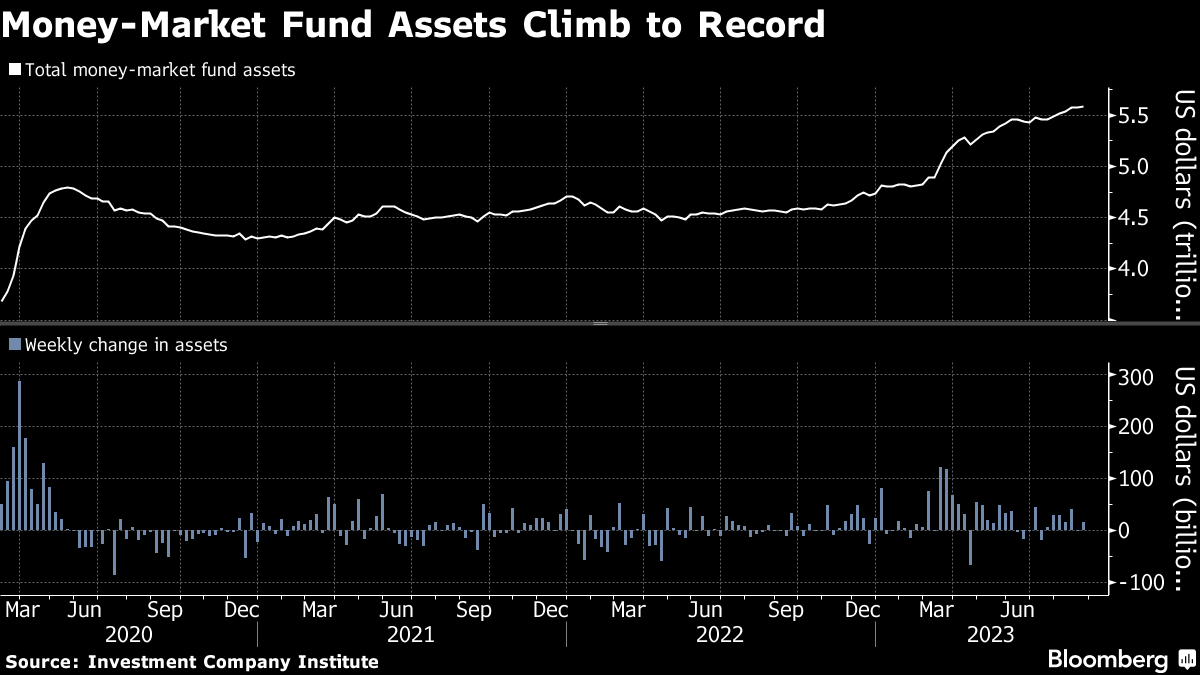

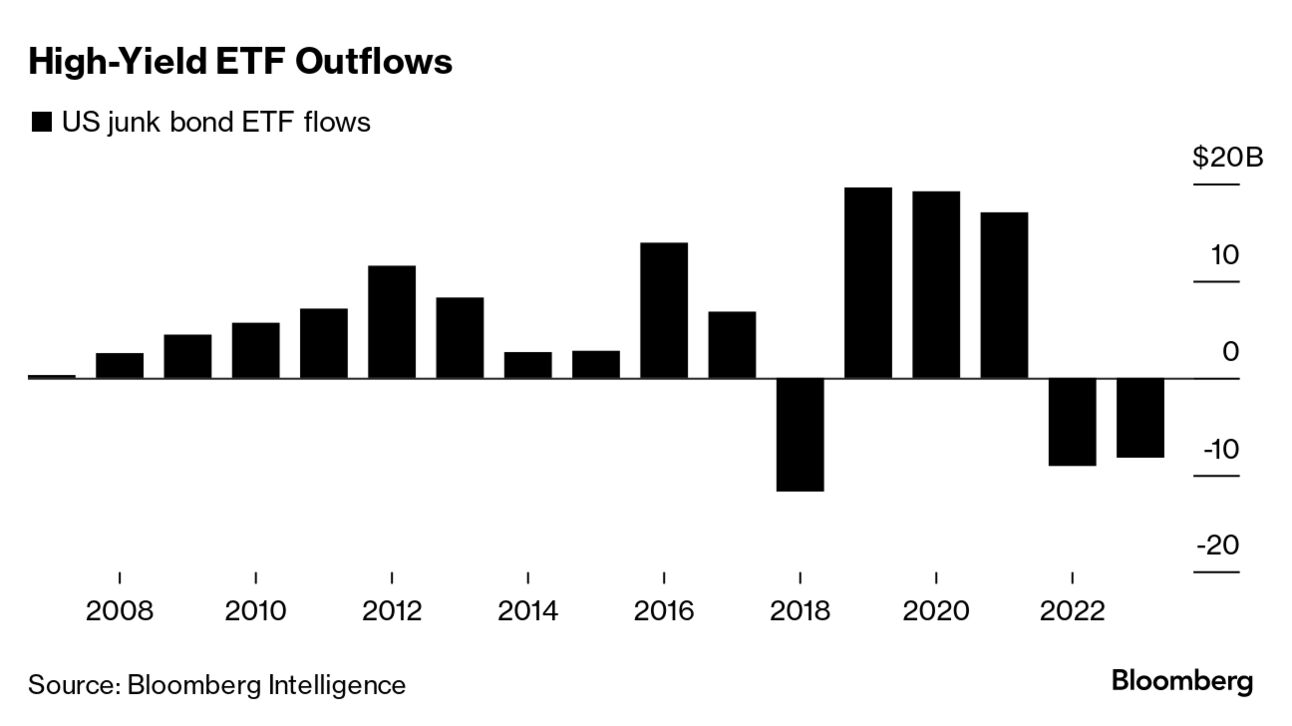

| Welcome to the Weekly Fix, the newsletter that's always screaming about something. I'm cross-asset reporter Katie Greifeld. My favorite type of sentence is one that includes both "screaming" and "Treasury" in it. Luckily for me, Ian Lyngen of BMO Capital Markets delivered a beauty this week. "The 10-year Treasury in my mind is a screaming buy," Lyngen said on Bloomberg Television. "I think that from here the path forward for nominal 10-year yields is going to be lower." Specifically, Lyngen sees benchmark 10-year yields returning to a range between 3.5% to 3.75% by the end of this year as investor confidence in the Federal Reserve's inflation-fighting prowess builds, en route to reaching 3% in the first half of 2024. For context, 10-year yields broke decisively above 3% last August and have climbed since. Evidently, Lyngen isn't alone. While this August saw 10-year yields climb for a fourth straight month, a big bid returned to the bond market in recent weeks: after rocketing as high as 4.36% on an intraday basis, the rate is sitting at about 4.1%. But even as the selloff loses steam, some of the world's biggest investment firms aren't yet ready to give the all clear. As reported by Bloomberg's Michael Mackenzie, money managers from the likes of BlackRock Inc., T. Rowe Price Group Inc. and the Vanguard Group expect yields to resume their climb higher as a still-strong US economy threatens further Fed hikes. Take Roger Hallam, Vanguard's global head of rates. While his base case is that the US tips into a recession around the middle of next year, the economy's resilience has been a surprise — and as such, the 10-year "is not attractive until it gets to 4.5%." BlackRock's Craig Vardy is of a similar mind. The head of fixed-income at the asset manager's Australian office says that central banks are likely to extend hiking cycles, meaning that 4.25% to 4.5% is a "more realistic" range for 10-year Treasuries. Whether you're screaming buy or stay away from benchmark Treasuries, both narratives face a test on Friday morning with the last jobs report before the Fed's September meeting. Economists anticipate that the US added about 170,000 jobs in August, the slowest pace of gains in over two and a half years. Meanwhile, things are heating up at the very front end of the yield curve. More than $7 billion has flooded into ultra-short duration fixed-income ETFs in August through Wednesday's close, the biggest one-month haul since February, Bloomberg Intelligence data show. Appetite is similarly robust for money market funds, sending assets to an all-time high of nearly $5.6 trillion this week. There's two dynamics at play. The first is that turbulence finally returned to the stock market in August, sending the S&P 500 to its first monthly loss since February. Not to mention, September is waiting on the other side — the worst month on average for the benchmark, according to 30 years of seasonal data. The other explanation is a continuation of a dynamic that's been at play all year — more than 5 percentage points of rate hikes have lifted yields on the shortest-dated paper to the highest levels in decades. That's both boosting the appeal of cash while creating a headache for banks. "I'll tell you what's driving those flows. I won't name names, but my bank pays 80 basis points on cash. So guess what my bank doesn't have? My cash," Mimi Duff of GenTrust told me and Romaine Bostick on Bloomberg Television. "What we've also seen in these small regional, small regional sized banks, those money flows are coming out of those banks that aren't paying on deposits. There's a lot of pressure." While peak panic in the aftermath of March's banking turmoil has passed, the deposit story remains a long-term pain point for small- and mid-sized lenders. It was one of the main reasons why Moody's Investors Service and S&P Global Ratings both downgraded a slew of US banks in August, months after the crisis unfolded. Many depositors have "shifted their funds into higher-interest-bearing accounts, increasing banks' funding costs," S&P wrote in a note summarizing the moves. "The decline in deposits has squeezed liquidity for many banks while the value of their securities — which make up a large part of their liquidity — has fallen." One of the near-universal truths in investing tis that flows follow performance. For high yield bonds, that hasn't been the case all year. Judging by some of the category's largest exchange-traded funds, junk debt has handily outperformed this year. Take popular tickers such as JNK and HYG; they're sitting on total returns of 6.7% and 5.9%, respectively, so far in 2023. That compares to a 1.5t% return for AGG, which tracks the broad bond market, while TLT — long-dated Treasuries — is underwater this year. You'd never know it from the flow show. Nearly $1.8 billion has exited from JNK so far this year, while HYG is nursing outflows of almost $1.5 billion. High-yield bond ETFs have bled over $8.2 billion so far this year, after shedding more than $9 billion in 2022. So why does no one love this rally? "Because valuations are so rich," said Sameer Samana, senior global market strategist at the Wells Fargo Investment Institute. "Overall risk/reward is pretty poor — earn about 400 basis points of carry if all goes well, and a recession could easily see spreads well north of 600 basis points." It's true — both investment-grade and high-yield spreads are narrow relative to history, especially given that the jury's still out on what kind of landing the US economy is heading for. But while that might neatly explain the junk outflows, it's still a bit of a mystery while investors keep lining up to be burned by TLT. The long-dated Treasuries fund has absorbed a stunning $15.5 billion this year, the second-largest haul of more than 3,100 US-listed ETFs this year. |

No comments:

Post a Comment