A Message from Golden Portfolio U.S. Treasury Secretary Scott Bessent is the man who oversees America’s $37 trillion debt load. No one has more insight into what’s happening with the US dollar… mounting US debt… of the likely changes coming to the US monetary system. Not surprisingly… His largest personal investment holding is gold. Not tech stocks… Not U.S. Treasuries… Not “safe-haven” index funds or ETFs… Gold. When the U.S. Treasury Secretary’s largest personal holding is gold… That’s known as “a clue.” Wanna know who else sees what Bessent does? Warren Buffett. At last count, Buffett is sitting on $330 billion in cash. But he knows he cannot hold this much cash forever. - Cash is losing purchasing power at roughly 22% a year (measured in gold).

- The US political system is printing money like it’s Monopoly cash

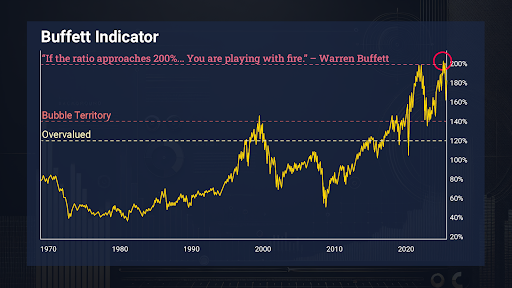

- And – most importantly – Buffett’s favorite indicator currently sitting just over 200% – which means US stocks are still more overvalued than they’ve ever been.

Every time the “Buffett Indicator” reaches a peak… Gold goes on a tear for a decade or more. Every. Single. Time. That’s why I believe Buffett is preparing to buy the one gold miner large enough to protect his cash. And here’s the kicker… This large-cap miner is still trading at a 40% discount to its free cash flow. What’s more, Trump recently tapped the CEO of this mining powerhouse to help lead America’s mining revival! Add it all up and here’s what you get: - The US Treasury Secretary is positioned for a major move in gold… and move that’s sure to come when he authorizes all the money required to finance more deficit spending.

- The world’s greatest investor needs a major gold position to protect his $330 billion cash pile… and there’s only one company big enough to do it.

- Trump has entrusted the CEO of the #1 major gold miner to lead a Renaissance in US mining.

Final confirmation of my prediction could come by August 15th — when Buffett’s 13F filing hits the tape. You want to be in position before that happens. You still have time to “front run” the world’s greatest investor by taking a stake in the one mining company big enough to handle his $330 billion cash hoard. That’s why I’ve prepared a private gold briefing with: - The name and ticker of the company Buffett is likely targeting

- Four tiny gold miners with “anomaly” upside potential up to 100X

- A special bonus pick that doesn’t mine gold at all – collects royalty income on mines it financed

Go here to get the name and ticker of Buffett’s next big move into gold. Regards, Garrett Goggin, CFA, CMT

Chief Analyst and Founder, Golden Portfolio

Today's Bonus Article D-Wave Rises 12% in 1 Day, Beating Rivals: What Caused the Spike?Written by Nathan Reiff

Despite tripling in value in the last six months, shares of D-Wave Quantum Inc. (NYSE: QBTS) seemed to be rallying once again with an increase of nearly 26% over a five-day period in mid-July 2025. This surge comes after D-Wave shares traded mostly horizontally for about two months starting in mid-May. Rivals including Quantum Computing Inc. (NASDAQ: QUBT) and IonQ Inc. (NYSE: IONQ) rose as well, but only by about 10% each over the same period. D-Wave managed to log a 12% increase in share price in just a single day. What's behind the latest spike, and, perhaps more importantly, could it signal a push toward new record highs? The Hunt for Profitability Many quantum computing stocks have risen in recent weeks as investors have tracked noteworthy technological achievements. D-Wave had its own milestone earlier this year when it achieved a feat known as quantum supremacy for the first time, while rival Rigetti Computing Inc. (NASDAQ: RGTI) announced in July that it had successfully halved its median two-qubit gate error rate, sending RGTI shares skyrocketing by about 40% in a week. These achievements are undoubtedly important for firms like D-Wave, as they signal crucial technological advances that presumably bring these companies closer to bringing mass quantum computing to market. They can also help fuel investor speculation (indeed, some portion of the gains D-Wave and other quantum firms saw in mid-July may be attributable to investor optimism inspired by Rigetti). However, technical advances do not necessarily have a direct impact on top-line performance. Like its competitors, D-Wave has found profitability to be elusive so far. Although the company's revenue, just $15 million in the latest quarter, was well above analyst predictions, it is still reliant on major quantum rig purchases from large institutions and governments. However, the company posted its smallest quarterly losses since going public for the same quarter. Further, D-Wave has a key leg up as it works toward sustained profitability: its strong balance sheet. The company's recent $400-million ATM offering, which brings reserves close to $1 billion, was especially important in the building of that balance sheet. Market Sentiment Is Strong While profitability is challenging for the entire quantum computing industry, building investor hype is not. There seems to be a feeling across the investment world that quantum firms are approaching a point where technology will become widespread. NVIDIA Corp. (NASDAQ: NVDA) CEO Jensen Huang was one of the latest significant tech figures to fuel that fire when he remarked that quantum computing as a field may be on the verge of an "inflection point" in comments made in June. For this reason, it's also possible that D-Wave's recent surge has resulted from further speculation. In the midst of the mid-July spike, investors purchased more than 201,000 call options for QBTS shares in a single day, a full two-thirds higher than daily averages. Because other investors often interpret the purchase of call options as a signal of bullishness, the fact that options trading was up may have helped to spur a new round of speculation. Analyst Bullishness Remains, But Beware the Hype Analysts are uniformly optimistic about D-Wave's potential, as the company has garnered eight Buy ratings against zero Holds or Sells. In June, a wave of analysts either reiterated Buy ratings, increased price targets for QBTS shares, or both. In early July, Cantor Fitzgerald analysts initiated coverage of QBTS with an Overweight rating and a $20 price target. This is good news for D-Wave, although the company is trading some 24% above the consensus price target. However, investors would be wise to remember that even strong bullishness from analysts across Wall Street is likely based on D-Wave's presumed potential. Considering real earnings and sales figures, D-Wave trades at sky-high valuations, like many of its quantum computing peers. For example, the company has a price/sales ratio of more than 624 and a price/book ratio of 82.0. Could D-Wave shares priced below $20 each one day seem like an unbelievable bargain? Absolutely, but in the meantime, investors will have to bide their time, and of course, there is no guarantee that will ever be the case. |

No comments:

Post a Comment