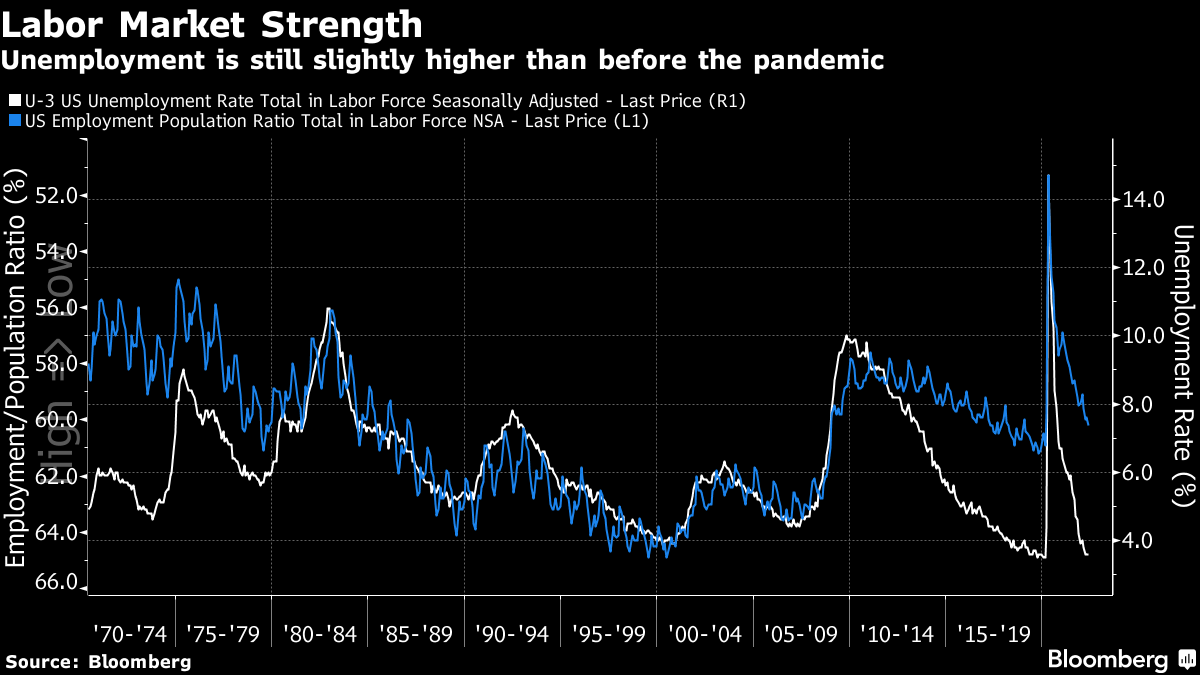

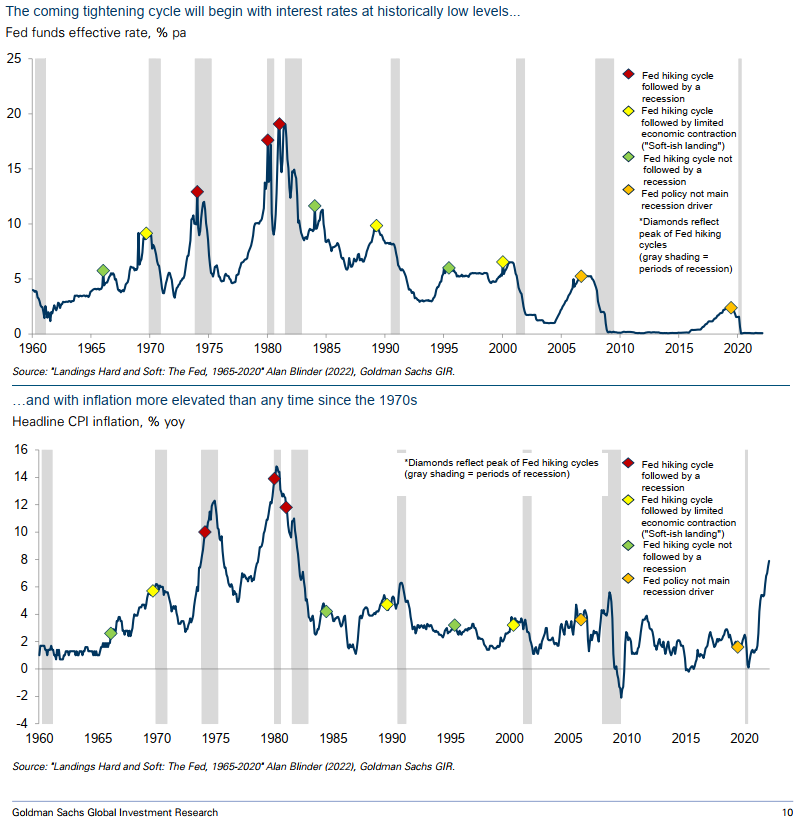

| What are the chances of an economic soft landing? A month ago, I likened this to Captain Chesley Sullenberger's heroic landing of a passenger jet on the Hudson River; possible, but very, very difficult. Since then, predictions of a hard or crash landing have proliferated, from people as distinguished in the financial world as Jamie Dimon of JPMorgan Chase & Co., who predicts an economic "hurricane"; Elon Musk of Tesla Inc. who has a "super bad feeling" about the economy; Larry Fink of BlackRock Inc., who sees "elevated inflation for years"; and John Waldron, president of Goldman Sachs Group Inc., who warns of an unprecedented "confluence of the number of shocks to the system." Despite all this, the glide path to a soft landing may be very slightly easier than it was a month ago. To bring down inflation without crashing the economy, we need to see data grow steadily less positive without plunging through the floor. Another month on, and it still looks possible. The latest ISM supply manager surveys suggest that the services sector has cooled significantly. But both manufacturing and services remain comfortably above the 50 level that marks the difference between expansion and recession: The employment market is still red-hot but its behavior is arguably consistent with economic policy makers eventually making a soft landing. Friday's US employment numbers were slightly stronger than expected, but showed growth slowing slightly. Employment has surged back since the pandemic, but whether we take the "headline" unemployment rate, as a proportion of those officially making themselves available for work, or the broader measure of the working-age population who are in jobs, employment levels are still a little lower than at the beginning of 2020:  Within the unemployment data, the most consequential numbers for the future of inflation concern earnings. The great fear of the Federal Reserve is to avoid a wage-price spiral, in which higher salaries raise costs and boost demand for products, thereby driving up prices. Year-on-year growth in average earnings is still above 5%, but it's dipped a little for the second month in a row. These numbers are still just about consistent with an eventual soft landing:  According to Mark Haefele of UBS Global Wealth Management, this picture "is still consistent with our view that inflation will decelerate but remain above central bank targets, economic growth should slow below trend growth but remain above zero, and markets will end the year higher." That's roughly what people mean when they refer to a soft landing, although if inflation is not decelerating enough by the end of the year, there would still be the possibility of further Fed hikes beyond what have been priced in. All of this is consistent with many more months of difficult trading, in which value stocks and defensive sectors make most sense. But if what's happened so far is consistent with a relatively benign soft or "soft-ish" landing, to use Jerome Powell's phraseology, how likely is it? Hard landings tend to come after the Fed has hiked. In general, economic fine-tuning is difficult, so this isn't surprising. But Alan Blinder, the Fed's former vice chairman, made a presentation called Landings Hard and Soft, in March this year that argued there'd been quite a few soft or at least soft-ish landings. The following charts based on Blinder's material were published by Goldman Sachs, shortly before the current tightening started: A positive take on this is that a Fed tightening cycle hasn't ended with a serious recession since the Age of Paul Volcker. The negative way to look at it is that all the cycles that ended without a hard landing happened with inflation significantly lower than it is today. Indeed, inflation is now very close to the levels at which the Fed has felt obliged to crash-land the economy in the past. All that said, Blinder's presentation, which can be found here, arrives at this positive conclusion: - Seven of the eleven episodes were arguably "pretty soft" landings: 1965-66, 1967-69, 1983-84, 1988-89, 1994-95, 1999- 2000, and 2004-06.

- In three other cases, there was never any intention to make it "soft": 1972-74, 1977-80, 1980-81.

- In 2004-06 and 2015-19, it certainly wasn't tight money that caused the deep recessions that followed.

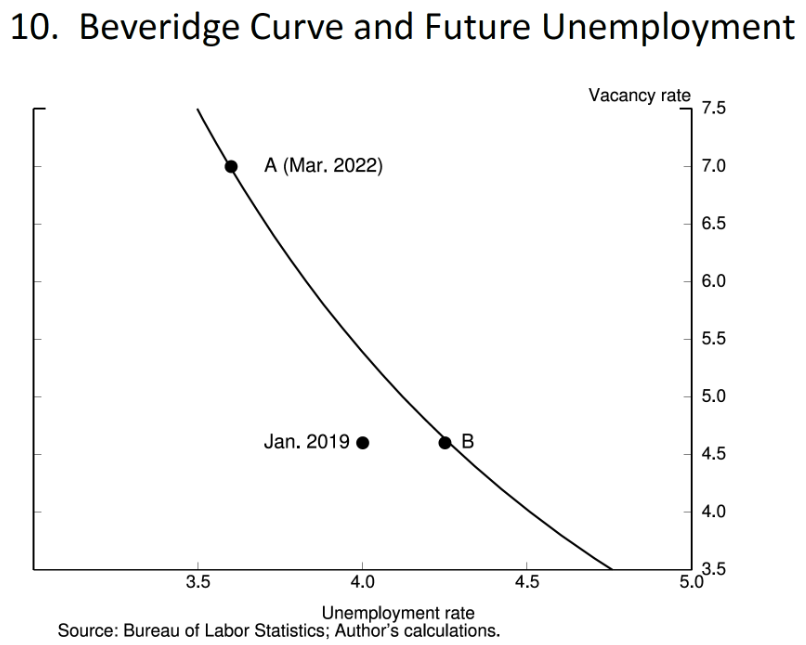

So soft landings can't be all that hard to achieve. I might draw some caveats. In 2004-06, the gradual tightening by the Greenspan Fed has been criticized (fairly) for being too steady, and not shaking investors out of the massive leverage that was building up, particularly in subprime mortgages. Once 10-year bond yields briefly topped 5%, a year after the tightening, the credit structure started its epic collapse. So it's true that this tightening didn't directly cause the 2008 crash — but an earlier and more aggressively executed policy might have led to a "soft-ish" or even "hard-ish" landing that would still have been much preferable to the Great Recession. The tightening of 1999-2000 led to a "pretty soft" landing (the recession that followed the bursting of the dot-com bubble), but there's an argument that a tougher approach and an earlier harder landing amid the fallout from the Asian and Russian crises in 1998 might have served the world much better in the longer run. The broader point is fair enough, though. There have been a number of Fed tightening episodes over history that didn't end in a crash or even a hard landing. Will the Fed be able to stop hiking before it has inflicted damage on the economy? Judging by one major Fed speech last week, central bankers believe they still might be able to do this, although it's possible they'll be forced to go further. Don Rissmiller of Strategas Research Partners finds the Fed's likely strategy in last week's much-discussed speech by Governor Christopher Waller. He describes the following chart from Waller's speech as "the skeleton key for understanding "peak inflation," the chance of a Fed pause, and the odds of policy-induced recession." Here it is: For those interested, the curve is named after William Beveridge, a British liberal (as opposed to Labour) economist and Oxford academic, who is famous chiefly for drawing up the wartime "Beveridge Plan" which laid out the economic building blocks of the postwar welfare state. A great and respected figure, his is still an unlikely name to pop up when charting a course for US monetary policy in 2022. The key, as summarized by Rissmiller, is that Beveridge provided a way for the Fed to look at the unemployment rate and how much of an effect it can be expected to have on inflation. Beveridge noted that when unemployment is low, it grows harder to generate vacancies. That leads to the idea that by knocking the top off companies' appetite for expansion, vacancies will come down a lot, but unemployment needn't rise so much. In terms of the graph, Waller would like to get from A, where we are now, to B, somewhere like January 2019 but with slightly higher unemployment. As Waller put it: "[t]he unemployment rate will increase, but only somewhat because labor demand is still strong – just not as strong – and because when the labor market is very tight, as it is now, vacancies generate relatively few hires. Indeed, hires per vacancy are currently at historically low levels. Thus, reducing vacancies from an extremely high level to a lower (but still strong) level has a relatively limited effect on hiring and on unemployment."

This is important to the central bank because it has some degree of control over the US labor market, while other inflationary forces are beyond its reach. To quote Rissmiller: US inflation has surged due to goods bottlenecks, but these are expected to reverse. A key problem is that services inflation (which is "stickier" and ~60% of the CPI) is starting to move higher. Goods inflation is set by global factors. Services inflation is set by the domestic labor market (i.e., wage increases). So the central bank's key concern about lasting inflation ties closely to the overheating labor market. Waller has given us a way to monitor how the Fed is thinking about this labor equation, and thus a way to think about services inflation

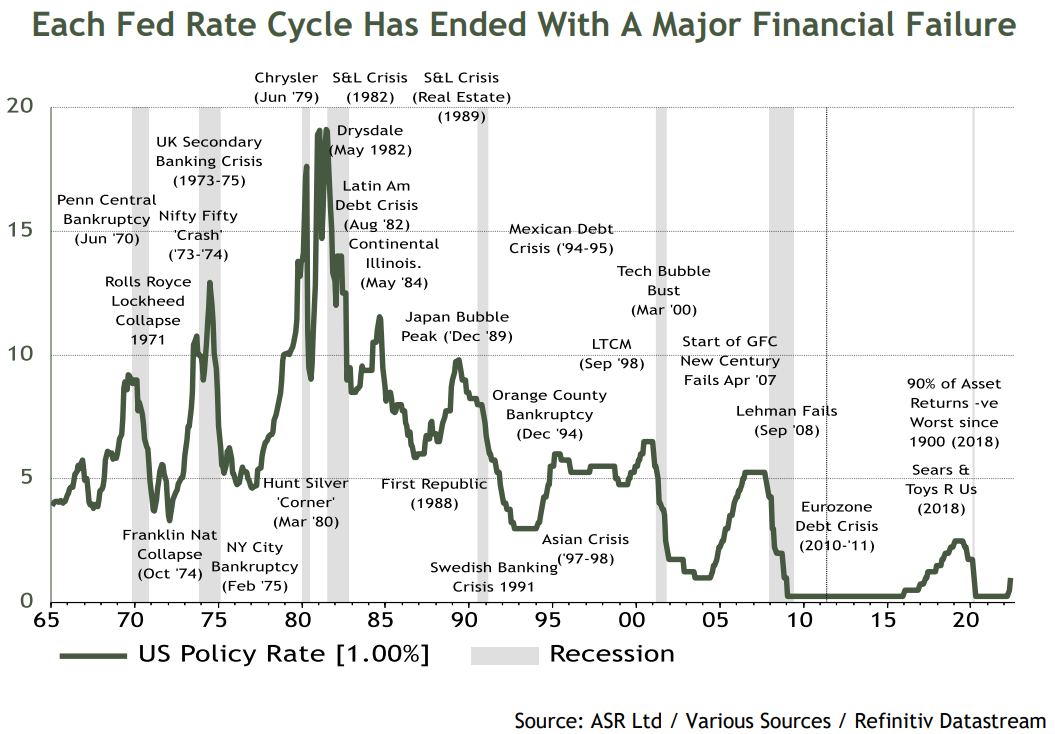

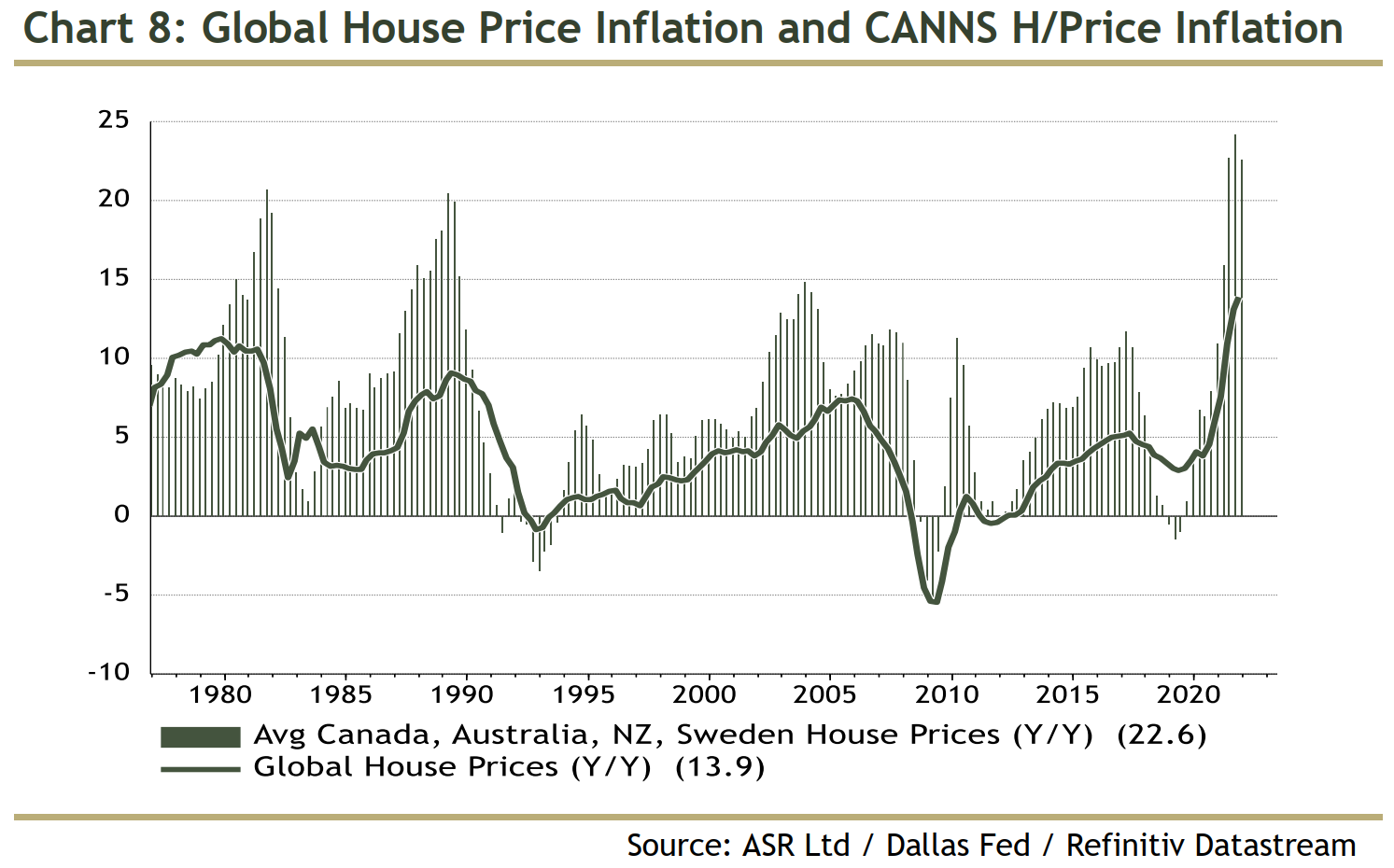

If vacancies begin to decline without any significant deterioration in the unemployment rate, that should embolden the Fed to keep hiking in line with current expectations, in the belief that a soft landing is possible. If the unemployment rate rises sharply, then the risk of a recession and a reversal by the Fed grows greater; and if employment remains high, the risks of eventual stagflation grow that much greater. So far, with vacancies down a little and unemployment stabilizing, the Beveridge Curve analysis suggests a soft landing could still happen.  | What are the problems with this? If interest rates can rise without directly crashing demand, there remains a risk that they can trigger a financial accident bad enough to create a recession. This would fit the model of the two worst US recessions of the last hundred years, the implosions of 1929 and 2008. As shown in the following chart produced by Ian Harnett of Absolute Strategy Research Ltd. in London, a Fed hiking cycle more or less invariably ends with a financial failure of some magnitude:  Lightning almost never hits in the same place twice, or at least not twice in a row. At different points in history, crises have afflicted the UK secondary banking system, Wall Street investment banks, emerging market debt, large industrial groups, or the sovereign debt of euro-zone countries. In the typical pattern, the sector that causes the crash is rescued at great expense, and then regulated in a way that makes sure it won't crash again. Then, financial engineers get to work, and risk and leverage move elsewhere. When the Fed next starts to hike rates, we discover that leverage has gone just where regulators should instead have been focusing their attention. Thus, following the experience of Long-Term Capital Management's meltdown in 1998, many waited in 2008 for a hedge fund collapse that never happened. Emerging market debt proved much more robust than in other hard landings — and then it grew clear that the crisis had instead had a ruinous effect on sovereign debt in the euro zone. Where to look this time? Harnett suggests that obvious candidates include housing markets, particularly in a group of smaller and relatively prosperous economies that have done well out of the commodity market of late — Canada, Australia, New Zealand, Norway and Sweden. Those economies reinvested heavily in property. Global house price inflation is already at records, but in those countries it looks extreme. As they're mostly regarded as safe places to invest, that means the fallout from a housing bust could be that much worse:  Beyond that, dollar appreciation — which should continue with rising US rates — threatens the pile of US dollar-denominated debt around the world. And the rise of the non-bank financial sector, particularly in the US, has seen a group of companies take a big share of markets, particularly in mortgage-lending and in crypto. They can be nimble because they aren't as heavily regulated as banks. In a crisis, we might start to wish they were regulated more tightly. The very bearish Absolute Strategy conclusion is as follows: The last nine US rate cycles, since the 1970s, have all ended with significant financial failures. We doubt this cycle will be different. What is less clear is whether it will be in US credit, US dollar denominated debt in EM economies, or a housing issue in the CANNS or the US. The key risk for us, however, is in the new entrants to the non-Bank Financial Services space. These companies have untested business models and are large enough to create potentially systemic risks for policy makers. This could get very ugly,

meaning that it is too soon to 'buy the dips' rather than 'sell the rallies'.

A soft landing is still possible. But it involves soothing not only the US labor market, but also ensuring that there are no accidents in an over-extended financial system that has come to take negligible interest rates as a given. Let's all wish good luck to the pilots. A minimalist tip to start the week. Last week, my wife and I went to an opera for the first time since the beginning of the pandemic — Akhnaten by Philip Glass. It's spectacular and weird in equal measures, but the music has hypnotic beauty to it. The Metropolitan Opera's production involved a chorus of jugglers and a male lead — the doomed monotheistic Pharoah Akhnaten — who spends much of the first act traversing the stage naked. The music does help escape the cares of the material world for a while (for something a bit shorter and more approachable, try Songs of Liquid Days, which includes lyrics written by the likes of David Byrne, Suzanne Vega and Paul Simon), and it really is a good idea to go on a date with your significant other. Have a good week everyone. More From Other Writers at Bloomberg Opinion: Want more from Bloomberg Opinion? Terminal readers head to {OPIN <GO>}. |

No comments:

Post a Comment