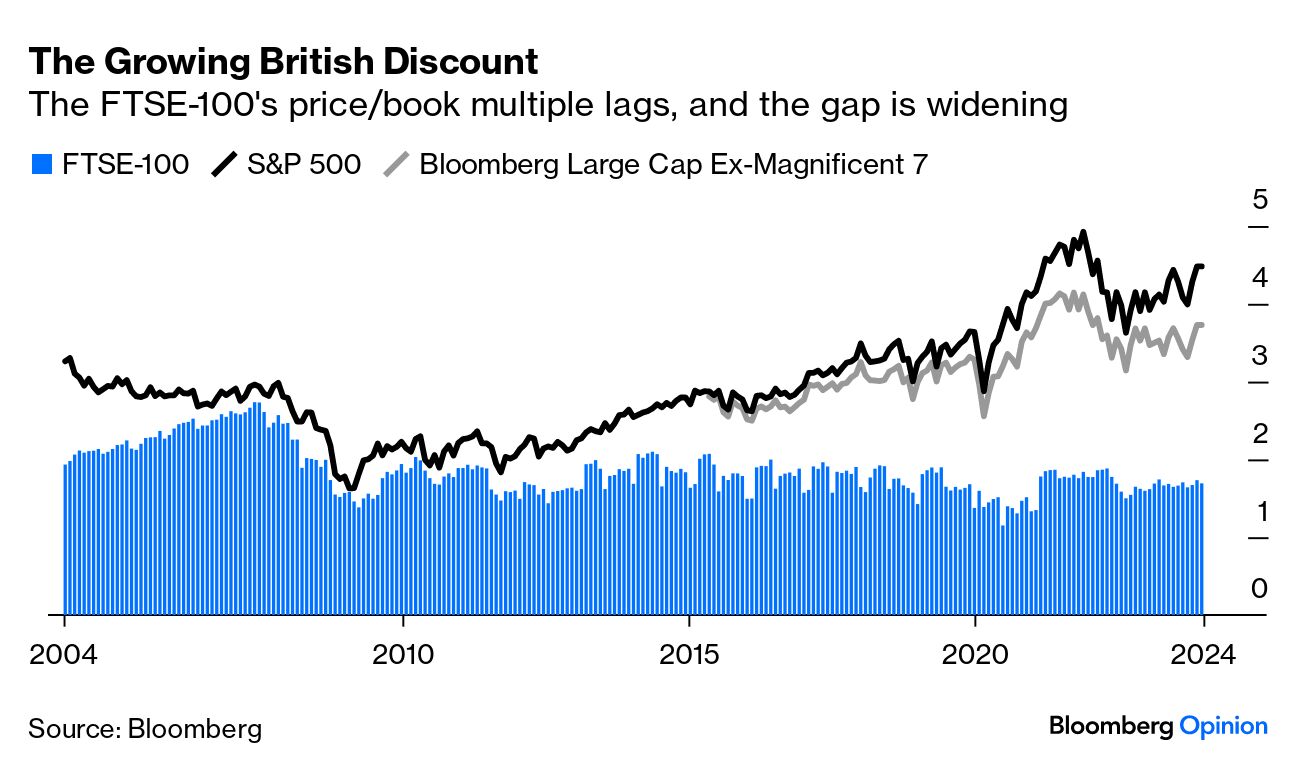

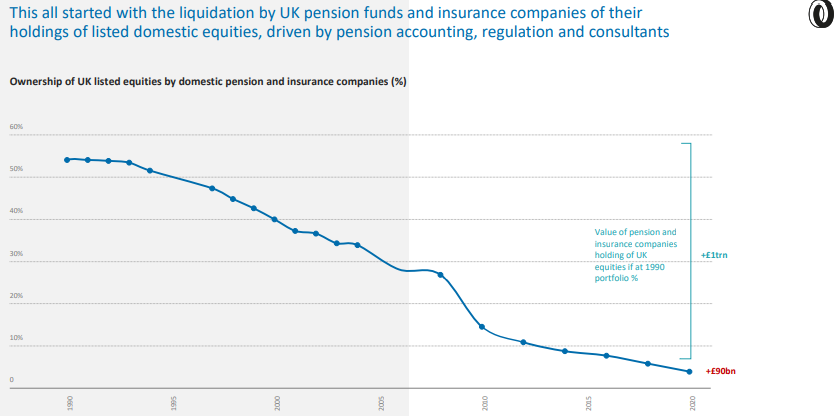

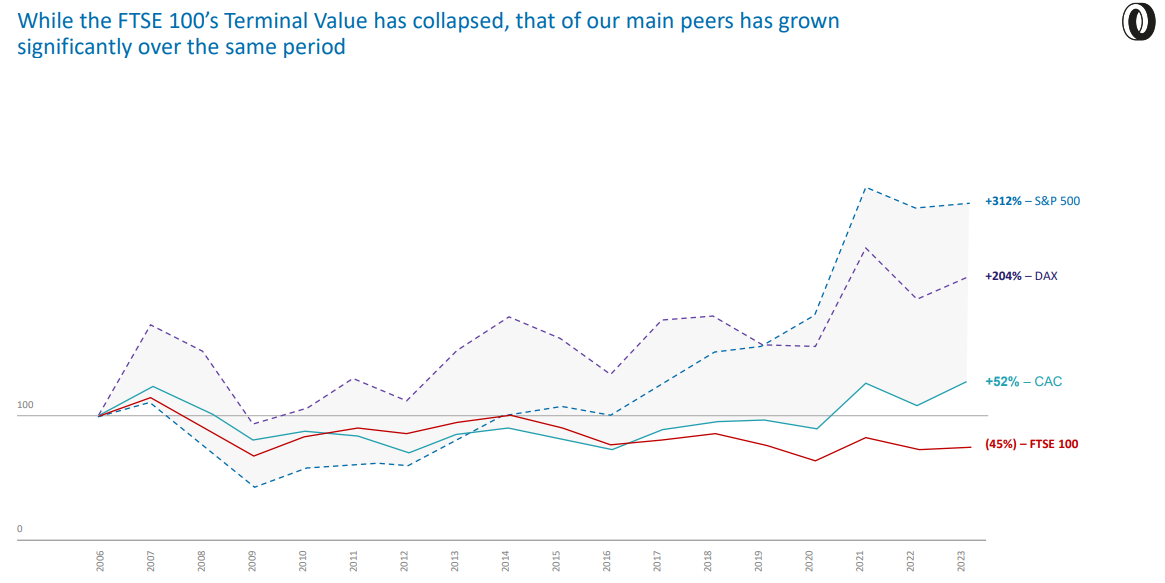

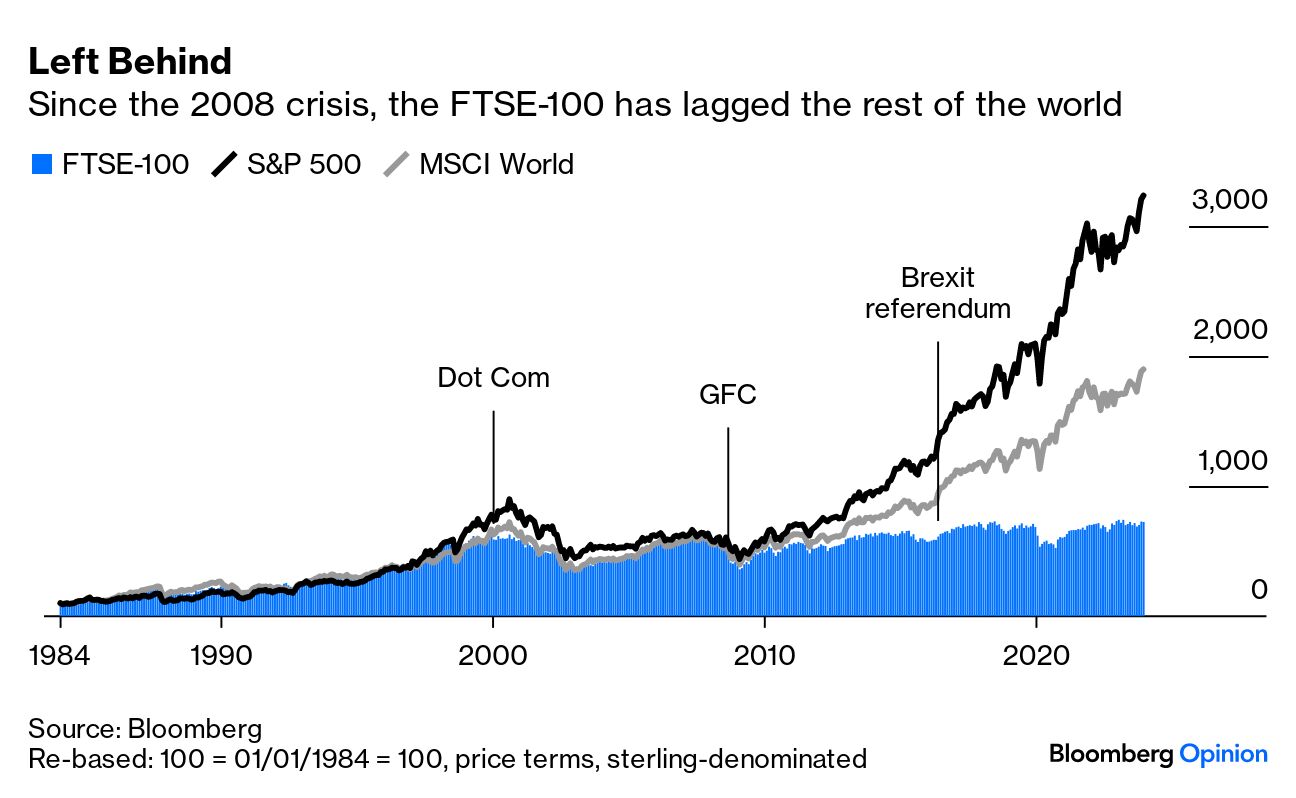

| London has an anniversary to celebrate. Jan. 3, 1984, saw the launch of the FTSE 100, and with it a big step forward in the way markets are traded and investments made. It has been the most closely followed index of the corporate UK ever since. Its arrival was one of many innovations that transformed the City of London in the 1980s. The performance over those 40 years, sadly, isn't much to celebrate. The following chart shows how the FTSE 100 has done in the 40 years since inception, compared to the S&P 500 in the US (its most obvious counterpart) and the MSCI World index of developed markets: The trajectory has been acutely disappointing from a British perspective. But the excruciating lag is a recent development, dating from about three years after the 2008 Global Financial Crisis. The gap widened significantly after the Brexit referendum in 2016, but it would be too simple to blame everything on leaving the European Union; the FTSE had been trailing badly for several years at that point. Some of this is because the most-elevated valuations these days are in high tech, a sector that's barely represented at all among UK-listed stocks. The likes of Apple Corp. and Nvidia Corp. should plainly aid the S&P 500. But a look at the numbers shows that the "Magnificent Seven" dominant US tech companies aren't central to the valuation gap, although they have exacerbated it in recent years. Again, it's notable that the FTSE only starts to be left behind a few years after the GFC:  The performance of RELX Plc, previously known during the FTSE 100's history as the Reed Group and Elsevier-Reed, suggests that the FTSE might have done better with more tech companies. A large data provider, it's the strongest performer among the original constituents, returning 36,151% over the four decades, and narrowly beating the tobacco group BAT into second place. It's now Britain's largest "TMT" (telecommunications, media and technology) group, and has been lifted recently by its investments in artificial intelligence. Unfortunately, it doesn't have much company in the UK. Another issue for the UK is the FTSE's heavy weighting in international mining groups, which tend to list in London. When commodity prices are weak, as for most of the last decade, this drags on the index. Alternatively, it's possible to blame Britain's pension funds. Back in the 1950s, they pioneered what would become known as the "Cult of the Equity," led by George Ross Goobey of Imperial Tobacco's pension fund. Rather than stick to bonds, they piled into equities, which at the time yielded more. Over the last 20 years, that effect has moved totally into reverse. The following chart is from Britain Plc in Liquidation, a startling report by Michael Tory of London's Ondra Group, and shows how the proportion of equities in pension funds' portfolios has fallen over time:  From more than half of pensions' funds under management in 1990, equities now account for less than 10%, a staggering reduction over a period when stocks have generally performed well. Pension funds are famously about the long term, which effectively enables them to pile into stocks, so why have they abandoned them?

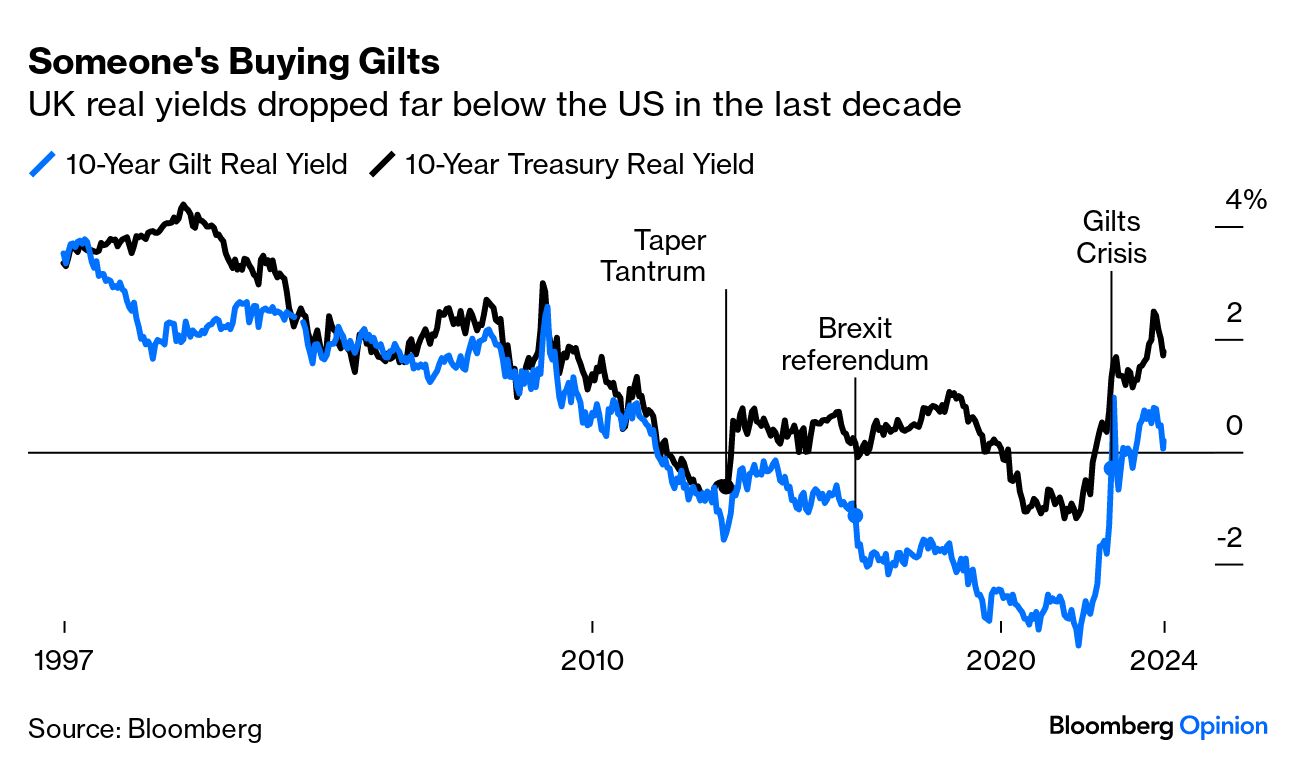

The main reason is the move toward liability-matching, which got going in earnest two decades ago, egged on by regulators and investment banks. With many defined benefit pension plans in deficit, meaning their assets did not cover their liabilities to pensioners, they began to buy bonds so that they could come closer to guaranteeing an income.

This helped British gilts perform even better than US Treasuries. It also created a cycle, as lower bond yields made it more expensive to guarantee a future income, prompting more purchases of bonds and even lower yields. It led many British funds to make derivative bets on interest rates to stay low, a practice that culminated in the implosion of the gilts market in October 2022.

Will Hutton, a veteran left-of-center economic commentator, even argues that they have forced the UK into a "doom loop" and created a system that is "rigged against growth."   There is more to this issue than pensions. But one certainty is that fixing it will be difficult, because at a national level pensions seem close to impossible to get right. Just before the pandemic, the 2019 eruption of civil disorder in Chile shook many assumptions. The country's pension system, adopted under the Pinochet dictatorship, had been widely regarded as the template for all to follow. The sight of Chileans rioting over inadequate pensions was terrifying — and might help explain why liability-matching might be a good idea.

There's also a risk of taking things too far. If British capital has oozed out of the UK stock market, it's at least in part because investors thought there were better returns to be had elsewhere, and they were probably right. And with capital moving so freely in the era of globalization, the whole debate over protectionism versus trade is coming back. This time, it's over the international movement of money, rather than goods. Some of Hutton's ideas veer close to a modern version of protectionism, or even to attempts to pick winners. For example, he suggests:

UK companies in aggregate warrant their shares being bought, and, if all pension funds simultaneously directed disproportionately more of their assets to the UK, it would lift corporate Britain off the rocks. It is a classic case of where the state has to act decisively because the market can't and won't.

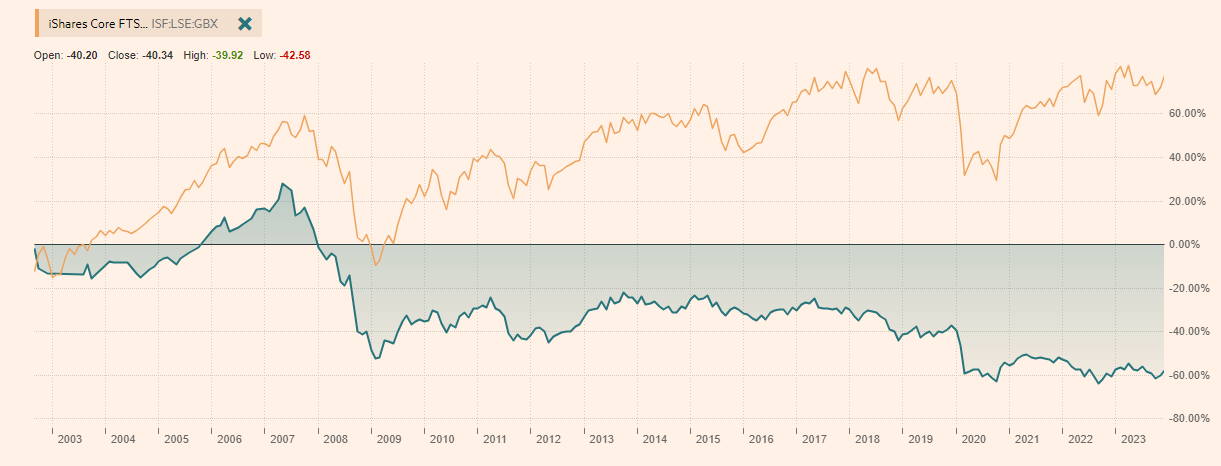

I understand the point being made, and it's necessary to stake out positions to move debate forward. But forced investment of pensioners' money in British companies doesn't sound like a good idea to me. That said, the FTSE 100's unhappy birthday does suggest strongly that something is going systematically wrong with the UK stock market. Others take note. Even if the last four decades haven't been the greatest for London markets, there is at least one way they've gone ahead of the US. Prior to 1984, the ubiquitous benchmark for London stocks was the FT 30, compiled by the editors of my alma mater, the Financial Times. Modeled on the Dow Jones Industrial Average and in place since the 1930s, the index featured 30 big stocks chosen by the editors. Only mergers and bankruptcies could dislodge a member, and they were equally weighted. A selling point for the newspaper for many years, I started my career there in 1990 with a colleague whose job had once been to calculate the FT 30 every afternoon after the market closed, with a slide rule. At that point, such a service was a competitive advantage for which our readers were happy to pay. But data services have moved on since then, and it's possible to calculate far more complicated movements by markets throughout the day and publish them in real time. As British journalists at the Guardian and Times point out, the 100-stock benchmark now turning 40 was initially set up by the London Stock Exchange in competition with the FT 30. It was received very frostily by my old bosses. Within weeks, however, they had instead decided to join forces and the name FTSE was born. The indexing group formed by the London Stock Exchange and the FT went on to greater things. These days, the FT no longer has a stake, and what is now known as FTSE Russell is controlled completely by the LSE. All of this sounds very similar to the history of the Dow Industrials, which spawned a family of indexes and eventually became part of the Standard & Poor's indexing business under the same roof as the S&P 500. The difference, unfathomable, is that the tradition-lovers in London have lost all interest in the FT 30, recognizing it for the anachronism it is, while the modern iconoclasts in the US still insist on treating the Dow Industrials as if it matters, when it plainly doesn't. After much searching, I couldn't find the FT 30 on the ft.com website, or on Bloomberg. I did, however, find a fund managed by Phoenix Life which has tracked the FT 30 since 2002. It's marked in green in the chart from the FT below. You can find it here. The yellow line shows the performance of a fund which tracked the FTSE 100 for comparison: If you wanted to make money, the FT 30 was not the place to be. If you just wanted to track an index, its equal-weighting and the big allocations to often declining and illiquid shares doesn't help, either. The FT 30 is a grand piece of financial history, and like the Dow Industrials it helped open markets and aid understanding in its time. But that time has passed. The Dow Industrials doesn't look anything like that bad, but only because its composition is now regularly being reverse-engineered to look as much as possible like the S&P 500. Most of the Magnificent Seven aren't in it. In several cases, it chooses a smaller member of a sector over a larger competitor because this fits its price-weighting methodology (for example, it includes Chevron Corp. but not the larger ExxonMobil Corp.). The FT 30 does, I suppose, say that a group of strong, large UK companies have declined badly over the last decade or so. The Dow doesn't tell us anything. So yet again, I suggest to all journalists and particularly those at Dow Jones that there's no need to cite the Dow, and that there'd be no embarrassment in consigning it to the dustbin. Keep calculating it and publishing the number in the inside pages of the Wall Street Journal by all means. But admit that it's obsolete. One possibility I've aired in the past: Change the name of the S&P 500 to the Dow Jones 500 (or "the Dow") for short, do a one-off recalculation so that the S&P 500's number equals the previous night's close for the Dow, and carry on as before. Why not? For those who missed last week's newsletters on what would have been the best trades of 2023, you can catch up with them now. Hindsight Capital Part One can be found here, and Part Two is here. We also have a video, courtesy of my brilliant colleagues in Bloomberg Opinion's multimedia department. You can watch it here. Enjoy. And now for the much tougher job of navigating 2024, without the benefit of hindsight... On the subject of 1984, some Orwellian-inspired music would include substantially all of David Bowie's Diamond Dogs album (try "1984," "Big Brother" or "We Are the Dead"), or 1984 (For the Love of Big Brother) by the Eurythmics. Both projects were unsuccessful in a way; Bowie was going to write a full opera of "1984" but didn't get approval from Orwell's widow, so took the material he had and put it into the album, while the Eurythmics wrote a soundtrack for the movie of 1984, starring John Hurt, which in the final version wasn't used. They're both good albums. Still on the subject of 1984, but much less Orwellian, you could try Van Halen's 1984 album, from (you guessed it) 1984.

Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close.

More From Bloomberg Opinion: - Mark Gilbert and Marcus Ashworth: The Fed Will Set the Pace for Markets More Than Ever This Year

- Adrian Wooldridge: The Trump Comet and Four More 2024 Predictions

- Allison Schrager: 2024 Will Mark the End of the Post-Pandemic Economy

Want more Bloomberg Opinion? OPIN <GO>. Or you can subscribe to our daily newsletter. |

No comments:

Post a Comment