Get the key 2026 travel demand catalysts and why Hilton, Delta, and Marriott stocks are breaking out, plus the guidance and technical levels... ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ |

| | Written by Dan Schmidt

The world is gearing up for a travel boom in 2026, and investors are starting to take notice with their stock rotations. Travel is moving from a laggard to a leadership group as demand drivers reaccelerate and visibility improves across airlines and hotels. With several major events on deck and premium spending holding up, the setup is improving even before the peak travel months arrive. The travel industry is one of the formerly downtrodden sectors, producing outsized gains to start 2026, and several fundamental factors are driving the rally. Three stocks could stand out as potential leaders if the 2026 travel boom materializes. Global Travel Demand Expected to be Strong in 2026 Pent-up demand, several catalysts, and economic dynamics are converging to create a strong environment for global travel. Many stocks in this space have already started breaking out, and the outlook has improved over 2025’s weak travel season. Some of the key factors that have investors intrigued by travel stocks include: - Return of Business Travel: You’re probably tired of hearing about the K-shaped economy, but the phenomenon is boosting a lagging area of the industry. Business travel is rebounding significantly, resulting in higher spending, as corporate clients tend to occupy the upper tier of the K and opt for premium options. Analysts at Morgan Stanley anticipate corporate travel budgets growing 5% in 2026, while hotel room rates are projected to increase 3.9%.

- Global Sporting Events: 2026 is shaping up to be a big year for international sports, with some of the world’s biggest spectator events occurring within a few months of each other. The Winter Olympics in Milan are currently underway, followed next month by the World Baseball Classic (WBC). But the biggest event, the 2026 FIFA World Cup, is scheduled for this summer across the U.S., Canada, and Mexico. It’s been more than 20 years since the U.S. last hosted a World Cup, but the 1994 tournament attracted more than 3.5 million attendees.

- Sector Rotation: Market mechanics are also at play here, and the travel industry is a beneficiary. The AI rally is starting to fizzle as investors seek safer sectors such as consumer staples and financials. Travel stocks have several catalysts on the horizon, and are a natural landing spot for some of the capital flowing out of tech right now.

3 Travel Stocks Breaking Out This Month If a breakout in travel stocks is imminent, it will likely get its start with these three companies. Each stock benefits from increased spending by more affluent clientele and has technical momentum behind its breakout. Hilton: Stock Breaking Out of Year-Long Consolidation Hilton Worldwide Holdings Inc. (NYSE: HLT) is a premium brand with an asset-light business model that makes it an intriguing investment in the current market environment. The company reported more than 515,000 rooms in its pipeline during its Q3 2025 report back in October and is targeting 6-7% annual growth in 2026 and 2027. Management also projects 2-3% growth in 2026 in the crucial Revenue per Available Room (RevPAR) metric, which was flat in 2025. The company reports its Q4 and full-year 2025 results on February 11 before the opening bell, and investors will be watching closely for 2026 RevPAR guidance projections. Analysts are bullish on the stock ahead of earnings. The stock received five different price target boosts last week, including new $330 targets from TD Cowen and Goldman Sachs.

The chart also shows a stock with strong bullish momentum. Despite a summer Golden Cross, the stock was stuck in a tight range for most of the second half of 2025 before breaking out above the 50-day simple moving average (SMA) in November. HLT shares have already reached several new all-time highs this year, and there could be more upside if the company reports strong earnings this week. Delta Air Lines: Corporate Travel Boosting Earnings Growth Delta Air Lines Inc. (NYSE: DAL) has soared to new all-time highs this year thanks to strong earnings growth boosted by corporate travel clients. The company released its Q4 2025 earnings report on January 13 and posted a slight EPS beat and a slight revenue miss, but the slowdown in sales growth can largely be attributed to the government shutdown. More importantly, the company reported a record $4.6 billion free cash position and projects 20% year-over-year (YOY) EPS growth in 2026, driven by further increases in premium cabin revenue.

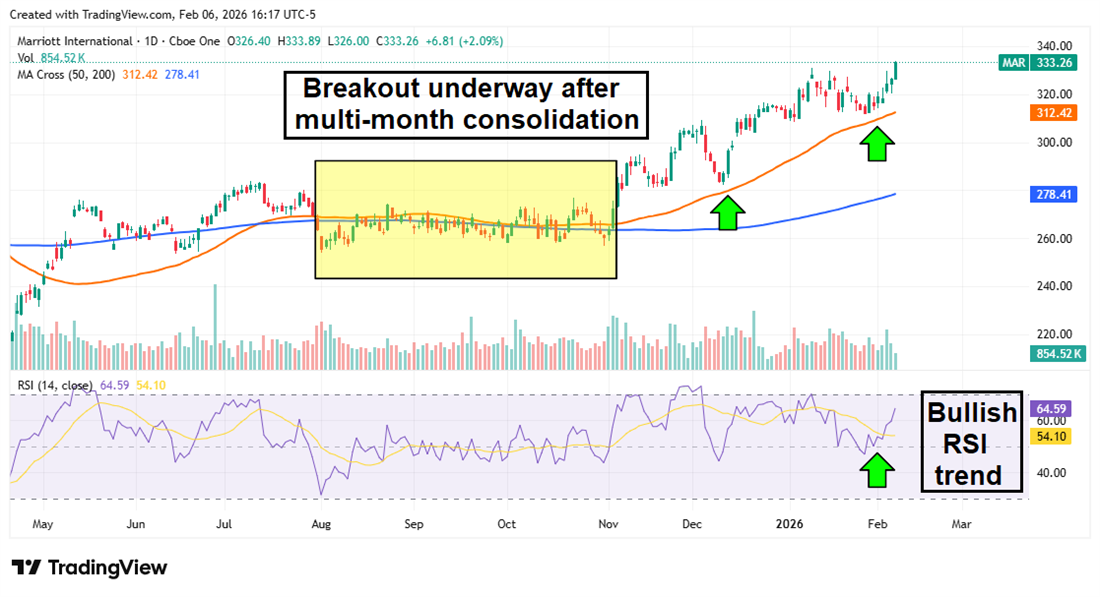

If the economy-class clientele recovers, the 20% EPS growth estimate could prove modest. The stock’s breakout is also backed by several technical signals, including strong support at the 50-day SMA and an uptrending Relative Strength Index (RSI). Marriott: High-End Clientele and Loyalty Program Provide Solid Floor Marriott International Inc. (NASDAQ: MAR) is also a global premium hotel brand, and its Bonvoy loyalty program is widely regarded as the industry standard, with nearly 237 million members. The company projects 2026 revenue to grow more than 6% YOY, and its RevPAR projections are improving after just 0.5% growth in Q3 2025. MAR shares spent most of the fall consolidating around the $270 mark in a very tight range before breaking out above the 50-day SMA in November. The 50-day moving average is now acting as support, with the RSI trending upward, providing strong bullish momentum to this rally. Marriott reported its Q4 results on Feb. 10 and posted a strong revenue beat and a slight earnings miss, but optimistic 2026 guidance sent the stock surging 8% after the release.”

Read This Story Online Read This Story Online |  After signing more than 220 Executive Orders… more than any president in American history… Donald Trump is preparing for one final move.

On February 24th — I have every reason to believe he will sign his Final Executive Order.

When I say that it's his FINAL executive order… Click here or below for this unbelievable story… |

| Written by Nathan Reiff

The year is off to an exciting start for quantum computing leader D-Wave Quantum Inc. (NYSE: QBTS) as the firm has announced major new contracts, acquired a key rival in Quantum Circuits, and set off some warning signs for investors with shelf registrations adding to about $330 million. The last of these seems to have offset the positive developments for many investors, as QBTS shares are down almost 20% year-to-date (YTD). Amid all the other updates as D-Wave aims to cement its position as a dual-focused quantum annealing and gate-model firm, the company is quietly expanding its reach into the defense sector through an expanded partnership aimed at serving U.S. air and missile defense needs. But can the project lead to real business gains for D-Wave? Or is it the latest in a series of developments that, while promising on paper, may not yet translate into sales boosts or profitability? Inside D-Wave's Latest Collaboration With Davidson and Anduril The late-January announcement reveals a collaboration with defense and aerospace consulting outfit Davidson Technologies and autonomous system defense tech firm Anduril Industries. The goal is to create hybridized quantum-classical computer applications for U.S. air and missile defense planning scenarios. The results of the joint efforts are already promising—D-Wave said that a hybrid quantum-classical approach yielded both a ten-fold reduction in time-to-solution and a 9% to 12% improvement in threat mitigation. In a 500-missile attack simulation, the partnership intercepted an additional 45–60 missiles, surpassing earlier efforts. D-Wave previously partnered with Davidson in early 2026, installing an Advantage2 quantum annealing computer system at the latter company's headquarters in Alabama. The partnership aimed to build on quantum research efforts with defense applications, with an eye toward serving the U.S. Department of Defense. Is Another Practical Application of D-Wave's Tech Emerging? This latest expansion builds on the earlier partnership between D-Wave and Davidson and moves toward a new practical use case for the Advantage2 system, which has received less hype in recent months as D-Wave has appeared to shift its focus toward more traditional gate-model quantum tech. Last year's Davidson partnership, while promising, was fairly open-ended and did not immediately make clear to investors how the company might translate an expansion into the defense space into real sales. The 2026 announcement, on the other hand, already comes with a bit of practical data suggesting it could be marketable for government and military agencies. With proof that quantum systems can outperform traditional classical ones emerging, there is a stronger case to be made that the military will gain strategic advantages by enlisting D-Wave in future operations. On the other hand, though, the company has yet to announce any significant U.S. military contracts and certainly faces significant competition if it does expand into the defense world. D-Wave does not seem to be positioning itself as a defense company overall—rather, it appears to be making a number of cases that quantum tech can be revolutionary across many industries and sectors. Investors may be excited about the potential for this technology to be transformative, or they may worry that D-Wave is spreading itself too thin—despite its significant cash reserves—to be truly successful in any of those cases. Has D-Wave's Partnership With Davidson Moved the Needle For Analysts? It's not entirely clear how Wall Street reacted to D-Wave's announcement of its expanded partnership. To end January, three firms—Rosenblatt Securities, Needham & Co., and Canaccord Genuity—all either reiterated Buy ratings or set fairly lofty price targets for QBTS shares. The company is broadly favored across the analyst class and now has a consensus price target above $38 per share, 80% higher than where the stock is trading as of mid-February. However, it's difficult to assess whether that positive analyst reaction was the product of D-Wave's defense move, as it could be related to other updates the company issued at the same time, including the announcement of a major quantum-computing-as-a-service (QCaaS) agreement with a Fortune 100 company and a key sale of an Advantage2 system to Florida Atlantic University. What is clear, however, is that the firm continues to make aggressive efforts to expand its reach into the new year. Investors will have to determine for themselves if D-Wave's approach is likely to be successful. Read This Story Online |  Market volatility hasn't disappeared — but investor behavior has changed.

Instead of chasing broad rallies, capital is increasingly flowing toward areas showing clear demand, real-world adoption, and long-term relevance. Artificial intelligence continues to stand out on all three fronts.

Across earnings calls and corporate spending plans, AI investment is no longer theoretical. It's being deployed, measured, and expanded — even as other sectors lose momentum.

That shift is creating selective opportunities for investors paying attention. 2 AI Stocks Positioned for the Next Phase of Growth |

| Written by Ryan Hasson

Shares of Rocket Lab Corporation (NASDAQ: RKLB), one of the fastest-growing names in the aerospace and defense space, have come under pressure recently. The stock is down nearly 10% for the month and more than 20% from its record-setting highs reached in January. As of the market close on Monday, Feb. 9, shares were off almost 24% from their peak, technically placing the stock in bear market territory. The pullback marks a clear shift in momentum after an exceptional run. But it also raises an important question for long-term investors: Has the growth story fundamentally changed, or is this simply a routine reset within a much larger uptrend? What Triggered the Pullback? The initial catalyst for the sell-off came in January, when Rocket Lab disclosed that a Stage 1 tank ruptured during qualification testing at its Long Beach, California, facility. While the headline spooked markets, Rocket Lab quickly noted that such outcomes are not uncommon during development testing. The company confirmed that there was no damage to surrounding facilities and that a replacement Stage 1 tank is already in production. Importantly, Neutron’s development program remains active. Still, uncertainty around whether the incident could lead to another delay for Neutron’s maiden flight weighed on sentiment. Rocket Lab stated that it would assess the impact and provide an updated timeline during its fourth-quarter earnings call later this month, leaving investors without immediate clarity. More recently, shares faced additional pressure after Congress declined funding for a planned 2031 Mars sample-return mission. That headline reignited concerns around long-term government funding visibility, adding to the negative news flow. After a massive multi-year rally that saw RKLB surge more than 1,300% over the past three years, and with the stock trading at extremely overbought levels earlier this year, some degree of profit-taking was inevitable once sentiment shifted. The Bigger Trend Remains Intact Despite the recent volatility, Rocket Lab’s broader technical structure remains constructive. The stock has pulled back toward its rising 50-day simple moving average and, so far, appears to be finding support in the low-to-mid $70s. That price action suggests a potential higher low within its longer-term uptrend. Crucially, shares remain well above the 200-day moving average, a key indicator that the primary trend is still intact. Even after the correction, Rocket Lab remains positive year-to-date, underscoring how strong the underlying move has been. Other space-related stocks have also experienced similar pullbacks in recent weeks, pointing more toward sector-wide consolidation rather than company-specific deterioration. With investor enthusiasm around the space economy still elevated and speculation building about a potential SpaceX IPO later this year, interest in the sector remains strong. From a technical standpoint, the picture would only materially weaken if RKLB were to fall below its 50-day moving average and drift toward its 200-day moving average. For now, that scenario has not played out. Wall Street Remains Supportive Analyst sentiment has remained notably resilient throughout the pullback. Rocket Lab currently carries a consensus Moderate Buy rating, and price targets have continued to move higher. Three months ago, the consensus target sat near $57. As of early February, it had climbed to almost $73. Several analysts characterized the Neutron testing issue as a routine part of launch vehicle development rather than a fundamental setback. Bank of America reiterated its Buy rating, while TD Cowen echoed confidence in Neutron’s long-term potential, emphasizing that no facility damage occurred and replacement hardware is already underway. Looking ahead, Rocket Lab’s upcoming earnings report will be a key inflection point. Investors will be focused on updates to Neutron’s launch timeline, progress on vertical integration, margin trends, and the company’s growing backlog. For now, the recent pullback appears less like the end of the story and more like a pause. One that, over the long term, risk-tolerant investors may view as an opportunity rather than a warning sign. Read This Story Online |  While everyone's making predictions about what might happen in 2026, we've identified 5 stocks with catalysts that are already locked and loaded.

These aren't hopes or projections. These are scheduled events, signed contracts, and approved projects that will play out over the next 12 months.

The difference between 100% gains and missing out completely? Positioning before 2026 arrives. Click here to get your free copy of this report |

| More Stories |

| |

|

To get John Authers' newsletter delivered directly to your inbox, sign up here. Profits are going up, even for companies that ar...

-

Trader Plans Bids at $94K, $82K for P...

-

PLUS: Dogecoin scores first official ETP ...

-

Hollywood is often political View in browser The Academy Awards ceremony is on Sunday night, and i...

|

No comments:

Post a Comment