| Five centuries ago, Shakespeare wrote these words for Brutus, who lived 2,000 years ago. His friend Julius Caesar had brought down the Roman Republic; Brutus decided that he had gone too far, and then found he couldn't control the response. It's startling how relevant Brutus' words now seem: There is a tide in the affairs of men

Which, taken at the flood, leads on to fortune;

Omitted, all the voyage of their life

Is bound in shallows and in miseries.

On such a full sea are we now afloat;

And we must take the current when it serves,

Or lose our ventures.

As the first quarter of 2025, and the first 10 weeks of the second Trump administration, come to an end, these words are as good a guide to markets — which sold off aggressively again last week and started Monday with a juddering 4% fall for Japanese stocks — as any. Noise isn't abating. We now know that President Donald Trump is considering oil sanctions on Russia; that he thinks he can run for a third term; that he "couldn't care less" if tariffs mean higher imported car prices; and that a big block of new tariffs will be announced Wednesday, Liberation Day. It's hard to know which way to look. Here's a guide to what we've learned so far, what we know, and what we still need to ask. - The Fault Is Not in Our Stars… But in Ourselves

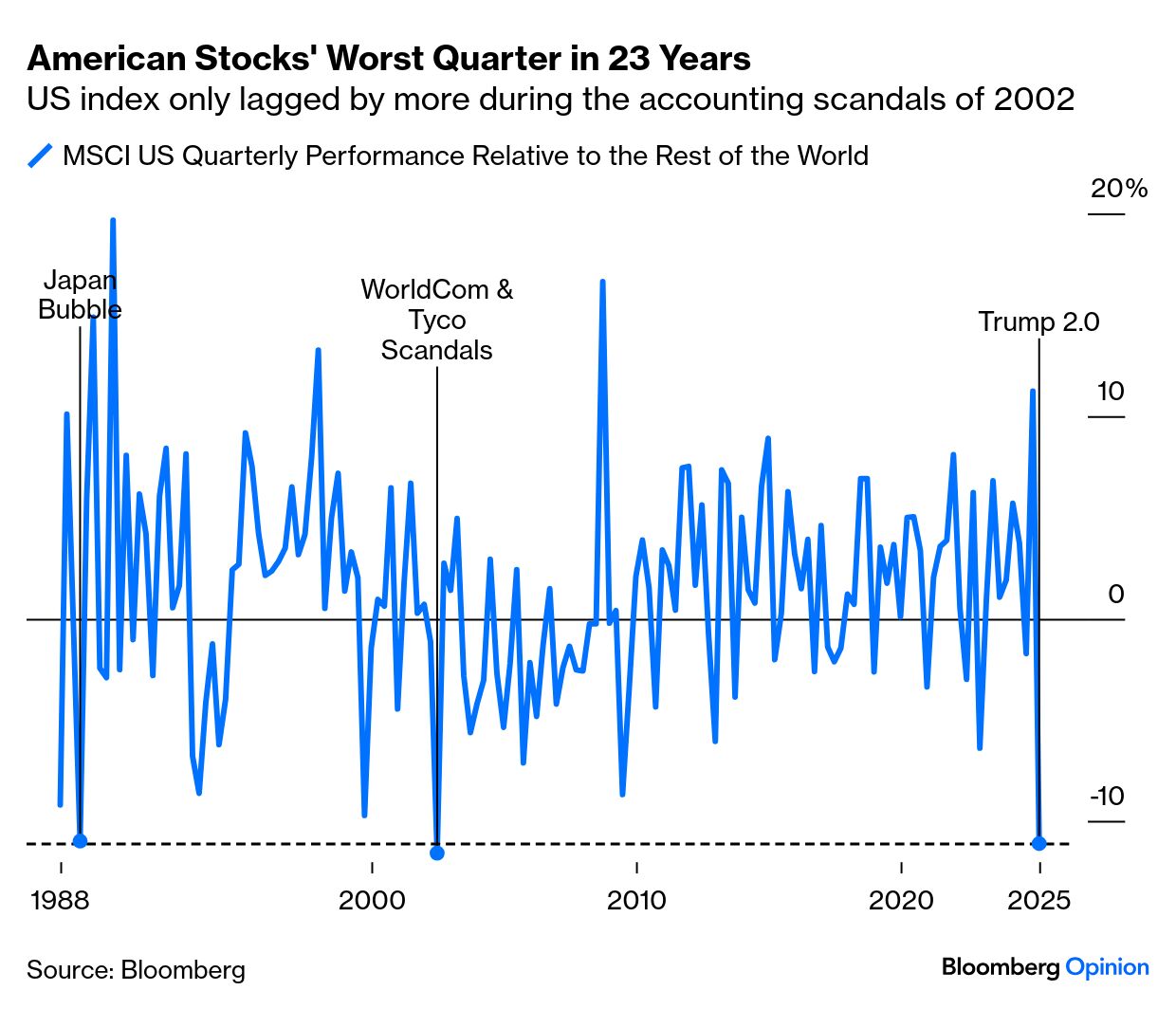

Or, the post-election rally is over. Relative to MSCI's index for all world stock markets outside the US, the MSCI US index — to all intents and purposes identical to the S&P 500 — is on course for its worst quarter since at least 23 years. The tide is flooding — in the wrong direction. A bad Monday would make it the worst quarter for the US since the index's inception. Only the second quarter of 2002, which produced the shocking corporate governance scandals at WorldCom and Tyco, saw the US lag the rest of the world by more. This is an epic change of judgment on where the US will go from here. It would be absurd not to attribute this in large part to Trump: - As Constant as the North Star

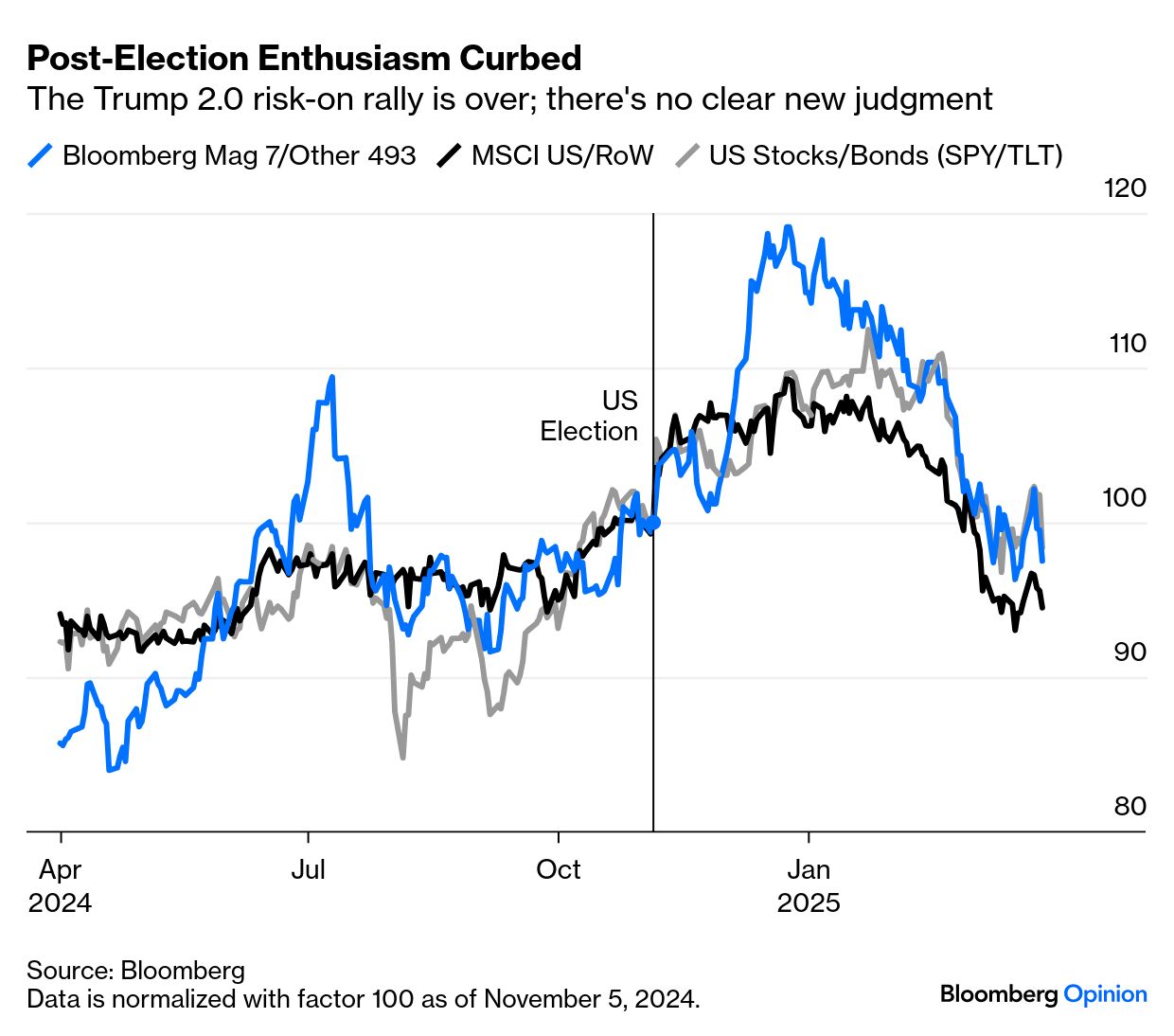

Or, no new trend has replaced US exceptionalism. Note that all the worst quarters for the US above were followed by periods of outperformance. We can't extrapolate the massive shift in sentiment that we've just witnessed into the future. Breaking the risk-on "Trump Trade" into three of its key elements — US stocks relative to the rest of the world, the Magnificent Seven stocks relative to everyone else in the US, and US stocks versus Treasuries — all are only slightly lower than they were on Election Day. This is a big shift, but it's done little more than cancel out a prior shift in the opposite direction. On such a full sea we're now afloat: - What Means This Shouting?

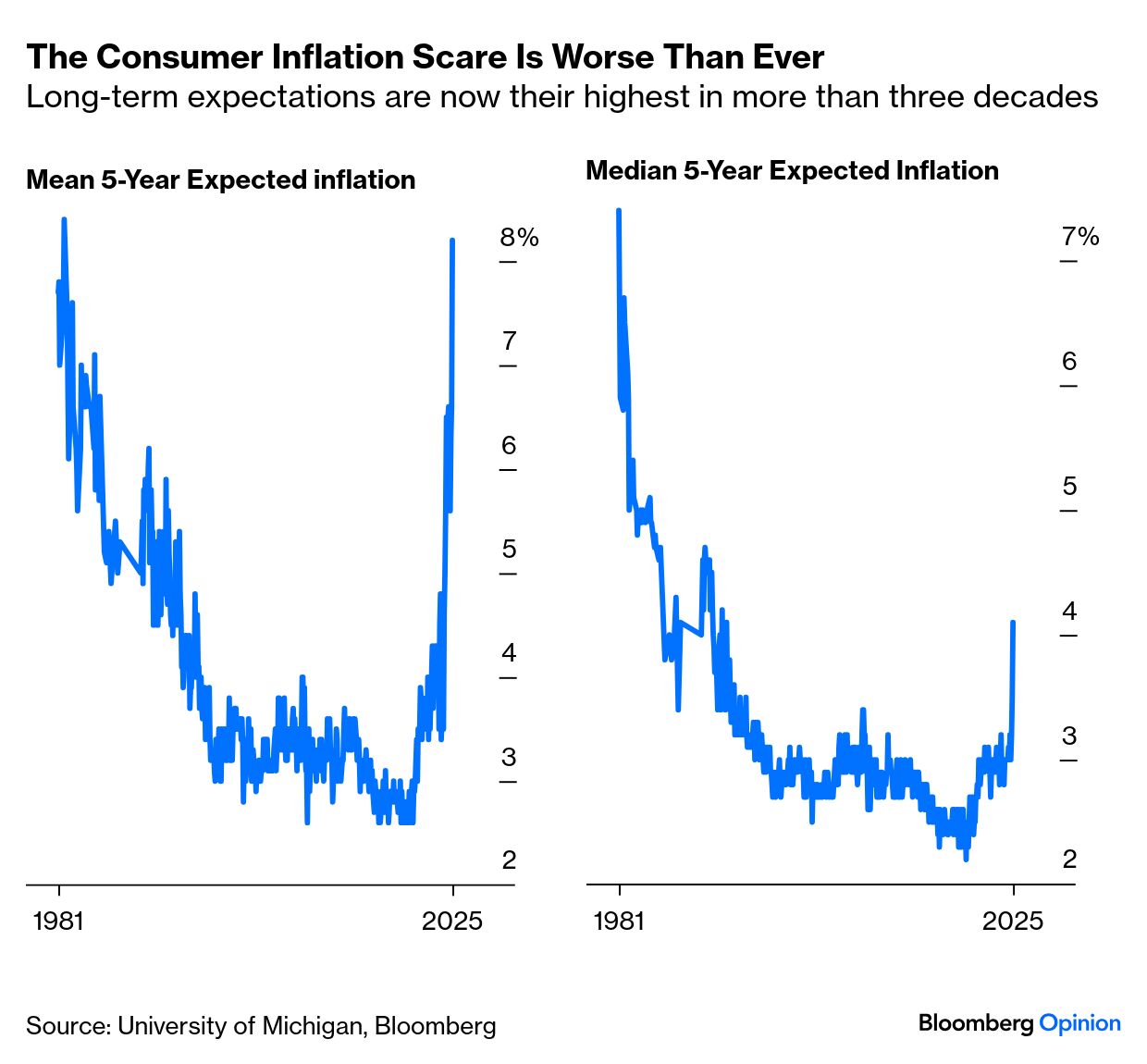

Or, 'soft' survey data have tanked, but hard data aren't so clear. George Soros' concept of reflexivity holds that in markets and the economy, perceptions can change reality. That means the spectacular shift in consumer sentiment needs to be treated with respect. Consumers in the US are braced for a return to serious inflation. They're more convinced of this than at any time in four decades, even though the average self-identified Republican still expects inflation to tick down to zero:  Bracing for 8% inflation is on the face of it irrational. Many things need to go wrong before we get back to levels like that. But Soros' dictum suggests we should take it seriously. Also, the bond market is also growing more concerned that inflation is coming back. Breakevens imply that inflation will top 3% over the next two years. Forecasts are their highest since a brief spike around the Silicon Valley Bank crisis two years ago. The inflation narrative is falling out of control, and could be self-fulfilling: - What a Terrible Era in Which Idiots Govern the Blind

Or, the real sea change has been in US foreign policy. Many elements of the Trump 2.0 agenda were well-signposted. But the extent of the US shift on foreign policy, siding with Russia in a United Nations vote on Ukraine, threatening the annexation of Canada and Greenland, and pouring scorn on the European Union, took most everyone by surprise. Forceful moves to get NATO allies to spend more on defense were expected; rhetoric so aggressive that those allies are rearming on the assumption that the US is no longer an ally is something very different. That has already triggered a remarkable shift in German fiscal policy — a rare example of a time when mere words (most significantly in Vice President JD Vance's speech in Munich and then the humiliation of Ukraine's President Volodymyr Zelenskiy in the Oval Office) have had instant massive economic effects.  Brutus by Michelangelo, circa 1540. Source: Mondadori Portfolio/Hulton Fine Art Collection/Getty This is a deliberate move away from an international order that has served the US well. When world hegemonic powers withdraw, they generally do so because they have no choice (such as Ancient Rome, or Britain a century ago). Their economies suffer greatly as a result. If people no longer trust the US, they won't continue the inflows of investment that have kept the stock market high and inflation and interest rates low. The questions for the next quarter concern how far the break in US foreign policy will go. If Trump turns against Putin, as now seems possible, then assumptions will change again. And Wednesday's tariff announcement should reveal much more about how far the administration will go. In particular, if it attempts to levy different rates according to how friendly a nation has been, or retaliates against value-added taxes, or launches more blanket tariffs on sectors, then sentiment will worsen. As reciprocal tariffs in themselves would be quite a retreat from earlier Trump positions (as the US doesn't in truth receive such unequal treatment), it's also possible that Liberation Day could start a retreat back toward the current world order.  Marlon Brando's Marc Antony becomes leader of the opposition. Source: 'Julius Caesar' (MGM 1953) Sunset Boulevard/Corbis Historical/Getty As it was for Brutus, the response is also critical. After Caesar's assassination, opposition to Brutus and his followers soon grew overwhelming. Will this prove to be just a momentary spasm of disgust at perceived American arrogance, or something deeper? Canada's election next month looks particularly interesting. The incumbent Liberals have roared back into contention on the back of Canadian anger at US behavior. But the polls are tight. If the conservative leader Pierre Poilievre wins, the current international anti-Trump anger might begin to look like more of a passing phase. There's game theory to be done on what happens next. But the reason the tide has turned is that deep assumptions about the international order have been challenged. Until there is some clarity on the scale of the breach between the US and its allies, it will be hard for risk assets to gain any new positive momentum. The best course is to follow Brutus (not that his own fate is encouraging) and take the current when it serves. |

No comments:

Post a Comment