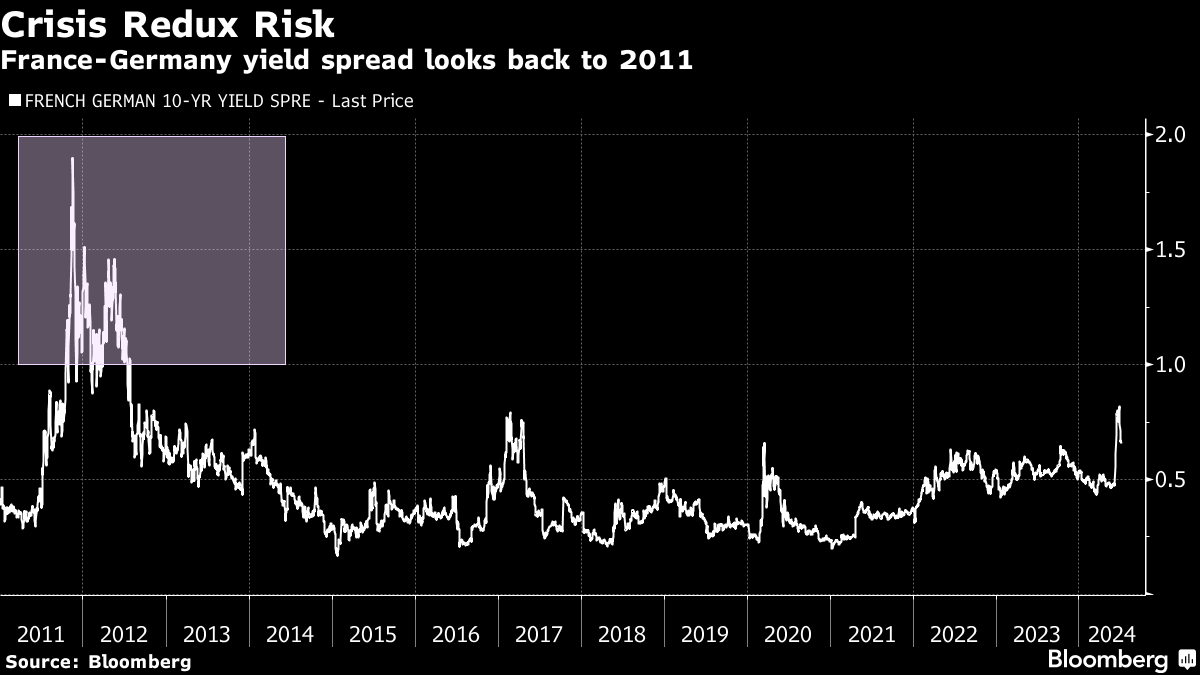

| France looks headed for a hung parliament with the nation already under scrutiny for having excessive deficit. This points to an extended period where the yield spread between French and German bonds widens. Investors will be looking back toward the European debt crisis from 2011 through 2012 for a sense of how dysfunctional French debt markets could become. Back then the France-Germany spread spent a prolonged period above 100 basis points, which could be an objective for aggressive traders in the months ahead. Meanwhile, French sovereign notes can't expect any assistance from US Treasuries, even though yields stateside appear to be on a downward trajectory. Federal Reserve Chair Jerome Powell is poised to fuel more demand for US fixed-income this week in what is set to be a dovish leaning appearance before lawmakers in Washington. Rather than support bonds in France, it is more likely to draw even more flows into Treasuries for the clarity of policy direction. In contrast, France is becoming a new headache for European leaders in Brussels as political gridlock sets in, which is negative for French bonds and equities. Long-term investors may find comfort that a full-blown European debt crisis looks less likely than the dark days when Greek angst undermined the region's markets. But with France entering a new era of political uncertainty, there is plenty of room for bond vigilantes to extract more pain from the France-Germany yield spread.

Mark Cranfield is a macro strategist for Bloomberg's Markets Live team, based in Singapore |

No comments:

Post a Comment