| I'm Chris Anstey, a senior editor for economic policy in Boston, and today we're looking at Japan's stealth monetary-stimulus removal. Send us feedback and tips to ecodaily@bloomberg.net or tweet to @economics. And if you aren't yet signed up to receive this newsletter, you can do so here. One market participant on Friday, trying to make sense of what Bank of Japan Governor Kazuo Ueda had unveiled earlier in the day, quipped that he was essentially trying to both have his cake and eat it. And he pretty much did, based on what's happened in markets since the BOJ announcement. Exiting any sort of peg in financial markets is fraught with risk, as former Treasury Secretary Lawrence Summers, a paid Bloomberg TV contributor, likes to highlight. An extreme example was Argentina breaking the peso's decade-long 1-1 fix to the dollar in 2002, which triggered a massive inflation spike and a severe economic contraction. China's August 2015 currency devaluation sowed confusion across global markets, with reverberations even for Federal Reserve policy. When it comes to Japan, the world's largest net creditor, there's plenty of cause for concern about any unbridled freeing of the central bank's peg for longer-term bond yields it has kept in place for seven years now. Even the whiff of Japan joining the rest of the advanced world in retreating from zero rates could send markets reeling. That was on display Thursday, when US Treasury yields jumped and a Wall Street stock rally turned into a tumble after Japan's Nikkei newspaper reported the BOJ would relax its yield-curve control. So there's every incentive to move carefully. And indeed, the BOJ has been. The shift away from pegging 10-year yields near zero already began last December, when Ueda's predecessor Haruhiko Kuroda doubled the tolerance range for yields to 0.5%. Friday, Ueda said that 0.5% mark isn't so much a ceiling as a vaguer reference point. But to avoid lacking any kind of anchor, he also said daily bond purchases would be conducted at a fixed rate of 1%. At the same time, he insisted that there's been no move toward normalization of policy. And just to keep markets on their toes, the BOJ on Monday sprung another surprise, announcing an unscheduled bond-purchase operation to tamp down rates. The move pushed the yield on Japan's benchmark debt from a fresh nine-year high of 0.605% while also jolting the yen, which reversed a gain against the dollar and weakened about 0.4%. On its face, the BOJ's various maneuvers are complex and jargon-filled. But in fact that's a help. It allows for stepping away from the peg without clearly declaring it.  Kazuo Ueda, governor of the Bank of Japan Photographer: Akio Kon/Bloomberg The result on Friday: barely a peep in broader financial markets. Japan's equities dipped. US stocks and Treasuries rose. And rather than careening higher, the yen ended down on the week. Japan's bond-buying operations are complicated enough that further tweaks could be made, continuing the erosion of the former policy. By the time it's declared dead, the announcement may become moot. As for the short-term policy rate, now set at negative 0.1%, there'd be ways to dilute the relevance of that, too, if it turns out inflation is sustained enough that a further BOJ shift is required. If the world's No. 3 economy is able to extricate itself from long-held monetary pegs without roiling financial markets, Ueda would arguably merit quite the cake. - Britain's young families and low-to-middle earners in the Millennial generation are shouldering the burden in an effort to curb inflation.

- The Rhine River has been a vital shipping lane for centuries, but the climate crisis means a desperate scramble with falling water levels.

- A Lebanon's central bank deputy will take the top job on an interim basis after the governor faced money-laundering allegations.

- Nigerian President Bola Tinubu ordered a special investigator probe the central bank's operations in a fight against corruption.

- Chile slashed its key rate by a larger-than-expected 100 basis points, spearheading Latin America's shift toward looser monetary policy.

- Germany's economy — Europe's largest — is struggling to grow, and the weakness is set to persist.

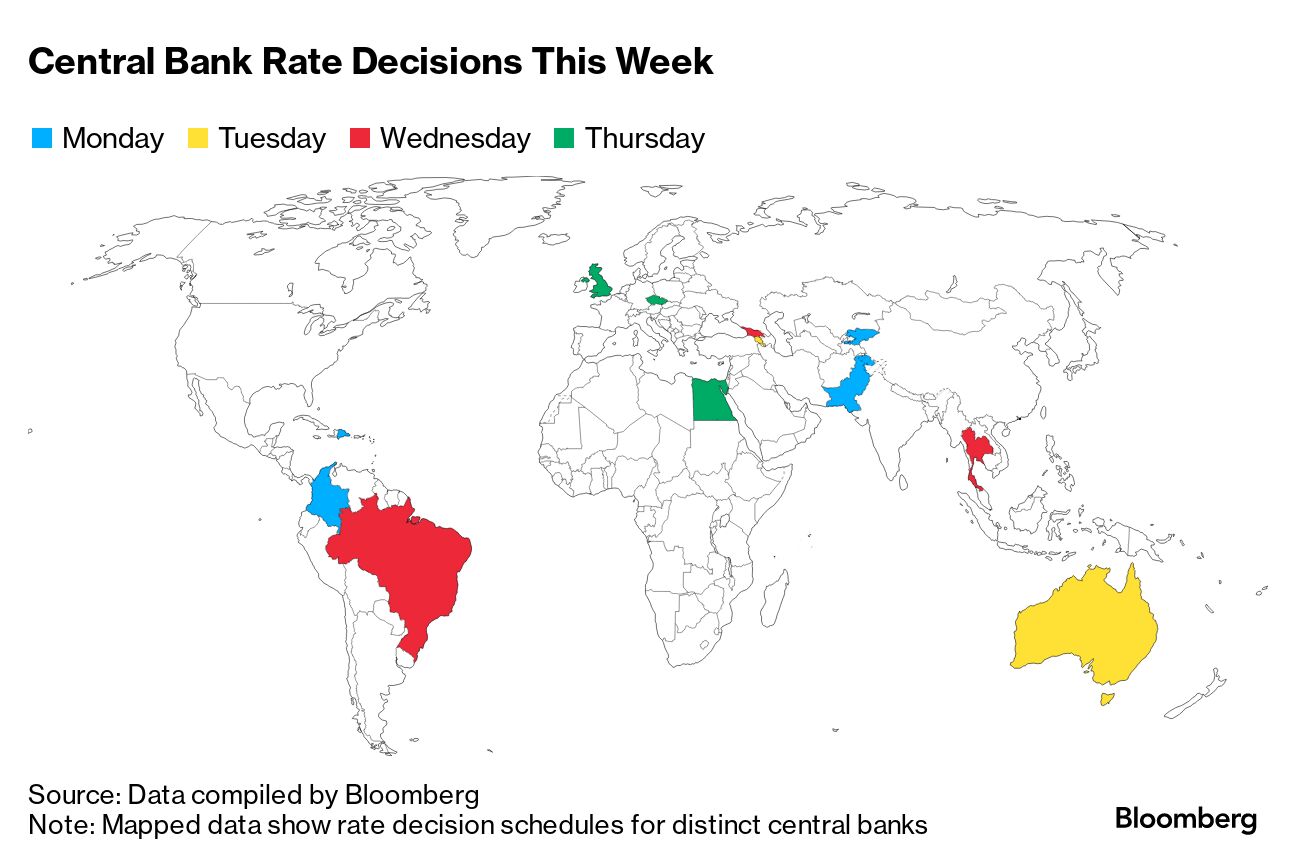

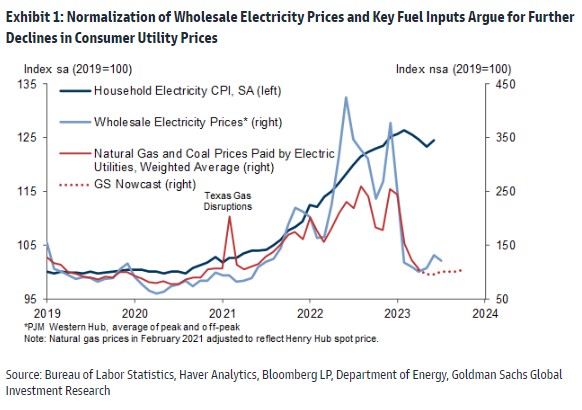

Hiring in the US probably increased at a healthy yet more moderate clip this month, representing a vote of confidence about the demand outlook after a solid first half of the year. The closely watched jobs report on Friday is projected to show employers boosted payrolls by 200,000 in July, while unemployment held at a historically low 3.6% and hourly pay cooled. Earlier in the week, separate data are seen showing fewer June job openings that indicate better balance in the labor market. Elsewhere, suspenseful decisions on possible rate hikes in the UK and Australia, along with a potential cut from Brazil's central bank, will be among the highlights for investors. See here for the rest of the week's economic events. Gasoline prices may not be helping with inflation these days, but Goldman Sachs economists are saying to keep an eye on electricity prices. Those paid by consumers are starting to unwind what's been a 25% surge since 2019, they said late last week. Using a consumer price index measure, Goldman's team is projecting a 3% to 4% pullback in cumulative electricity prices by this fall, economist Spencer Hill wrote in a note. Goldman even shaved its December CPI year-on-year inflation forecast to 2.9% from 3.1% as a result. "We also find a surprisingly important role for consumer electricity prices in forecasting personal consumption, and we estimate that the tailwind from cheaper electricity could offset as much as half of the consumption drag from the resumption of student loan payments," Hill wrote. Read more reactions on Twitter |

No comments:

Post a Comment