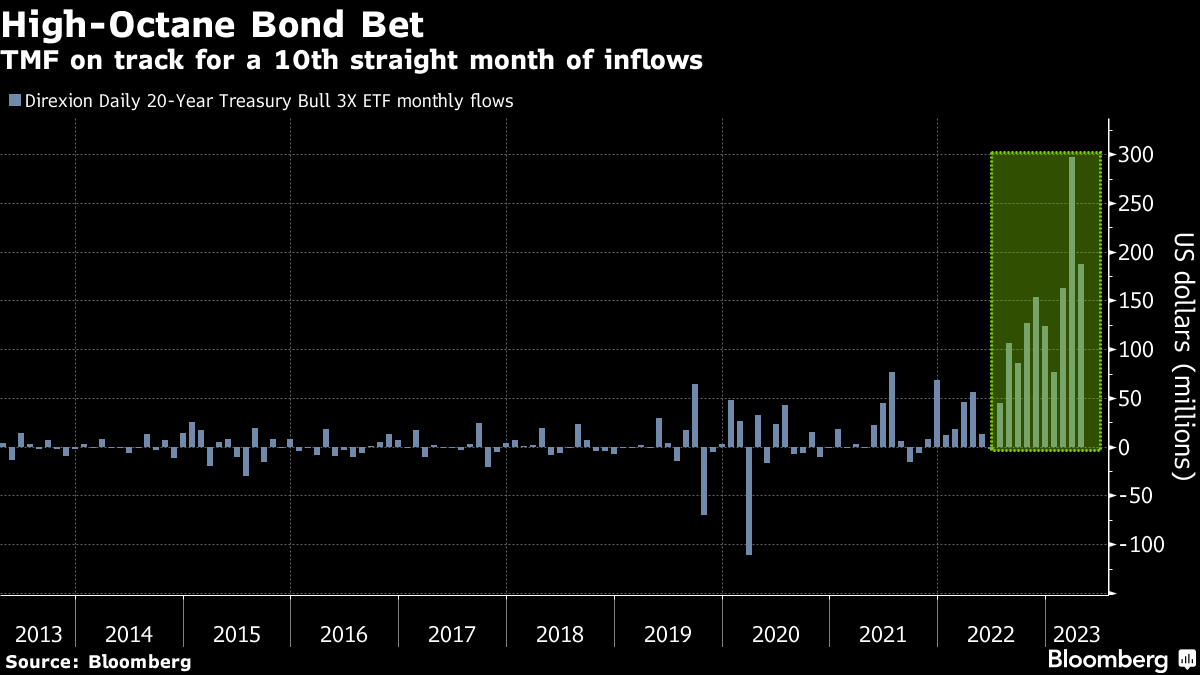

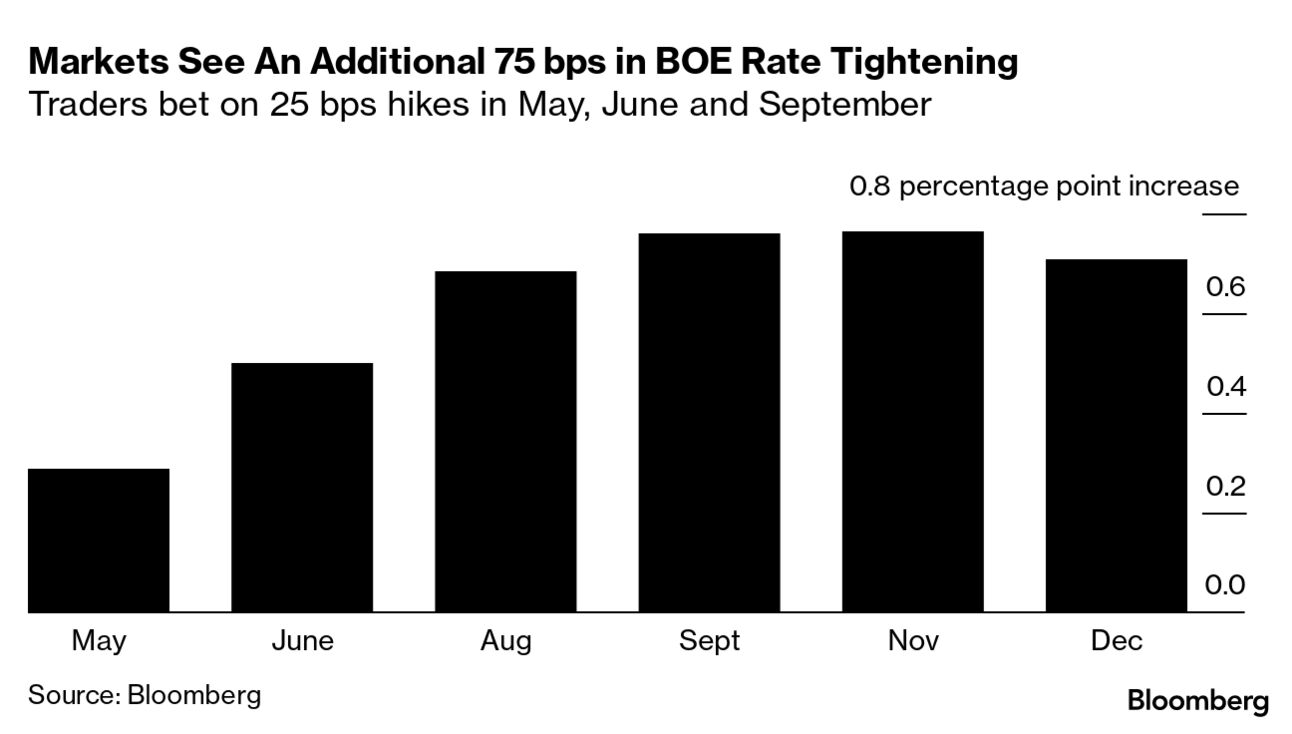

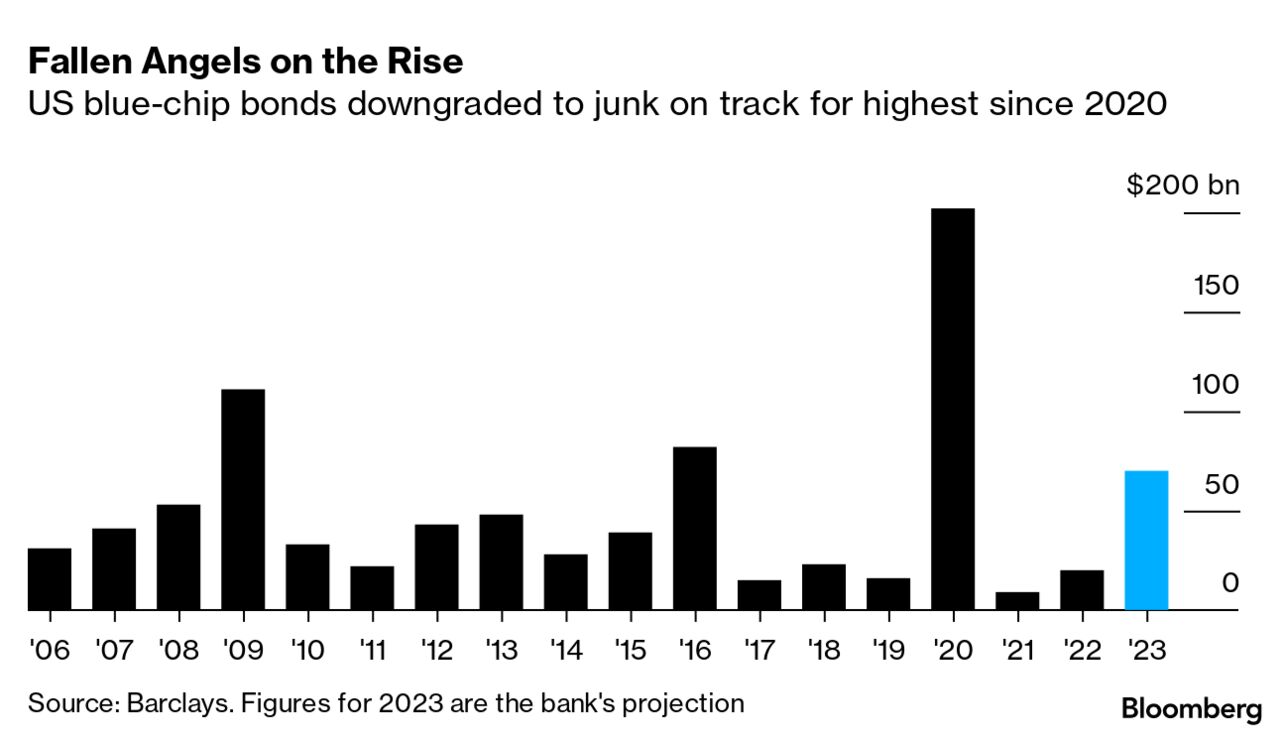

| Welcome to the Weekly Fix, the newsletter that's always been firm in its commitment to fighting inflation. I'm cross-asset reporter Katie Greifeld. Much has been made of the bond market's standout volatility over the past few months. But for a small cohort of exchange-traded fund investors, it's not enough. Assets in the 15 leveraged fixed-income ETFs trading in the US have climbed to $3.5 billion, Bloomberg Intelligence data show. The largest such product — the $1.6 billion Direxion Daily 20-Year Treasury Bull 3X (ticker TMF), which uses derivatives to deliver three times the performance of long-dated Treasuries — has absorbed more than $720 million already this year. That puts the fund on pace to eclipse last year's record of $783 million. While the world of leveraged fixed-income ETFs has more than doubled since ending 2020 with just $1.4 billion in assets, the category actually used to be much bigger. At the end of 2013, the funds held roughly $7.7 billion overall, at a time when bond ETFs held just $254 billion versus $1.4 trillion currently. The boom-and-bust is likely a result of a robust options market developing around the big bond ETFs, according to Bloomberg Intelligence ETF analyst Athanasios Psarofagis. For example, total open interest on the $35 billion iShares 20+ Year Treasury Bond ETF (TLT) currently stands at roughly 2.2 million contracts, compared to about 827,000 contracts at the end of 2013. Given that professional money managers are more likely to buy calls on TLT, for example, than buy a fund like TMF, the present-day revival in leveraged bond ETFs can likely be traced to retail traders, Psarofagis said. "I don't think the fixed-income options market was as mature then. Bond ETFs tend to be more institutional, so they were using these, then slowly mapped over to options," Psarofagis said. "I think the new money coming in is more retail, that's why it's to a lesser extent. I think bonds kind of became the new popular 'meme' stocks in a way." Like meme stocks, it goes without saying that a triple-leveraged fund comes with eye-watering volatility. While TMF has gained 12.5% on a total return basis this year, that follows a 73% plunge last year and a 20% drop in 2021. After moving in lockstep for much of the past three years, developed-market central banks are set to go their separate ways this summer. That much was clear from this week's surprisingly hot UK inflation data, which showed that prices rose 10.1% in March from a year earlier. That return to double-digit territory stands in contrast to the latest US reading, which showed that inflation cooled to 5% on an annual basis last month. Traders were quick to ramp up bets that the Bank of England will need to lift interest rates to 5% by September, which would require an additional 75 basis points of hikes from current levels. Compare that trajectory to the Federal Reserve, which is widely expected to deliver its last hike of this tightening cycle at next month's meeting. But even with inflation double US levels and markets braced for more hikes, UK policymakers have struck a different tone than their US counterparts over the past several months. While Fed officials from Jerome Powell down have been diligently hammering home the message that price pressures must be brought back to 2%, BOE members have been a bit more sanguine. Just on Thursday, BOE chief dove Silvana Tenreyro said that interest rates are already too high, and that the bank's inflation target is "flexible." "The Fed's been taking this far more seriously at least once they realized this has been getting away from them. We've not seen the same commitment from the Bank of England," Ella Hoxha, Pictet Asset Management senior investment management, said in a Bloomberg Television interview. "So let's see what they say at the next meeting. If they put a firm message on it, that they're going to get much more serious and much more hawkish, perhaps they're turning a corner, but I would not stake my money on it." And where would Hoxha stake her money? Short gilts versus Treasuries, she said. You wouldn't know it by looking at credit spreads, but red flags are flying in the corporate bond market. For starters, ratings agencies have already downgraded more than $11 billion of investment-grade bonds to high-yield status this year, according to Barclays Plc research. That's already about 60% of 2022's full-year total, putting 2023's volume on track to be the highest since 2020's pandemic-fueled downgrade wave. All told, Barclays expects between $60 billion of $80 billion of freshly minted fallen angels this year as downgrades accelerate in the second half of 2023. The demotion to junk comes with an additional boost to borrowing costs, given that a smaller universe of investors is eligible to purchase high-yield bonds, Bloomberg's Olivia Raimonde writes. While that's scary enough, TD Securities found additional cause for concern. Yield on blue-chip bonds have shrunk relative to the effective federal funds rate, bring the "carry spread" — a proxy for funding cost — to levels only seen twice in the last 27 years. As detailed by Bloomberg's Tracy Alloway, that could spark a painful reset in risk premiums should the higher cost of funding curb demand from banks. Again, that all sounds very bleak, but none of that anxiety is reflected in overall bond spreads at the moment. IG spreads are currently hovering near 130 basis points, while high-yield spreads stand at about 450 basis points. The placidity of credit spreads is almost as frustrating as the grind lower in the VIX, despite the stock market's hot-and-cold mood swings — but TD sees the calm breaking soon enough. "The US recession we forecast in the final quarter of the year, along with the recent collapses of Silicon Valley Bank and Credit Suisse, has heightened the risk of a correction in the US investment-grade corporate bond market," says Cristian Maggio, TD's head of portfolio and ESG strategy. "Tighter lending conditions ahead may act as a catalyst for this correction." The largest Wall Street lenders rolled out their first-quarter numbers this week, and one thing is clear: March's banking crisis barely scratched the big banks. However, as beautifully reported by Bloomberg's Michael Regan, competition for deposits is still very much a thing. The likes of money-market mutual funds — which can be far more nimble than banks in passing along higher rates — beckon to the broader public in a way not seen in decades. The flow of funds says as much. The amount of money on deposit shrank by a surprise 1.5% last year — the first decline since the 1940s, Federal Deposit Insurance Corp. data show. It's reasonable to think another drop could follow in 2023, given that the cash stashed in money-market funds has ballooned to a record. As Regan outlines, there's an element of inertia for individual depositors at any bank: if you have your savings, checking, credit card and investment accounts sitting with the same bank, you'd have to be incredibly motivated to go shopping around for a better rate. JPMorgan's Chase is a great example — despite paying out as little as 0.01% on basic savings deposits, the bank actually grew its deposit base by 2% in the first quarter. It was a similar story among the other big banks. Citigroup also posted inflows, while Bank of America — which didn't provide a specific number — said that checking account deposits have been on the rise since early March. Wells Fargo was the odd one out with a 2% decline in deposits. Regardless, it's now in the mainstream consciousness that there's potentially better-paying places to park your cash. And competition is building — just this month, Apple Inc. unveiled a new savings account product with Goldman Sachs that would allow Apple Card holders to earn a 4.15% annual yield. Not to mention, Goldman's Marcus — the posterchild for high-yield savings products — boosted its rate to a record 3.9%. - Barclays to shut 21 ETNs a year after costly note blunder

- Kim Kardashian hires Wall Street talent to bulk up buyout firm

- SpaceX says it blew up starship rocket after engine mishap

|

No comments:

Post a Comment