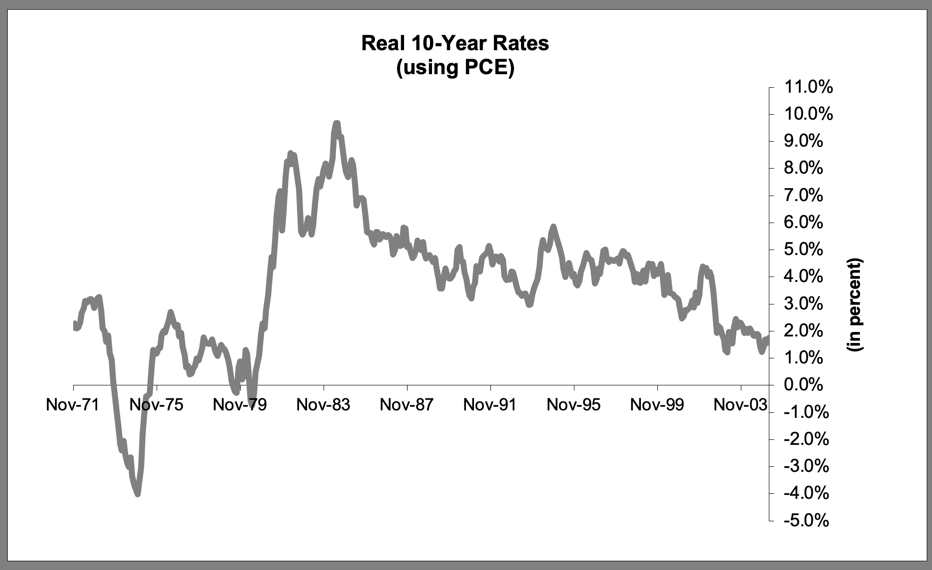

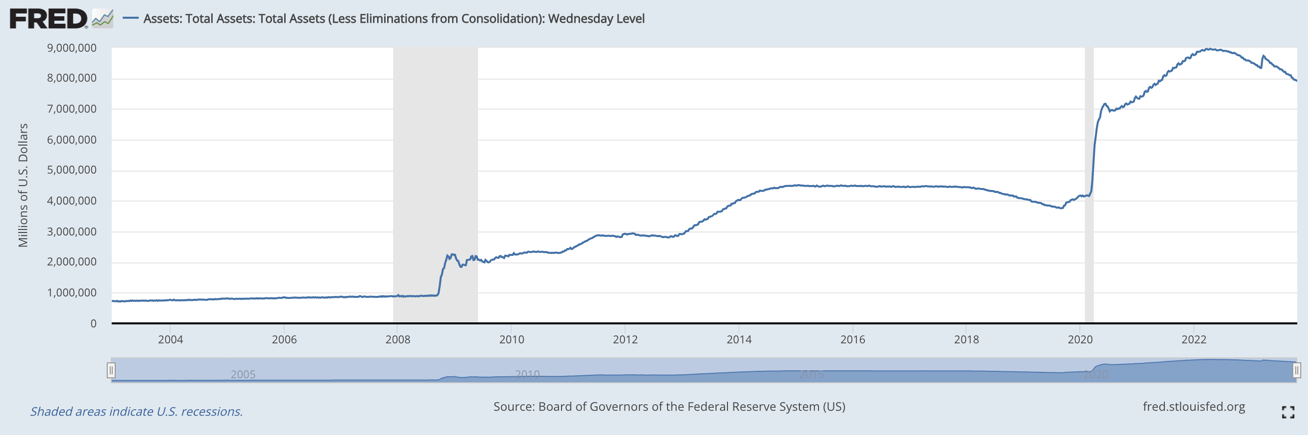

| How far will the Fed let its balance sheet shrink? Well not back to where it was before certainly. The Treasury market is much bigger now. So the Fed's balance sheet needs to be correspondingly bigger. And if the Fed wants to have ammunition to impact financial stability it needs an even bigger balance sheet if the outstanding Treasury debt was $10 trillion in 2008 and it's $33 trillion now. You could easily see a $3 trillion Fed balance sheet. Throw in higher regulatory capital requirements requiring higher reserve balances and a buffer for fighting crisis and you could get to $4 or 5 trillion. That's not the $7.9 trillion we currently see. But it's a lot bigger than before the Great Financial Crisis. So while rate policy may be going back to the 1980s and 1990s, the balance sheet is not. Likely, if you listen to what the Fed officials say they want to achieve, we're going to see a bigger balance sheet in perpetuity. One corollary here is that it reinforces the concept the Fed isn't going back to zero. The Fed won't need to cut to zero if it uses its balance sheet for financial stability. Imagine a world where the Fed cuts rates from 6% to 3% in a recession and mops up any financial instability concerns with special targeted programs using its balance sheet. That way real interest rates act as friction against higher inflation after the recent stagflationary scare, scarred as we now are. Gone are the days of massive rate cuts to near zero that began in the 2000s and huge Fed buying that began in the late 2000s. Savers will continue getting 3% interest, mortgage rates won't drop to 3%, and the discount rates for stocks will remain elevated. That's a lot different than the past 15, even 25 years. All of that sounds a lot more like the Fed of William McChesney Martin, who led the institution from 1951 until 1970 and famously quipped that the Fed's job was "to take away the punch bowl just as the party gets going." So forget the Fed put and get ready for a less forgiving safety net for investors. Even so, if you listen to the way Powell and others speak, there has been a sea change in how they think about monetary policy's influence on the more economically vulnerable and less wealthy. Time and again Powell talks about raising rates to quell inflation in order to help exactly those members of society who are most impacted by inflation. He also stresses the balancing act they have in not overdoing it and causing a recession that throws those same people out of work. After all, having a paycheck but dealing with inflation is a lot better than having no paycheck at all. I don't think this is just lip service. The Fed really wants to thread the needle. And that means the days of NAIRU — the non-accelerating inflation rate of unemployment — driving the Fed to hike lest a too, too low unemployment rate cause inflation to spiral out of control are over. The Fed now believes we can have our cake and eat it too, keeping inflation and unemployment low as long as real interest rates are permanently restrictive. Their hope is it means the end of boom bust, which most benefits those that get onto the employment ladder last in any business cycle. On Wednesday afternoon I expect to hear the contours of this policy framework in what Powell has to say as he speaks after the rate decision at 2 PM. A lot of it is the a repeat of what we saw before, but with key differences on the balance sheet and thinking about the Phillips Curve pitting unemployment against inflation. Bonds are going to love this. It's not the bond market rally we saw as the 10-year Treasury yield came down from over 15% in 1981. But it does ensure bond investors can safely clip coupons once we reach the plateau the Fed thinks is restrictive enough to keep tightening policy. I think there is a non-zero chance the Fed is forced to go to 6% in 2024 if the US economy remains hot and inflation stays above 3%. So we're talking about the period just afterward. Even so, some investors already feel near 5% yields are good enough. They're moving out of cash and further out the curve. Stan Druckenmiller even recently said he's very bullish on 2-year Treasuries. And the bond market math behind so-called convexity says it's not much harder to inflict further huge losses on Treasury investors. If there is a recession, you can see the Fed cutting rates and giving enough rate relief to debtors that it buoys the economy without the Fed needing to get to zero rates. If mortgage rates fall from 8% to 5%, how many people with 4% mortgages would be willing to move? A lot. All you need is to get into the ballpark of where their existing rate is and suddenly people are willing to make different decisions. That's not a 'Fed Put' though. So those people who overweighted risky equities instead of hugging the index via ETFs are not going to find a lot of rate relief to help them as recession takes hold. AMC is nearly 88% down from its 52-week high, for example. A few Fed cuts isn't going to get you anywhere close to those previous levels. For equities overall though, let's remember that we only recently came off the 4th ever period of 200% real returns over a decade. That's a headwind for future returns since long-term equity returns tend to overshoot to the downside after such magnificent run-ups. And it's the real yield that will do it. Back in August I wrote "the peak in US equities was probably in July." Stocks have since had an official 10% correction from that July peak — and for the reasons I outlined then, rising real yields. And as the Fed wants higher real yields permanently, this is a permanent headwind for equities from that high base. Mind you, stocks can continue to rally as long as we avoid recession. But that rally is capped by a higher discount rate and competition from bonds. A 60-40 portfolio, in that context, doesn't seem so bad. I want to end this on a bright note. Since increasingly people are thinking about getting exposure to different asset classes via ETFs, they can tax-efficiently mimic the indexes and outperform active management with lower fees. We see that with equities and the same trend is coming for bonds. That will keep people liking a 60-40 portfolio as long as equities don't crater. One asset class to also think about in that context is crypto. If crypto gets an ETF, it's a game changer. From a compliance perspective, suddenly you have a whole host of asset gatherers who have no problem getting into crypto. And that's going to help keep interest in the asset class going. Something to think about if you consider ETFs and the diversification benefits they will bring as they start to dominate the investment landscape. |

No comments:

Post a Comment