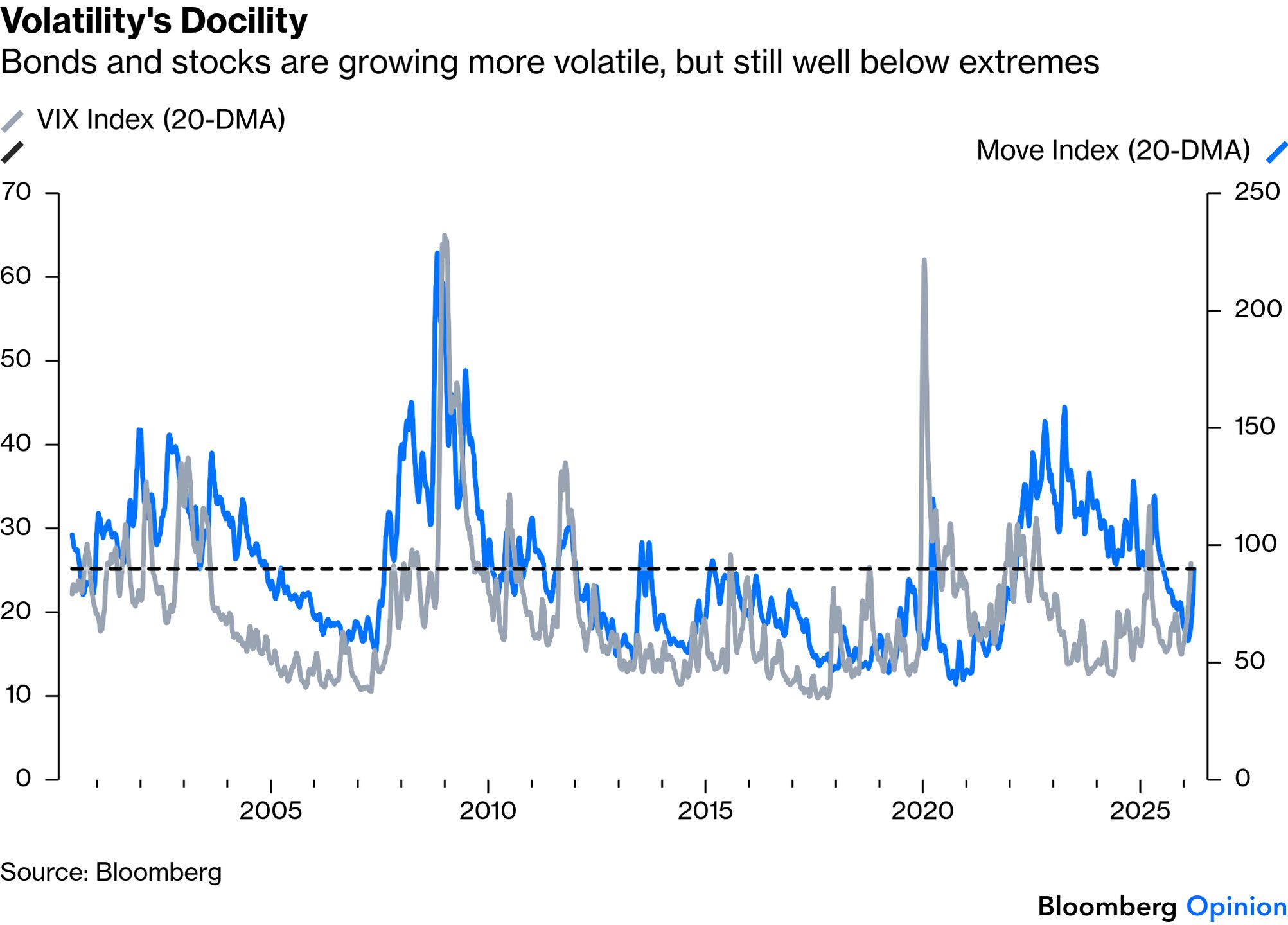

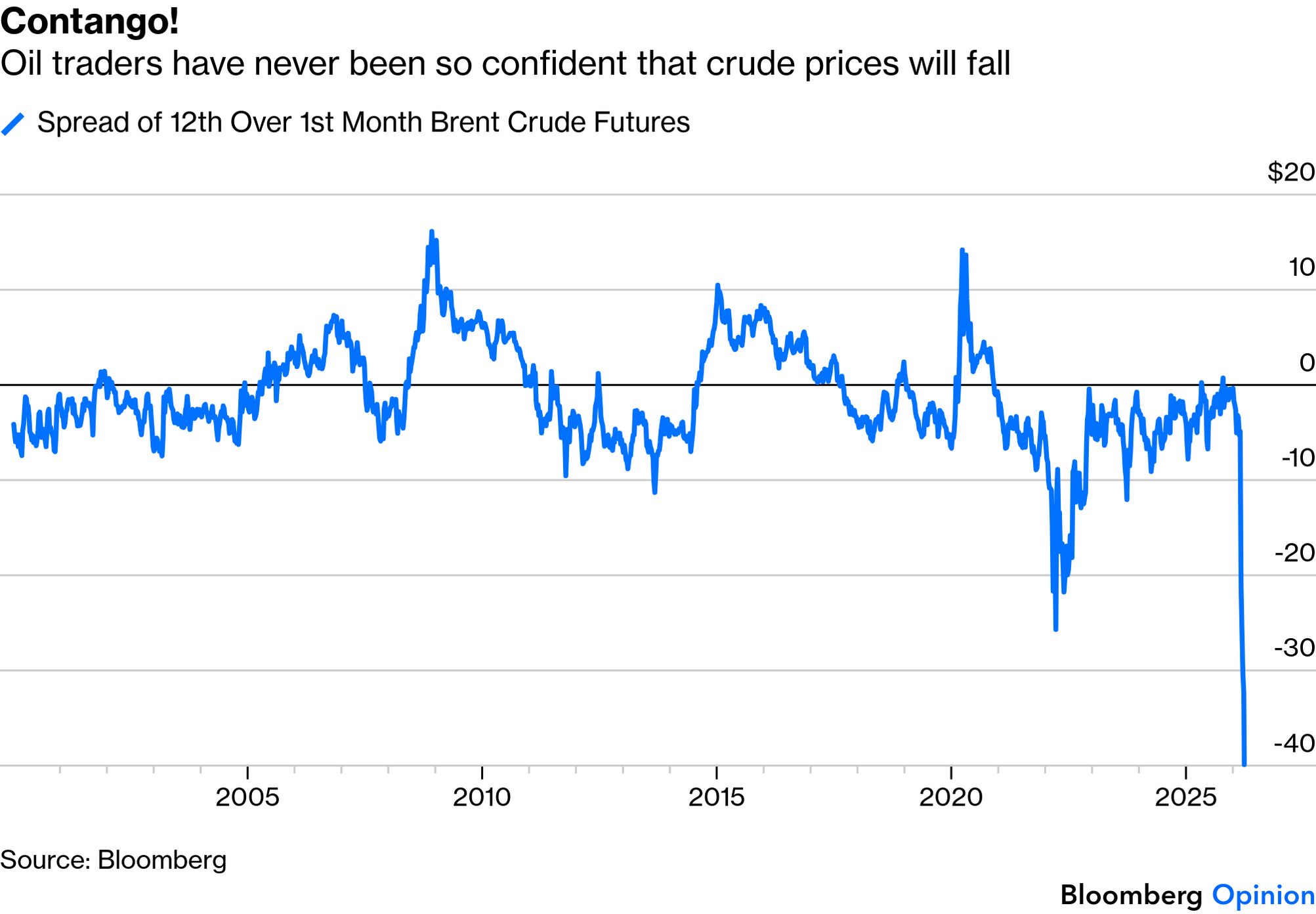

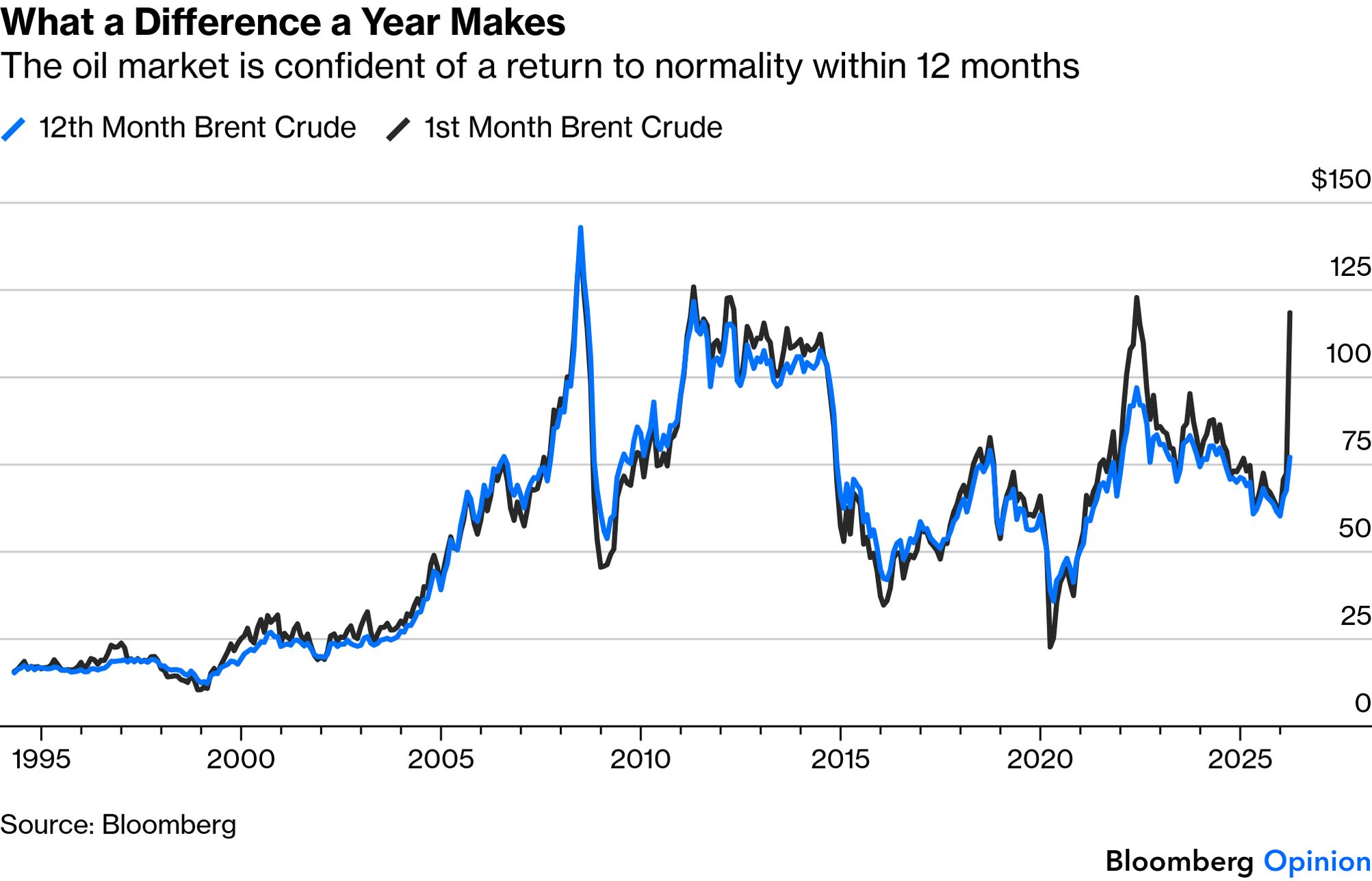

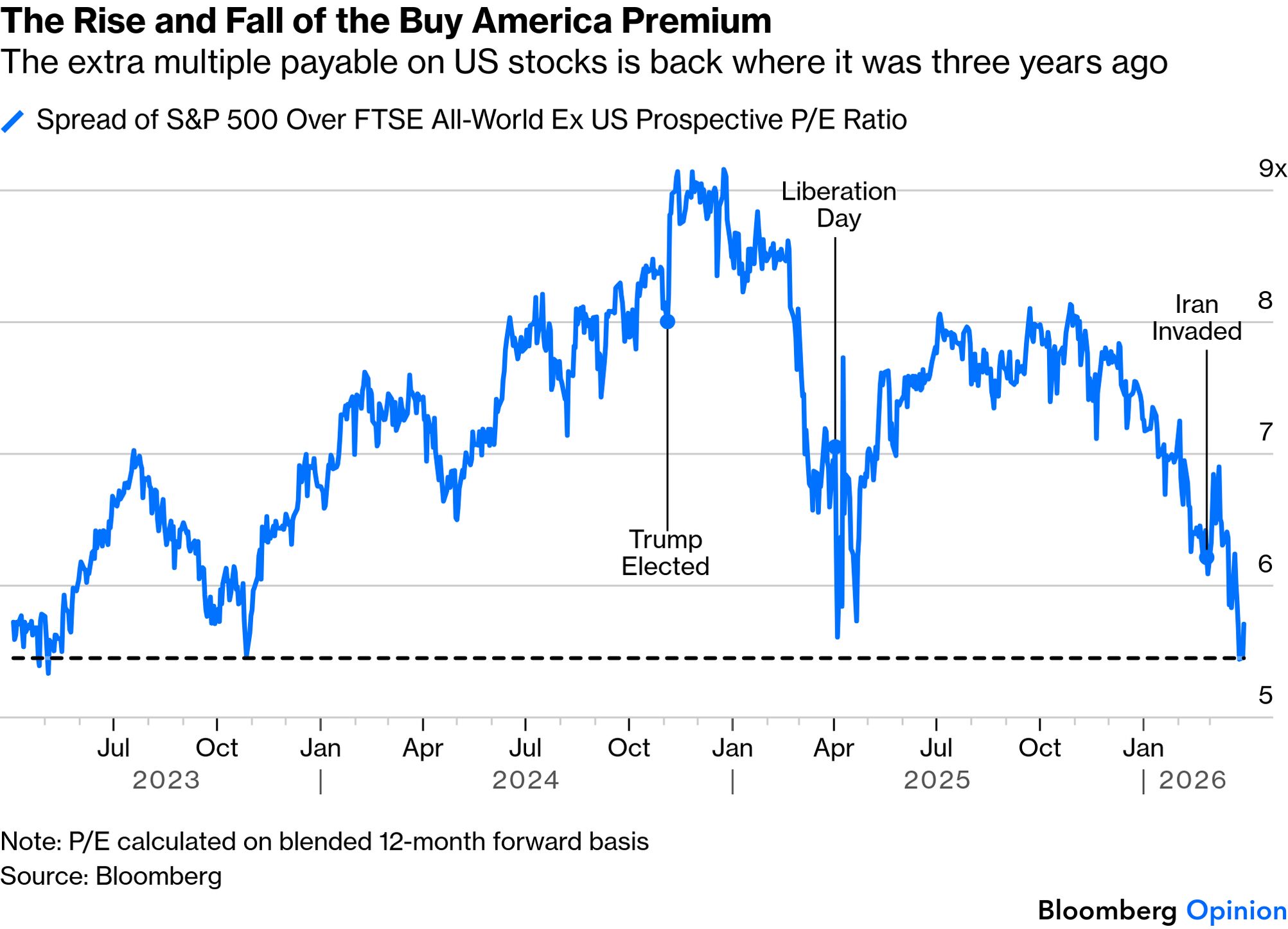

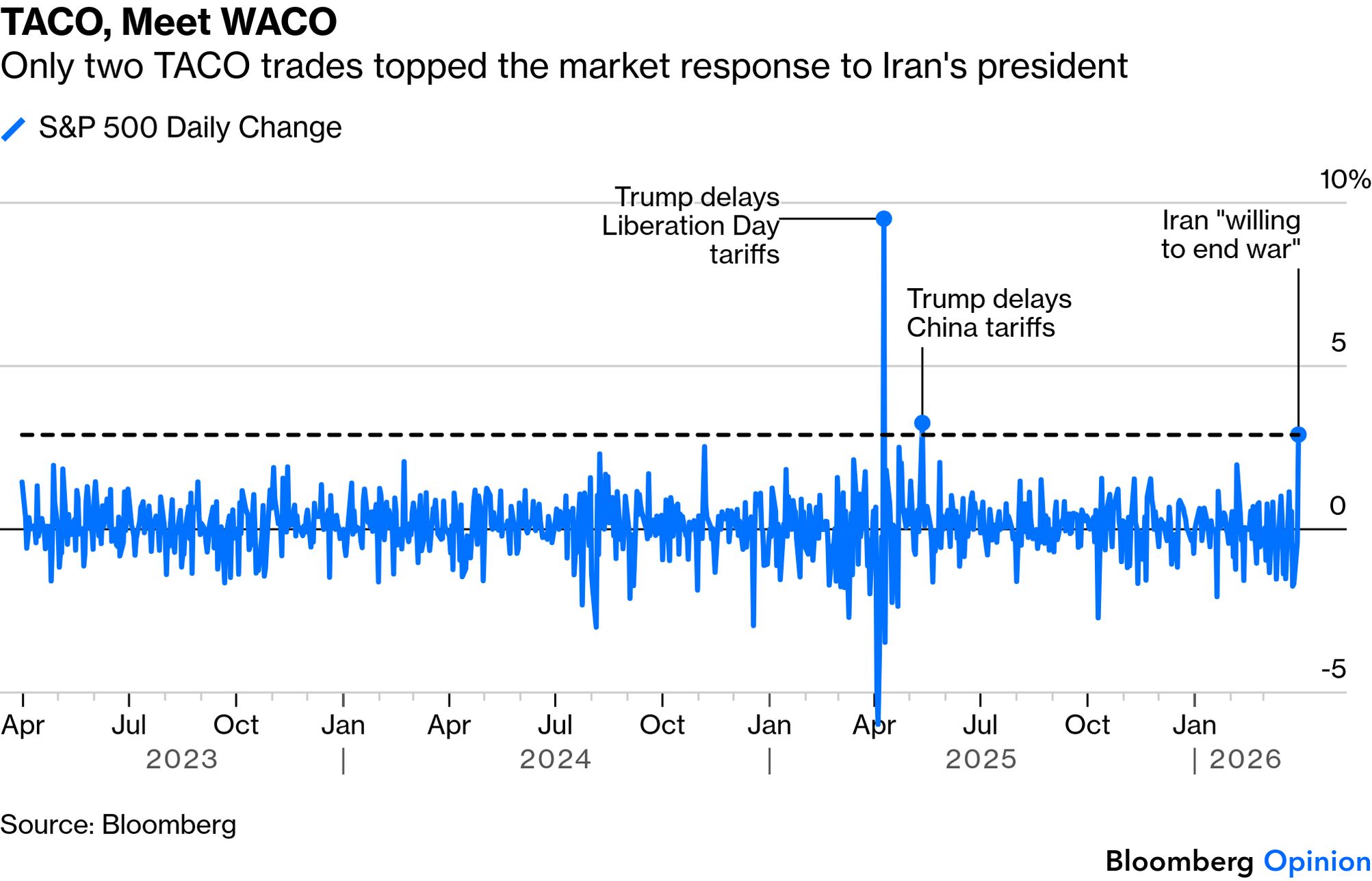

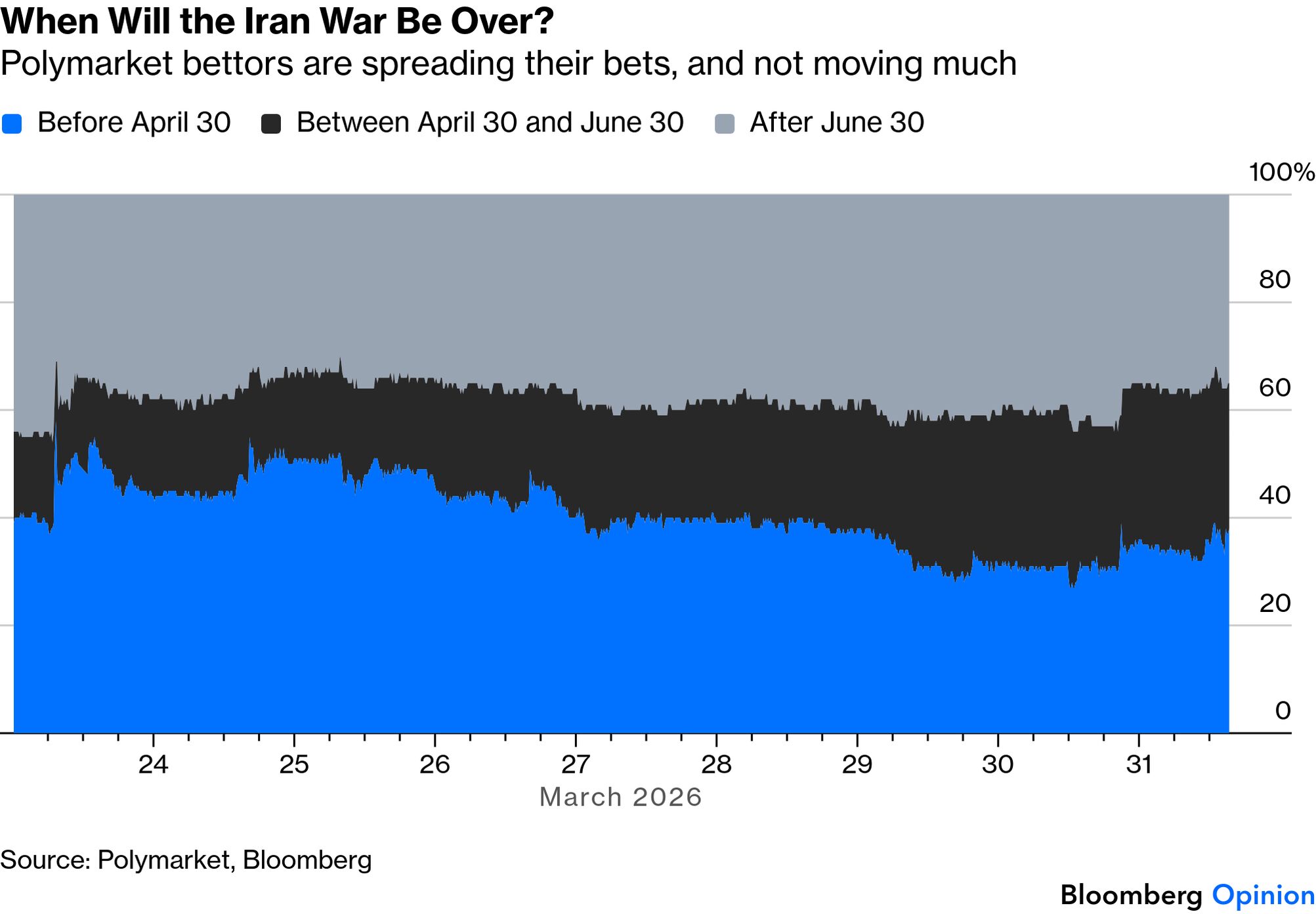

Four Questions for Passover | Much of the world is about to pause to ponder its faith. Ahead of Good Friday, Jews embark on Passover, the holiday that Jesus was celebrating at the Last Supper. An elaborate ritual to commemorate the Hebrew slaves' flight from Egypt, it involve a stylized meal, or seder, designed to evoke the Exodus. It starts with the youngest person asking four questions about why things are being done differently than on all other nights. I've long found this a useful exercise for looking at markets; what's different from usual, and can we explain it? In that spirit, on a day which markets seem to believe was an inflection point in the Iran war, here are 2026's four financial questions for Passover, all of which centered on another crisis in the Middle East. Why are stock markets still only 8% below their highs at the beginning of this war, when all the headlines speak of escalation and disaster? Even before Tuesday's rally (which we'll come to), this has been an oddly underdone reaction to a profound geopolitical shock. FTSE's index of all world stocks (including emerging and developed markets) peaked before the bombardment started, but is down only 8%. That's not the 10% many demand for a correction, and only the fifth-biggest selloff in this decade: While volatility, as measured for stocks by the CBOE VIX and for bonds by the MOVE index, has risen in the last month, it's still at unremarkable levels — particularly for bonds: So why the calm? Geopolitical shocks matter primarily through the effect they have on the supply and price of oil. A short interruption can be tolerated, while a sustained surge to higher levels cannot. Crude oil is in the deepest contango (meaning that futures are trading at levels that imply prices will come down in the future) on record: For those who find the contango concept tricky, here is how futures for Brent crude one month and 12 months ahead have moved since 1994. There is remarkable confidence that this oil spike is transitory: Ultimately, the belief persists that this war will conclude without lasting economic damage. Finally, as Points of Return has covered, there's no evidence as yet that this hurts companies' profits — a proposition that will be tested as they start to announce first-quarter results in a couple of weeks. The resilience of US markets compared to the rest of the world has far more to do with an ongoing rise in profit forecasts than with any great confidence in America as a jurisdiction. The premium that investors had to pay for US companies surged ahead of President Donald Trump's return to the White House and is now right back where it was three years ago. The decline has continued through the conflict in Iran: Why have stock markets just reacted so positively to a few words from Iran's president, when until now they had always been willing to buy or sell in response to a tweet from the US president? As Points of Return said Monday, the question is no longer Trump Always Chickens Out, but: Will the Ayatollahs Chicken Out? Tehran seems at present to have every incentive to fight on and very little to gain — given the awful damage it's already sustained — from a negotiated settlement. Any sign that the regime wants to talk, from Iranians themselves rather than from Trump's unsubstantiated claims, would therefore be huge for risk assets. So it proved. Tuesday in New York started with news that Iran had struck a Kuwaiti tanker at dock in Dubai — scarcely the action of a leadership hoping to reduce the tension. But at 12:30 p.m. came reports that President Masoud Pezeshkian had told EU officials that the country was "willing to end the war" but would need guarantees. It's not much, but it is the clearest official indication we've had that Iran might talk. The result was a WACO rally. Only the days when Trump chickened out of reciprocal tariffs last April and out of tariffs on China in May have seen bigger rallies in the last three years: Uncertainty over how long this conflict could last is so extreme that any sign of an interlocutor prepared to discuss a negotiated settlement is like manna from heaven for the markets. Ahead of Pezeshkian's remarks, Polymarket had been pricing roughly equal chances that the war ends in April, that it carries on into June, or lasts even longer: Since I drew this chart, the odds have shifted, with a 60% shot that the war ends in April and only 20% that it extends beyond June. Such a reduction in uncertainty would make markets happy. It doesn't mean they should be. The long-term prospects are darkening. Jean Ergas of Tigress Financial Partners argues that Iran's leadership now has what it wants, which is survival as a regime. The president's words show that it regards its legitimacy confirmed as a counterparty to any deal. Further, the guarantees that the regime requires before agreeing to a peace will likely entail a continuing ability to exert control over traffic passing through the Strait of Hormuz: At the end of the day they have a power that OPEC never had. Yamani knew that at the end of the day he had to sell his oil. These people are already cut off from the world economy. And now they have a chokehold on the rest of the world and they can decide who gets oil at what price. It's as though they become the world's most important central bank.

For now, the market is viewing this prospect positively. It's certainly terribly negative for oil importers, but it's not clear that an Iranian-controlled Strait is good for the US. Which raises another question. Why is Trump talking about ending the war without reopening the Strait when at all other times keeping it open has been regarded as a critical strategic objective? The president trailed the idea that the US could leave it to others to try to reopen the Strait on March 20 and followed that up on Tuesday morning by saying allies should "go to the Strait and just TAKE" oil if they wouldn't buy US jet fuel. An American military operation to force Iran to desist from blocking the passage would take a matter of many weeks. So Trump's comments Tuesday evening after markets closed that the US would leave Iran within two to three weeks seem to confirm that he isn't going to try to reopen the waterway. Note that the administration's official foreign policy strategy document, published four months ago, says: America will always have core interests in ensuring that Gulf energy supplies do not fall into the hands of an outright enemy, that the Strait of Hormuz remains open, [and] that the Red Sea remains navigable.

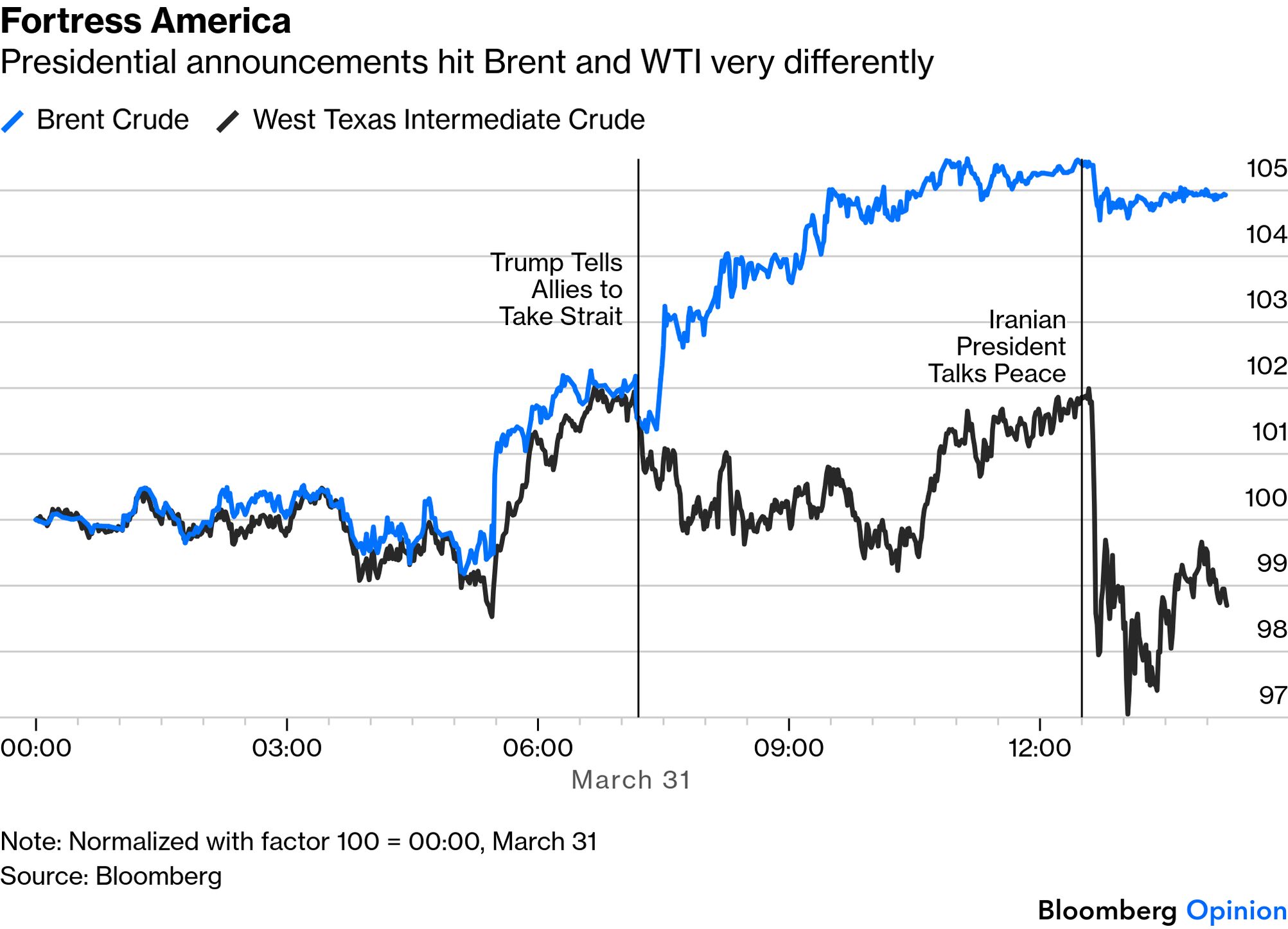

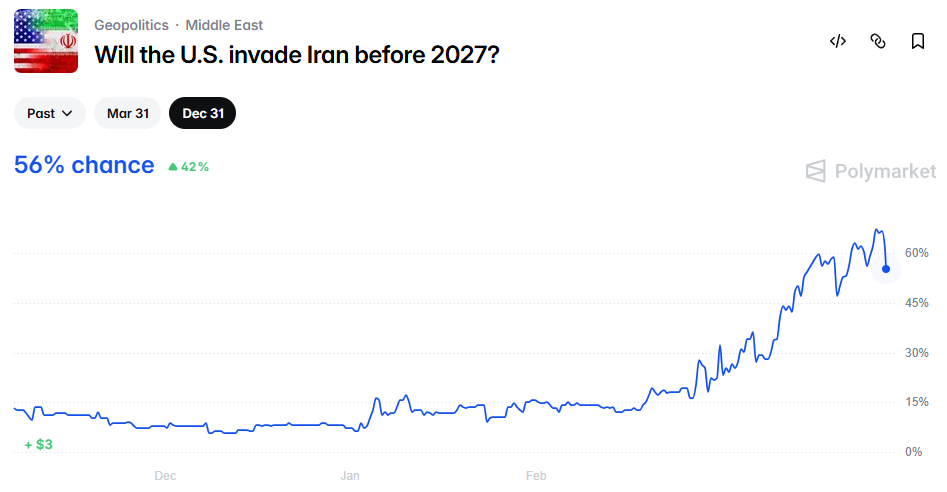

How is his new position tenable? It's true, after the shale revolution, that the US is less dependent on the Strait than Europe, Africa or Asia. That shows up in Tuesday's behavior of the different crude oil benchmarks. Brent (covering the rest of the world) surged after Trump said he could leave the Strait unopened, while West Texas Intermediate declined. Then WTI dropped impressively at reports that Iran would consider peace, while Brent barely budged. Financially, this is more of a problem for everyone else than for the US: But there are limits. The US is less affected than others, but gasoline at the pump has just passed $4 for the first time since the early months of the Ukraine war in 2001. The US addiction to the automobile means that this will hurt: Supplies of helium (necessary for making chips) and fertilizers come through the Strait, and the US needs them. A world with Iran as the effective price-setter for oil won't be great for American exporters. The calculation seems to be that Iran has shown that the Strait cannot be opened without risking American lives in a ground operation. Prediction markets put the chance of this happening at only 56%: Trump may be right politically to pay the price of leaving the chokepoint under effective Iranian control rather than preside over significant US casualties. Safeguarding American lives should be a priority for any president. But it means accepting a far worse strategic position than the US had before the war. Which suggests that it was a mistake to launch this conflict in the first place. Why did Trump choose to attack Iran when all his predecessors of the last half-century, Democrats and Republicans alike, disliked the Iranian regime just as much but decided it was too dangerous? This is a great question. What's done is done, but we all deserve an answer. And Israelis gathered for seders might want to ask their Prime Minister Benjamin Netanyahu whether it was such a good idea to kick the hornets' nest. I don't ask for much. But excitingly, a video we made a year ago, on the day after Liberation Day, has been nominated for a Webby award. The winner is decided by the people's choice, and I'd like your vote, please. You can find the video, made by the brilliant Ale Lampietti in defiantly low-fi fashion, here. It explained the absurdity of the formula behind the "reciprocal" tariffs. You can vote here. And thank you! |

No comments:

Post a Comment