| Assumptions were made to be broken. An oil price spike automatically raises prices, so it's bad for inflation. That generally causes bond yields to rise, as the assumption is that central banks will have to raise rates to combat the higher prices. But it also acts like a tax hike, forcing consumers and companies to spend less on things other than oil. All else equal, that justifies a rate cut, and lower yields. Further, the logic of bonds is that they act as a shelter in times of stress — which means investors buy them during extreme uncertainty and conflict, like the past month. Thus it's always been strange that the bond market unambiguously reacted to the Iran war's inflation risk, but not to the threat to growth, and sent yields higher. Until now. Both yields and rate expectations for the Federal Reserve suddenly dipped Monday: It's not obvious why this happened when it did. Traders entered the crisis with leveraged positions, meaning that some of the rise in yields since then has come through a classic trading squeeze. Also, comments by Fed Chair Jerome Powell in the US morning helped further dispel the notion that rate hikes were a certainty. The immediate effect was to spark a sudden recovery in equities despite another dispiriting weekend of news from the Gulf. To quote one macro strategist: Interesting. Equities trading much better because Fixed Income is trading much better. Fixed Income is trading much better because we suddenly chose to fear growth more than Warflation.

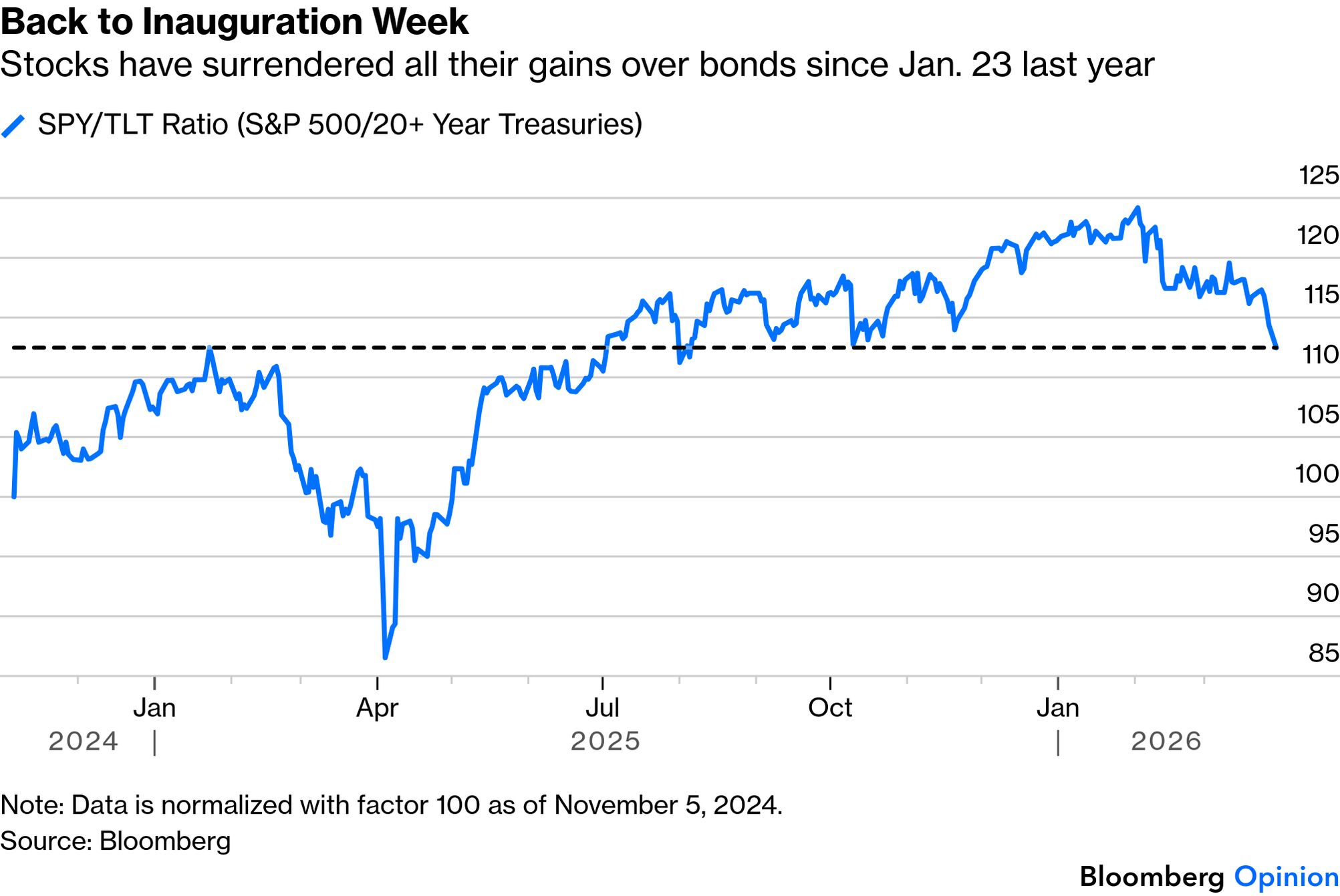

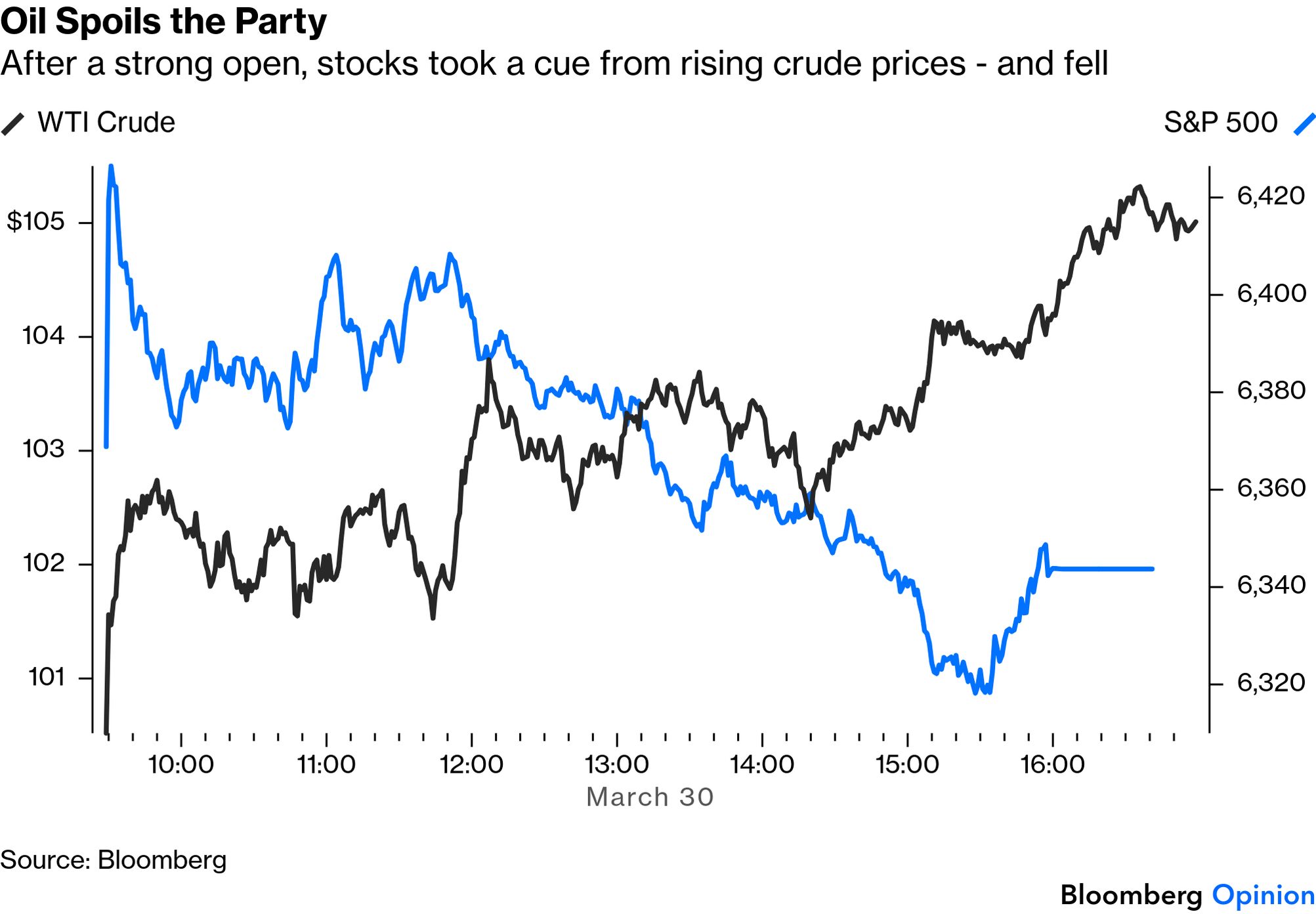

The classic measure of a growth scare is to track the performance of stocks relative to bonds. On that basis, although nothing like last year's Liberation Day selloff, the fall in stocks has now brought them back to their level of inauguration week in January 2025. Since then, stocks and long bonds have exactly matched each other: The bond market did allow a nice lift for stocks at the US opening, but it didn't last. Even when handed an excuse for a rally, equities didn't take it. That was mainly because of the oil price, with West Texas Intermediate, the main US benchmark, closing above $100 for the first time since the attacks on Iran began. (It fell later after the Wall Street Journal reported that Trump was considering ending the war without reopening the Strait). As Points of Return has covered, the markets remain on alert for a relief rally, and this is deterring many from selling. Measures that normally gauge extremes of risk appetite suggest that people are now negative enough for a rally to start — but the problem is that this selloff isn't a question of risk appetite. To quote Harry Colvin of Longview Economics: Equities are in an environment when you have all these technical and sentiment risk appetite models that really suggest you should get involved and buy again. But markets aren't really driven by risk appetite so much as news flow. If it does rally it's probably an opportunity to unload more risk, absent some sort of resolution of this conflict.

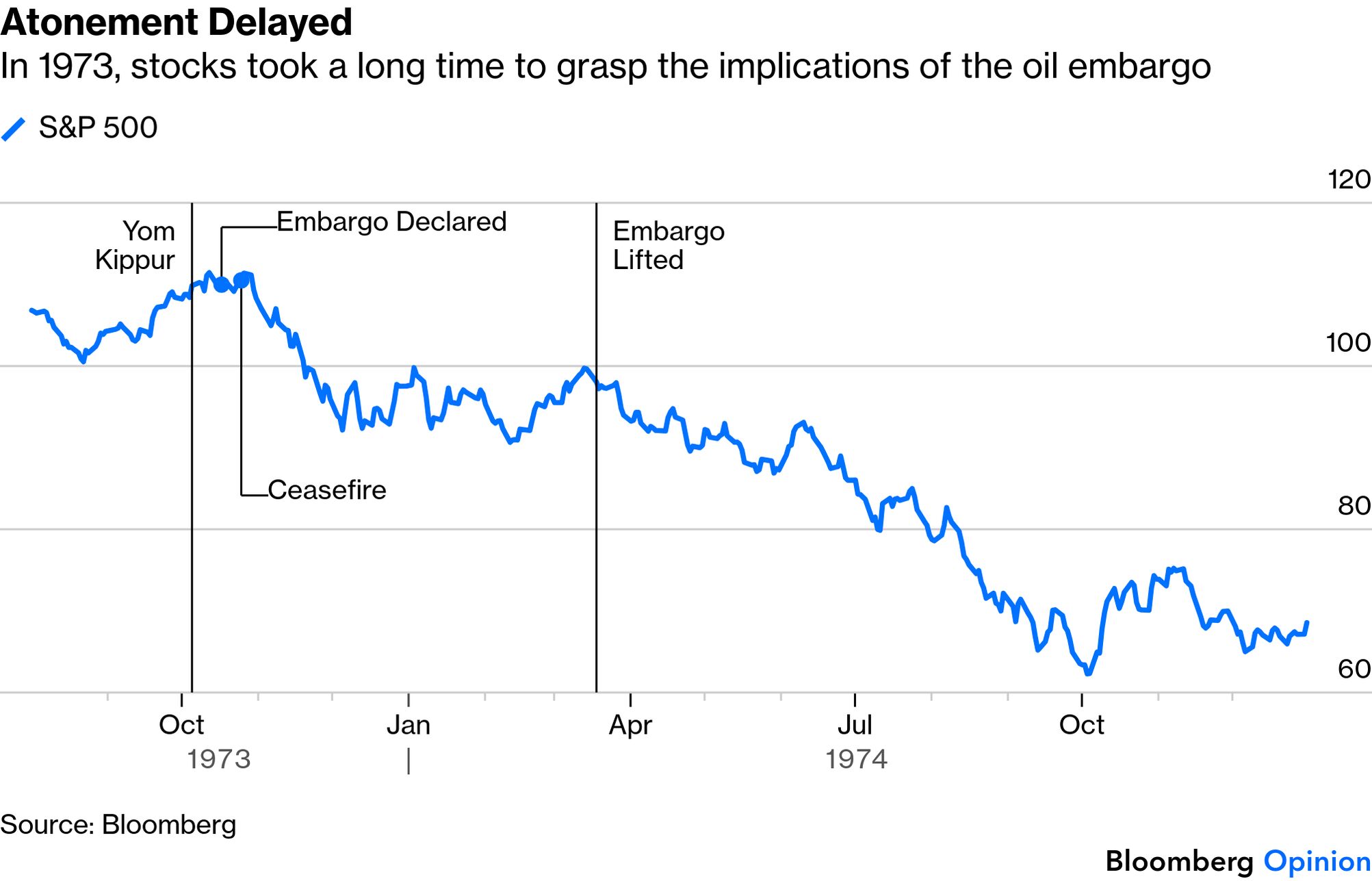

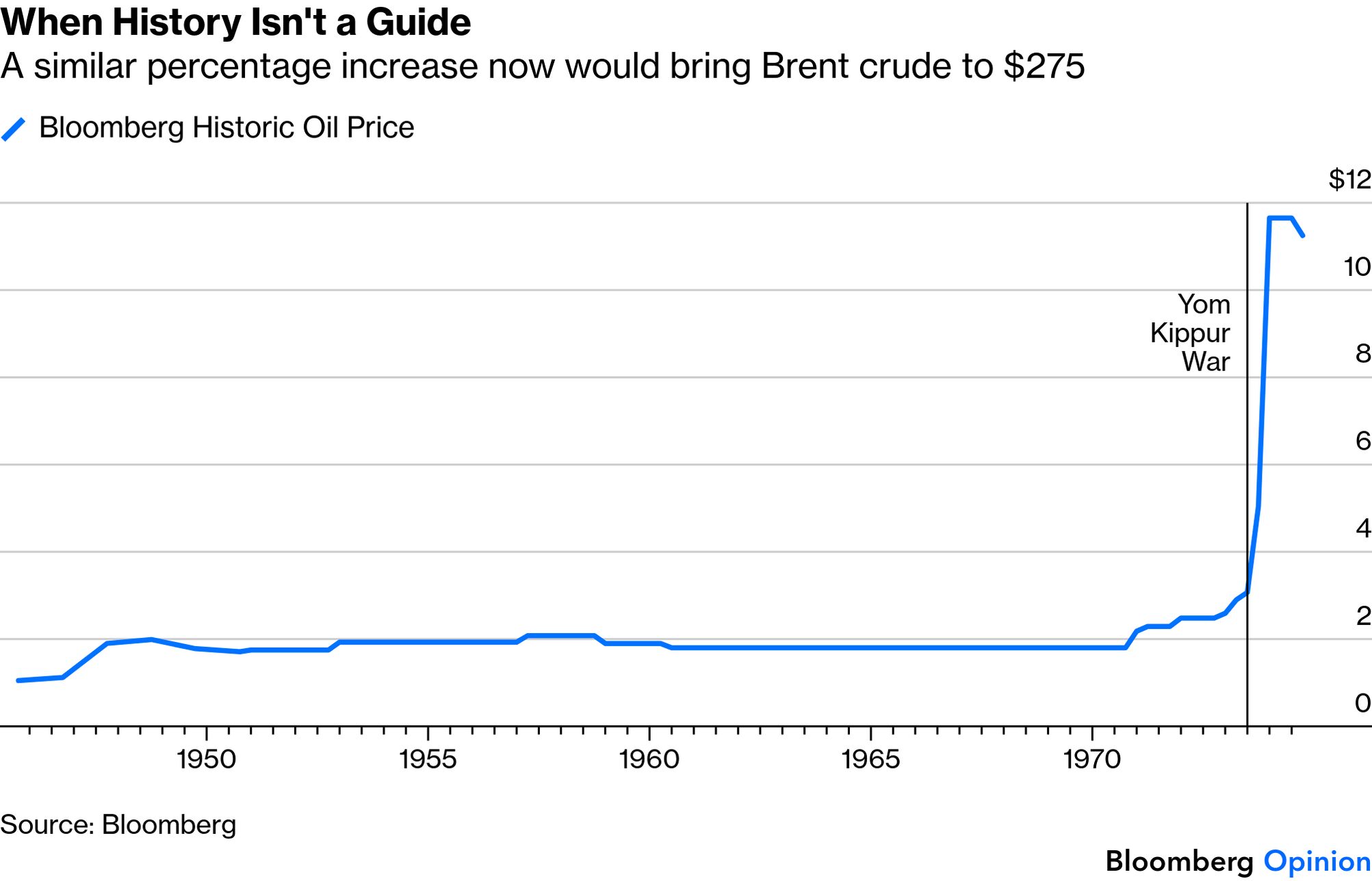

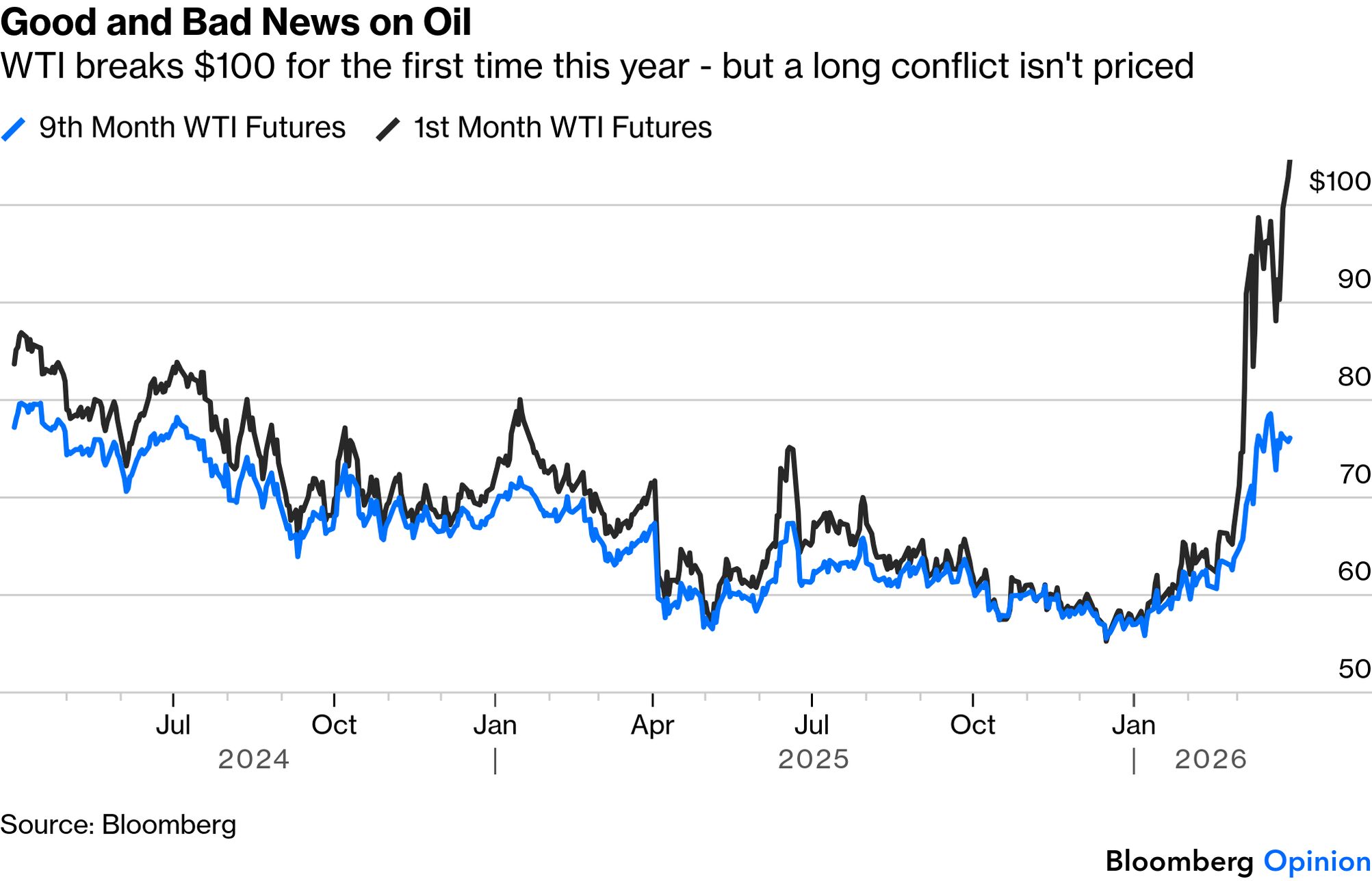

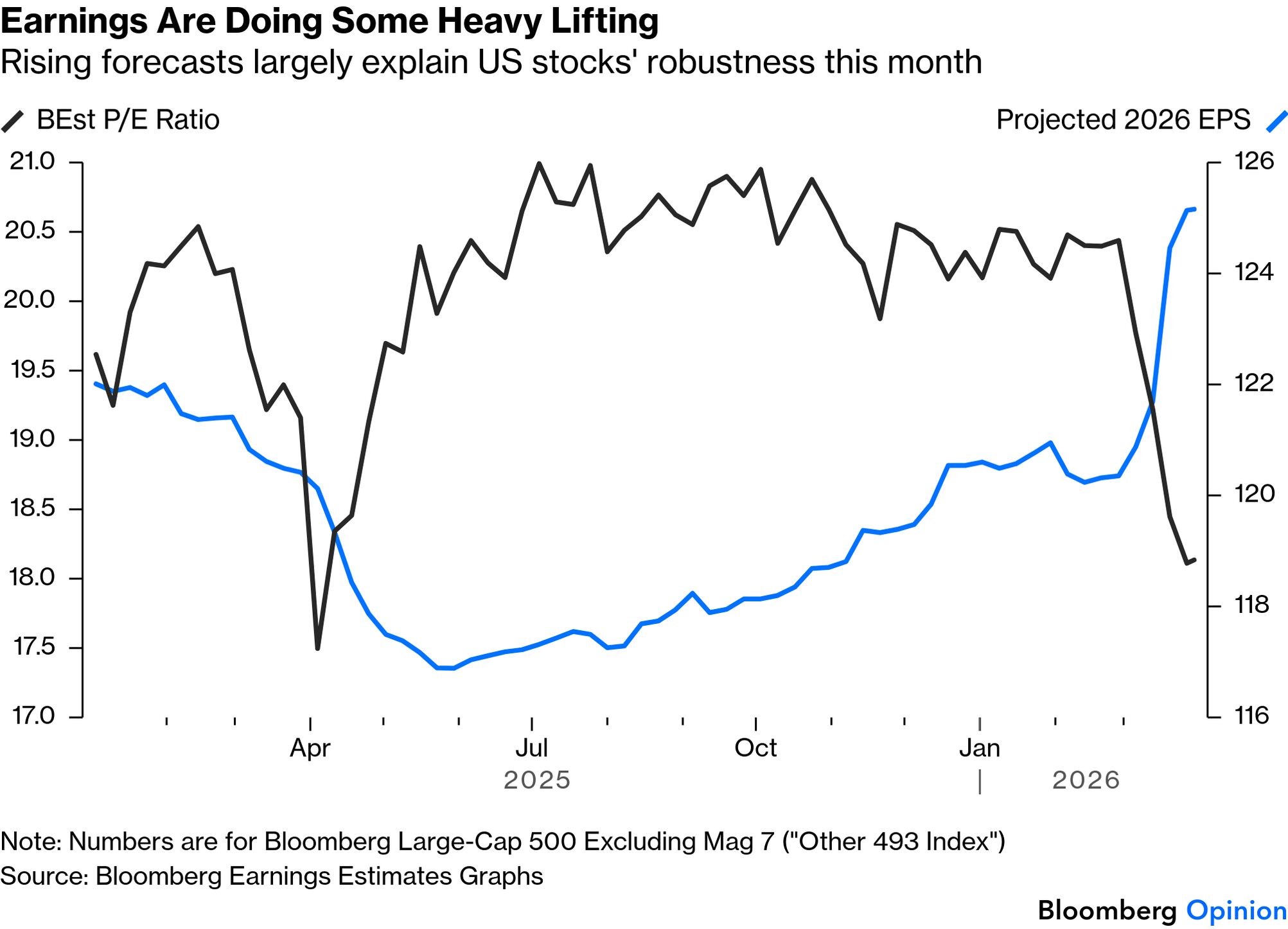

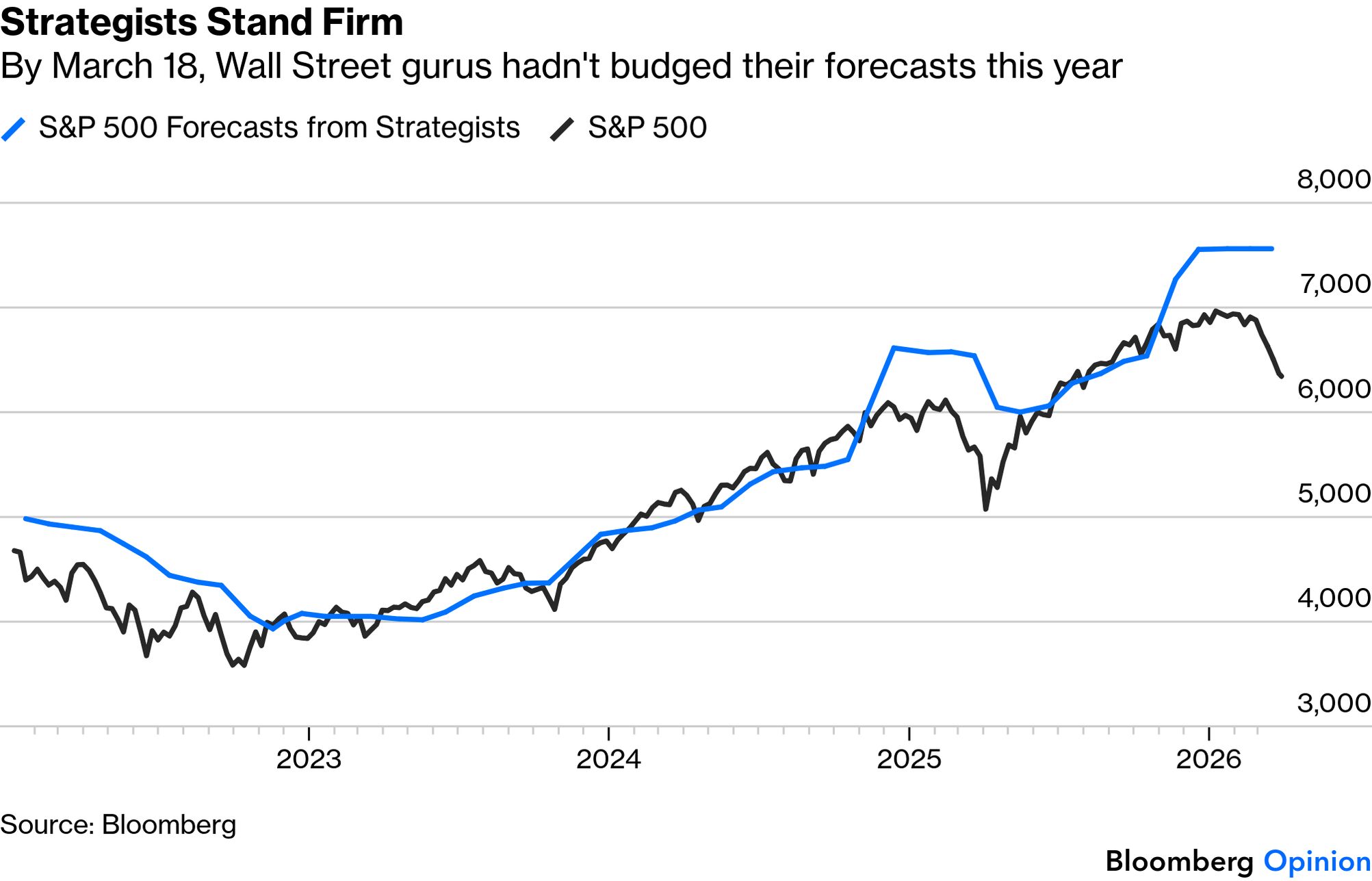

Put differently, stocks are almost in the textbook world where they follow a "random walk" incorporating all news as soon as it is known. Usually, waves of sentiment ensure that moves aren't truly random. But now, we need to keep watching the news and be prepared to react. It's the uncomfortable reality of the moment. Market catharsis — the moment when fear finally overcomes greed and share prices stage a big fall to catch up with bad news — is surprisingly elusive. Because it depends on mass sentiment as well as the news, hope can delay it, but not indefinitely. The relevant example for today is, yet again, the Yom Kippur War of 1973, the oil embargo that ensued, and the subsequent bear market in stocks. The conflict had a worse impact on the US equity market than either of the world wars, but it took a while for markets to grasp that. A coalition of Arab nations led by Egypt and Syria attacked Israel on Yom Kippur, the Jewish Day of Atonement, which fell on Oct. 6. In response, US President Richard Nixon organized an airlift of arms to Israel, which prompted the world's most important oil exporting countries to impose an embargo Oct. 19. The UN-negotiated ceasefire followed on Oct. 25; the embargo remained in place. The S&P 500 peaked the next day, at which point it had gained 2.3% since the outbreak of hostilities. Only then did catharsis ensue: Even after the embargo was lifted the following March, US stocks had almost 40% further to fall before reaching their 1974 low. The gas lines and trauma to public sentiment didn't immediately dissipate. If this seems baffling in hindsight, bear in mind that history at that time gave no useful guidelines. For the first quarter-century after World War II, the oil price was stable and controlled. It began to pick up after the end of the dollar's peg to gold in 1971, but nothing prepared traders (or the broader population) for what would happen once the embargo came into force: If the oil price were to repeat its 277% rise in the six months following Yom Kippur, that would imply a price for Brent crude of $275 by the end of this year. That seems almost unimaginable today — just as nearly $12 oil was in 1973. What is perhaps worrying is that crude futures show that traders are behaving as they did in the 50 years that followed the Yom Kippur War, and working on the assumption that any spike will be reasonably short-lived. WTI futures for nine months ahead are still below their level of two years ago, even as short-term prices move far ahead: The futures market may well be right, but if it isn't, the bad news will have to be incorporated into oil and stock prices. Hard economic impacts of big geopolitical shocks take a while to have an effect, while market prices, refracted through human emotions, take even longer. For now, traders are guarding against the considerable upside risk that the Iran conflict is resolved without significant long-term effects on oil supply. If the major interruption to supply actually happens, then stock market catharsis still lies in the future. Good Reasons to Postpone Catharsis... | The value of stocks, textbooks will tell you, ultimately depends on the discounted present value of the future cash flows they will generate. If the discount rate goes down — as it did when bond yields dipped Monday — that will help increase the value. More importantly, and harder to track, higher estimated earnings will tend to push up the price we should pay now. So far, the conflict has had minimal effect on earnings estimates. If we exclude the Magnificent Seven platform stocks, indeed, we find that 2026 earnings per share estimates for Bloomberg's index of the "other 493" of the 500 biggest US stocks have risen sharply this month: That gives greater reason to hope for the future, but also casts stocks' resilience in a different light. The Iran war's hit on forward earnings multiples has been almost as serious as last year's selloff around the Liberation Day tariffs drama. The loss of confidence in stocks looks less severe because of the earnings momentum, but the hit has been serious. That momentum might also help to explain why Wall Street strategists have reacted with calm to the conflict. Last polled by Bloomberg News colleagues led by Lu Wang on March 18, they haven't budget their end-year estimates at all. That mirrors how they behaved during the Liberation Day selloff last year, and it worked then: The first quarter is about to end. If companies have bad news to get off their chests about the effect the war is having on the bottom line, they'll probably start pre-announcing once the long Easter weekend is over. Until such a time as that happens, what remains a positive earnings outlook remains a good reason for delaying catharsis. If profits are really growing like this, it's invidious to get out of stocks now and let someone else buy them cheap. |

No comments:

Post a Comment