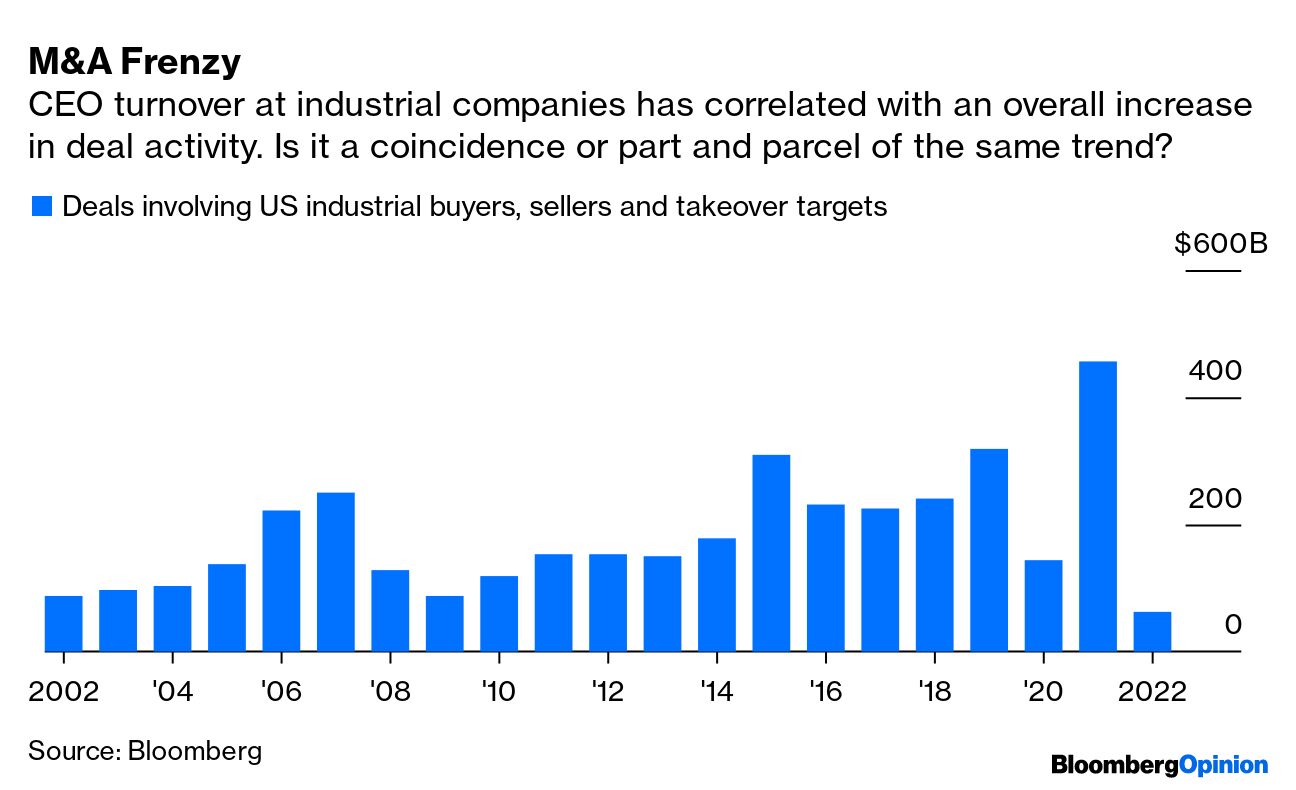

| Have thoughts or feedback? Anything I missed this week? Email me at bsutherland7@bloomberg.net Have a good weekend! The industrial C-suite is getting a refresh. Since the end of 2019, about a third of the industrial members of the S&P 500 have swapped out their chief executive officers. This includes the replacement of long-tenured leaders of FedEx Corp., Emerson Electric Co., Southwest Airlines Co. and Cintas Corp. This week alone brought news that Jim Loree is stepping down as CEO of power-tool giant Stanley Black & Decker Inc. in July and will be replaced by the company's chief financial officer, Don Allan, while David Petratis is handing over the reins at lock maker Allegion Plc that same month to Deere & Co. executive John Stone. Loree has served as Stanley's CEO since 2016 while Petratis has overseen Allegion since the company was spun out from Ingersoll Rand in 2013. All told, including these latest announcements, the average tenure of CEOs on the S&P 500 Industrial Index will drop to just 4.9 years, according to data compiled by Bloomberg. That's down from 5.5 years at the end of 2019 and about six years as of five years ago in mid-2017. For context, the average CEO tenure on the broader S&P 500 Index is currently about seven years. The recent flurry of turnover in the industrial C-suite is a microcosm of a bigger trend. Through April this year, more than 500 CEOs at U.S. companies have left their posts, the highest year-to-date total since researcher Challenger, Gray & Christmas Inc. started tracking the data in 2002.  There may be pent-up demand for retirements after some CEOs chose to stay in their roles longer to help steer their companies through the pandemic crisis. Gary Kelly of Southwest Airlines and Doug Parker of American Airlines Group Inc., for example, waited until the travel sector had emerged from the worst of the Covid slump in flying demand before announcing their respective succession plans in 2021. Read more: Southwest Shake-Up Shows Covid Reboot Is Here The challenges companies have had in navigating supply-chain logjams and labor shortages may also be inspiring boards to hit the reset button with new leadership and fresher eyes. Stanley Black & Decker has had an exceptionally difficult stretch, culminating in a dismal earnings update in April. The company chopped its full-year guidance on higher-than-expected input and freight costs and delayed a planned share repurchase because swollen inventories are pressuring its cash flow. Incoming CEO Allan's top priorities will be to restore management's credibility on financial guidance, stabilize cash flow, further simplify Stanley's mix of businesses after the recently announced divestitures of its security and automatic doors businesses and continue to transition the company away from its reliance on a complex, China-heavy supply chain. It's worth noting that Allan has been Stanley's CFO since 2009, so it isn't entirely clear how differentiated his perspective will be. Read more: Stanley Trips Over a Low Bar for Industrials Still, the new CEO faces in the industrial world mark a shift for a sector where up until fairly recently it was common for tenures to stretch into multiple decades. Jack Welch, for example, led General Electric Co. for 20 years, and his successor Jeff Immelt held the top job for 16. Emerson's Dave Farr became CEO in 2000 and didn't retire until 2021. Dave Cote ran Honeywell International Inc. for 15 years, while Brian Jellison headed Roper Technologies Inc. for about 17 years. The longest-serving current leader among S&P 500 industrial companies is Rollins Inc.'s Gary Rollins at 21 years, and that is a somewhat exceptional situation because the company is still in many ways a family business. While it's difficult to draw a direct cause and effect from the data alone, shorter CEO tenures at industrial companies have correlated with a significant pickup in divestitures and deal-making. US industrial companies bought and sold assets worth $456 billion last year, according to data compiled by Bloomberg. That was a record, but the pace of activity has been steadily climbing in recent years. The parallel increase in portfolio and leadership shakeups likely in part reflects reactions to — or fear of — activist investors, who tend to cast a skeptical eye toward both long CEO tenures and overly diversified companies. But the reality of a shorter tenure also means that CEOs have less time to make their mark on their companies and steer them in a new direction, if one is needed. Some leaders have been particularly busy: Jim Lico became CEO of Fortive Corp. in 2016 after the company was spun off from Danaher Corp. and has already carved out the Vontier Corp. transportation and mobility businesses into a standalone entity, merged the automation and specialty products platform with Altra Industrial Motion Corp. in a Reverse Morris Trust transaction and spent about $10 billion on more than a dozen acquisitions of software and health-care assets. Parker-Hannifin Corp.'s Tom Williams ascended to the CEO role in 2015 and he has since announced almost $20 billion of takeovers, with a goal of making the company's earnings less vulnerable to economic swings. Emerson's Lal Karsanbhai has held the CEO job for just over a year but he has already completed a blockbuster deal to merge the company's software business with Aspen Technology Inc. and is reportedly evaluating a sale of the InSinkErator garbage disposal unit that could fetch as much as $3 billion. Read more: Emerson Is Stuck in the Past. Ask Its New CEO Is this healthy? Probably more so than leaving one guy — and, frustratingly, they usually are men — in charge for as long as it takes to get a newborn infant into college. But the fast pace of change can cause whiplash as investors digest the new strategies and wait for the dust to settle on all these transactions. The turnover also raises interesting questions about how prepared industrial CEOs are for the kind of inflation that the economy is currently experiencing and the likes of which hasn't been seen in decades. "You continue to see disruptions in the supply chain continuing for the foreseeable future. At the beginning of the year, we were hopeful we would start to see improvements in the second half. Right now, we see the challenges continuing. We see inflation continuing" — 3M Co. CEO Michael Roman Roman made the comments this week at the Bernstein Strategic Decisions Conference. Covid lockdowns in China will shave about $300 million off 3M's revenue in the second quarter, Roman said. That plus foreign-exchange volatility will trim earnings per share by about 30 cents in the period. Inflation is now trending toward the high end of 3M's previous expectations, Roman said. The company is sticking to its forecast for organic sales growth of 2% to 5% for the full year, and said it is confident in its ability to offset rising costs and supply disruptions with higher prices and sourcing creativity. But Roman said it was a "mistake" earlier this year to flag a moderation in the pace of inflation as a sign that cost pressures might be peaking. "You have to be careful about calling a couple of data points early," he said. The update is troubling because many industrial companies were relying on an improvement in supply-chain and inflation conditions to meet their full-year guidance. Allegion, Stanley, GE, Honeywell and Rockwell Automation Inc. are among the industrial companies with more back end-loaded annual guidance, according to Barclays Plc analyst Julian Mitchell. On the bright side, Roman said he is watching closely for signs of a consumer slowdown but isn't seeing a material drop-off in demand yet in 3M's more retail-oriented businesses. Evidence also is building to suggest that the semiconductor shortage that has disrupted production of everything from cars to tractors is stabilizing. The time between when chips are ordered by companies and when they are delivered effectively held steady in May from the prior month, according to research by Susquehanna Financial Group. Daimler Truck Holding AG and Mercedes-Benz Group AG both commented this week that access to semiconductors was improving and related production stoppages were easing. Roper Technologies Inc. agreed to sell a majority stake in its remaining legacy industrial businesses to private equity firm Clayton, Dubilier & Rice for $2.6 billion. The deal includes the entire process technologies division, which makes pumps, compressors and controls and certain measurement and material analysis units. Roper will retain a 49% stake in the new industrial entity, a position that it intends to sell down over time. The transaction is the capstone of a multi-decade strategy to pivot Roper away from traditional metal bending via takeovers of niche software businesses that offer higher margins and more stable cash flows. It's fitting that Roper's final exit from its industrial roots comes as the company joins the S&P 500 Information and Technology Sector Index. After the divestiture to CD&R closes, Roper will get about 75% of its sales from software, with the remaining quarter coming from health-care and water products. The implied valuation for the industrial businesses — which generated about $940 million of revenue and $260 million of earnings before interest, taxes, depreciation and amortization in 2021 — is fairly high. The deal will give Roper more than $7 billion of financial firepower to direct toward more software purchases.

Frontier Group Holdings Inc. agreed to pay Spirit Airlines Inc. $250 million in the event antitrust regulators block the airlines' proposed merger. The underlying stock-and-cash offer from Frontier remains the same and currently values Spirit at about $21 a share, compared with a rejected all-cash proposal from JetBlue Airways Corp. that values the company at up to $33 a share pending due diligence. The rejiggering of Frontier's terms comes after proxy firm Institutional Shareholder Services Inc. recommended that Spirit investors vote against that deal as a way of signaling to the board that it should more thoroughly consider JetBlue's higher-priced offer. ISS also flagged the lack of a reverse termination fee in the Frontier deal; JetBlue had offered to pay Spirit $200 million in the event the takeover crumbled under regulatory scrutiny. Another proxy firm, Glass Lewis & Co., is taking the opposite side and recommends investors vote for the Frontier merger, in part because the stock component of that airline's offer allows the target shareholders to participate in the future upside for the combined company. Glass Lewis also praised the Frontier reverse termination fee for giving shareholders "added protection" against potential regulatory risk. The vote is scheduled for June 10.

Freightos Ltd., an online freight marketplace, is planning to go public via a merger with special purpose acquisition company Gesher I Acquisition Corp. The implied pro forma enterprise value for the combined company is $435 million. The new entity has also secured $80 million in capital commitments, funds that will be used to further grow Freightos and expand its margins. Existing investors include FedEx Corp. and Qatar Airways.

| CEOs are getting gloomier about the economy

Consumers may be the losers in an industrial boom

The future of agriculture is robots

Airlines' lack of preparation for the travel rebound is shocking

How much should we care about Elon Musk's " super bad feeling"?

Jobs picture is different at small companies, rates-sensitive sectors

Prices for lumber, an early inflation signal, are tumbling

There's now a shortage of movie theater popcorn

|

No comments:

Post a Comment