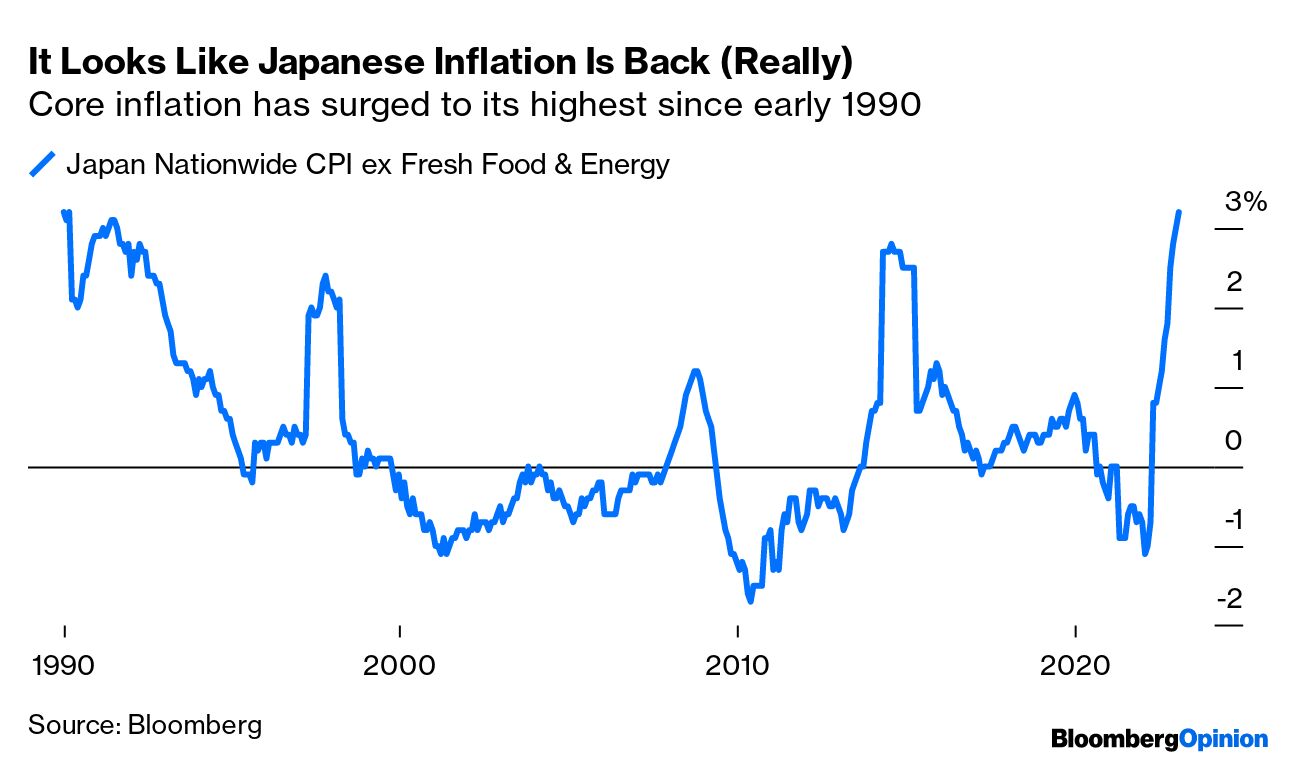

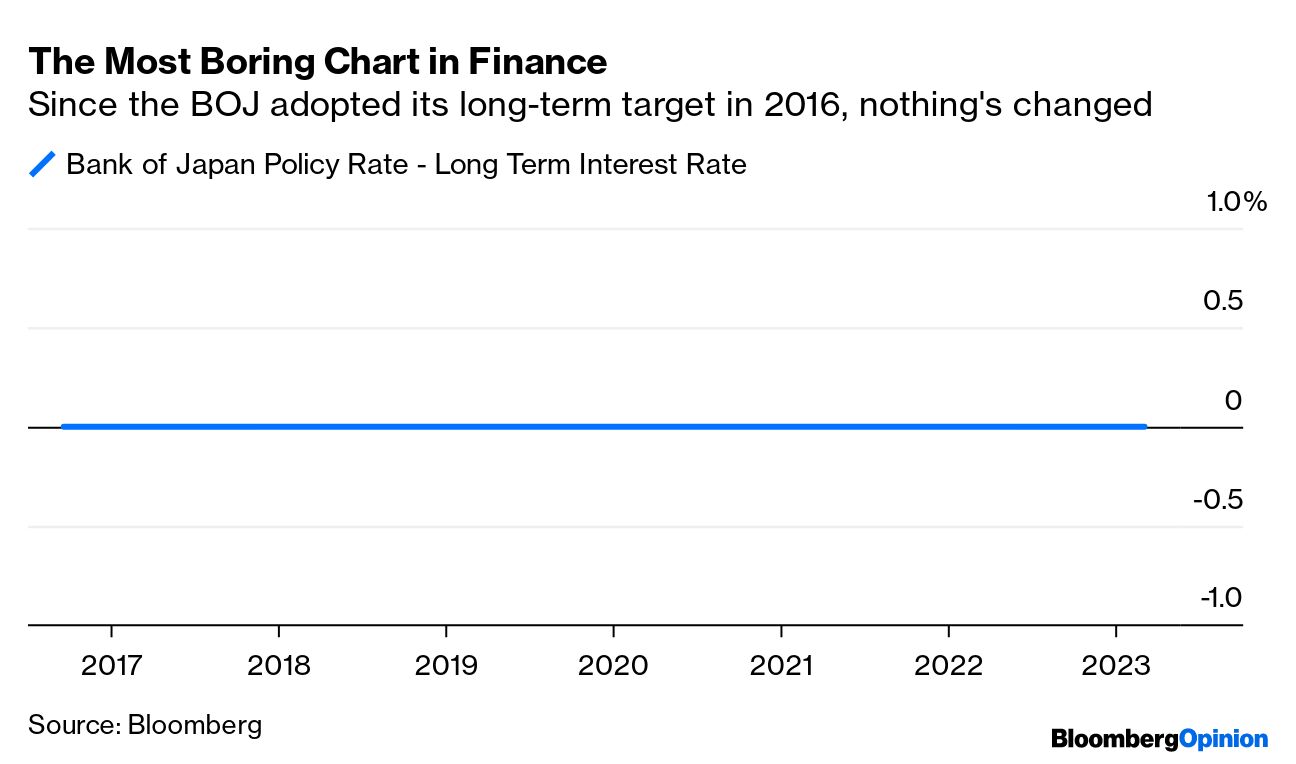

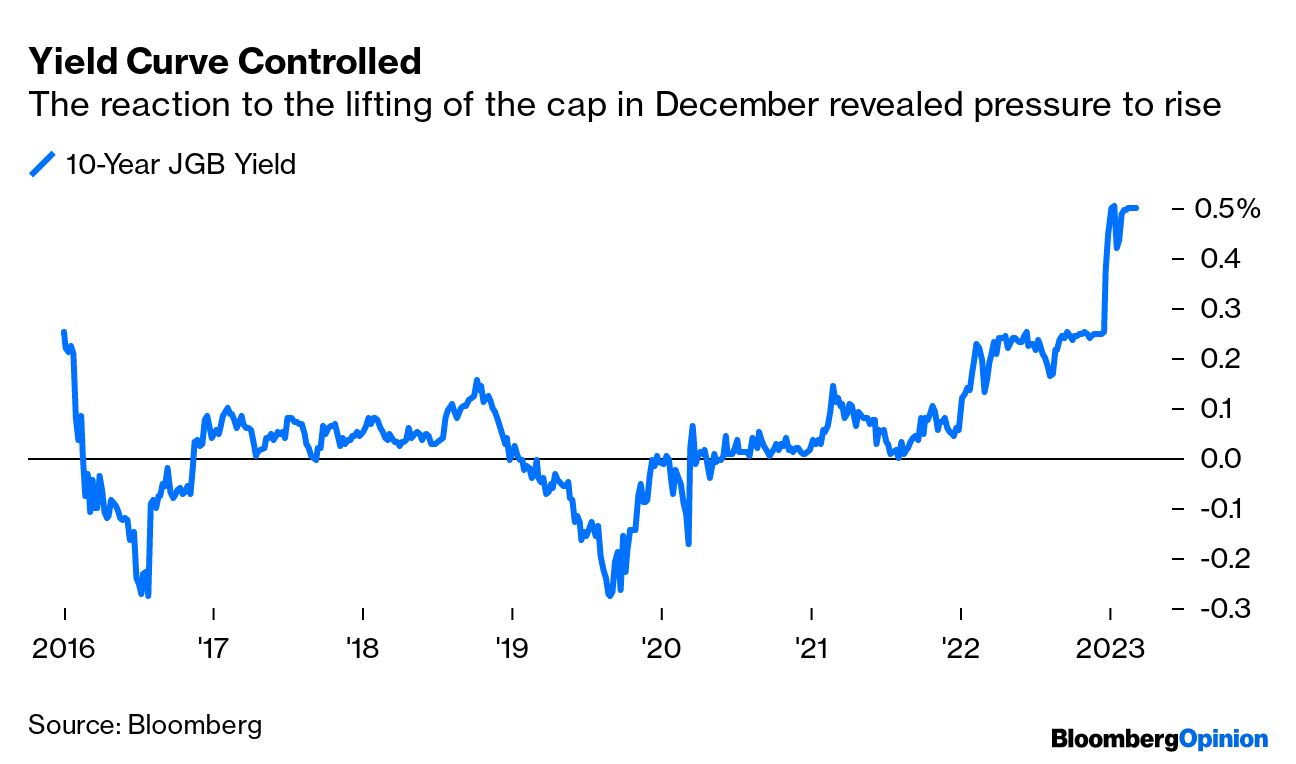

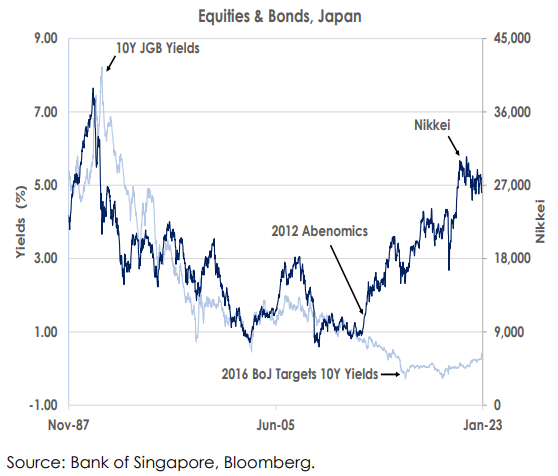

| It's far too easy to declare the end of an era, but in Japan it really looks as though momentous change is afoot. Later this week, a few hours before the US reveals February unemployment, Haruhiko Kuroda will preside over his last meeting as governor of the Bank of Japan. He has been a force of stability in a country that has arguably had too much of it, and his departure will require the world of finance to adjust some deeply held assumptions. The first concerns Japanification — the notion that the country fell into a deflationary morass, or liquidity trap, some three decades ago, and cannot escape. Core inflation has now risen just above 3%, which is high but still a rate that many countries would be glad to see. What's remarkable is that this is the highest since 1990, the year the nation's great asset bubble began to burst: If the absence of inflation can no longer be taken as a given, the same follows for monetary policy. There are plenty of important details to the BOJ's management of the money supply, but the bottom line under Kuroda has been of startling consistency. Since the 2016 inception of the current program of yield-curve control (buying 10-year bonds to keep their yield below a certain cap), the Kuroda BOJ has also published a long-term interest rate. Here it is: In the context of continuity like that, any shift at the margin can have a big effect. For proof, look at the way the bond market responded to the news in December that the 10-year yield cap would rise from 0.25% to 0.5%: Whatever else intervening in the yield curve might have achieved, it's been great for Japanese stocks, at least when they are valued in yen (the effect of lower yields on the strength of Japan's currency has counteracted some of this for international investors.) This chart is from Mansoor Mohi-Uddin, foreign-exchange strategist at the Bank of Singapore: Kuroda may not have shaken the Japanese economy back into life, but he has at least managed to revive the stock market. All of this entails that there is a risk of serious uncertainty and volatility once he finally leaves. Markets have grown used to endemic Japanese inflation, and to a mightily consistent hand on the rudder. Both these reassuring conditions have now been taken away. This doesn't mean that anything too drastic will happen this week. Hiroyuki Ueno, senior economist at SuMi TRUST says: Despite speculation of a reset in monetary policy, we do not believe that this will happen in the short-term. Prospective governor Kazuo Ueda has said that an accommodative monetary policy is necessary for the time being. It is interesting that he declined to specify whether the YCC policy will continue, but this is likely to change as the outlook for prices improves.

Another critical point of difference lies in the political environment. The BOJ is independent, but for years it was part of Abenomics, as Kuroda allied with long-serving premier, the late Shinzo Abe, on his attempt to break out deflation. There are many criticisms of Abenomics, but the vision was clear and well-communicated. The relationship between Ueda and current Prime Minister Fumio Kishida could be very different. This is summarized in a fascinating post by Tobias Harris of the Observing Japan newsletter: In the case of the former, you had a prime minister elected in part on the basis of his plans for macroeconomic policy and for the Bank of Japan in particular, the public at his back, and his party unified under his leadership. In Kuroda you had a Bank of Japan governor who was sympathetic to the prime minister's goals but had been a senior official at the Ministry of Finance and head of the Asian Development Bank, having the managerial experience and institutional relationships expected of a BOJ governor. The Kishida-Ueda relationship is different in almost all aspects. Kishida has been reluctant to outline a particular direction on macroeconomic policy (and has in fact been constrained by Abe's choices). The LDP is far from united, not least on fiscal and monetary policy questions, Kishida's base of support within the party is fragile, and his approval ratings have been in a prolonged slump. Ueda, meanwhile, has an unconventional background for a BOJ governor and has not managed a large organization, although of course is highly knowledgeable about monetary policy. Maybe the pragmatism of Kishida and Ueda is the appropriate quality for the BOJ's thorny problems — certainly preferable to either a dyed-in-the-wool reflationist or monetary hawk — but it's also possible that Ueda will be outmaneuvered by the other actors with a stake in the direction of monetary policy.

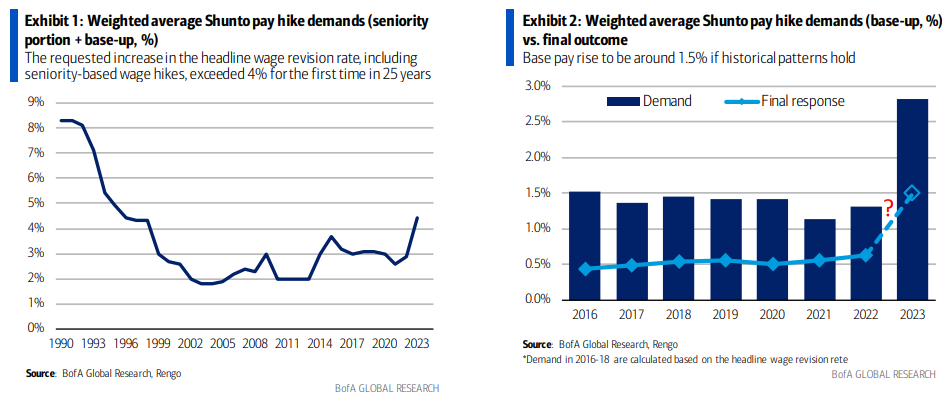

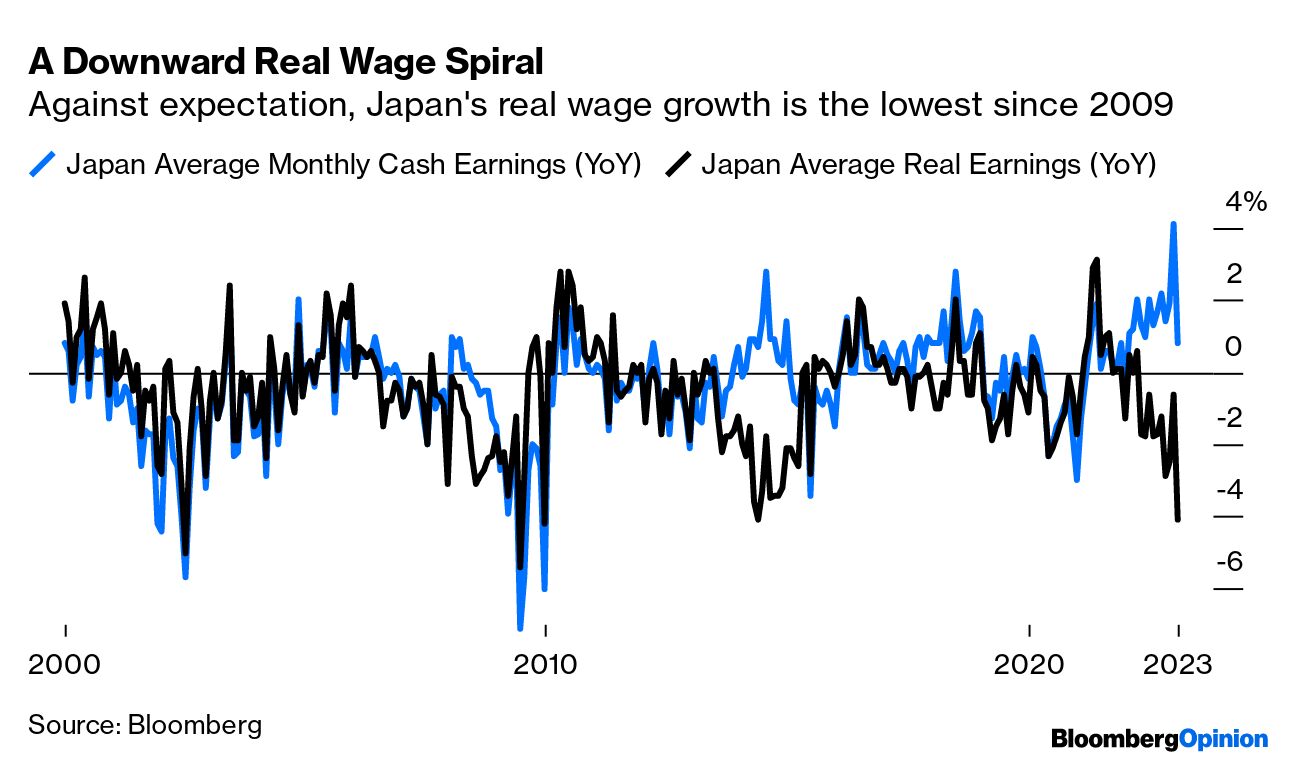

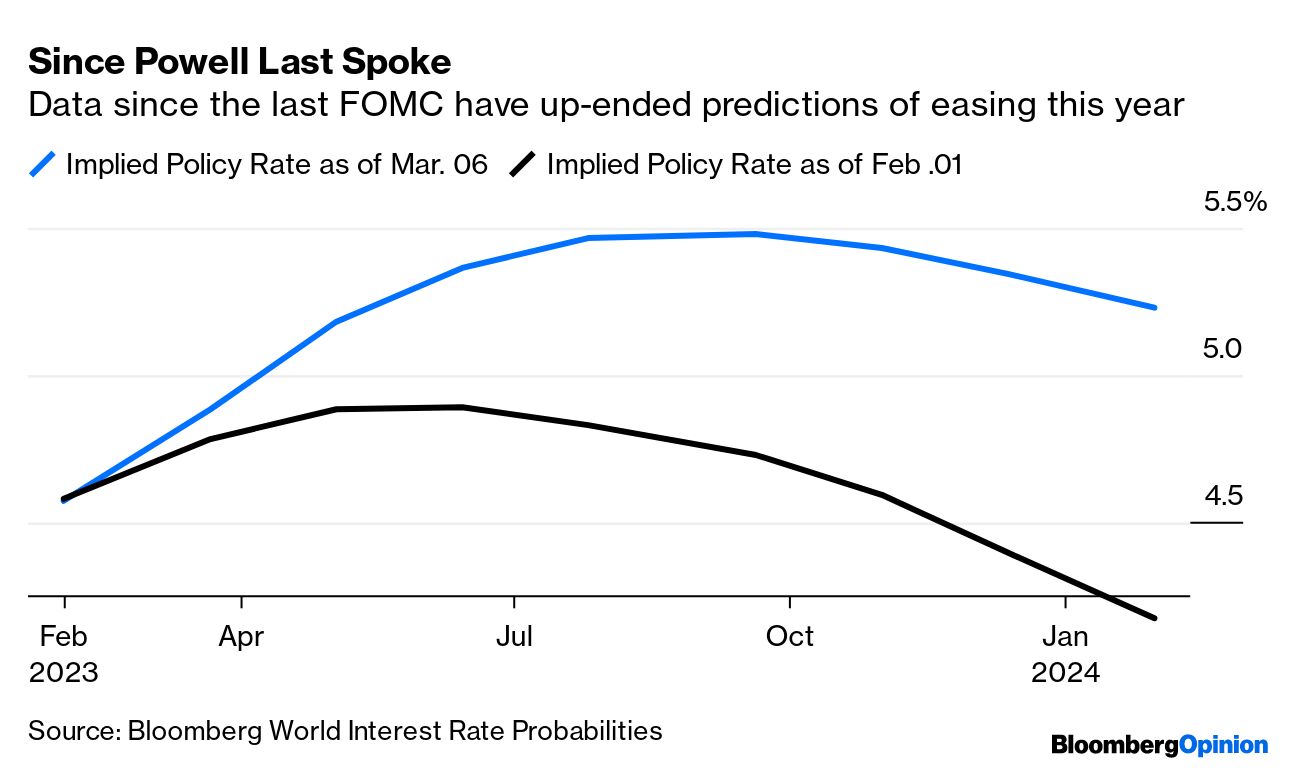

For a while, Japanese politics have been (relatively) simple, at least as they pertain to monetary policy. For the next few years, attempts to predict where the economy will go will have to incorporate guesswork on the political position, and on the personalities and priorities of two figures who are still very little known outside Japan. What, then, have we learned of Ueda's likely approach so far? Like any central banker, he has to keep his cards close to his chest, but he appears still to be on the side of what in the US is called "Team Transitory." He's not convinced that the rise in inflation will be sustained. Thus, he has said in as many words that the BOJ "needs to firmly support the economy with easing." As Mohi-Uddin points out, Ueda is on the record with the thought that "Japan's inflation is led by cost-push factors" and "it will still take time to achieve sustainable inflation." That suggests someone who's not going to make any sudden moves. As strategists prepare for Kuroda's last meeting in charge, there is unanimity that rates are not going to change, and near-unanimity that YCC will get through this meeting unscathed. There is also something close to unanimity that the yield-curve control's days are numbered, thanks to the sheer amount of money that the BOJ is spending on containing its intervention, and because there are deepening worries that the bond market is becoming unworkable. In Japan, trying to work out where the new central bank team sits on a spectrum from hawks to doves could matter a lot. But the data is also important. Wages are central to the possibility of a return to structural inflation. Japan's typical pay structure includes bonuses and much more flexibility than is typical in most other western countries, and so wages are not quite as sticky or difficult to cut as elsewhere. However, the evidence emerging from the annual "shunto" — a big wage negotiation between unions and employers — finds that workers are asking for the largest raise in base pay in 25 years. As the chart from Bank of America demonstrates, the unions don't get all that they want, but these kind of demands likely ensure a significant rise: Until now, it's been possible to attribute Japan's inflation to the rise in the cost of imports driven by the weak yen. Big wage increases would change that. This round could be the critical variable in determining just how Ueda proceeds in office. That said, the latest data, published Tuesday, show that wage growth isn't running as fast as had been thought. In cash terms, it touched the highest in decades at the end of last year, but the January figure was far lower. Real wages, accounting for inflation, are falling by the most since the crisis year of 2009: So Ueda will need to be data-dependent. And before the Kuroda era draws to a close, we will be hearing from the man charged with steering the Federal Reserve for at least another three years. Fed Chairman Jerome Powell is set to appear before Congress for two days to deliver the semi-annual monetary policy report on Capitol Hill. On Tuesday, he will be at the Senate Banking Committee and on Wednesday at the House Financial Services Committee. He will need to mind what he says. But the evidence of the last five weeks is that the economic data matter more to the market than any guidance from the Fed's chair as to how he might respond to them. Since he last spoke publicly, in his press conference after the Feb. 1 Federal Open Market Committee meeting, expectations for the Fed's likely course of action for the next year have been radically reshuffled. This is perhaps best illustrated using the World Interest Rate Expectations (WIRP) function from the terminal, which derives implicit expectations for the fed funds rate after each FOMC meeting from the futures market. After Powell's last big utterances, the market expected hiking to be over in the next couple of months, with rate cuts starting soon after. Now, the hikes are expected to continue perhaps as long as September. If there is any easing this year, the market now believes it will come very late, and won't be more than 25 basis points: This shift was driven almost exclusively by January's data, which were almost all hotter than expected. With inflation still way above target, Powell's testimony will come under even more scrutiny than usual. Investors are debating whether the Fed will hike by 25 basis points, or potentially be more heavy-handed (and implicitly admit that it had made a mistake in slowing down the pace of hiking) and raise by 50 basis points. The timing isn't ideal. There are still several major data releases before the March FOMC. These include the crucial February consumer-price index as well as the pivotal jobs report on Friday, the last before the Fed convenes in March. If they have as big an impact on the outlook as the last data points in those series, they will swamp anything Powell could say to Congress. In practical terms, that leaves him with little alternative but to stick to his script, acknowledging the firmer data while keeping his hawkish rhetoric — which investors are now more inclined to believe. Here is the view from Bloomberg Economics led by Anna Wong: Powell will seek to strike a balance between highlighting progress thus far in slowing inflation without job losses, while noting the FOMC has more to do as risks to the inflation outlook remain skewed to the upside... We'll be listening for indications of how Powell views the trade-off between achieving a higher terminal rate with urgency, versus keeping policy rates around 5.25% for longer.

Fort Jim Reid of Deutsche Bank AG, it's hard for Powell to be confident about where the Fed is going to land, although he might reveal something about the "reaction function." "He may provide clues as to what employment and inflation numbers need to do to make the Fed act in a particular way," he said, "especially how it pertains to whether 50 basis points hikes are back on the table." Bipan Rai, head of FX Strategy at Canadian Imperial Bank of Commerce, suggests that "the key to watch for is what he says about recent data and whether his views have evolved since last month." That data, as far as Ian Lyngen and Ben Jeffery of BMO Capital Markets are concerned, give Powell no choice but to be hawkish. He will also likely "prepare" Congress for a higher terminal rate and an extended period in restrictive territory: The Chair is certainly cognizant of this reality and, as such, the market is expecting an upbeat message on the state of the US economy and ongoing angst regarding the trajectory of inflation ... Progress on the inflation front, combined with the ongoing strength in the US economy is a recipe for reinforcing the 'more work to be done' mantra that has provided the unifying theme of Fedspeak throughout this year.

As for UBS Group strategists led Jonathan Pingle, Powell also needs to defend his policy: Price stability is the 'bedrock of our economy,' a phrase he has been using, is a start. Restoring price stability and the 2% inflation target is necessary for strong labor markets, he will probably again argue.

If Powell's contribution to the two-day event, which will be live-blogged by Bloomberg, looks predictable, the same can be said of the questions from politicians on these occasions. They are generally of no great use in discerning the course of monetary policy. But if there is a wildcard, it may not come from Powell but from Congress. Any pushback from lawmakers on the prospects for higher rates for longer and the risk of unemployment increasing is something to watch out for. While an angry faction among Republicans disputes the entire legitimacy of the Fed, progressive Democrats have been vocal on the prudence of prolonged restrictive policy, including Senators Elizabeth Warren, Sheldon Whitehouse, Jeff Merkley and Bernie Sanders. Warren, for instance, has expressed how Fed rate hikes have hurt lower income workers. On Wall Street, though, Powell has more allies — and not only among Republicans. One of them is President Bill Clinton's former Treasury Secretary Lawrence Summers who was fiercely critical of the Fed's slowness to act two years ago. Now, he is happy to support what appears to be a much more hawkish agenda. Last week, he told Bloomberg that the Fed "should have the door wide open to a 50-basis-point move in March." The door is open — but he will need more data before he's ready to kick through it. — Isabelle Lee In a moment of boredom, I tried watching 63 Up over the weekend. It's the latest and possibly final documentary in the series that has been revisiting a group of British youngsters every year since 1964. As Michael Apted, the ever-present director, has died since it was made, and all the participants will be 70 if there is a next installment, it might well be the last. This has been said many times before, but it's the most extraordinary and beautiful documentary ever made. It's no longer about the British class system and much more about life, and it's worth watching it if you never have. In the US, you can stream it on Britbox. To whet the appetite a little, you could read this great piece from The New York Times when 63 Up came out, along with the profile The Guardian published on the child who went on to have the most difficult and eventful life, Neil Hughes. After Apted died, this piece brought together what the participants thought of him and the way he had memorialized their lives. It's a world that's very much worth diving into. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. More From Bloomberg Opinion: - Stocks Aren't the Inflation Hedge You Think They Are: Merryn Somerset Webb

- We Now Know How Much the Coal Surge Set Us Back: Lara Williams

- Less Work Is Making People More Unhappy: Allison Schrager

Want more Bloomberg Opinion? OPIN <GO>. Or you can subscribe to our daily newsletter. |

No comments:

Post a Comment