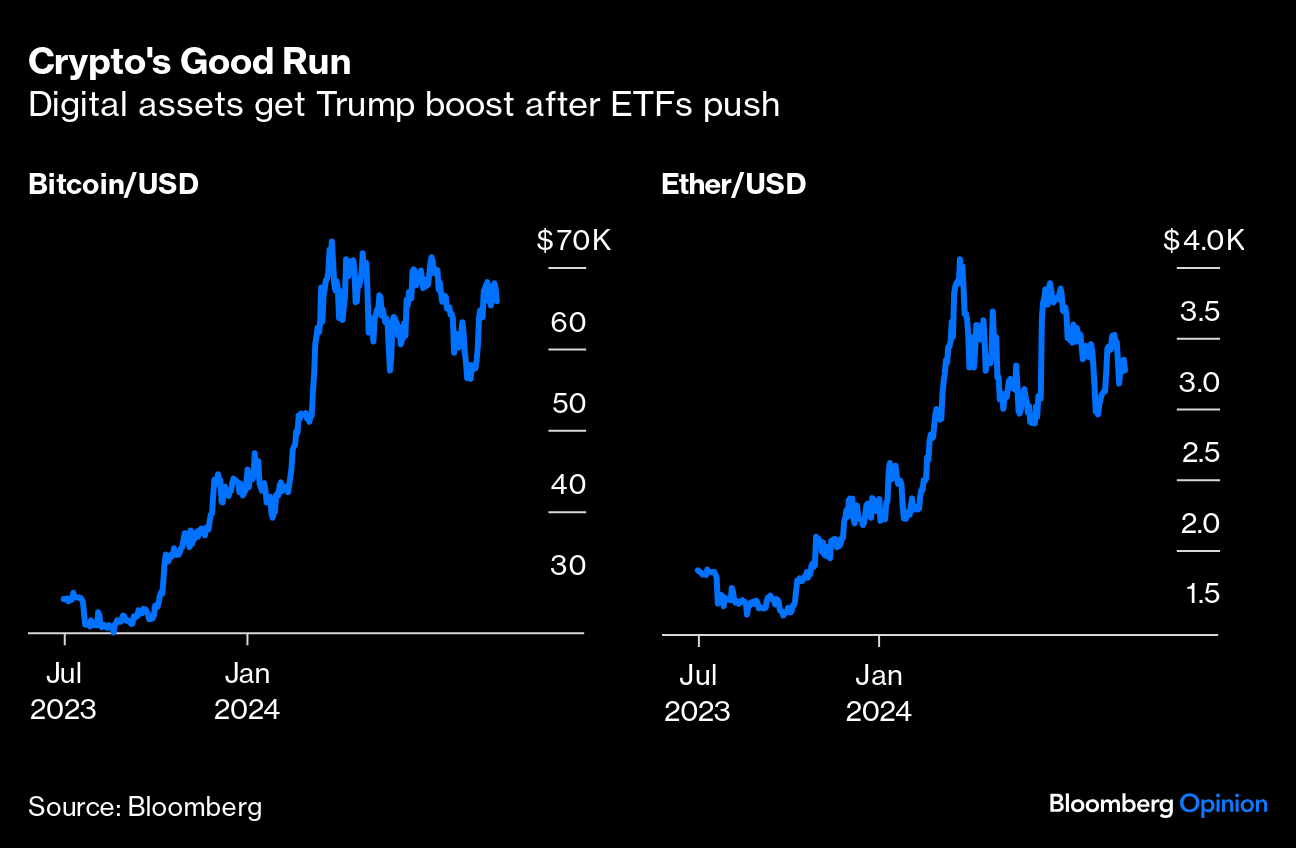

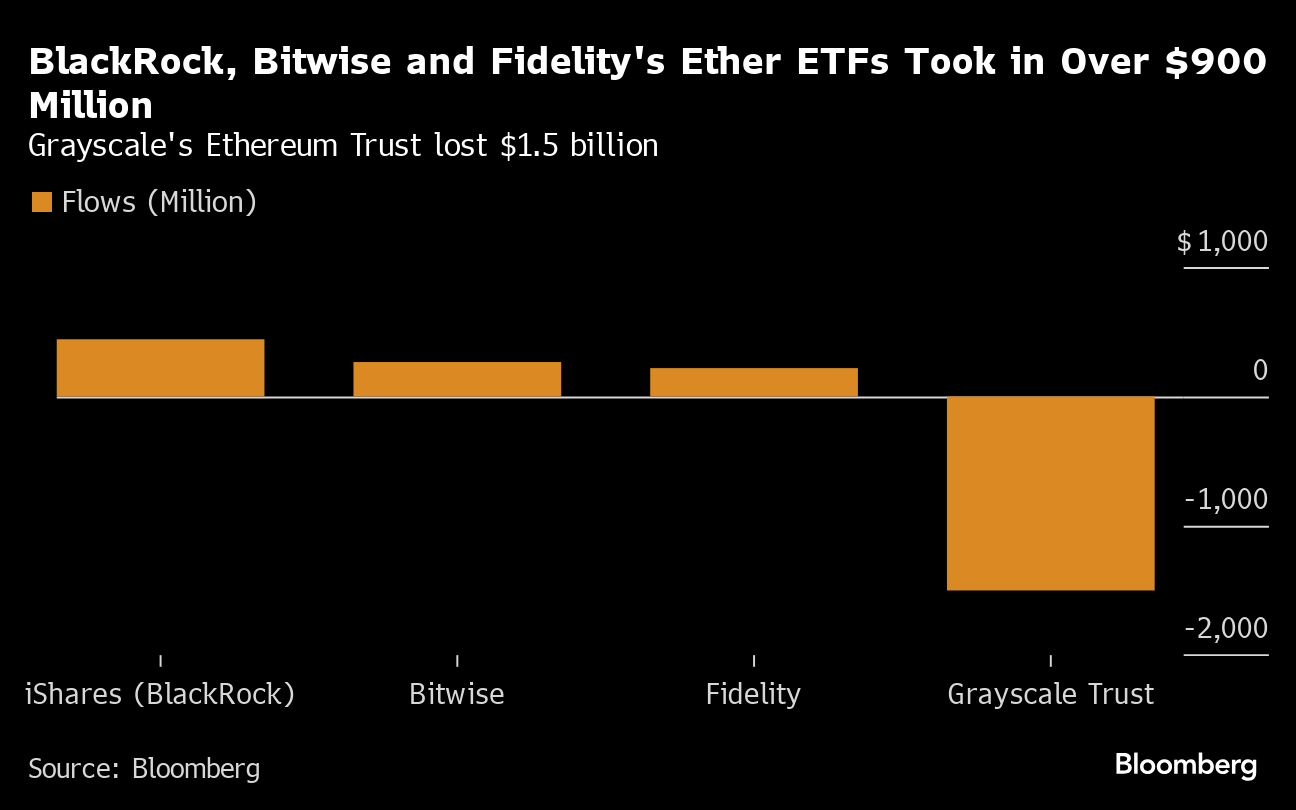

| There's a bull market for cryptocurrency promoters. Donald Trump's endorsement of Bitcoin is only the latest win for the digital asset. As Bloomberg News' reporters note in this Big Take, his backing capped a complete about-face on an asset class he considered a crime-riddled scam when in office. There may also be a reversal from crypto bros now happy to back him. Their original libertarian concept was that the currency would break the hold of banks on the financial system, and of the government over the currency. The notion of benign anarchy had already seemed to be dying; official embrace now could bury it once and for all. Trump's support drove a Monday rally that brought Bitcoin close to the $70,000 mark for the first time since mid-June. It's regained some of the momentum provided by the launch of exchange-traded funds back in January, and is still up by more than 50% this year. Ethereum, since last week also available in ETF format, is up by more than 39%: Beneath Ether's rosy performance, its ETFs saw outflows of nearly $350 million. The eight that came into existence last week had taken in a net $1.17 billion in the first four trading days ended July 26, according to Bloomberg data, but that was more than counterbalanced by the money that came out of the pre-existing Grayscale Trust: While Trump's courtship with cryptocurrency may seem sudden, he had long embraced non-fungible tokens or NFTs — and even sold some of his own. Regarding motives, the presidential elections suddenly looks more open after Joe Biden's withdrawal, making it illogical for Trump to alienate any group (such as crypto bros) that's already courting his attention and could offer a lot of financial support. But there's a big issue for crypto enthusiasts here. They long for a currency outside the control of central banks or the state. Therefore, an endorsement from a potential US president must raise the question of whether this is a bona fide marriage or one at variance to the tenets of libertarianism. Rather than strengthening Bitcoin, might not a big government stake instead subvert it? China's purchase of huge quantities of Treasuries was widely seen as affecting the US credit market and compromising US independence; wouldn't the same arguments apply to a government stake in Bitcoin? If the government became a big holder, it would inevitably gain great influence over the price. To prove the point, Bitcoin fell Tuesday after a report that the government intends to dispose of the crypto stockpile built up through confiscation from criminals. A strategic Bitcoin reserve, however, would be much more ambitious. Trump says that he favors this, while Wyoming Republican Senator Cynthia Lummis is planning a bill establishing one. Her idea is that bolstering the dollar with a digital hard asset will "secure our nation's standing as the global financial leader for decades to come." This strategic Bitcoin reserve "would be required to hold onto the Bitcoin for 20 years," and could only be used during that time period to pay down the national debt. Rather than replace the dollar, then, it appears Bitcoin is now intended rescue it. Under Lummis's proposal, the US would buy approximately 5% of the total Bitcoin supply — about $68 billion at current prices — over a period of time. That sounds like the government taking a degree of control. However, Stephane Ouellette, CEO and co-founder of Frnt Financial, believes the proposal strongly supports a more libertarian financial system: If the US began shifting its interest toward self-custodied cash, the concept of a central bank would drastically change, if it remained an idea at all. Governments would see their ability to censor political opponents drastically decrease, and we'd simply be entering a paradigm with an asset that is much more free-market oriented at its center. This was in effect the plan. "Hyper-Bitcoinization," which is the final boss of Bitcoin adoption, sees it at the center of the global financial system, which necessitates moments like these and figures like Trump shifting their viewpoint.

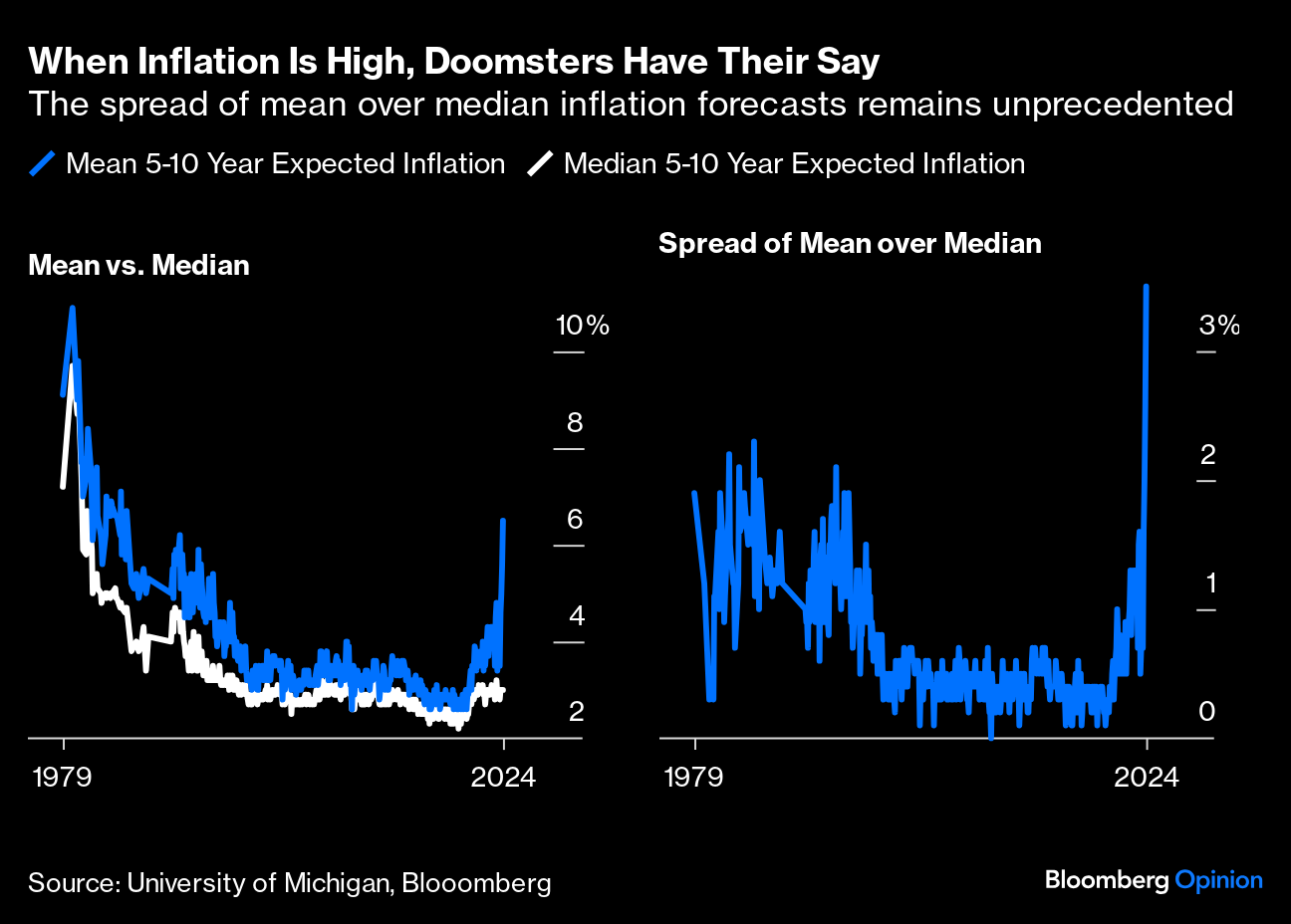

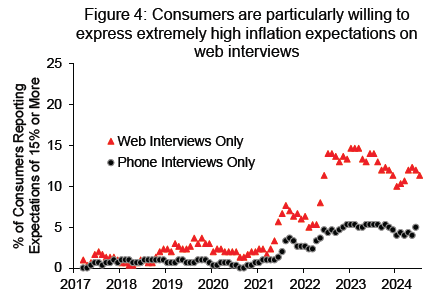

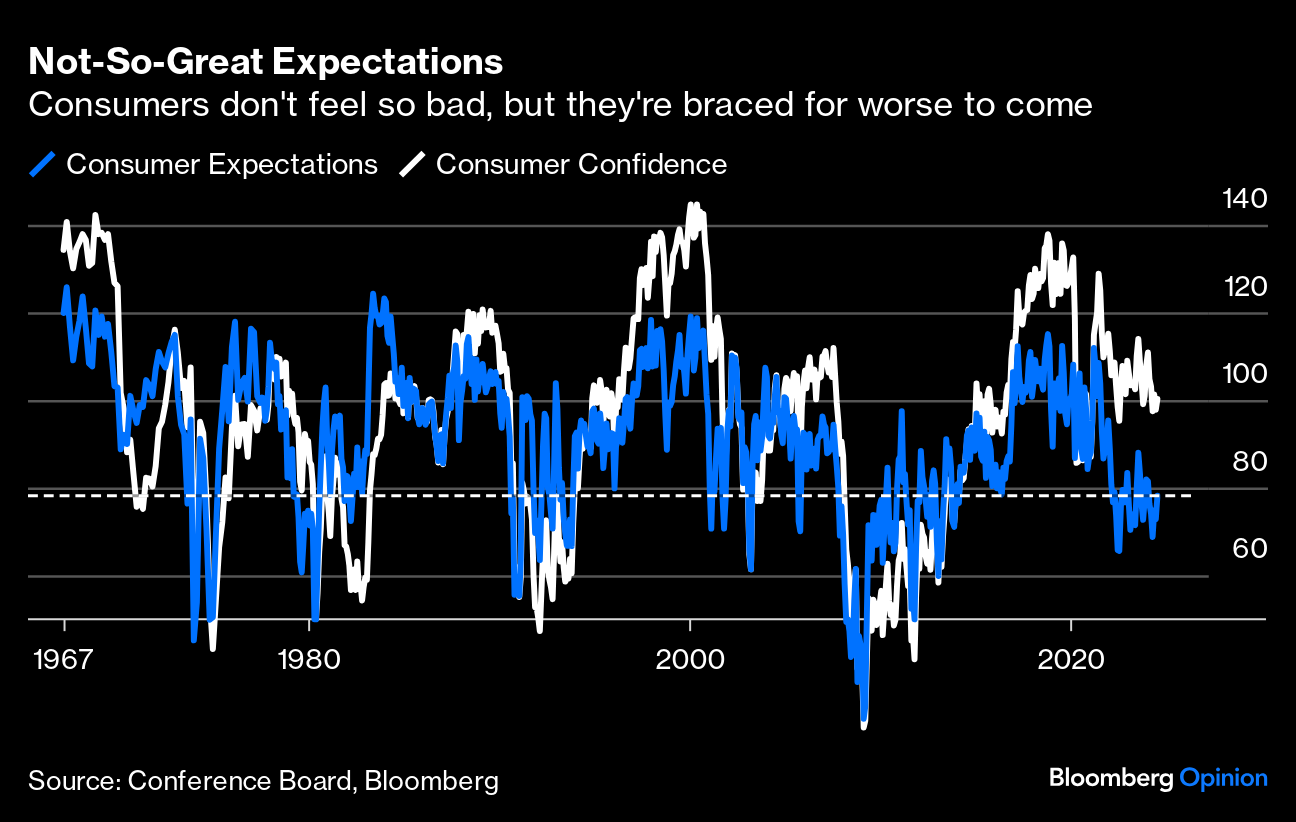

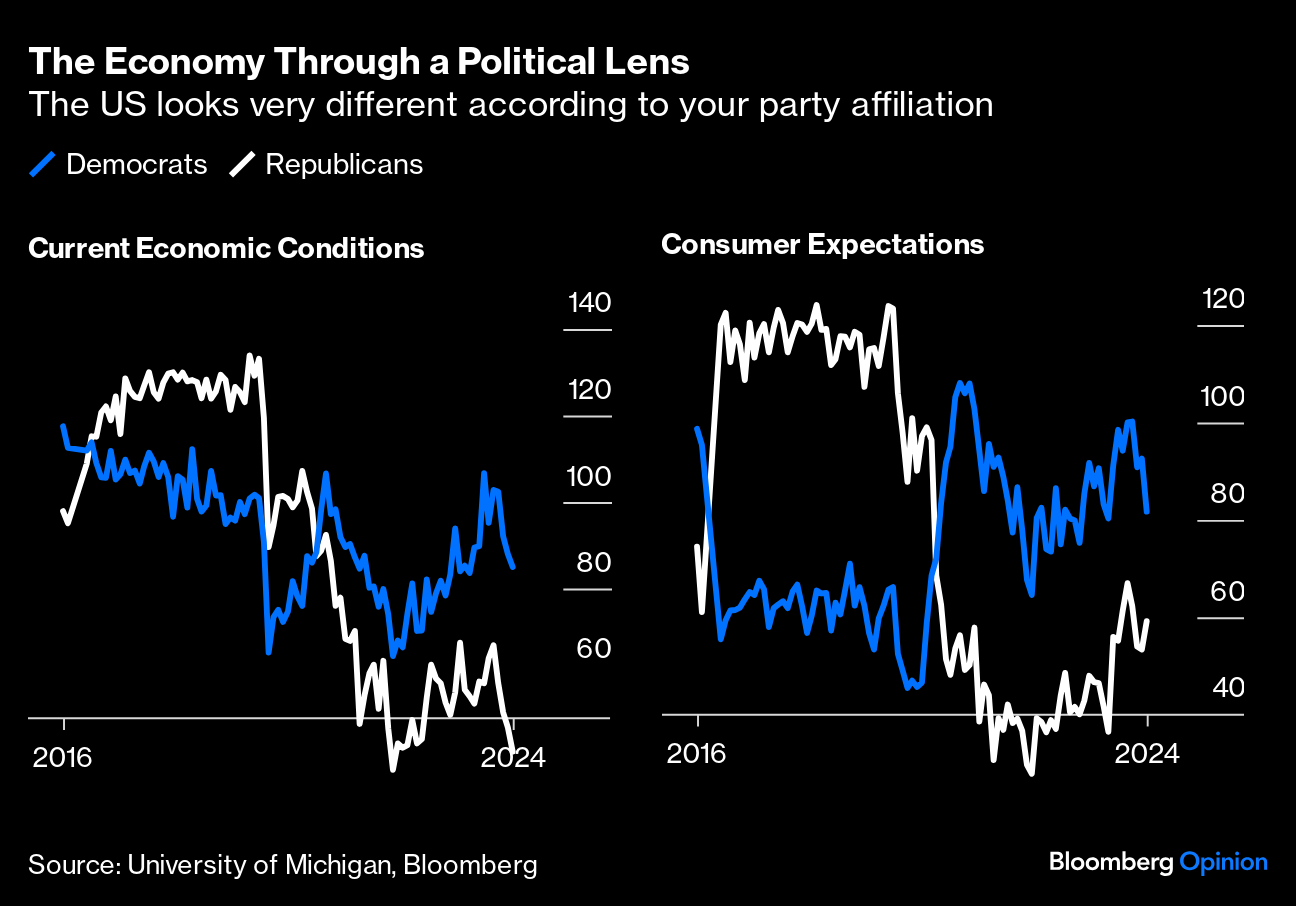

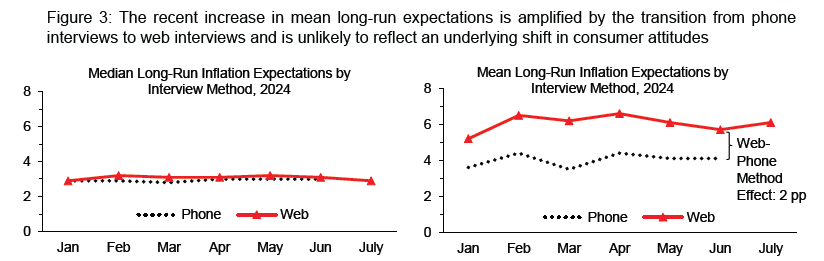

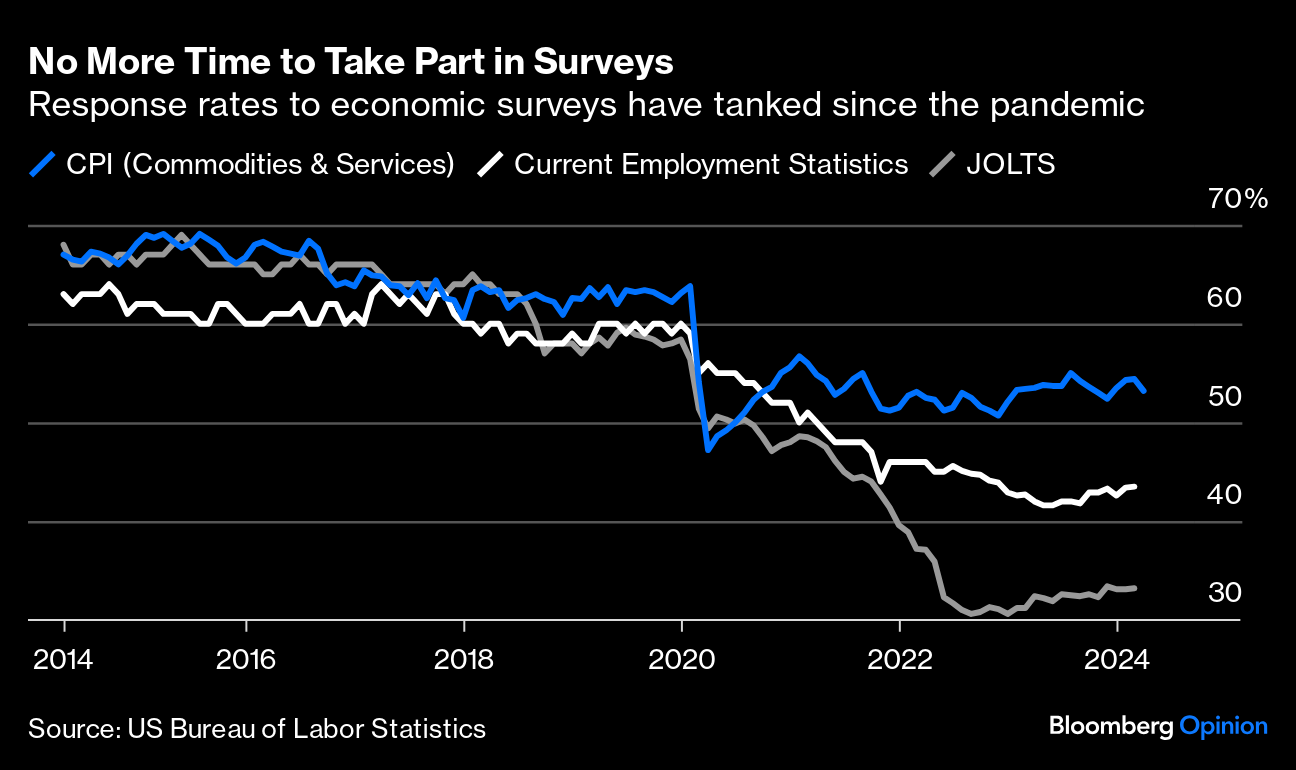

Lummis argues that the reserve would "supercharge" the dollar and bolster the US economy. On that basis, Trump's love for Bitcoin is hard to reconcile with his oft-stated preference for a weak currency that helps US exporters. And Bitcoin can, of course, like all risky investments, go down as well as up. A detailed version of the bill might provide more clarity. Undeniably, a nascent asset like Bitcoin could benefit from additional legitimacy through increased government holdings. Those who already hold Bitcoin or run crypto-related businesses would also stand to make a lot of money from taxpayers' largesse. It's understandable that the news has boosted the price — but whether the idea is a win-win for Trump remains to be seen. His immediate task is to get past a surging Kamala Harris. — Richard Abbey We live in data-dependent times. It would therefore be helpful if the data were reliable. It's not clear that they are. The old computer maxim of "Garbage In, Garbage Out" could apply — input poor data and you'll get a bad result. The latest download gives some classic examples. US consumer confidence, as measured by the Conference Board in a survey that has been running since the days of Lyndon Johnson, is bang in the middle of its range, but expectations for the future are as low as they've been outside of recessions in the entire history of the survey: Note also that the spread of confidence over expectations has been high and persistent ever since the the pandemic's first stage began winding down at the end of 2020. Expectations have real-world consequences; they can make people bring forward purchases or delay them, and inspire either risk-taking or extreme caution. So this does matter. Since 2016, the other most closely watched survey of consumer expectations, run by the University of Michigan, has tabulated its results by respondents' partisan identification. As politics grows more polarized, it's not surprising that the gap between Democrats and Republicans is widening. What is very surprising is the extent, and the way entire perceptions can move on the results of one election: Both Republicans and Democrats perceive the economy in real-time to be weakening, but the former perceive it as far worse. Expectations similarly seem much rosier for the latter — although it's fascinating that Democrats are suddenly much less optimistic. That might well be because of Trump's strong polling numbers at the time the survey was conducted. Whatever the explanation, political polarization appears to be moving consumer sentiment data in ways that aren't predictable. That brings us to a critical element in perceptions of the economy — expectations for inflation. There's a big debate among economists over how much they can drive future price rises. Predictably, Republicans at present tend to expect higher inflation than Democrats. The gap isn't that wide, however. Instead, the yawning divide in Michigan's inflation survey is between the median and the mean. The latter is far higher, and the spread is unprecedented:  Some of this can be explained by the level of inflation. When prices are rising fast, people are more likely to believe that extremes lie ahead. The mean was also well above the median in the early 1980s. But it wasn't as far ahead as it is now, and in any case inflation is currently falling. So what is going on? Joanne Hsu, a director of the Michigan survey, has published some fascinating research that suggests that inflation expectations may not be running amok as the data show — but also that in the internet age, all survey data is less trustworthy. Michigan reaches an increasing proportion of its surveyees over the web. The median results online and by phone were virtually identical; the mean for online interviews has been about two percentage points higher than for the phone: Further, when looking at the proportion prepared to predict inflation of 15% or more over the last seven years, we find that in both formats extreme predictions like this rose after the pandemic — but went ballistic in web interviews in a way that wasn't matched over the phone:  So, if addressed over the internet, we are far more likely to offer an "out there" opinion than by phone. This isn't surprising, but it's alarming that the effect is so great and so easy to quantify. For now, the good news is that the data aren't as frightening as they look. Hsu explains that web interviews were phased in over a four-month period starting in April, so that about two percentage points of the rise in the mean from 3.5% in March to 6.1% in July, when all interviews were conducted via web, can be attributed to that shift. As such, she says, "The recent increase in published mean inflation expectations is unlikely to reflect a substantive shift in consumer attitudes." The bad news is that data gathered in the impersonal domain of the internet is likely to be contaminated by the same id instinct that takes over people on social media. Another problem goes beyond exaggeration — people simply don't reply at all. These are some of the key numbers from the latest JOLTS (Job Openings and Labor Turnover Survey) produced by the Bureau of Labor Statistics. The rate at which people are leaving jobs is falling, as is the rate at which they're being hired. That suggests a labor market steadily returning to normal after Covid-19: That's believable, but it's not clear that we can put much faith in it because response rates, already declining before the pandemic, have collapsed since. For the JOLTS, response rates are barely above 30%, and numbers answering inflation and employment surveys have also dropped severely: The BLS explains what's going wrong in a lengthy research report. Again, the forced move away from the tried-and-tested method of talking to people on their landline is an issue. As we brace for more key economic survey data, and decisions by data-dependent central banks, bear in mind that if garbage goes in, garbage will come out. To help, you could provide some truthful answers to the latest MLIV Pulse survey on what the effects of an easing cycle could be. Please share your views here. And that leads to a survival tip… A tip few readers should need: Be careful of what you read online. Monday brought the horrible news that a teenage boy had broken into a Taylor Swift-themed party in the English town of Southport and stabbed three young girls to death and left another five in while hospital. It's savagely upsetting, and didn't stop there. Under British law, police cannot name criminal suspects under the age of 18. All we know about this perpetrator officially is that he's 17, lived in a nearby village, and was born in the Welsh capital city of Cardiff. But social media quickly flooded with reports naming him as Ali Al-Shakati, whose nationality was variously given as Syrian and Rwandan. Internet sleuths soon pointed out that "al shakati" shows up in translation engines as the Arabic for "to my apartment." The police took the unusual step of announcing that the name was wrong. For 24 hours, British social media reverberated with revulsion at Al-Shakati and Muslims in general. Many police were injured in a riot Tuesday night as protesters lit fires around Southport's mosque. Whatever motivated this obscene falsehood, it's no better than yelling fire in a crowded theater. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. More From Bloomberg Opinion: - Marcus Ashworth: Germany Versus Spain Poses a Problem for the ECB

- Lionel Laurent: Trump's Embrace of Bitcoin Is the Art of the Grift

- Liam Denning: The National Security Twist in an EV Maker's Graphite Deal

Want more Bloomberg Opinion? OPIN <GO>. Or you can subscribe to our daily newsletter. |

No comments:

Post a Comment