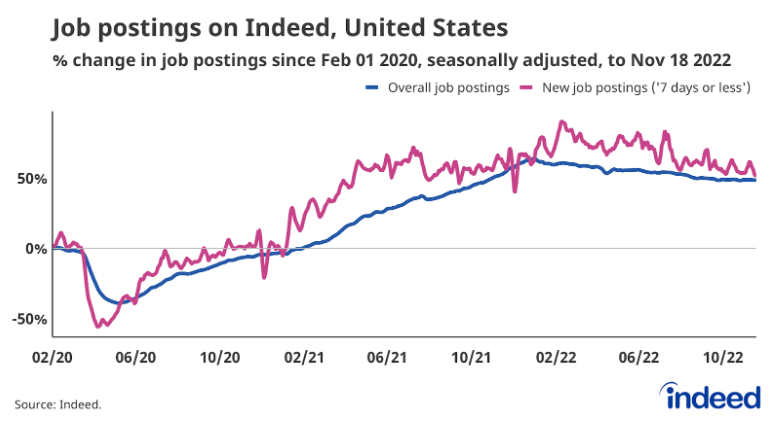

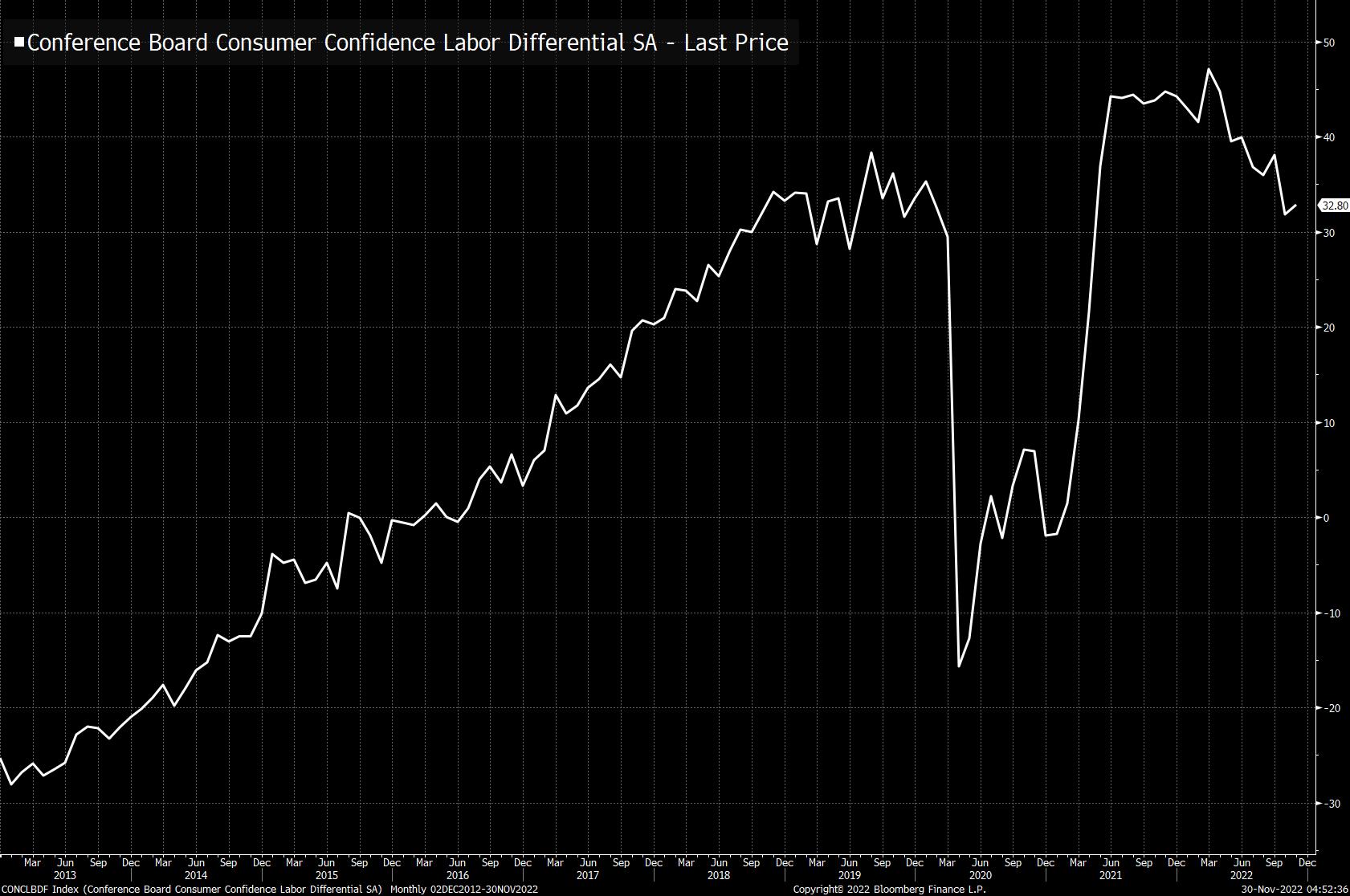

| China grapples with Covid consequences, Fed's Bullard calls for more rate hikes and the world's debt balloons to trillions. China's top law enforcement body pledged to crack down on "hostile forces" and their "sabotage," comments that appear to be intended as a warning to protesters. While officials have refrained from acknowledging the unrest, health authorities struck a conciliatory tone on Tuesday, saying that people's "reasonable" concerns must be resolved in a timely manner. Meanwhile, economic activity contracted further in November amid a record Covid outbreak, with growth likely to remain weak and the central bank expected to add more stimulus to bolster the recovery. Meanwhile, Jiang Zemin, the Chinese leader who presided over more than a decade of dramatic economic growth following the bloody Tiananmen Square crackdown in 1989, has died. Ahead of remarks by Federal Reserve Chair Jerome Powell later, St. Louis Fed President James Bullard repeated his call for additional rate hikes to a level that will restrict economic growth. In an article posted online on Tuesday, Bullard said estimates show a rate of at least 4.9% would be needed. Fed officials have signaled they plan to raise their benchmark rate by 50 basis points at their final meeting of the year on Dec. 13-14, after four successive 75 basis-point hikes have lifted it to a 3.75% to 4% target range.  | Total debt by households, businesses and governments stands at $290 trillion, according to research by the Institute of International Finance, and many borrowers now face a relentless increase in interest payments as the Fed and other central banks raise rates at the fastest pace in decades. Rising interest costs are "a slow-moving train for consumers and companies, just like for governments," says Sean Simko, global head of fixed-income portfolio management at SEI Investments Co. "At some point you are going to be watching it slowly creep up. And then all of a sudden it's going to be in your face. And then it's going to be too late." US equity futures climbed, with S&P 500 contracts gaining 0.2% and Nasdaq 100 futures rising 0.4% as of 5:31 a.m. in New York. The dollar traded near its lowest levels of the day, boosting most Group-of-10 currencies. Treasuries were little changed, diverging from declines in global bond markets. Oil, gold and Bitcoin climbed. How high can the Fed hike before crashing the credit market? What are the best investment opportunities in corporate bonds? Let us know, fill out the MLIV Pulse survey. All eyes will be on Powell when he's due to speak at 1:30 pm. Before that, we'll get mortgage applications data at 7 a.m. That will be followed by ADP employment data at 8:15 a.m., then figures on trade and wholesale inventories 15 minutes later. At 10 a.m., data on pending home sales and the JOLTS report will be published. Fed speakers apart from Powell include Governors Michelle Bowman and Lisa Cook. Here's what caught our eye over the past 24 hours: It's Jobs Week. On Friday we get a fresh reading of the Non-Farm Payrolls report, where economists are looking for 200K new jobs and for the unemployment rate to hold steady at 3.7%. In the meantime, today we get the October JOLTS report (always interesting stuff in there) and tomorrow we get Initial Jobless Claims, which have been trending up a bit over the past two months (though the actual numbers are quite low). There's two related labor market questions right now, as they relate to the Fed and inflation. One is still, whether we need sustained weakness (layoffs) in order to see inflation come down. The second question is whether we can have a modest rise in the unemployment rate, or whether a modest rise will inevitably turn into a substantial rise. As economist Tim Duy noted on Twitter yesterday, there's no historical precedence for the unemployment rate to just edge up modestly. Once it gets going, it gets going. All that being said, in the meantime, the data does look like cooling or softening, but not outright freefall. Yesterday, Nick Bunker at Indeed.com posted a bunch of charts that all kind of show the same story. Things aren't as hot as they were earlier this summer, but almost every indicator is still good by historical standards. So here for example, new job listings posted to the website are below where they were at the start of the year, but still well above the pre-pandemic baseline. Meanwhile, yesterday we got the latest reading of the Conference Board's "Labor Differential" index. It's just a survey measure that asks people whether jobs are plentiful or hard to get. And the higher the number, the wider the gap between the two groups. This number has come in since early this year. But it's still around 2019 levels, and also it actually ticked up a little bit last month. So for the moment (knock on wood and all that) we're seeing some cooling, but actual activity remains consistent with a strong labor market. Follow Bloomberg's Joe Weisenthal on Twitter @TheStalwart |

No comments:

Post a Comment