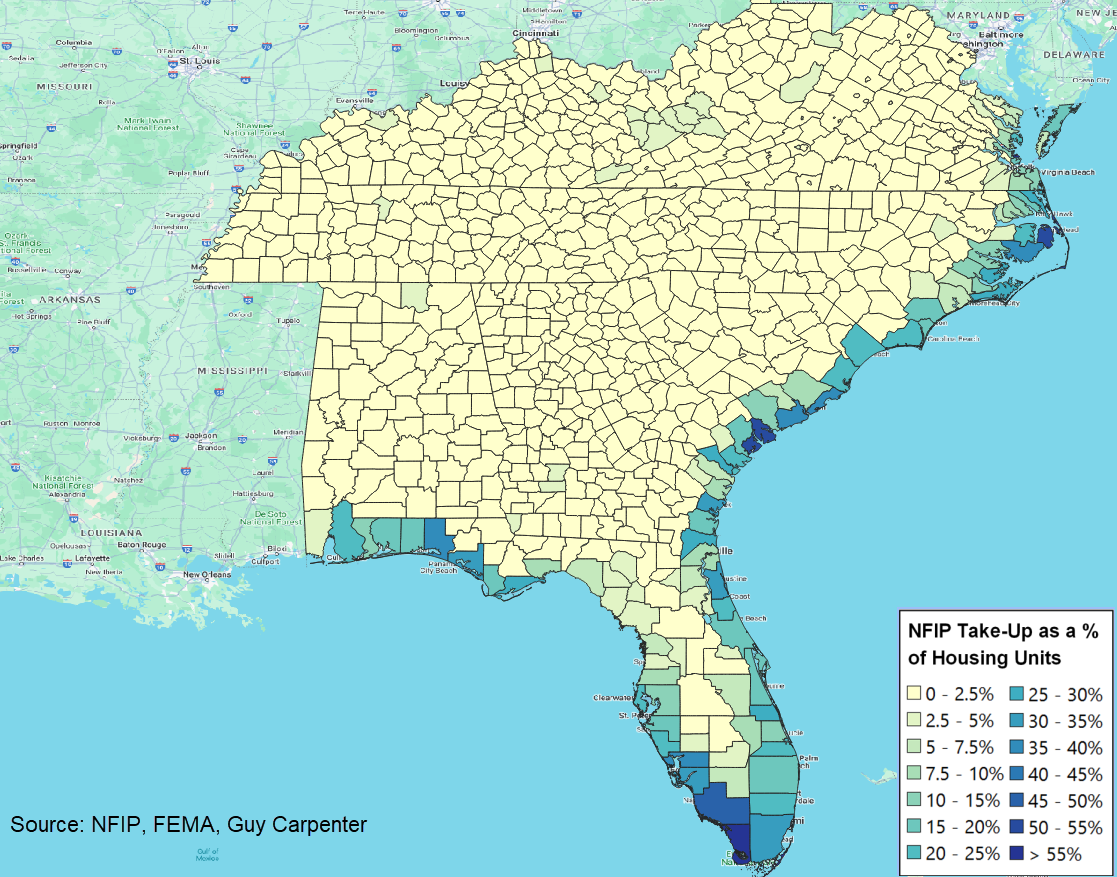

| By Leslie Kaufman and Brian K Sullivan On Thursday night Helene crashed into Florida's coast as a Category 4 hurricane. The giant storm with 140-mile-per-hour winds made landfall close to where Hurricane Debby hit in August, and where Idalia struck just over a year ago. It quickly made its way inland, knocking out power for millions. Even before that, it started dumping rain — 12, 15, 29 inches. The disaster underscores Americans' dangerously low levels of flood insurance coverage, especially away from coastal areas. Massive flooding is being reported across the South and into Appalachia, with footage of towns from Florida to North Carolina underwater. "This will be one of the most significant weather events to happen in western portions of our area," a weather service in western North Carolina said.  Floodwaters near Steinhatchee, Florida, on Sept. 27. Photographer: Sean Rayford/Getty Images North America Chuck Watson, a disaster modeler at Enki Research, estimates Helene will cause $25 billion to $30 billion in physical damage and losses, the majority of which won't be covered by insurance. "The ratio of insured to uninsured has been dropping" among US homeowners, he said, "and a lot of that is due to floods not being covered by the private sector." Roughly 4% of Americans have flood insurance, according to the Federal Emergency Management Agency (FEMA), with most policies issued under the government's National Flood Insurance Program. The rate in no way matches the risk posed by more frequent extreme rainfall events. This shortfall, which has been documented for years, is caused by two main factors: Many people are unaware that regular home insurance usually does not cover floods, or that they live in a flood-risk area where this extra purchase would protect them. Homeowners who live within FEMA-designated flood zones are required to buy flood insurance if they have a mortgage. However, FEMA has mapped only one-third of America's floodplains, according to the Association of State Floodplain Managers. Moreover, most FEMA maps don't consider pluvial flooding, or flooding from rain. That's likely one reason why flood-insurance takeup away from the coasts is negligible.  Flood-insurance coverage is much lower in inland areas. Guy Carpenter Then there are cost issues: Some Americans who had flood insurance previously are now giving it up because of rising insurance prices. Homeowner insurance rates in the seven states in Helene's path — Florida, Georgia, South Carolina, North Carolina, Kentucky, Tennessee and Virginia — went up by an average of more than 27% from 2018 to 2023, according to S&P Global Intelligence. The price hikes have also been steep for flood insurance, leading some people to drop their policies. Doing so is a big gamble: Flooding is the most damaging of all perils. It has cost US taxpayers more than $850 billion since 2000 and is responsible for two-thirds of the costs from all natural disasters, says Flood Defenders, a nonprofit flood insurance advocacy organization. FEMA estimates that a single inch of floodwater in a home can cause $25,000 in damage. Un- and under-insured homeowners typically believe they will be able to rely on help from the federal government, but FEMA provides very limited help to individuals without federal flood insurance, and even that safety net is fraying. FEMA faces a financial crisis as disasters mount, and Congress failed to replenish the federal funds used for storm aid in a government funding bill that passed this week. Read and share a full version of this story on Bloomberg.com. By Lauren Rosenthal Hurricane Helene may be post-hurricane now, with winds dipping from a peak of 140 mph (225 kph) to less than a third of that. But flooding remains a major threat, in part because Helene started dumping historic rainfall across parts of the Southeast US a day before it touched land. The storm was steered north across the Gulf of Mexico by a dip in the jet stream known as an upper-level trough. That same atmospheric feature channeled moisture northward well ahead of landfall, dumping up to a foot of rain over the Carolinas and southern Appalachian Mountains on Wednesday and triggering flash floods.  A car is submerged in Atlanta floodwaters in the aftermath of Hurricane Helene on Sept. 27. Photographer: Megan Varner/Getty Images North America "If you're washing dishes and you've got a really saturated sponge, at some point the sponge can't take any more water," said Peter Mullinax, a meteorologist at the US Weather Prediction Center in College Park, Maryland. "The ground is similar. As Helene moves inland, that's why there's such a significant threat for power outages and downed trees, which are loose in the ground. There's a higher risk of damage." It's not uncommon for a hurricane to generate rainfall over land while still churning across the ocean, said Justin Lane, a meteorologist for the National Weather Service's Greenville-Spartanburg office in North Carolina. But most storms don't unleash as much early rainfall as Helene. "We call these predecessor rainfall events," Lane said. "Maybe you see two to four inches of rain. You usually don't see six to 12 inches, and that is really what made this event in particular so bad." Read and share a full version of this story on Bloomberg.com. For unlimited access to climate and energy news and original data and graphics reporting, please subscribe. |

No comments:

Post a Comment