Ticker Reports for July 22nd

A Bullish Storm Is Brewing for High-Yield Verizon's Share Price

Numerous factors, including Verizon’s (NYSE: VZ) valuation, yield, business traction, and analysts' sentiment, are aligning, setting the stock price up for a significant advance. Verizon’s 5G networks are gaining traction with consumers and businesses, revenue is growing, cash flow is improving, and the capital return is increasing annually.

The critical factors are cash flow, free cash flow, and capital return. Verizon is a deep-value, high-yield stock that yielded more than 6% as of late July. It is on track for inclusion in the Dividend Aristocrats Index within a handful of years.

The highlight from Q2 is that margins improved throughout the report for this telecom company. The company’s EBITDA (earnings before interest, taxes, depreciation, and amortization), adjusted EBITDA, earnings, cash flow, and free cash flow all improved compared to last year and at an accelerated pace relative to revenue.

The net result is that the company improved its balance sheet condition in the first half while paying the dividend, and improvements are expected to continue as the year progresses.

The balance sheet reflects reduced cash and assets at the end of Q2, offset by a more significant reduction in liabilities, improved leverage, and a 4% increase in equity.

Price action following the report is bullish. The market advanced nearly 5% at the close of the session, indicating support at a critical level and a high likelihood of advancing. Bullish signals include a spike in trading volume, an advance from the six-day EMA, a bullish crossover in the stochastic, and an almost-crossover in the MACD.

The crossovers are particularly telling; assuming MACD completes its crossover, the pair will form a strong signal, with both lows in their respective ranges, indicating a move to the top of the long-term range is likely.

Verizon Wows Market With Beat and Raise Quarter

Verizon had a solid Q2 with revenue growing by 5% and outpacing the consensus estimate by 235 basis points. The strength was driven by all segments, with gains in the core wireless segment led by equipment. Equipment sales topped 25% year-over-year growth, offset by a smaller 2.2% in services.

Net additions were good across the network. FIOS continues to gain traction and is on track to reach its goals. The only bad news is that the net additions are slowing. However, sustained growth, better-than-expected quarterly numbers, and increased market share offset the slowdown.

The margin news is good. The company has been working on its operational quality for years, and the tailwind was amplified by favorable tax news. The takeaway is that earnings and free cash flow are growing faster than the pace of capital return growth, which has been approximately 2% over the past three to five years.

The company is well-positioned to continue paying its distribution and sustaining the growth pace well into the next decade, likely for longer.

Guidance is another factor expected to propel this market higher in the second half of 2025. The company raised its outlook for margin and earnings, positioning the midpoint above MarketBeat’s reported consensus.

Based on the trends and expected surge in IoT growth predicted for this year, the company may outperform this target. The growth of the IoT will be underpinned by AI and the proliferation of AI-enabled applications, particularly among businesses.

Robust Analyst Trends Will Strengthen in Q3

The analysts' trends were robustly bullish leading up to the Q2 release and are likely to remain so in Q3. They include increasing coverage, firming sentiment with the Moderate Buy rating edging toward an outright Buy, and an uptrend in the price target.

The consensus price target is of interest because it was $47 in late July, sufficient to match recent highs, and the trend suggests a move into the high-end range. Recent revisions put this market in the mid-$50 range, a 30% increase and a three-year high when reached.

How to Collect Up To $5,917/mo From Trump's Made In USA Boom

How to Collect Up To $5,917/mo From Trump's Made In USA Boom

Palantir Bulls and Bears Set for an August Showdown

Palantir Technologies Inc. (NASDAQ: PLTR) continues to exceed expectations. As of July 21, the stock was up 102% in 2025. Perhaps more impressively, PLTR stock is up more than 68% after a pullback of approximately 40% between mid-February and early April.

The next significant catalyst for Palantir may come from its earnings report, which is scheduled for August 4. The company has a history of beating revenue expectations, and is now solidly profitable. The question is whether it can live up to investors’ elevated expectations.

Even if Palantir delivers blowout earnings, many investors find it hard to see past its lofty valuation, even in a pricey tech sector. PLTR stock is trading at around 665x earnings and 126x sales.

Even for a company with a healthy balance sheet, many investors aren’t buying into future growth that will depend on flawless execution and exponential growth.

Palantir stock sits at the intersection of bullish momentum and valuation anxiety. The deciding factor likely comes down to who’s buying PLTR stock, and the answer may be a surprise.

PLTR Stock Has Technical Strength That Points to Bullish Momentum

Palantir bulls will say don’t fight the chart, and they have a case. Since hitting its low in April, the PLTR stock chart shows a classic bullish pattern of higher highs.

The stock also continues to find support above its 50-day simple moving average (SMA), confirming plenty of willing buyers. Adding to the bullish case is that even with overall volume being down due to seasonal factors, the stock’s green (i.e., positive) days are supported by solid volume.

Skeptics could point to the relative strength indicator (RSI), which is between 60 and 70. However, since the stock’s recent run, the RSI has been moving in a range that suggests neither overbought nor oversold conditions, which adds further support to the idea that the stock isn’t breaking down from a technical perspective.

Traders Are Growing More Cautious

Traders Are Growing More Cautious

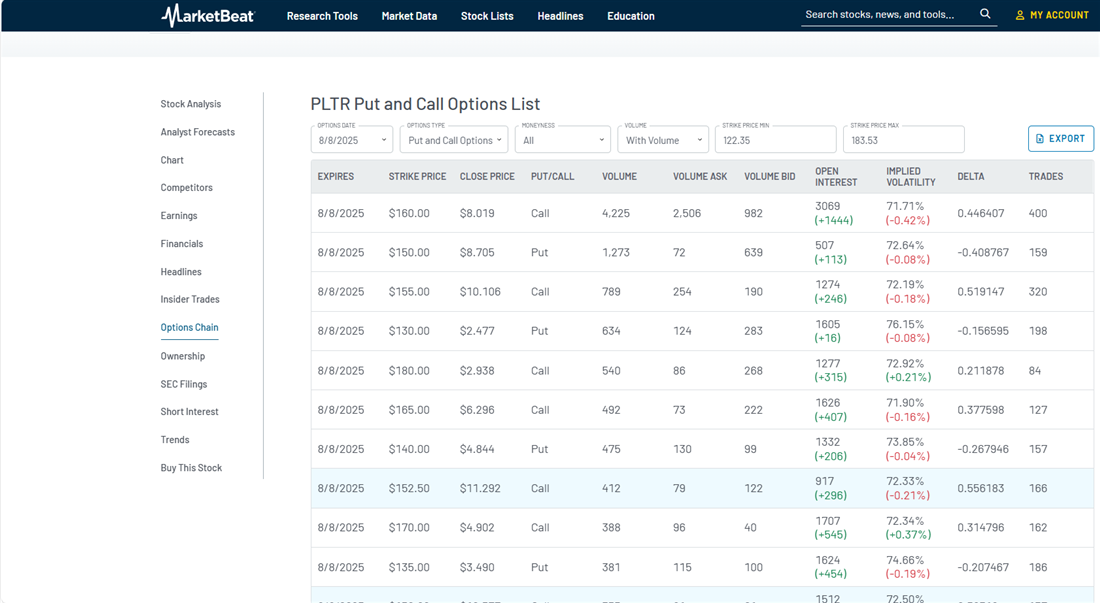

The Palantir options chain for August 8 contradicts the current sentiment of retail and institutional investors. That’s approximately one week after the company reports earnings on August 4.

Traders are showing increased interest in near-the-money puts, while call volume fades at higher strike prices. At the same time, implied volatility is beginning to cool, suggesting expectations for explosive upside are waning.

This activity implies that options traders see Palantir’s recent rally as potentially losing steam and are positioning for a period of consolidation or downside in the near term.

What May Be Causing the Disconnect in PLTR Stock?

Palantir shareholders will remember that PLTR stock has been added to the S&P 500 and the Nasdaq-100 in the last nine months. This is more than just a symbolic designation. Inclusion in those indexes means that Palantir stock is rising because of an influx of capital into passively managed funds and AI-focused ETFs.

This these automatic purchases are likely a key reason for Palantir stock's increase. They are driven by the company’s expanding market capitalization and AI sector position, rather than its fundamentals. Importantly, this contradicts the narrative that PLTR stock is a meme stock being mindlessly driven higher by retail investors.

But fund investors understand that money can flow out of funds as quickly as it came in. That's why Palantir’s upcoming earnings report will continue to draw interest from investors. PLTR stock is priced for perfection, and then some. If the company doesn’t deliver a blowout report, it could give fund investors a reason to trim their positions.

If that does happen, it’s not a reflection of the company's value but merely a healthy pullback that could set investors up for higher highs in the future. That’s the growing sentiment among analysts, such as Dan Ives of Wedbush, who has set a $160 price target for PLTR stock.

WARNING: Your Cash Could Be Worthless Overnight

WARNING: Your Cash Could Be Worthless Overnight

3 Reasons Palo Alto Networks Is Becoming a Wall Street Favorite

Up more than 10% year-to-date (YTD) and about 20% in the past 12 months, cybersecurity firm Palo Alto Networks (NASDAQ: PANW) has weathered the initial storm of tariff uncertainty well. In a sign of support for PANW, institutional investors have taken a particular interest in the firm in recent months.

In the first quarter alone, for example, HighPoint Advisor Group bulked up its stake by 20%, Crestwood Advisors Group by 18%, and J.W. Cole Advisors by 81%, among others. In the last 12 months, institutional buyers of Palo Alto shares have outnumbered institutional sellers nearly three to one, while institutional inflows have outpaced outflows by a similar margin. Institutional ownership for the company is roughly 80%.

Though it's not always possible to confirm what draws institutional investors to a particular stock, a few likely catalysts include Palo Alto's excellent fundamentals and recent performance, its strong next-gen security products, and the company's shift toward artificial intelligence (AI) platformization.

1. Top- and Bottom-Line Performance, Margins, and Forecasts Strong

Palo Alto Networks' latest earnings report was solid across the board and affirmed its stable financial standing. The company posted double-digit revenue growth of more than 15% year-over-year (YOY) to about $2.3 billion, ahead of analyst predictions. Earnings per share (EPS) of 80 cents also beat expectations. The company's margins are also improving—its non-GAAP operating margin for the quarter was 27.4%, close to two full percentage points higher than 25.6% in the prior-year quarter. What's more, Palo Alto expects these trends to continue, with fiscal 2025 operating margin anticipated in the range of 28.2% to 28.5%.

With growing revenue and earnings and improving efficiency, Palo Alto is well prepared for future growth. Further, the company's strong cash position provides an extra level of security should unexpected geopolitical uncertainty enter into the picture as well. Externally, analysts believe Palo Alto is positioned to continue to build on recent gains as well. Analysts expect the firm to grow its earnings by a sizable 19.3% in the coming year.

2. Next-Gen Security Products Take the Lead

Behind Palo Alto's YOY gains in the latest quarter are its next-generation security tools, Prisma and Cortex. Prisma is a cloud-based security solution while Cortex utilizes AI and machine learning. Thanks to Palo Alto's subscription-based service model, its next-gen security tools have experienced rapid annual recurring revenue (ARR) growth.

Indeed, for the latest quarter, these products had an increase of 34% YOY to ARR, reaching $5.1 billion. Palo Alto Networks expects this growth rate to roughly maintain into the next quarterly report and for the full fiscal year as well, as it has forecast next-gen security ARR growth of 31% to 32% for both of those periods.

3. Building a Compelling All-Around Platform

Climbing ARR for Cortex and Prisma is not only beneficial to Palo Alto's top-line performance, but it also helps to drive the company's ongoing shift toward becoming a unified, all-around security platform. When customers continue to subscribe to one or more of Palo Alto's products, they may be more likely to adopt other products as well—the platform thus becomes stickier and drives continued adoption and retention rates.

The firm is upgrading products and launching partnerships to further drive this multi-pronged approach. In July 2025, Palo Alto and identity and access management company Okta Inc. (NASDAQ: OKTA) announced an expansion of their ongoing partnership. Together, the companies will provide a unified security architecture based on AI, offering automated threat response, secure application access, and more. Partnerships like this are a win for Palo Alto because they both expand its service into new areas and provide heightened security for customers.

Keep an Eye on Valuation

While there are several compelling reasons for institutional and retail investors alike to consider investing in PANW, it's also worth keeping an eye on the company's valuation. With a price-to-earnings (P/E) ratio of 111.9, PANW significantly exceeds both the overall market average and the high-end tech sector average.

Despite substantial analyst support, PANW shares may also have limited upside potential in the short term based on a consensus price target of $209.16, just 5% above current levels. Still, it remains one of the most compelling cybersecurity firms in the second half of 2025.

Altucher: Turn $900 into $108,000 in just 12 months?

Altucher: Turn $900 into $108,000 in just 12 months?

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

No comments:

Post a Comment