| Markets have entered into a WACO reality: Will the Ayatollahs Chicken Out? Traders are concluding that they almost certainly won't, and so prices enter Holy Week under the worst pressure of the now-month-old conflict. The acronym does a little violence to the facts. Iran's new supreme leader isn't technically an ayatollah, a title reserved for the most senior ranks of the Shiite clergy. But many find acronyms helpful, and TACO (Trump Always Chickens Out) — which made a lot of money when the president backed off from his initial Liberation Day tariffs last year — has outlived its usefulness. The ayatollahs have very little left to lose after already suffering a military pounding. That reduces their incentive to quit. And analysts have started to look more than 50 years back into history. They realize that Tehran has found a way to exert control over what the once-seemingly-all-powerful Sheik Yamani of Saudi Arabia called the "oil weapon" during the embargo and crises of the 1970s. Iran's leaders have also established that they can control that weapon — limiting shipping through the Strait of Hormuz — at very little cost to themselves.  The world hung on Saudi Oil Minister Sheik Yamani's every word in 1973. Photographer: Roger Jackson/Hulton Archive/Getty With the weaponry now at their disposal, Tehran can make those who control tankers destined for unfriendly countries decide that it's not worth the risk to attempt the crossing. With the power to cut off oil supplies selectively, rather than resort to mining that would also block their own exports, the leadership's incentive to relent grows even lower. The obvious analogy is with the 1956 Suez Crisis, when Egypt nationalized the canal, started charging fees, and provoked the United Kingdom and France into the failed military campaign that would end their status as great powers. There are presumably limits to the pain Iran can tolerate, and its arsenal is finite. But the Suez precedent suggests that it not only has little to lose but much to win from continuing the conflict. Until now, traders had relied on thegame theory that showed President Donald Trump should try to end the war as swiftly as possible. But the new military reality in the Strait dictates that this is no longer his choice. While he had control of the tariff situation after Liberation Day, he is now dependent on a motivated opponent, as are the markets. As Kyle Rodda of Capital.com explains: Basically, everything is an oil trade and everyone is an oil trader right now. That trade depends on a reopening of global shipping lanes, whether that be through diplomatic or military means.

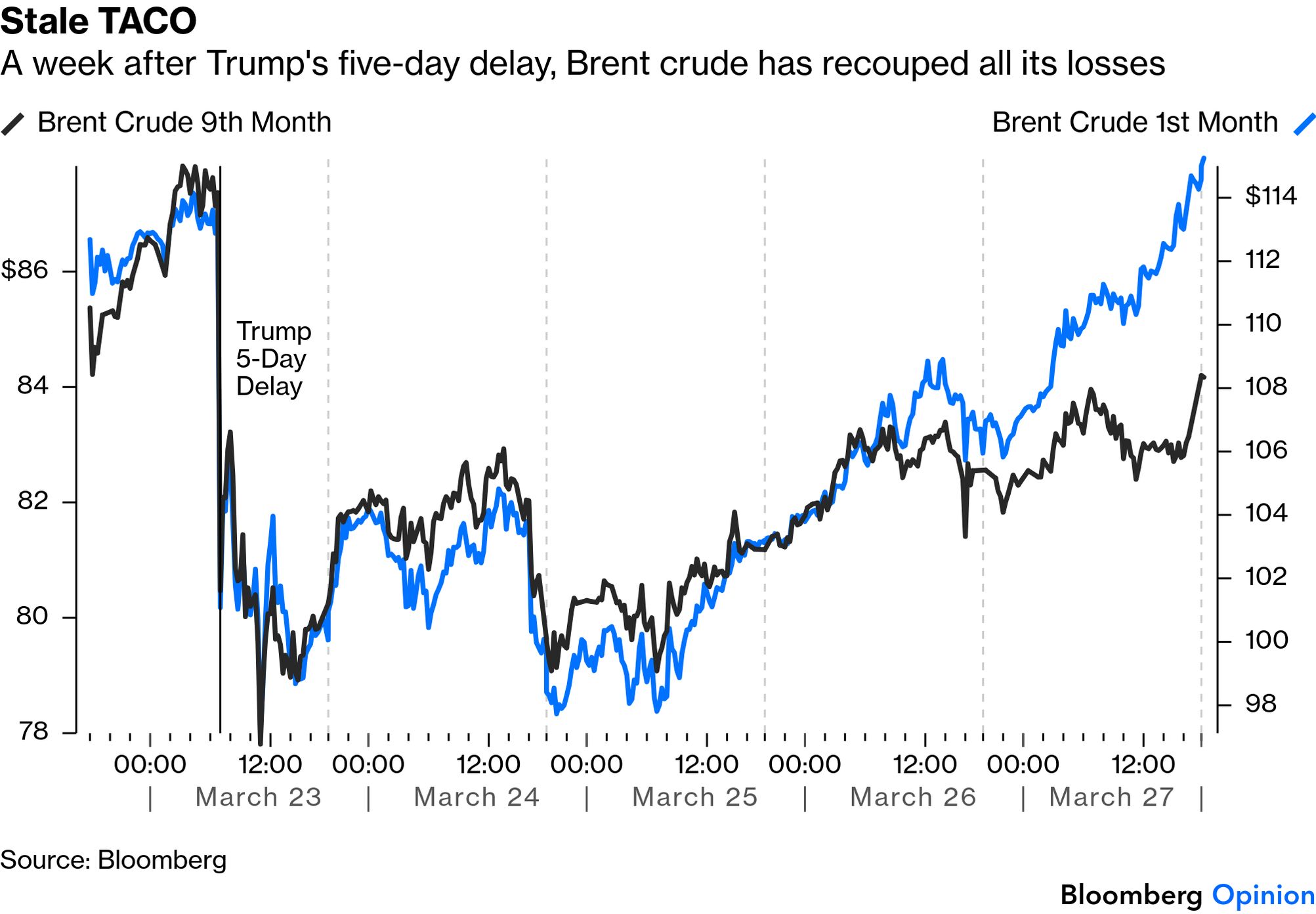

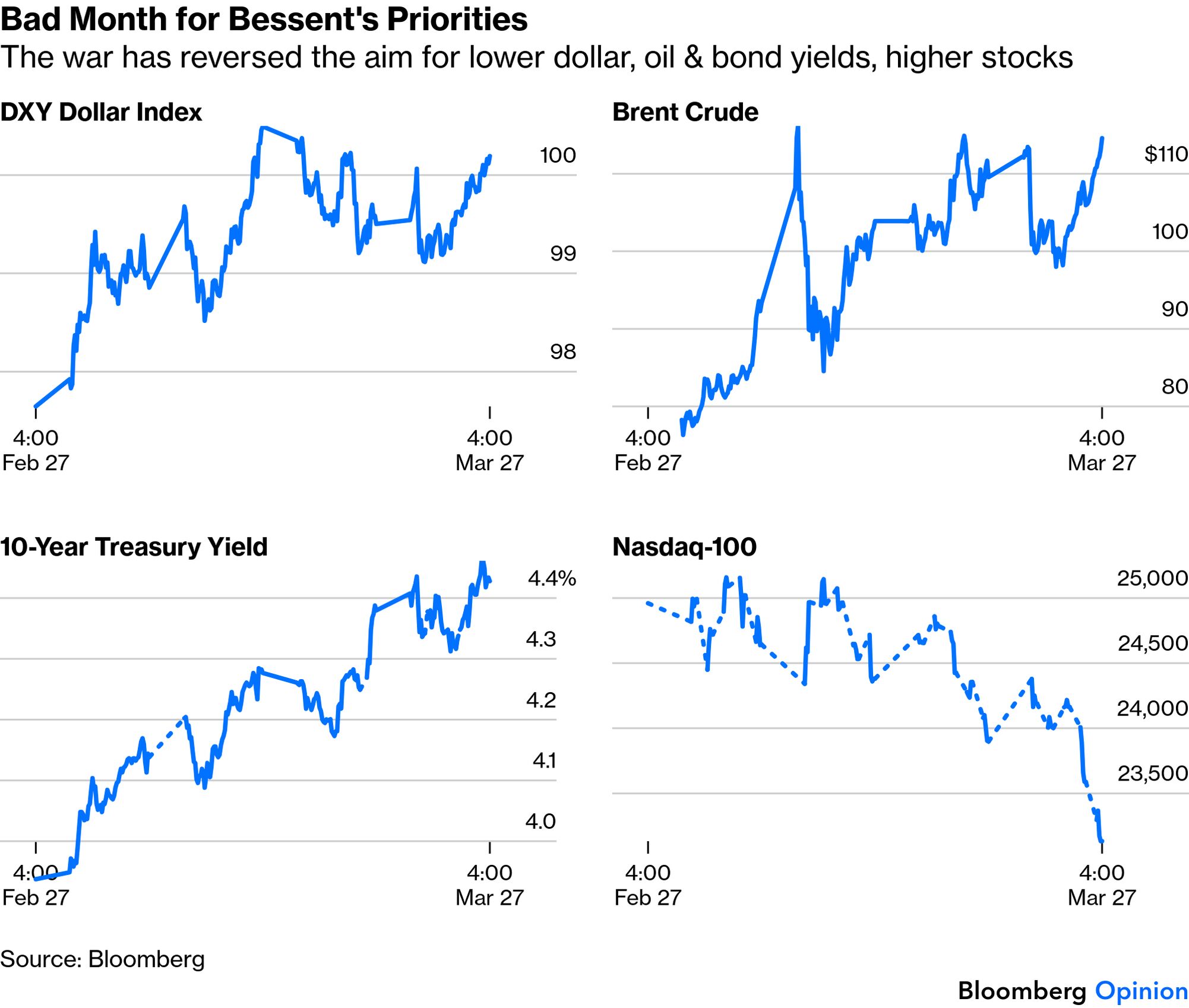

Markets over the past week — including a savage start to Monday trade in Asia — demonstrate a growing realization that reopening shipping will be difficult, and that Trump can no longer prompt a rebound by appearing to "chicken out." To start last week, the president sparked a stock market rally and a fall in the oil price by posting that he'd postponed his threat to bomb Iranian energy infrastructure by five days. But his extension of the ultimatum by a further 10 days, announced Thursday, had no effect. If anything, it revealed how weak his military hand was, and gave the impression that he would say anything to bolster the market. Brent crude is now higher than it was before Trump announced his initial delay: Note that while first-month futures, which set the current price, are higher than a week ago, ninth-month futures, predicting where oil will end the year, remain somewhat lower. Hopes for an imminent resolution have dwindled; the belief that normal supply will be resumed well before December remains intact. That's not an unreasonable position, but it does mean that further escalation into a more enduring conflict remains unpriced. The markets are also potentially forcing the president to escalate just to end the conflict. A month in, it has led to higher bond yields and a stronger dollar as well as more expensive oil. That is the exact opposite of the agenda that Treasury Secretary Scott Bessent had been following successfully for the previous 12 months: Then there is the weakness in the stock market. The Nasdaq 100, home of the biggest US growth stocks, is at an eight-month low and starts the week 11.5% below the all-time high it set last October. But this has been a very slow-moving correction, quite unlike the response to the Liberation Day tariffs. With traders expecting either a TACO or a comfortable US victory, they've been reluctant to capitulate. It's hard to see how the war can continue much longer without such catharsis: Second-order shocks, such as rising insurance premiums, higher transport costs, and shortages of vital goods are yet to affect developed economies. To avoid them requires a swift end; and Iran's leadership knows this. Investment commentary on the war has moved on from game theory to military explorations of how the US might use its navy to escort ships through the canal, and how ground troops might be deployed. David Woo, who runs the David Woo Unbound newsletter, argues: Trump has managed to talk up the stock market every Monday over the past three weeks. I wonder what he will say tomorrow to prevent the S&P 500 from joining the correction. The most he can say is that a ground offensive will be limited and short.

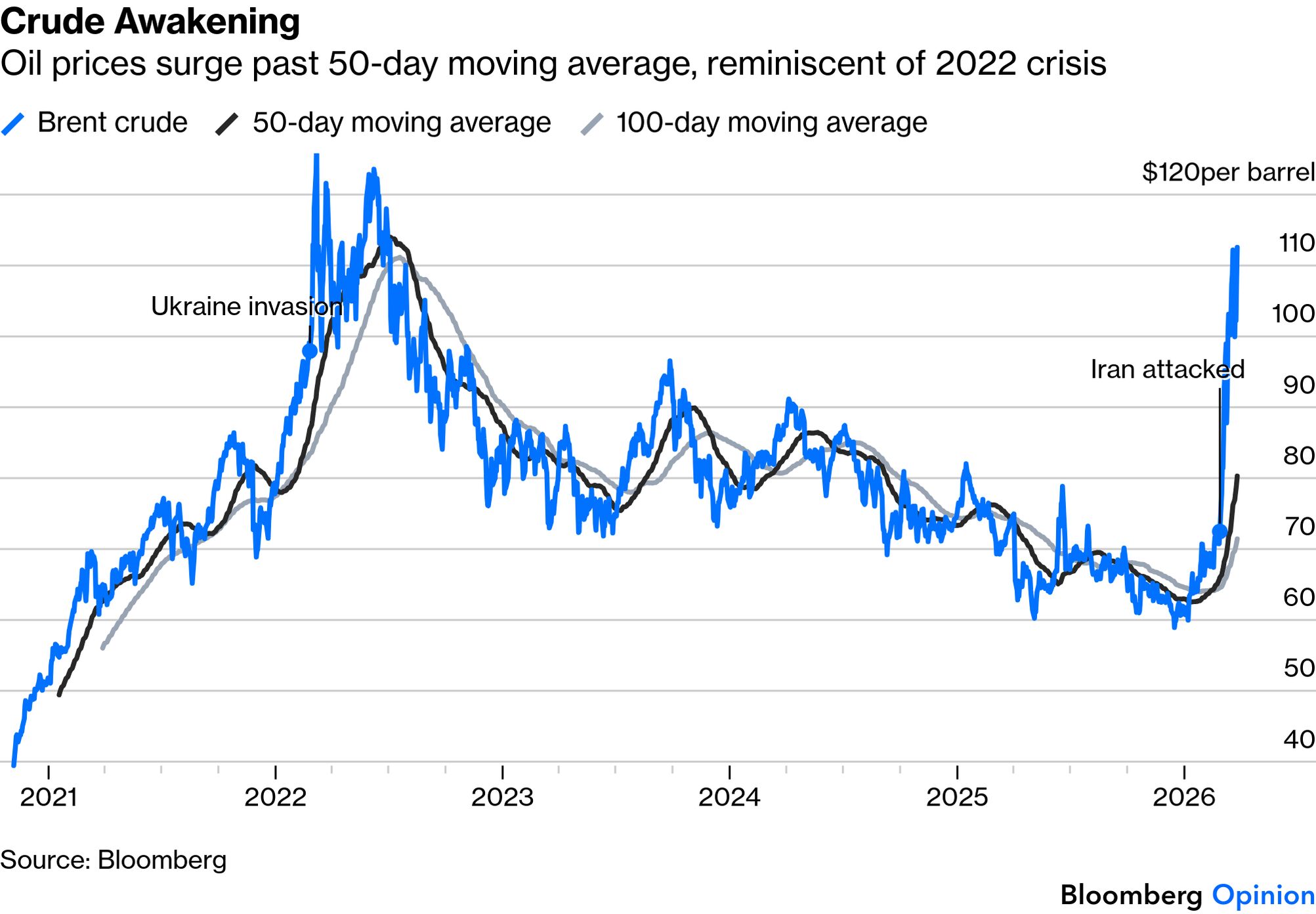

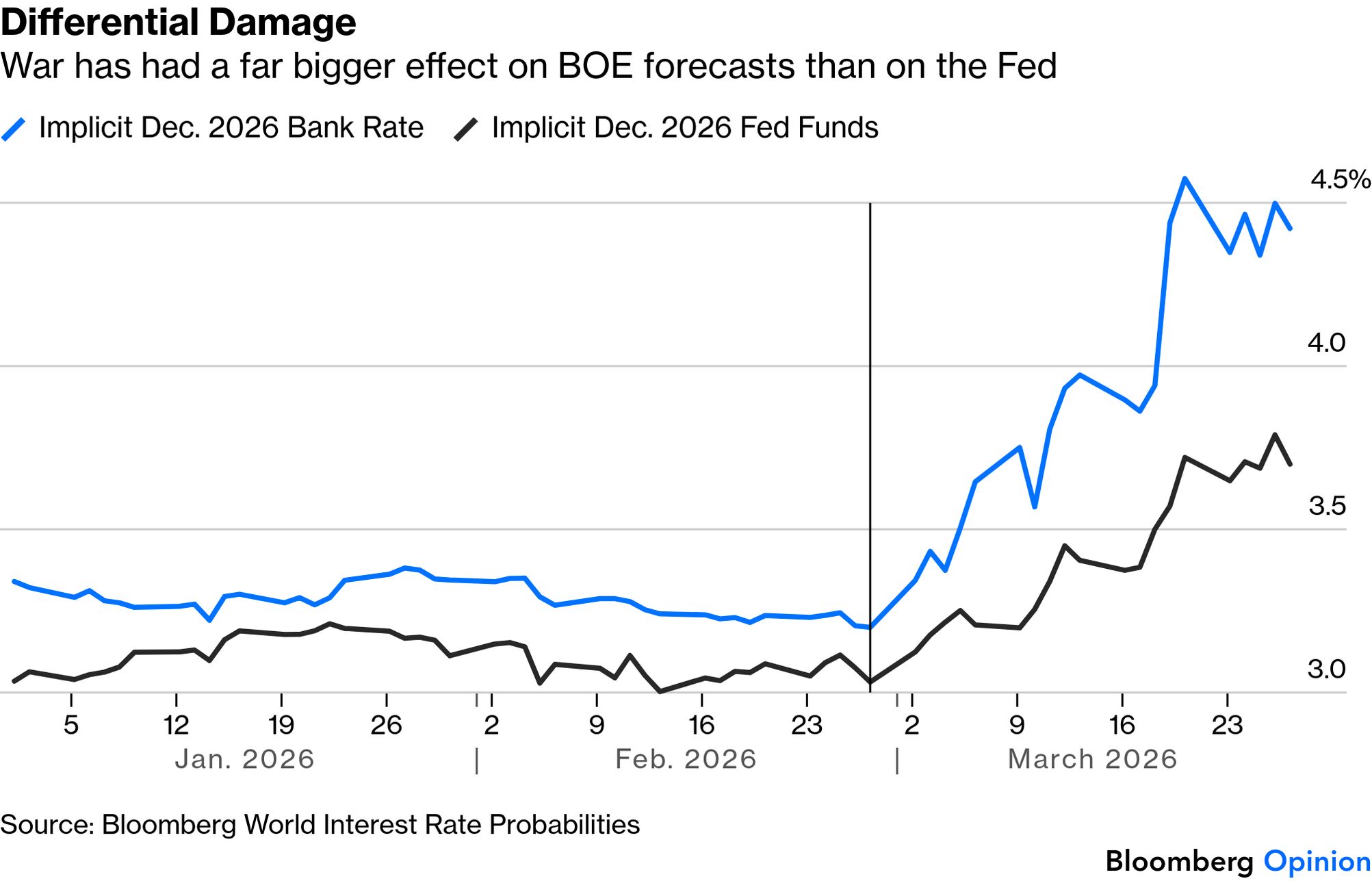

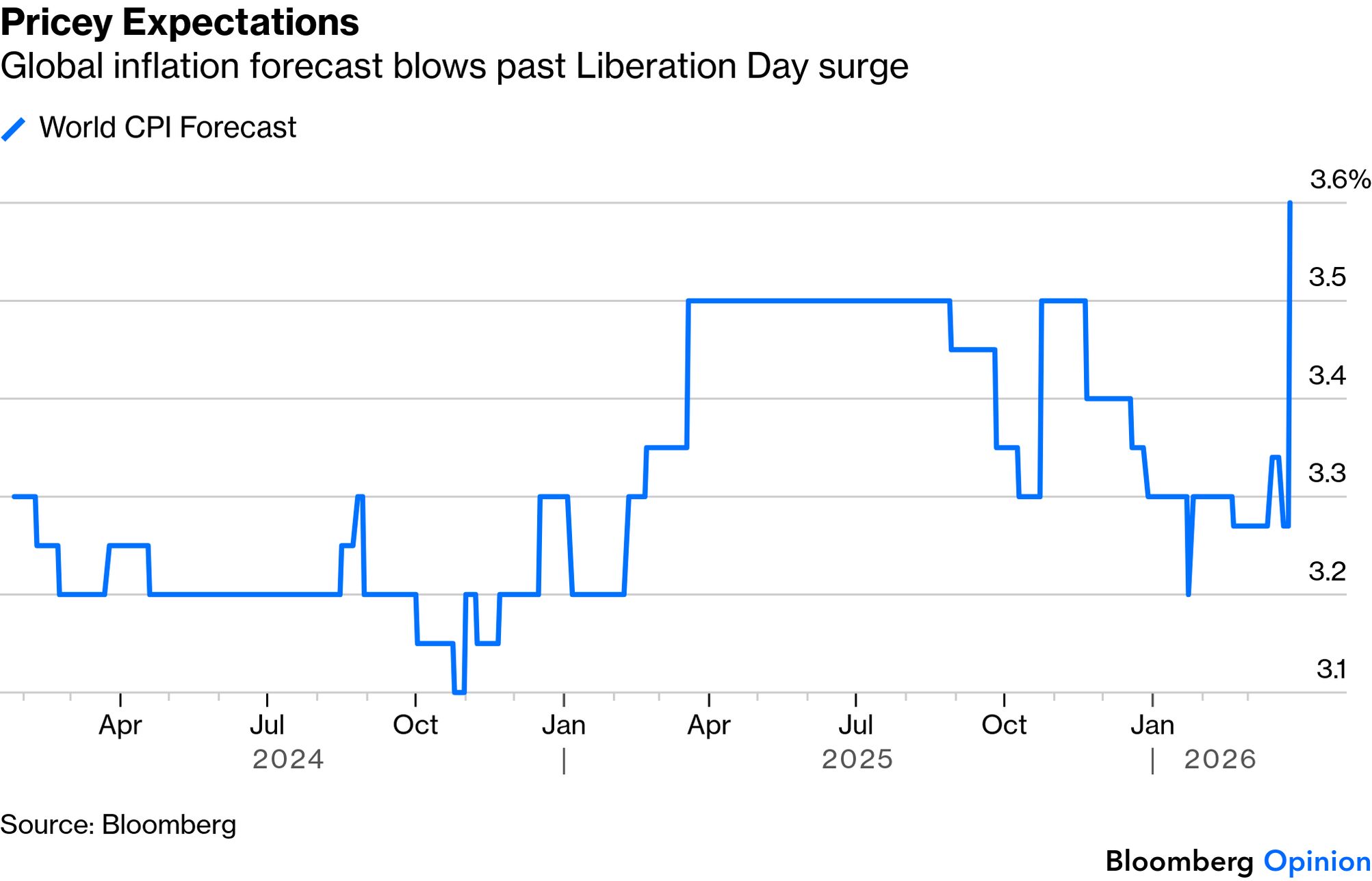

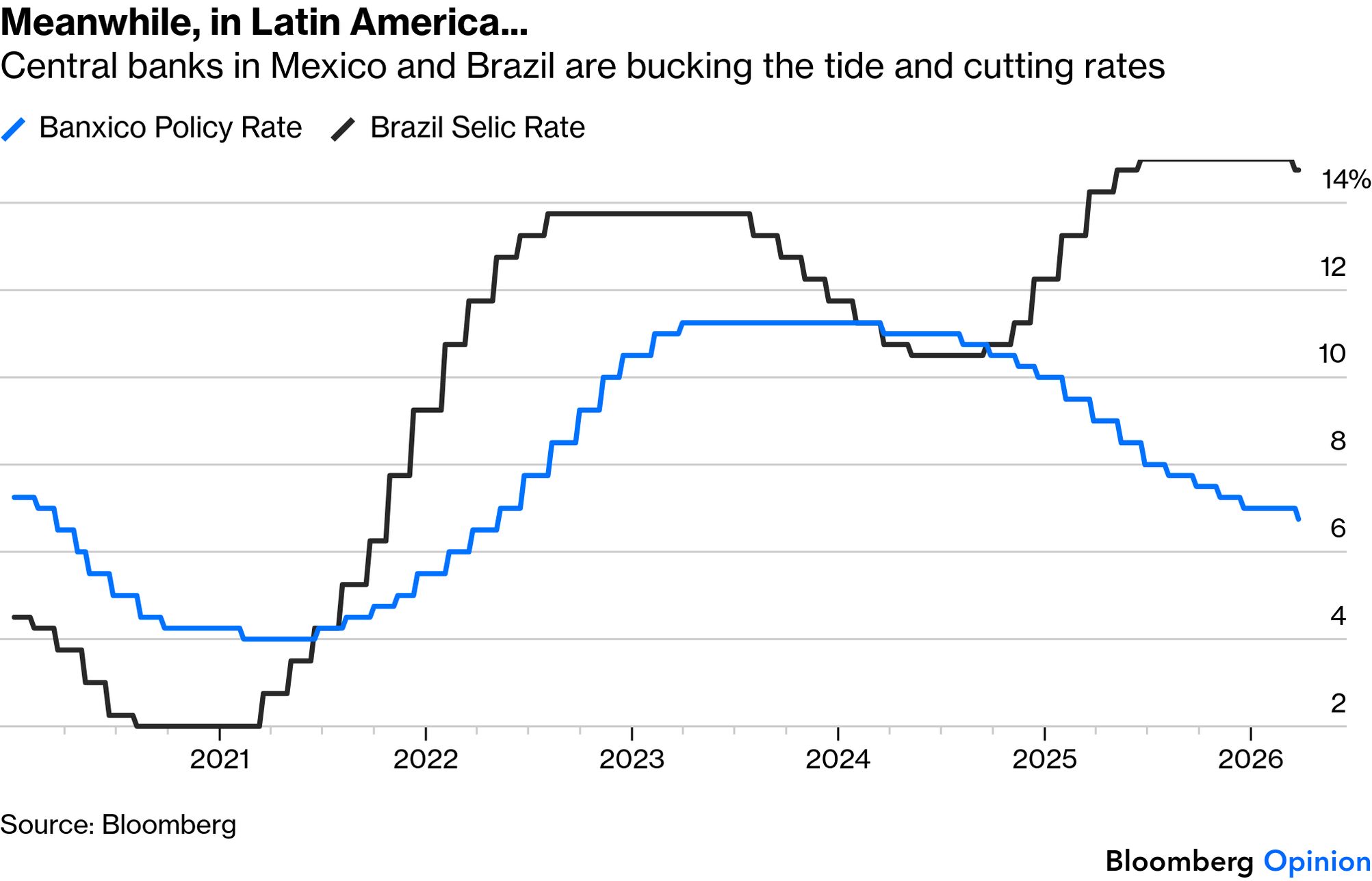

At this point, a major buying opportunity will depend on Iran springing a surprise and suing for peace. Absent that, Woo suggests that the "war risk premium will keep going up until the ground offensive starts." There are historical precedents for this; the S&P 500 set an enduring low and started to rally on the day US troops invaded Iraq in 2003. But it's growing harder to see how that point can be reached without a ground offensive — unless for some reason the ayatollahs chicken out. Central banks assessing the cascading impact of the war are reaching a familiar conclusion: A longer war would be inflationary and threaten the growth outlook, which was only just beginning to clarify after the twin shocks of the pandemic and last year's rise in US tariffs. But history shows that central bankers are rarely homogenous when reacting to big geopolitical shocks. They tend to react to domestic conditions and idiosyncratic pressures. And that is happening again. A sustained surge in crude oil, which has now jolted far further ahead of its short-term trends than after the dislocation following Russia's invasion of Ukraine four years ago, would be a serious problem: But the effects are varied. Those physically further from the conflict, and less dependent on oil imports, are suffering less damage. This shows up dramatically in the divergence of market expectations for policy rates in the US and the UK since the outbreak: Add policymakers' experience of navigating supply chain disruptions and their crisis-response playbook should be battle-ready. After the Fed and other developed central banks were too slow to respond to inflation five years ago, they are more likely to err in a hawkish way this time — and Bloomberg's inflation forecast is surging: That seems to have ruled out cuts for the developed world. The European Central Bank, Bank of England, and the Swiss National Bank all acted unanimously to hold interest rates, keeping tabs on geopolitical pressures. But Brazil and Mexico eased. They aren't immune to the fallout, but come to this crisis in a very different position and are relatively cushioned by geography from the worst impacts. Brasilia's cut, the first in two years, follows a cooling economy and relatively benign inflation. The growth outlook alone would point to easing. Here's how the bank's chief Gabriel Galipolo views the Iran situation: Although some sectors of the Brazilian economy, especially the oil sector, may benefit, the predominant aggregate effects of the conflict on the global and domestic economy should be the usual effects of a negative supply shock, increasing inflation, and decreasing growth.

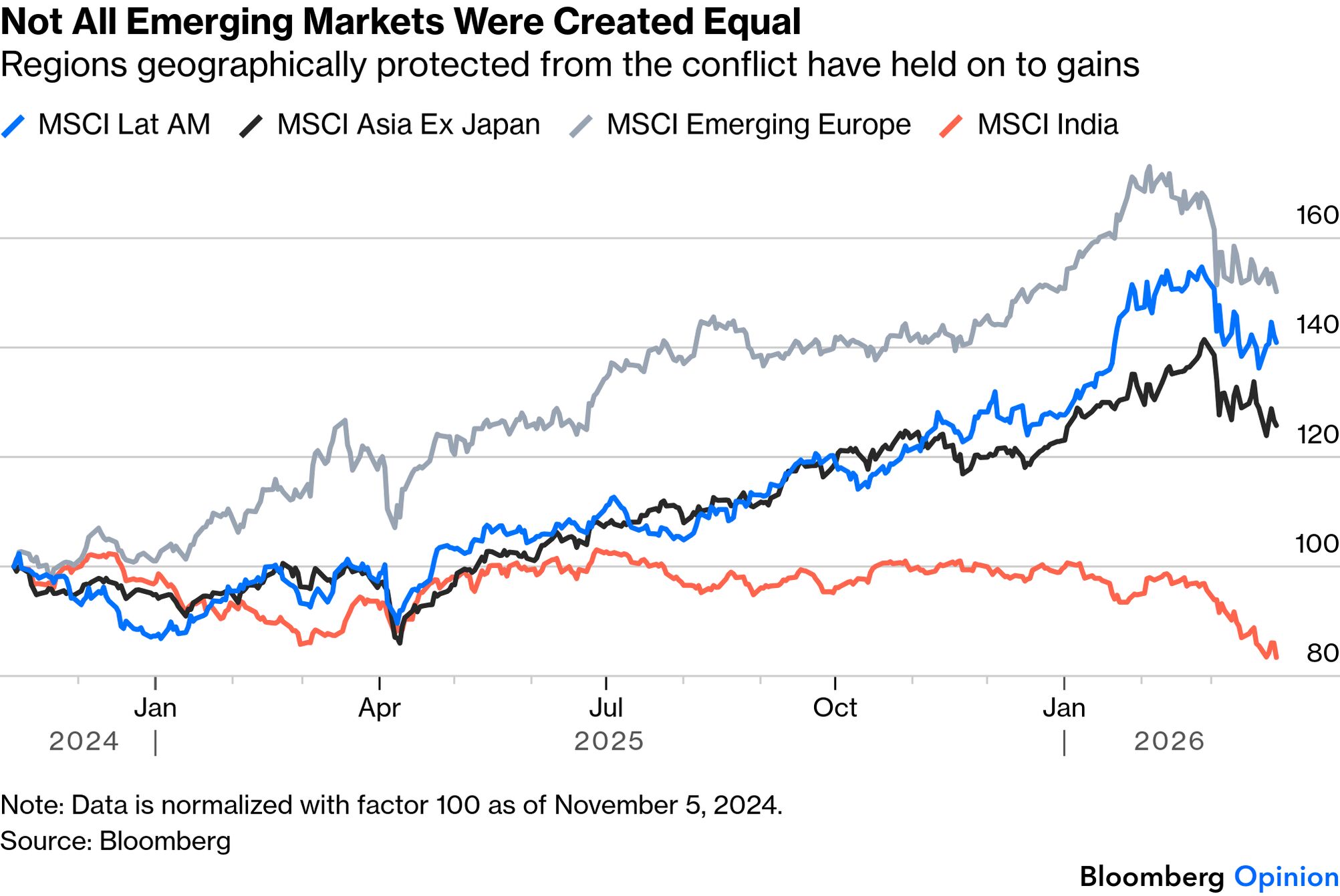

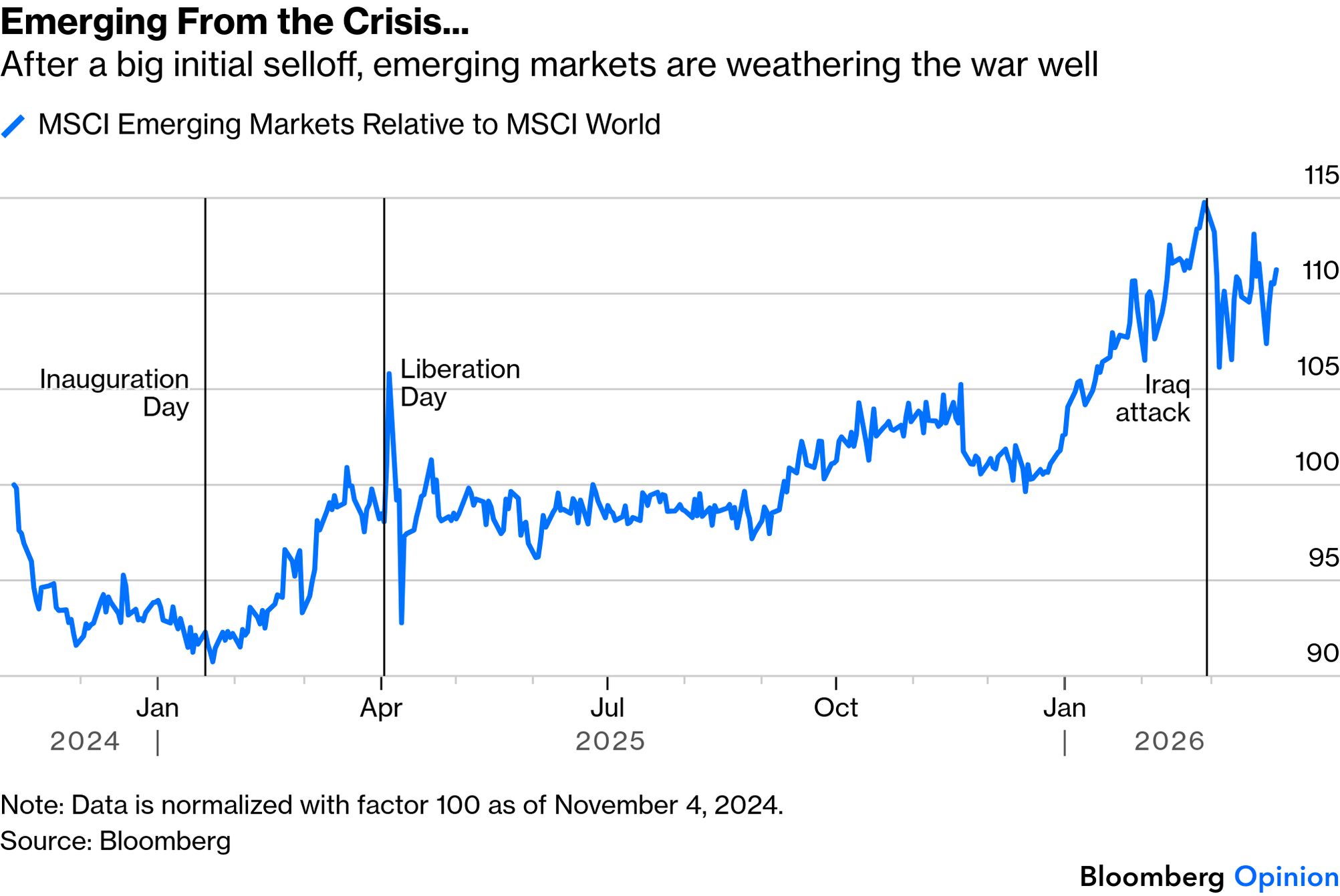

Mexico's return to easing was unexpected, and contentious, decided by a 3-2 vote. Its growth and inflation outlook are much the same as Brazil's. The cut's timing suggests it is indirectly betting on a shorter conflict and anxious to head off any immediate risks to growth: While virtually every emerging stock market has fallen since the war broke out, the performance is varied, with those that were outperforming beforehand generally holding on to their gains. Asia is hurting worse than most, while specific countries — like India, an energy importer close to the war zone — are bearing the brunt: Overall, the emerging world has avoided being caught up in a generalized risk-off cycle. After a huge reflexive selloff on the first trading day after the conflict started, they have recouped almost all of their losses. Anyone going long EM when Trump took office would still be very happy: Oxford Economics' Gabriel Sterne argues that this can continue, but not indefinitely: Central banks in Brazil and Mexico may succeed in seeing through the direct impact of the shock, a privilege normally reserved for central banks with ample credibility. However, if the crisis is prolonged, riskier countries will inevitably be hit harder, since by definition they have weaker buffers and, at some point, a global demand slump will exaggerate their vulnerabilities.

Jennifer McKeown of Capital Economics argues that a drawn-out conflict would likely mean a global recession. Her baseline scenario sees oil return to $60 by the end of 2026, but without an off-ramp, it could still be in triple digits to start 2027, with EU and Asian gas prices around three times prewar levels. Under such conditions, McKeown says all major central banks would hike rates this year. —Richard Abbey |

No comments:

Post a Comment