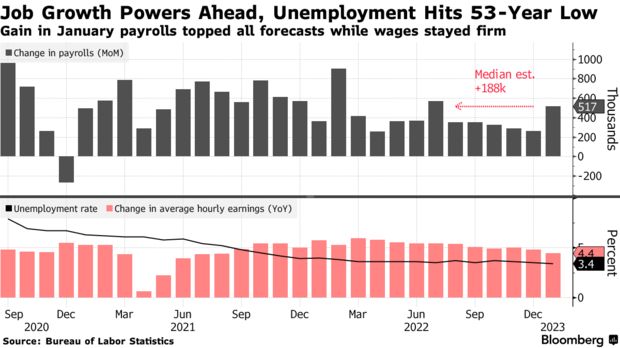

| Hello. Today we look at what strength in the US jobs market means for the Federal Reserve, the week ahead in global economics, and prospects for a wave of Chinese outbound investment. It took a while to land and only did so because Washington shot it out of the sky. What happened at the weekend to China's alleged spy balloon may now be the fate that awaits the US economy unless it soon starts deflating. The year began amid fears of a looming recession only for those to subside, if not completely disappear, as China reopened and Europe enjoyed a warm winter. That raised hopes of a "soft landing" in which the world's largest economy slows enough to restrain inflation, yet does so without a spike in unemployment. Now there's talk on Wall Street of a "no landing" after Friday's news that unemployment had fallen to the lowest since 1969 and a gauge of services advanced the most in almost three years. What that all means for households is detailed here by Reade Pickert and Olivia Rockeman. Consumers are "certainly on better footing than we or anyone thought just a few days ago," said Tim Quinlan, senior economist at Wells Fargo. "If hiring remains strong, and inflation continues to go from high and rising to high and falling, then there's an increasingly viable path toward a soft landing, where real consumer income is driving spending rather than a drawdown of saving."

That sounds like great news for companies and workers. But it may not be completely welcome at the Federal Reserve and thus for financial markets. To Torsten Slok at Apollo Management, such a backdrop suggests the economy might avoid a downturn, yet not fade enough to cool price pressures. "Under the no landing scenario the economy does not slow down, and upside risks to inflation are coming back after the initial decline in inflation driven by supply chain improvements," Slok said in a report.

That will unnerve the Fed, which remains focused on pulling back inflation even if that means higher interest rates. The Fed last week raised its key rate again, but did so by just a quarter point — a slower pace than the frenetic hikes of last year. Chair Jerome Powell also warned of further increases to come, a message hawkish markets seemed to ignore as they focused on him welcoming signs of disinflation. Investors even began pricing in rate cuts for the later in the year. As with the balloon, however, if the economy remains above the clouds, policymakers in Washington will need to bring it back to earth. Writing following Friday's data, economists at JPMorgan Chase said they see "material risk" the Fed will need to raise rates "well above" what markets are expecting. They reckon Powell will at least add two more 25 basis point increases in March and May. For investors "the no landing scenario is negative," said Slok. "Higher rates for longer increases the downside risks for equities and credit," he said. "In short, the no landing scenario brings back the volatile market action we saw in 2022 because it reintroduces uncertainty about inflation and about the Fed."

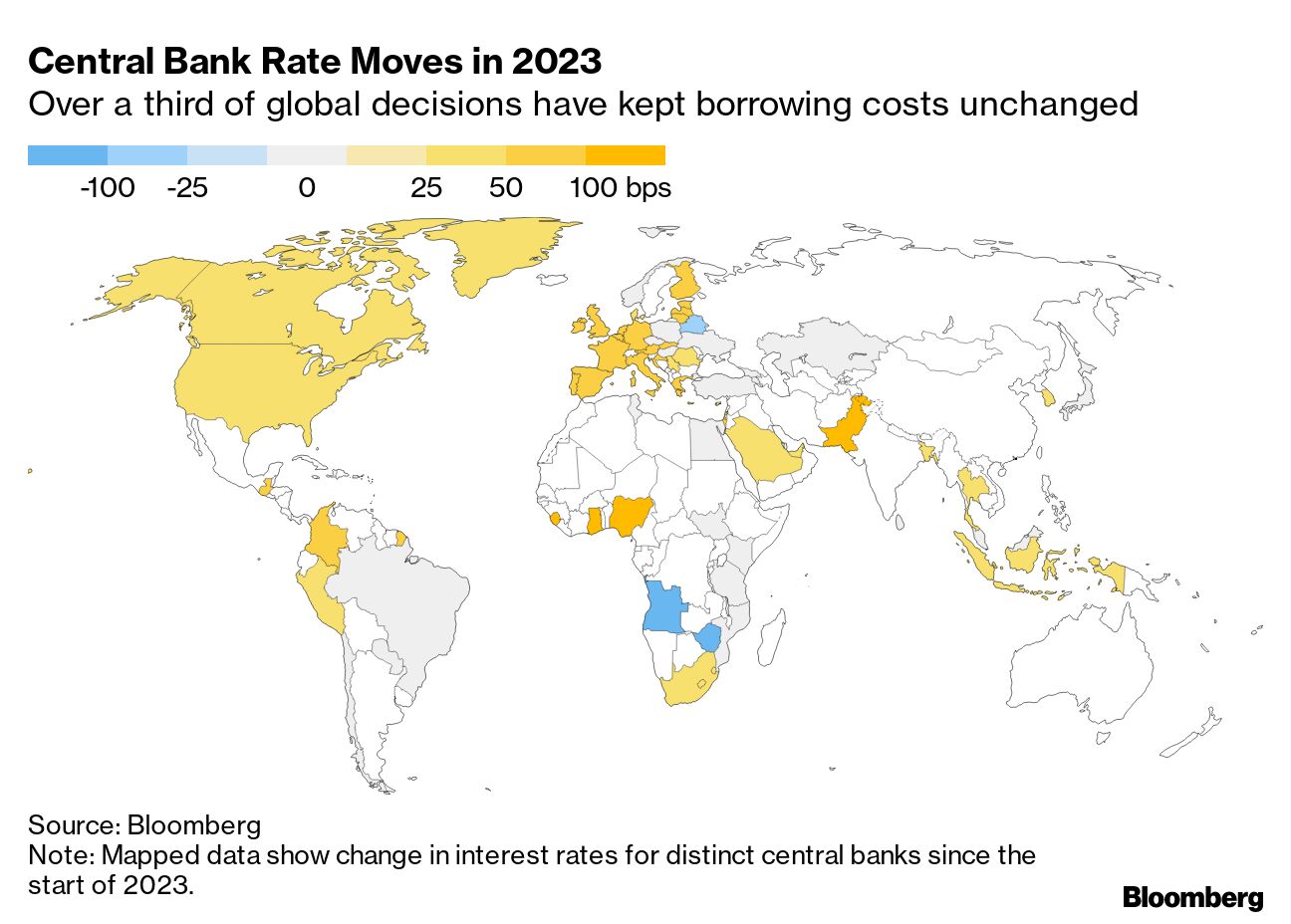

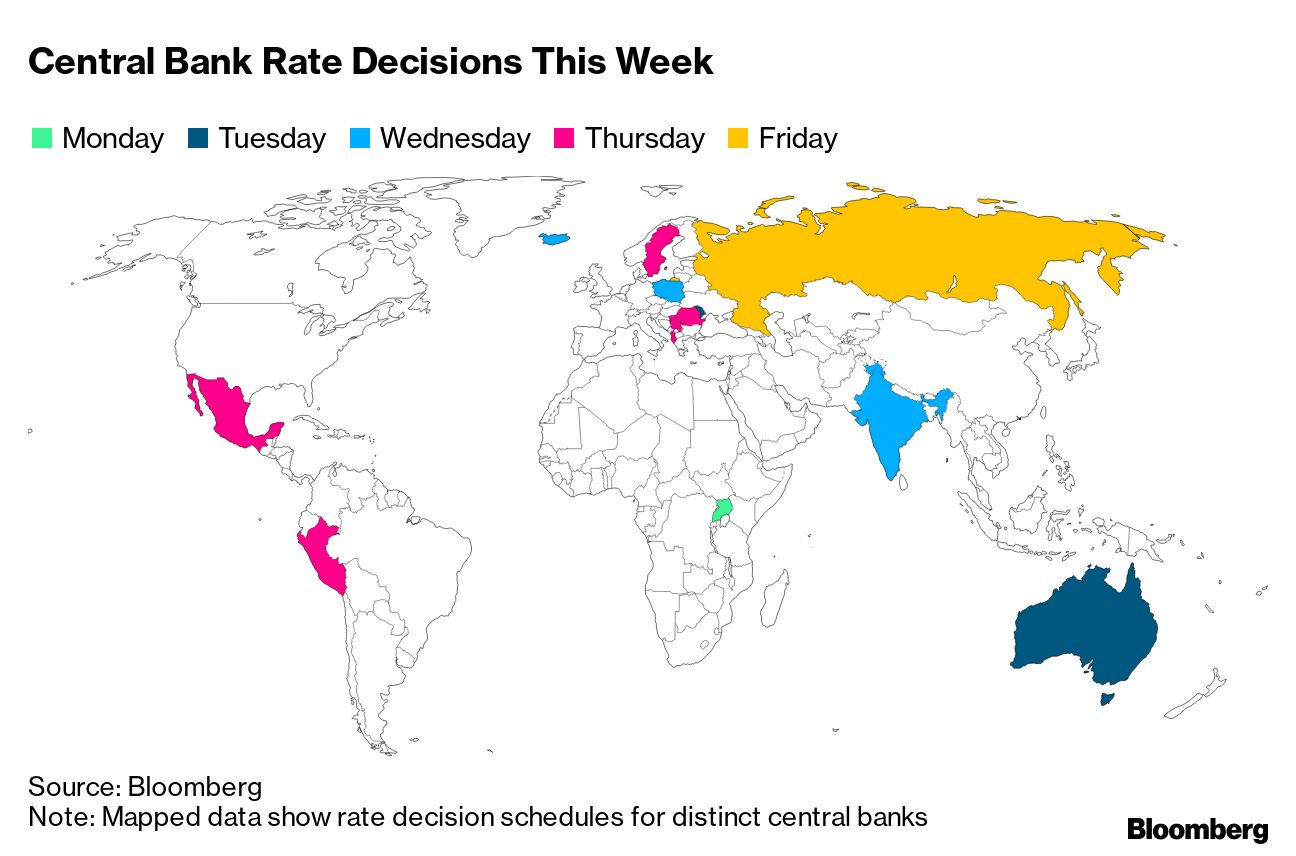

—Simon Kennedy A dozen more central banks are set to follow the Fed in proving less enthusiastic about rate hikes. The Reserve Bank of Australia on Tuesday and Reserve Bank of India on Wednesday are both expected to deliver quarter-point hikes, which may mark their final salvos. Poland's central bank has already halted rate increases and will probably ratify that view on Thursday, while its Romanian counterpart may decide to do the same. Mexico's central bank, while still determined to act against inflation, may deliver only a quarter-point increase — its smallest move since 2021. Still, Icelandic policymakers may increase their benchmark by 50 basis points on Wednesday, possibly echoed by Sweden's Riksbank on Thursday. Meantime, Chair Powell will speak on Tuesday and may provide greater insight into his thinking. A new Bank of Japan Governor may also be named. See here for the rest of the week's economic events. - BOJ boss | The Japanese government has approached Bank of Japan Deputy Governor Masayoshi Amamiya about succeeding Haruhiko Kuroda at the helm of the central bank, according to a Nikkei report that the government later denied. Here's what analysts say that could mean.

- Trade tiff | Joe Biden's clean technology law has dragged the European Union into a subsidy fight that may trigger a transatlantic trade war.

- AI in Argentina | Argentina, which for decades tried to beat runaway inflation with unorthodox policies, is now using a new tool to keep track of price increases: artificial intelligence. Meanwhile a survey shows most economists and traders don't see AI as a threat anytime soon.

- Lula tensions | Brazil's Luiz Inacio Lula da Silva was dismayed by a harsh statement published by the country's central bank, a signal that tensions between monetary policymakers and the president linger.

- Factory boost | German factory orders grew more than anticipated in December in the latest sign that Europe's largest economy will get through the winter without seeing a slump.

- Adani concern | Indian officials stepped in over the weekend to calm nerves over concerns turmoil surrounding billionaire Gautam Adani's conglomerate would spill over into the local economy and affect global investor sentiment toward the country.

- IMF warning | A US debt default would cause a spike in borrowing costs that squeezes American consumers and significantly harm the world economy, the head of the International Monetary Fund said.

- Don't let up | Bank of England policy maker Catherine Mann urged colleagues to "stay the course" and carry on raising rates as markets bet on the approaching end of their hiking cycle.

A tsunami of US dollars may be about to hit any number of markets across the globe, Louis-Vincent Gave, co-founder of Gavekal Research, wrote in a recent note to clients. Gave posits that Chinese business executives have effectively been building up a dollar cash hoard, having had limited options to spend surpluses from exports to the US during China's Covid Zero restrictions of recent years. It could explain the mystery surrounding the surging US current account deficit since Covid hit. In the past, deeper deficits were accompanied by a sliding dollar, and a big buildup in foreign holdings of dollars deposited at the Federal Reserve. But those things didn't happen last year. Now those funds — some held offshore — are mobile, they could end up in anything from Singapore and Dubai real estate to Chinese equities, he said. Or it could be converted to euros for use in Europe, he added. White House economists on the move… Read more reactions on Twitter here and here |

No comments:

Post a Comment