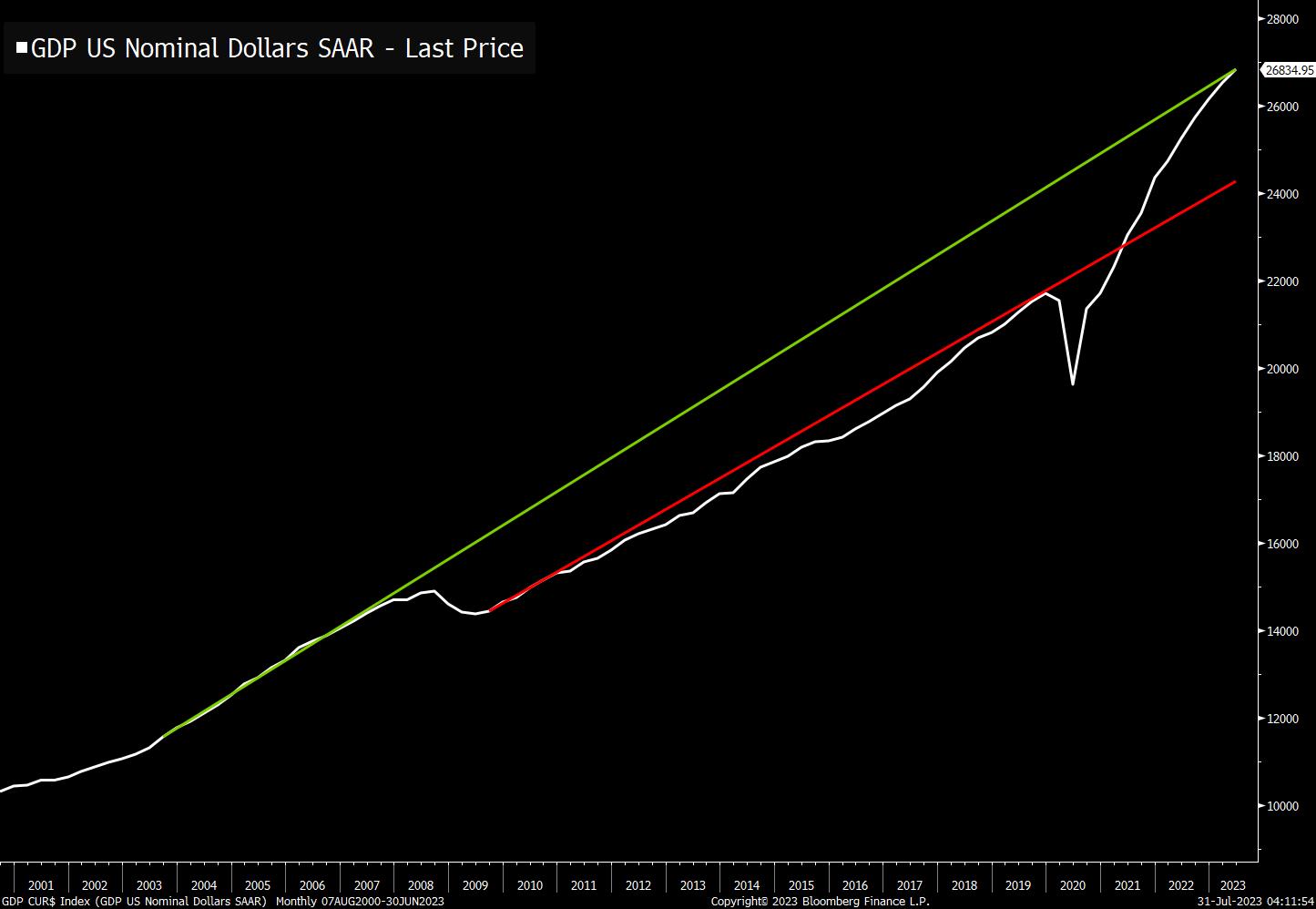

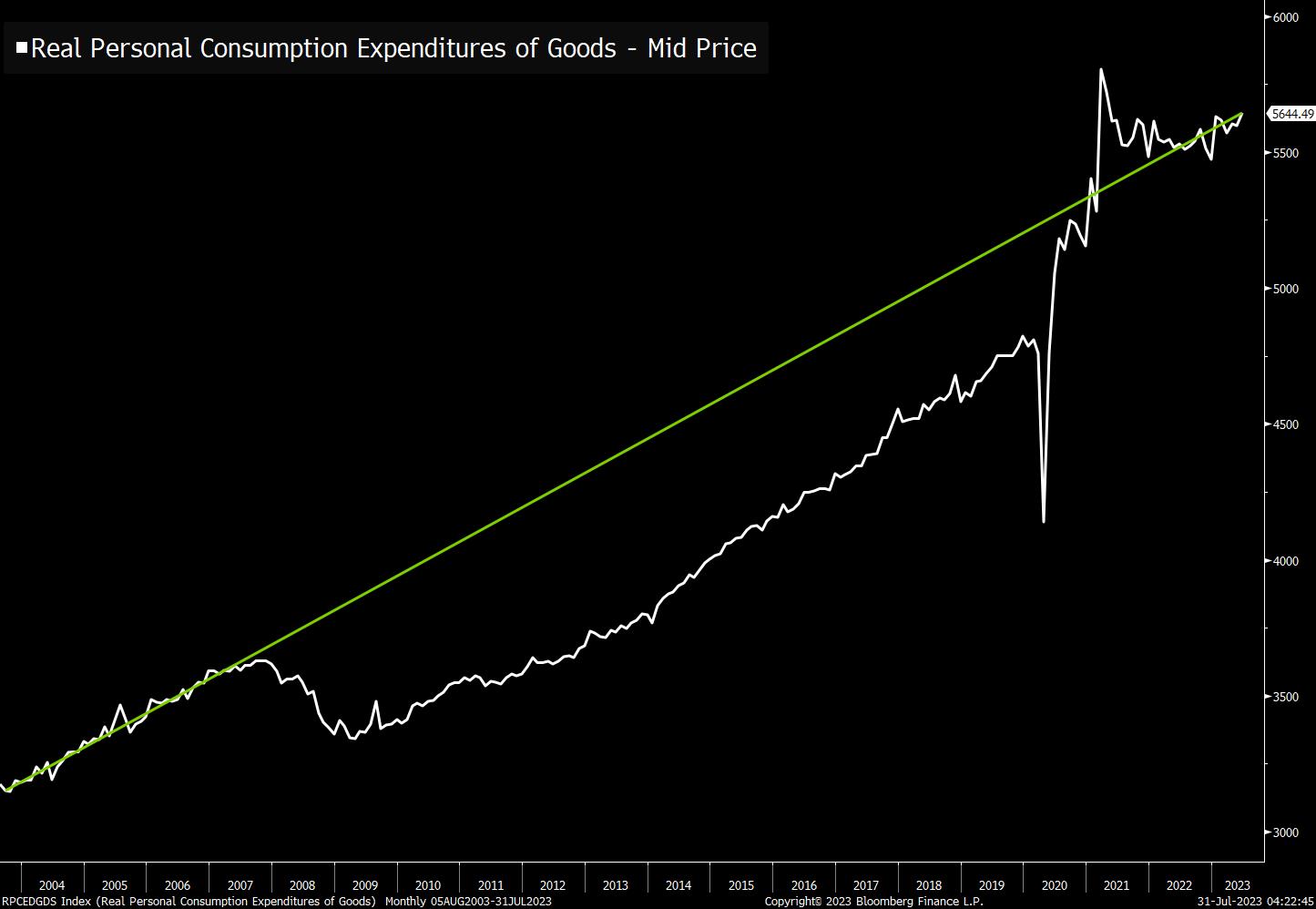

| US equities follow the 2019 playbook, China stops short of direct consumer support and investors are skeptical of the artificial intelligence hype. — Kristine Aquino US equities are tracking the same path they did in 2019, when investors saw a 29% return in one of the best years for the S&P 500 over the past decade. That's according to Morgan Stanley's staunch bear, Michael Wilson, who noted the rally a few years ago was "driven almost exclusively by multiple and not earnings." Wilson correctly predicted the selloff in stocks in 2022, though his bearish outlook is yet to materialize this year. He said his team is open to the view that the economy could eventually enter a new upturn cycle. Still, "we'd like to see a broader swath of business cycle indicators inflect higher, breadth improve and front-end rates come down before adjusting our stance in this regard," Wilson added. China is seeking to boost consumption to spur the economy's recovery, although the government has stopped short of providing direct fiscal support to consumers and companies to increase spending. The nation's top economic planning agency released a wide-ranging policy document Monday, which focuses on removing government restrictions on consumption, such as car purchase limits, improving infrastructure and holding promotional events like food festivals. Latest figures showed consumption-related growth is waning in China. Survey data showed weaker services activity in July than in June, while separate data from China Beige Book indicated consumers cut back on spending on everything but travel and restaurants last month. Investors are betting the great tech rally of 2023 has staying power, with 77% of the 514 respondents in a Bloomberg survey saying they plan to either increase their exposure to technology stocks or keep it steady over the next six months. Yet they're not going all in on artificial intelligence — half are disinclined to pay out of their own pocket for AI tools to aid their personal or business life, while a majority of firms aren't planning on using them for trading or investing ahead. "Right now, the near-term hype is over its skis," said Ted Mortonson, a technology strategist at Robert W. Baird & Co. US equity futures were little changed as of 5:49 a.m. in New York. The Bloomberg Dollar Spot Index pulled back from earlier highs, boosting most Group-of-10 currencies. Treasury yields edged higher, mirroring moves in UK and European bond markets. Gold drifted lower, while oil climbed and Bitcoin rose 0.3% Chicago Federal Reserve President Austan Goolsbee speaks in an interview on Yahoo! Finance Live at 9:20 a.m., while Dallas Fed will publish its manufacturing gauge at 10:30 a.m. and the Fed will release senior loan officer opinion survey at 2 p.m. Earnings include ON Semiconductor, Arista Networks. Here's what caught our eye over the past 24 hours: When the Global Financial Crisis hit, there was a huge negative shock to economic output. Numerous charts started to look like this one, where the whole growth trend shifted down onto a lower trajectory. It was popular in those years to accept that this loss of output, or potential output, was inevitable or justified. After all, 2004, 2005, 2006, 2007... those were housing bubble years right? Surely that growth rate must've been unsustainable. Obviously you can't just go back to the old trendline right? But if you think about it for more than 5 minutes, the acceptance of lower output never made much sense. All the labor and raw materials that existed in 2006.... it still existed in 2010. Yes, there were certain aspects of housing finance that created a run on the banking system. But from a production standpoint, whatever capabilities we had pre-crash still existed post-crash. There's a great line from Keynes "Anything we can actually do, we can afford." Perhaps it sounds tautological, but it's not. We had the real resources to keep building, we just stopped doing it. And then of course over the following decade, the whole idea of what was "unsustainable" got turned on its head. It wasn't all of the housing construction of the mid-aughts that was unsustainable. It was the lack of housing production in the 2010s that turned out to be unsustainable. That lack of production still haunts would-be homebuyers and the broader economy right now. Bringing things forward to today. We've been on a pretty nice run of economic data lately. And the world has woken up to a new type of chart. Alex Williams of Employ America has deemed it The Frying Pan Chart. The charts look like this. And it's such a good name, it is certainly going to stick and be a defining chart of this moment. Old trends from pre-crisis are beginning to re-assert themselves. Here's another Frying Pan Chart that was surfaced by Joel Wertheimer on Twitter. Real Goods Consumption has been gathering steam again and seems to be meaningfully above the 2010s trajectory. Sitting here today in the middle of 2023, looking at charts like these, it seems at least possible, that the money cannon originally fired by Trump and Mnuchin and then followed up by Biden and Yellen, not only knocked cold the Covid recession, but has begun to erase the costly lost output of the post-GFC period. Recessions may be inevitable, but that doesn't mean we have to accept that each downturn permanently curtails our economic capacity. Follow Bloomberg's Joe Weisenthal on Twitter @TheStalwart. |

No comments:

Post a Comment