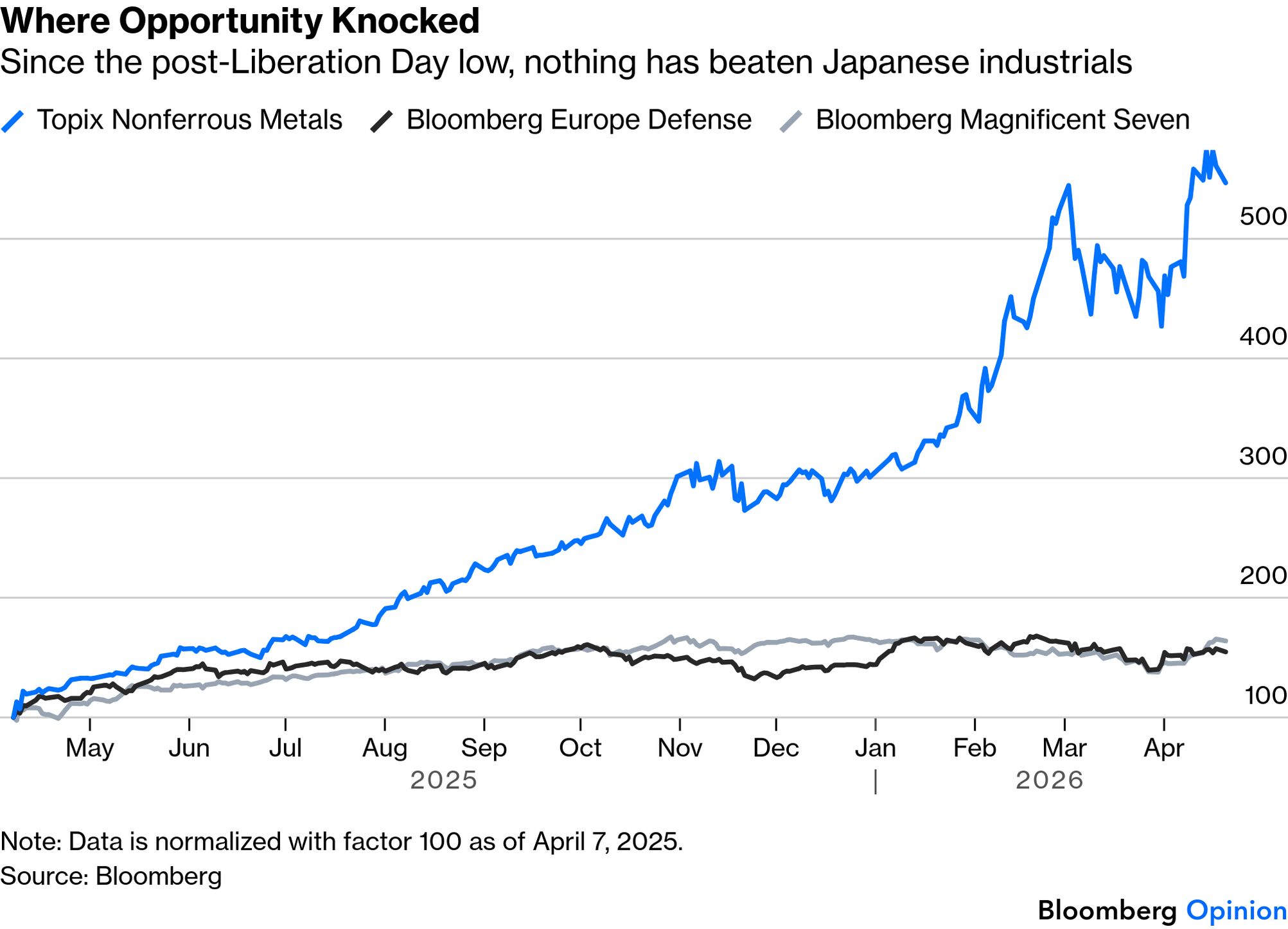

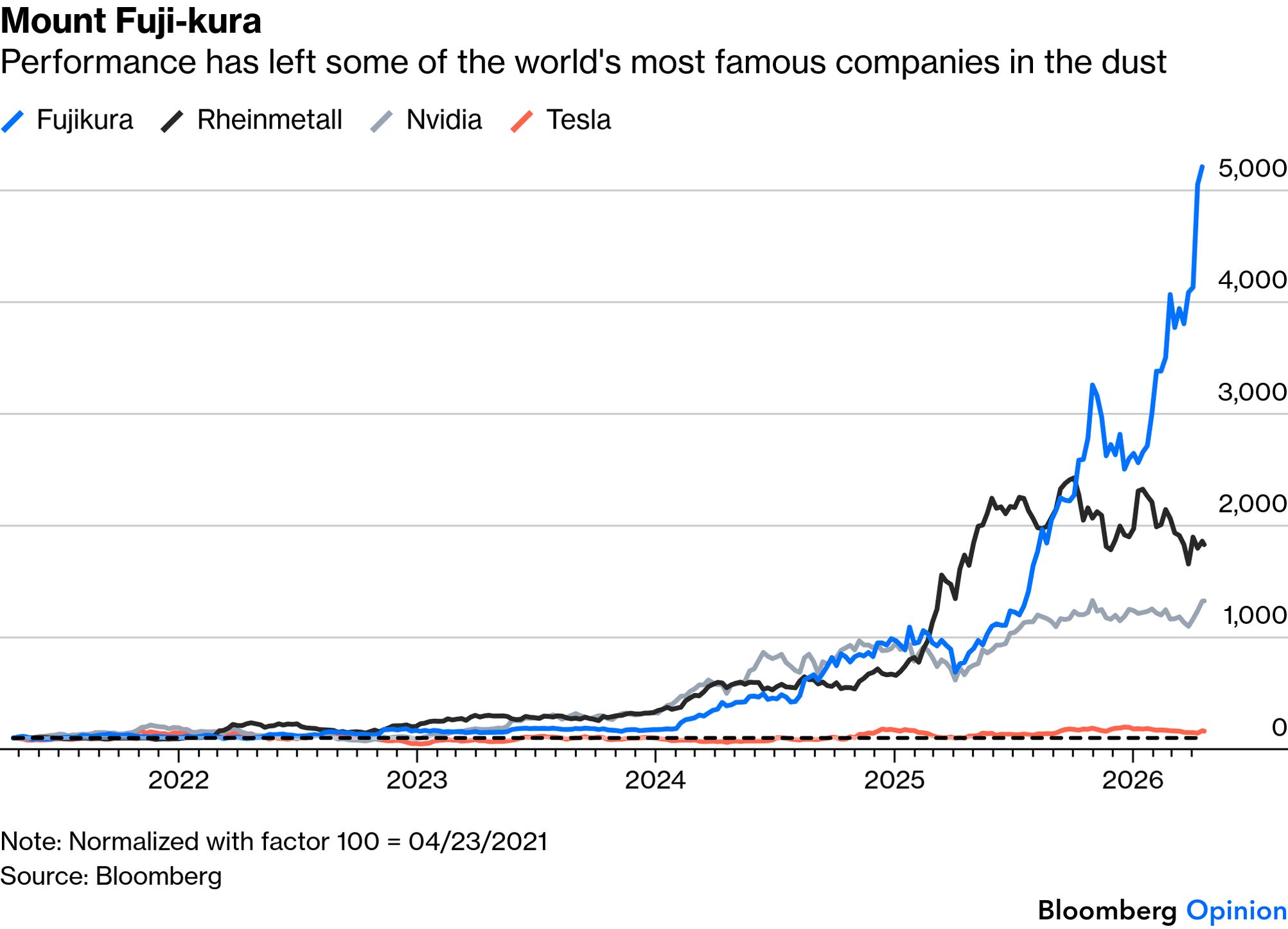

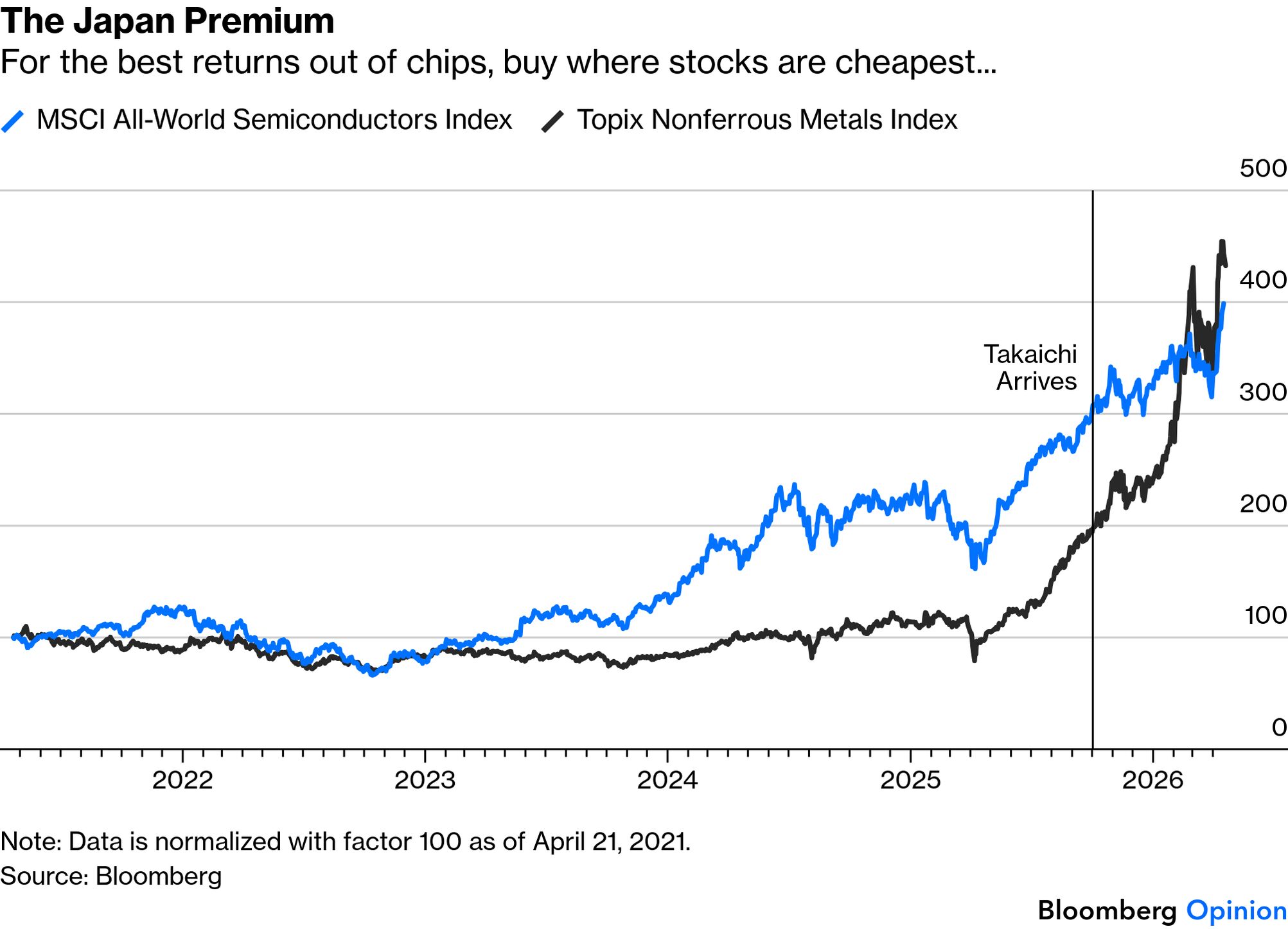

Time for some hindsight. We all now know that the first great TACO, when Trump rowed back his Liberation Day tariffs a year ago, was a great buying opportunity. But what would it have been best to buy? Very few people would have suggested Japan’s Topix Nonferrous Metals sub-index. But it’s left such exciting sectors as European arms contractors or the Magnificent Seven tech platforms far behind, gaining more than 400%:

The Topix sub-index has 20 companies, the biggest of which, Fujikura Ltd., is worth $60.2 billion. It makes wires and cables, and over the last five years has left global stars like Rheinmetall AG, Nvidia Corp. or Tesla Inc. in the dust:

This is ultimately being driven by a heavenly confluence of growth and value. The sector makes vital components for data centers, helping to raise revenues. And, like most of corporate Japan, its stock started dirt cheap because the entire country has long been out of favor. The sector lagged the global semiconductor industry, but did follow its rise over the last three years — and then Sanae Takaichi, who is seen as likely to force through major corporate governance reforms, arrived as prime minister and catalyzed a big re-rating:

The shift in the way Corporate Japan is operating didn’t start with Takaichi, but she has been seen as a guarantee that it will continue. Mergers and acquisitions exploded last year. The first quarter alone has seen more deals than the whole of 2024, as illustrated by Nicholas Smith of CLSA in Tokyo:

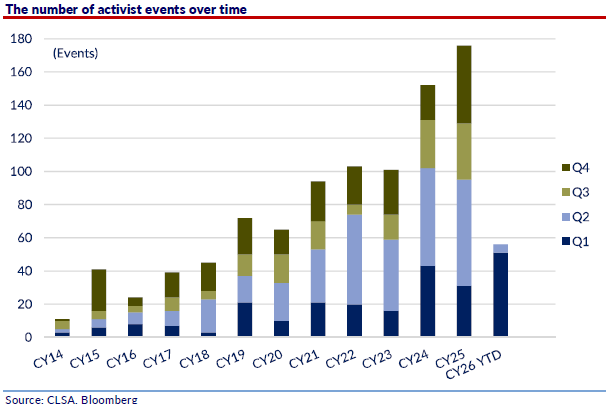

Corporate activism more broadly has also at last taken off. Smith shows in this chart that with foreign private equity groups looking for value, and many overcrowded sectors ripe for consolidation, it becomes far easier for activist investors to put pressure on managements:

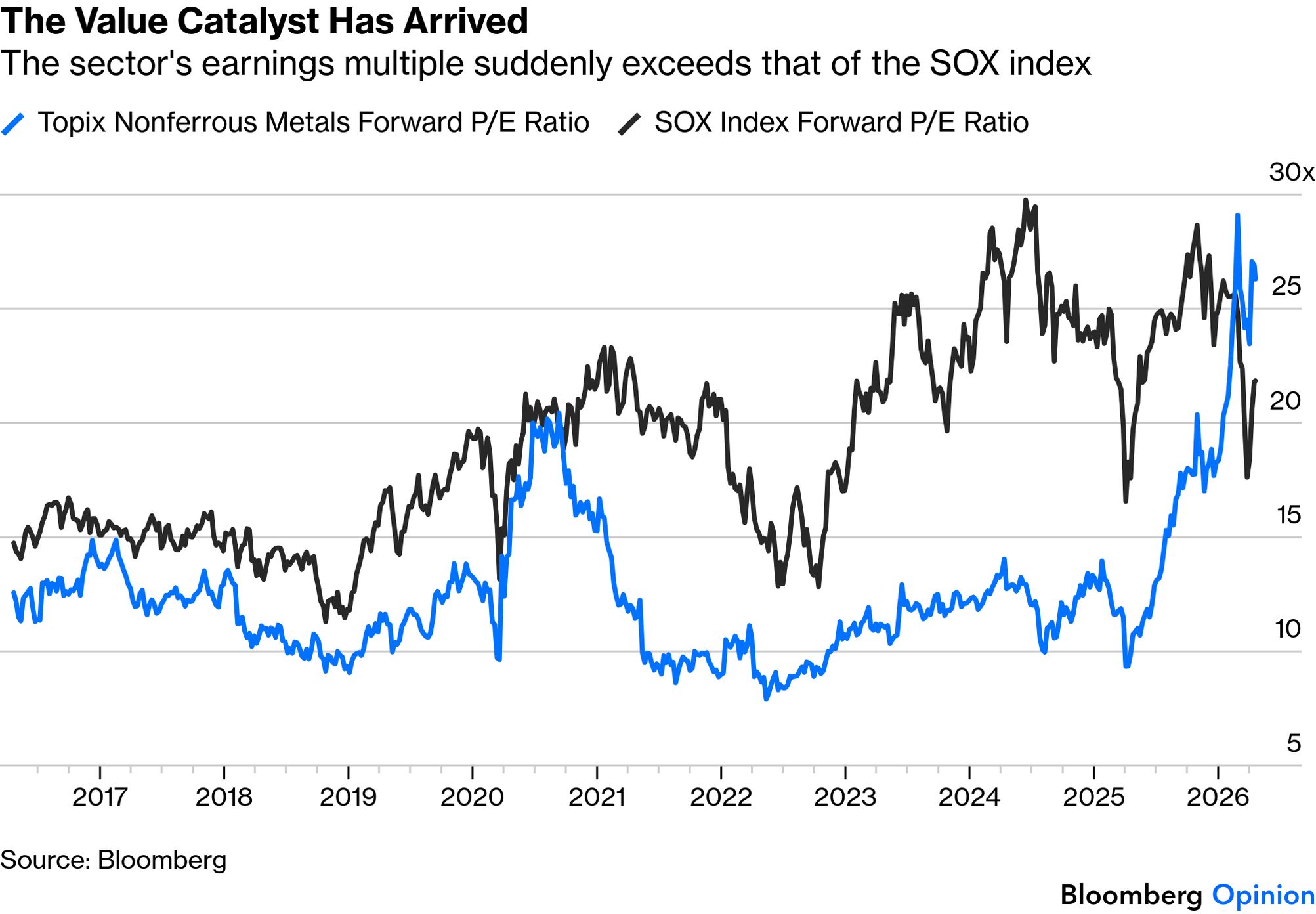

Is the opportunity gone? It’s hard to believe that there is much juice left in nonferrous metals after their extraordinary rally. On a blended 12-month forward basis, the sector’s price/earnings ratio has now overtaken the SOX semiconductor index, the main benchmark of the US chipmaking industry:

Value investors look for a catalyst, and it has arrived for these Japanese manufacturers. It is at least proof of concept that value investing can work. As Japan has many other sectors ripe for consolidation, the chances are that there are more opportunities, even if they don’t seem as exciting as Nvidia or Tesla. |

No comments:

Post a Comment