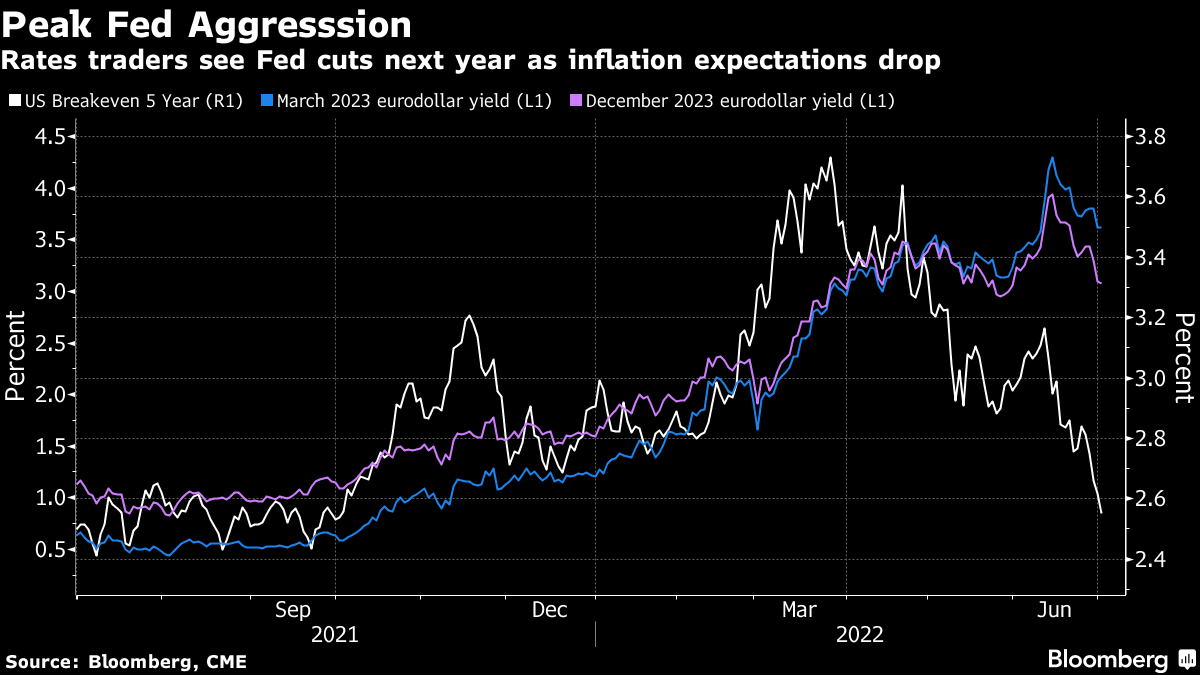

| Welcome to the Weekly Fix, the newsletter that sits back to enjoy the roller coaster ride in yields. I'm Bloomberg's chief rates correspondent, Garfield Reynolds. This was the week when bond investors piled back in as expectations grew ever stronger that central bankers will hike interest rates fast enough and high enough to cool inflation. And that they will cause recessions in the US and elsewhere in the process. Treasury 10-year yields that came within a whisker of topping 3.5% in mid-June for the first time in 11 years dropped back under 3% by Thursday. The zeitgeist was captured by Bob Michele, JPMorgan Asset Management's chief investment officer, who said the outlook now is worse than it was when he kicked off his Wall Street career during the stagflation crisis of the early 1980s. The backdrop to all this was a clarion call from the major central banks that, outside Japan, large and rapid rate hikes will keep coming. Federal Reserve Chair Jerome Powell, meeting in Sintra, Portugal with his international peers, led a requiem for the era of low inflation. The bond market moved rapidly to price in an end to hiking cycles, with the Fed now seen cutting rates by half a point over the second half of next year. And even as policy makers fretted inflation is here to stay, markets started betting that the "Great Inflation Trade of 2022" was done and dusted. The extraordinary shifts in bond prices that sent yields gyrating also underscored concerns that trading conditions are getting rough enough to distort markets. With central banks sitting on large parts of their own markets and a wave of post-crisis regulations aimed at de-risking banks, there's growing concern that patches of illiquidity are helping to add volatility to an already difficult environment. The $23 trillion Treasuries market remains vulnerable to meltdowns and the Fed needs to move more rapidly to help fix the problem, according to a panel led by former Treasury Secretary Timothy Geithner. Some asset managers are already saying they are in danger of being trapped in bond positions because some of the biggest traders are turning gun-shy. Massive losses across markets this year mean some traders are refusing to buy or sell with clients at all if it means the traders will have to hold the bonds even for a short while. The European Central Bank meantime faces a particular conundrum as it moves to raise rates — the specter of last decade's sovereign debt crisis is haunting the bond market there already. Bonds are swinging around in Europe at the wildest pace in decades. And the region's corporate borrowers are ditching plans to sell bonds amid massive market losses and volatility. Japan faces difficulties of its own — the Bank of Japan's determination to chart an uber-dovish course in a world of hawks is roiling markets there. Looming over it all is the return of a classic widow-maker trade, as investors from around the globe line up to bet that BOJ Governor Haruhiko Kuroda will be forced to abandon the 0.25% cap on 10-year JGB yields. Bond futures liquidity evaporated as a result of the BOJ's massive bond purchases. At least bond traders in Japan are finding they are again in demand amid all the volatility. None of the turmoil has made it any easier for those who hold the debt of developing economies. Asia's biggest currency rout since the days of the 1997 financial crisis is putting the region's central banks, and bond traders, in a bind. Sri Lanka and Pakistan are in talks with the International Monetary Fund as they try to go on servicing a combined $66 billion of debt. China's high-yield bonds also remain under stress, with China Great Wall Asset Management Co.'s missed deadline for its 2021 annual report renewing concerns about the health of the nation's state-controlled bad debt managers. Asian junk bond investors are therefore looking to smaller pockets of the region's markets — such as India and Southeast Asia. Russia finally ended up defaulting on its foreign bonds, leaving investors in the notes caught in the web of international sanctions imposed on the nation after it invaded Ukraine. Speaking of Ukraine, it is reportedly exploring the possibility of debt restructuring as the war-ravaged country's funding options are at risk of running out. Argentina is in better shape after it sold enough securities to roll over debt coming due in June, calming markets somewhat after local yields topped 70% earlier in the week. Korea's bond investors think rates traders overpriced central bank hikes Alabama trimmed a prison-bond deal because of weak demand UK to guarantee $2 billion of African debt to help finance climate projects |

No comments:

Post a Comment