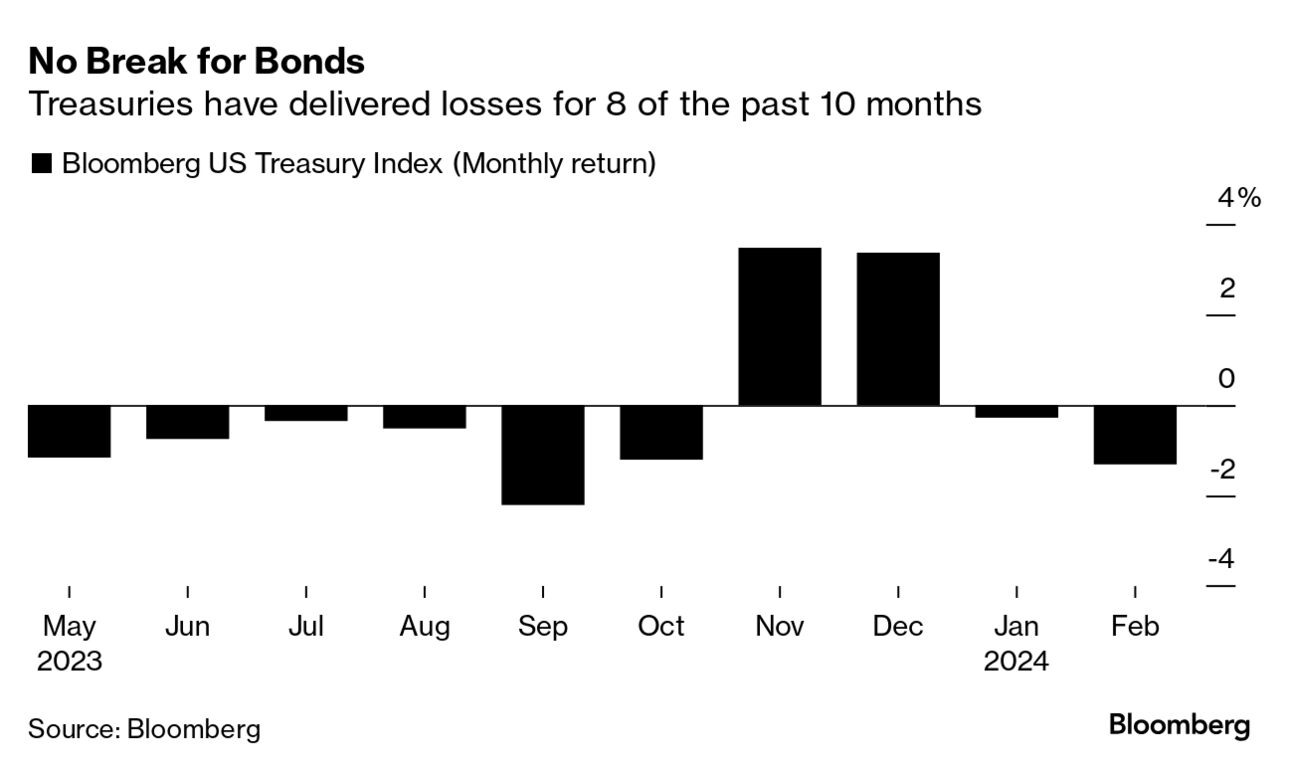

| Good morning. NYCB tumbles again, Dell heads for a record thanks to a boost from AI and Pimco warns bonds are heading back to the 1980s. Here's what's moving markets. — David Goodman Want to receive this newsletter in Spanish? Sign up to get the Five Things: Spanish Edition newsletter. Commercial real estate lender New York Community Bancorp is tumbling after saying it discovered "material weaknesses" in how it tracks loan risks, wrote down the value of companies acquired years ago and replaced its leadership to grapple with the turmoil. It's down more than 25% in premarket trading, after already falling 53% so far this year. Investors in regional banks have been on edge since, January when the company — a major lender to New York apartment landlords — said it is stockpiling cash to cover potential problems with loans. A wider index of regional lenders is down about 10% this year. Dell is moving in the other direction, with shares surging 21% in premarket trading and set for a record high. The jump comes after it reported better-than-expected sales and profit, fueled by demand for information technology equipment to handle artificial intelligence work. "We've just started to touch the AI opportunities ahead of us" Chief Operating Officer Jeff Clarke said. Pacific Investment Management Co. is warning that US fiscal largesse is at risk of dragging the Treasury market back to 1980s. In a paper this week, Pimco said a combination of stickier inflation and deteriorating budget estimates could see a return to the time when bond vigilantes demanded far higher compensation to own longer-dated bonds. There's a risk such dynamics "could start to reverse the 40-year downtrend" of term premium — a key measure of how much bond investors are compensated for holding long-term debt, the paper said. The lack of any nasty surprises in the US PCE data yesterday helped the S&P 500 notched its 14th record close this year, but the relief seems to be waning on Friday. US equity futures swung from gains to losses during the course of the European morning, while the Stoxx 600 pared an advance after data showed euro-zone inflation eased less than anticipated in February. Treasuries rose for a third session in a row, continuing a move that help net a payout of 20-to-1 for anyone who took heed of Citi's advice on Wednesday to put on a "quiet bull structure" options bet. The PCE data also allowed Fed officials to stick to a narrative of cautious optimism about rate cuts. Mary Daly yesterday said central bank officials are ready to lower interest rates as needed but emphasized there's no urgent need right now, while John Williams reiterated that he expects the central bank to cut rates later this year. Meanwhile Raphael Bostic said recent inflation readings indicate "there are going to be some bumps along the way" to target, and Austan Goolsbee cautioned against reading too much into a single month's inflation data. There's another deluge of Fed speakers due today, with at least seven officials slated to make remarks. The US also has manufacturing, construction and sentiment data ahead. This is what's caught our eye over the past 24 hours. When traders finally aligned with Federal Reserve on the outlook for interest-rate cuts in 2024, I expected wave of relief that would restart the rally in Treasuries. After all, while markets may have arguably overhyped their expectations for monetary policy easing, the direction of travel for rates remains the same — lower, which remains a positive for bonds… right? Not exactly. While Treasuries did enjoy a bit of an end-February rally, they also just delivered their biggest monthly decline since September and benchmark yields are holding near the highest levels in more than three months. So far, it hasn't shaken stocks, which continue to build on the euphoria induced by blowout Nvidia earnings last week. More broadly, S&P 500 companies are headed for their highest quarterly earnings beat rate since the fourth quarter of 2021, according to data compiled by Bloomberg Intelligence strategists Gina Martin Adams and Wendy Soong. Yet at some stage, yields that continue to march upwards — particularly on the back of growing expectations to remain higher for longer -- will have to bite for stocks. That will be especially true if more robust US data give credence to the idea that perhaps the economy doesn't need rate cuts -- or worse, maybe what it needs is rate hikes. As Jim Bianco of Bianco Research put it: "The old adage on Wall Street is that rates go up until something breaks."

Kristine Aquino is managing editor for Bloomberg Markets Today. Follow her on X at @krisaqnews. Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

No comments:

Post a Comment