U.S. Treasury Secretary Scott Bessent is the man who oversees America’s $37 trillion debt load.

No one has more insight into what’s happening with the US dollar… mounting US debt… of the likely changes coming to the US monetary system.

Not surprisingly…

His largest personal investment holding is gold.

Not tech stocks… Not U.S. Treasuries… Not “safe-haven” index funds or ETFs…

Gold.

When the U.S. Treasury Secretary’s largest personal holding is gold…

That’s known as “a clue.”

Wanna know who else sees what Bessent does?

Warren Buffett.

At last count, Buffett is sitting on $330 billion in cash. But he knows he cannot hold this much cash forever.

- Cash is losing purchasing power at roughly 22% a year (measured in gold).

- The US political system is printing money like it’s Monopoly cash

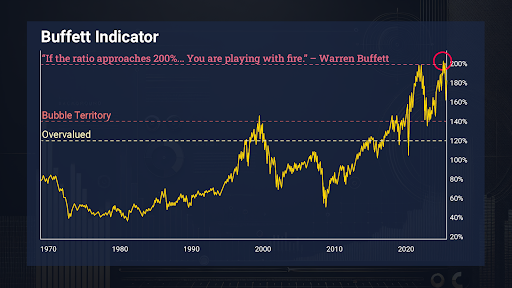

- And – most importantly – Buffett’s favorite indicator currently sitting just over 200% – which means US stocks are still more overvalued than they’ve ever been.

Every time the “Buffett Indicator” reaches a peak…

Gold goes on a tear for a decade or more. Every. Single. Time.

That’s why I believe Buffett is preparing to buy the one gold miner large enough to protect his cash. And here’s the kicker…

This large-cap miner is still trading at a 40% discount to its free cash flow.

What’s more, Trump recently tapped the CEO of this mining powerhouse to help lead America’s mining revival!

Add it all up and here’s what you get:

- The US Treasury Secretary is positioned for a major move in gold… and move that’s sure to come when he authorizes all the money required to finance more deficit spending.

- The world’s greatest investor needs a major gold position to protect his $330 billion cash pile… and there’s only one company big enough to do it.

- Trump has entrusted the CEO of the #1 major gold miner to lead a Renaissance in US mining.

You want to be in position before that happens.

You still have time to “front run” the world’s greatest investor by taking a stake in the one mining company big enough to handle his $330 billion cash hoard.

That’s why I’ve prepared a private gold briefing with:

- The name and ticker of the company Buffett is likely targeting

- Four tiny gold miners with “anomaly” upside potential up to 100X

- A special bonus pick that doesn’t mine gold at all – collects royalty income on mines it financed

Go here to get the name and ticker of Buffett’s next big move into gold.

Regards,

Garrett Goggin, CFA, CMT

Chief Analyst and Founder, Golden Portfolio

Southern Company: From Nuclear Risk to AI Reward

Written by Jeffrey Neal Johnson. Published 8/26/2025.

Key Points

- Unprecedented electricity demand from the technology sector is creating a historic growth opportunity for the company.

- A massive, regulator-approved capital investment plan provides a clear blueprint for expanding generation to meet this new demand.

- The company's strategic expansion translates into a visible, long-term pathway for earnings growth and stable shareholder returns.

The rapid expansion of artificial intelligence (AI) is creating an unprecedented challenge for the U.S. economy: an insatiable demand for electricity. For investors, this demand also represents a significant opportunity. At the heart of this energy surge is Southern Company (NYSE: SO), one of the nation's largest energy providers.

For years, the company's narrative was dominated by the immense cost and risk of bringing the first new nuclear reactors in decades online. With that chapter now behind it, Southern Company has pivoted toward a far more powerful investment thesis.

Trump's AI Agenda: The 9 stocks poised to benefit most (Ad)

While many are busy chasing the usual AI trends, a bigger opportunity is quietly brewing—and most are missing it. Imagine a major shift in how and where AI is built, opening up incredible wealth opportunities for those in the know.

I've found 9 AI companies primed to lead this change. These aren't the tired "AI hype" stocks; they're companies with real US operations, proven revenue growth, and deep AI integration.

It has moved from managing construction risks to executing a clear, large-scale growth strategy—positioning itself as a core infrastructure provider for the digital era.

The 50-Gigawatt Opportunity

The primary catalyst driving Southern Company's next phase is a historic surge in industrial and technological growth across its service territory. The Southeast—particularly Georgia—has become a global hub for data centers, the massive server farms that power everything from cloud computing to generative AI. This migration has produced an energy-demand forecast unlike any seen in decades, fundamentally reshaping the utility's growth trajectory.

Management has identified a "large load pipeline" of over 50 gigawatts of potential new demand from these customers. To put that in perspective, one gigawatt can power roughly 750,000 homes—making this pipeline an opportunity of monumental scale.

In its second-quarter 2025 earnings report, Southern Company noted that electricity consumption from data-center clients rose 13% year-over-year. That real-time growth validates the company's aggressive expansion plans and gives investors concrete evidence of accelerating demand.

How Southern Will Capture the Boom

Southern Company has secured a regulator-approved expansion roadmap. The cornerstone is Georgia Power's recently approved 2025 Integrated Resource Plan (IRP), which green-lights the utility to add roughly 10 gigawatts of new generation capacity—primarily via natural gas plants and battery storage facilities.

This plan is financially feasible largely because the multi-billion-dollar cash drain from the Plant Vogtle nuclear project has ended. With the final reactor unit online, the company stabilized its balance sheet, closed out years of heavy construction spending, and freed capital to invest in growth.

The IRP approval underpins an expanded five-year base capital plan that has risen to $76 billion. In a regulated utility model, these approved expenditures are added to the rate base—the value of assets on which the company earns a set return. A larger rate base translates directly into higher, more predictable earnings over time and supports Southern Company's long-term EPS growth target of 5%–7%.

What This Means for Shareholders

This strategic pivot delivers a compelling financial outlook. The $76 billion capital plan becomes a sustained driver of EPS growth, and the market is starting to take notice: Southern Company trades at a forward P/E of about 21.8, a premium to many slower-growing peers, suggesting that investors are pricing in this accelerated growth trajectory.

At the same time, the company retains its reputation for financial stability and reliable shareholder returns. With a debt-to-equity ratio of 1.69, Southern maintains a balanced capital structure that can fund ongoing expansion without compromising its credit profile.

For income-focused investors, the stock remains attractive, offering a dividend yield near 3.16%. Southern Company's dividend has increased for over 20 consecutive years, underscoring its commitment to a steady income stream.

Moreover, with a beta of 0.38, the stock exhibits notably lower volatility than the broader market, adding a defensive element to its growth story. The investment case for Southern Company has fundamentally evolved—from weathering risk to capitalizing on a clear structural opportunity.

Armed with a de-risked financial profile, a validated growth catalyst, and a stable dividend, Southern Company is now positioned as a core holding for investors seeking exposure to the build-out of America's digital infrastructure.

to bring you the latest market-moving news.

This message is a paid sponsorship provided by Golden Portfolio, a third-party advertiser of TickerReport and MarketBeat.

Contact Us | Unsubscribe

Copyright 2006-2025 MarketBeat Media, LLC dba TickerReport.

345 N Reid Place #620, Sioux Falls, South Dakota 57103. USA..

No comments:

Post a Comment