| In 2024, Bill Ackman came to the stock market with a proposition: You could give him $50, and he would invest about $49 of it in some stocks for you. (The other $1 would go to underwriting fees. [1] ) This is called a "closed-end fund," and Ackman's is called Pershing Square USA Ltd., or "PSUS." How much is that proposition worth? How much should you pay for $49 worth of stocks selected for you by Bill Ackman? Some possible answers include: - $49, because $49 worth of stocks is worth $49;

- less than $49, because Ackman will charge you fees for picking the stocks, which will reduce the value of your stake over time [2] ; or

- more than $49, because Bill Ackman is good at picking stocks and will pick ones that go up more than the average stock. [3]

Ackman obviously argued for "more than $49," because he is quite confident in his ability to pick the stocks that go up. Others disagreed. Closed-end funds often trade at a discount to net asset value (i.e., less than $49), so it would not be unreasonable to worry that Ackman's would also trade at a discount. In fact Ackman already has a closed-end fund in Europe, called Pershing Square Holdings Ltd., and it trades at a discount, so. This is a big problem when it comes to raising money. If Bill Ackman comes to you and says "give me $50 to buy $49 worth of stocks," and you think that proposition is worth $52, you give him the $50 and everything is great. But if you think that proposition is worth $47, there's a problem. You can't give him $47 to buy $49 worth of stocks: Where would he get the other $2? (He could just buy $46 of stocks for you, but that's not worth $47 — that's worth like $43. Etc.) Ackman can only raise new money from people who think that his fund is worth more than net asset value; he can only get this started by selling shares at a premium. Anyway this didn't work. Ackman set out to raise something like $25 billion for Pershing Square USA, cut that back to $2.5 billion, and ultimately raised $0. Oops. This analysis might make you wonder how anyone could ever launch a closed-end fund: If they all trade at discounts to net asset value, how do they start out by raising money at a premium to net asset value? [4] As far as I can tell, the main answers are "agency costs" and "sweeteners." Agency costs are, like, your broker puts you in a closed-end fund because she gets a kickback; sweeteners are, like, you buy the closed-end fund because you get a kickback. After Ackman pulled the Pershing Square USA offering, he and I and others thought about ideas for how to sweeten the deal for investors. [5] For instance: - Ackman could put in some of his own money to subsidize the new investors and get the thing going. (And then make money on the back end from fees, etc.) You give Ackman $50, he puts in $5 of his own money, he buys you $54 worth of stocks (after fees) and that's worth $51 to you. It costs him $5 but he's playing a long game.

- Ackman could put in some of his own money to get the thing going, and take back warrants. You give Ackman $50, he puts in $5, he buys $54 worth of stocks, and if that ends up worth more than $70 he gets half the upside, etc. Maybe that's worth $50.25 to you, but the warrants are worth $5.25 to him. [6] Everyone wins.

- Ackman could put some of the management company into the pot to subsidize the new investors. Ackman already runs a business, a hedge fund management company called Pershing Square Capital Management LP, which manages $30.7 billion of assets (including that European closed-end fund) and does some stuff with Howard Hughes Holdings Inc. [7] Running $30 billion of investor money is a good business — Pershing Square made $250 million of net income on $763 million of revenue in 2025 — and in 2024 Ackman sold a 10% stake in the management company to a group of investors for $1.05 billion. That suggests that the other 90% is worth, you know, $9 billion, more if Ackman keeps raising more money in new funds (like PSUS). If you put 5% of the management company into the new closed-end fund, then that increases the net asset value by $500 million and maybe gets the deal done. Of course this costs Ackman $500 million, but it's not cash, and it's maybe easier to justify. "If we raise a big closed-end fund, the value of the management company goes up, and I'd rather own 85% of a more valuable company than 90% of a less valuable one."

The third idea seemed like the favorite. And now here we are: Pershing Square Inc. filed for an initial public offering, in a deal that would see billionaire Bill Ackman's hedge fund make its debut on a US exchange alongside a new closed-end fund. The combined initial public offering includes a stake in Pershing Square USA Ltd., a closed-end fund, and Ackman's Pershing Square Capital Management, the filings show. For every 100 shares of the closed-end fund IPO purchased by a buyer, that investor will receive 20 shares in the hedge fund management company, the filing shows. Ackman is looking to raise between $5 billion and $10 billion for Pershing Square USA in the combined deal, with investors able to buy shares in the closed-end fund at $50 apiece. Part of the funds will be raised from a private placement, with $2.8 billion secured from qualified investors including family offices, pension funds and insurances companies, the filing shows. The investors in the private placement will receive 30 shares in the management company for every 100 closed-end fund shares purchased. Here are the prospectuses for Pershing Square USA Ltd. (the closed-end fund) and for Pershing Square Inc. (the management company [8] ). After the IPOs, Pershing Square Inc. will have 400 million shares outstanding, which means that a $50 investment in Pershing Square USA gets you $49 worth of stocks plus 0.00000005% of the management company. [9] If the management company is worth $10 billion, then that 0.00000005% stake is worth $5. If you think PSUS should trade at an 8% discount to net asset value, then the $49 in the pot should be worth $45.08, but then you get $5 worth of Pershing Square Inc. stock and it all works out? Pershing Square Holdings, the European closed-end fund, trades at about a 25% discount to NAV, but that's probably different.  | | | In 2021, US retail investors got together and all bought the same stocks at the same time, pushing up the prices of those stocks and causing much jollity and havoc. Which stocks? How did they decide which stocks to buy? How did they coordinate to all buy the same stocks at the same time? Well, there were some online discussion boards — Reddit's WallStreetBets forum was the most famous — and they got together there and talked explicitly about what to buy. This was important because they were mostly small investors. A big asset manager can buy a lot of stock and move the price, but a small retail investor can't. Millions of small retail investors acting together apparently can, but historically they typically didn't, because they had no way to coordinate: If I spend $1,000 to buy one stock and you spend $1,000 to buy another stock and someone else decides to sell those stocks, nothing really happens, but if we all agree to spend our $1,000 to buy the same stock on the same day it will go up. Social media provided a surprising new way for small-time retail investors to coordinate and, thus, to move stock prices. This phenomenon got the name "meme stocks," which emphasizes the fun and arbitrary nature of the picks, but it's also worth emphasizing the coordination. Last year there was another meme-stock wave and I speculated that the world had changed since 2021, and that in the future the retail coordination mechanism might be chatbots. Like: Millions of retail investors all want to buy stocks, and they all ask an artificial intelligence chatbot "what stocks should I buy," and the chatbot, which is extensively trained on Reddit, comes up with the sort of answer that would have been popular on Reddit in 2021. And the chatbot gets this question millions of times, and gives similar answers each time, and all the retail investors buy the same stocks and they go up. Today Bloomberg Businessweek reports: When he started trading in 2020, Lito Chen followed mostly well-trodden advice, tucking his modest university student savings into the kinds of blue-chip stocks like liquor companies that analysts had touted as safe bets. They proved to be anything but, erasing his nest egg and eroding his confidence in mainstream financial analysis. So when doing research for his next round of investment picks in the first half of 2024, Chen turned to what many young people know best: artificial intelligence chatbots and the social media hive mind. Investing in a mix of tech, defense, mining and other stocks recommended by internet friends and chatbots like Kimi and Zhipu, he's clawed back his earlier losses—and then some. "I'll rely more on AI for stock selection in the future," says Chen, a 24-year-old student in Shanghai. "Some of the stocks it picked for me really just kept rallying nonstop." Young, technologically savvy, even defiant, Chen represents China's newest generation of retail investors. These bold Generation Z traders have earned a nickname in China: Xiao Dengs, or "little guys"—and their swelling ranks are propelling the country's more than $14 trillion stock market. Yes, right, if AI picked stocks for you and those stocks "really just kept rallying nonstop," that might be because the AI is really good at spotting fundamental value. Or it might be that everyone is asking the AI the same question and getting the same answer, so they are all buying the same stocks. In 2021, loosely speaking, "Reddit" caused stock rallies; in 2026 maybe the chatbots are doing it. I wrote last week that "I am an old man and I tend to think that, if you want to bet that the Nasdaq 100 stock index will go up, the thing you should do is buy the Nasdaq 100 index." But obviously if I ran a gambling website I would think differently. I would think: "Buying the stock index might be a good way to bet on long-term economic growth, but it doesn't bring in any revenue to my gambling website, whereas I could probably sell somebody a short-term all-or-nothing bet on whether the stock index will go up." Traditionally securities law would prevent gambling websites from offering those sorts of bets, but not anymore. Bloomberg's Alexandra Semenova and Bernard Goyder report: The classic way to bet on the direction of the S&P 500 Index is in the options market, buying puts or calls tied to a preset price. But now, there's an alternative: placing a bet on Kalshi Inc. or Polymarket, using event contracts that allow rookie investors to make all-or-nothing wagers on stocks and indexes hitting a certain level."It simplifies it in a way that everybody can really understand, so it takes out the intimidation factor of the markets," said Danny Moses, the money manager made famous in The Big Short, and who has promoted Kalshi on his podcast. And: "It's hard to reconcile how those are not, both in legal definition and also economically, a security product that belongs on an SEC-regulated exchange," Craig Donohue, Chief Executive Officer of Cboe Global Markets Inc., said at a roundtable hosted by both regulators in September.

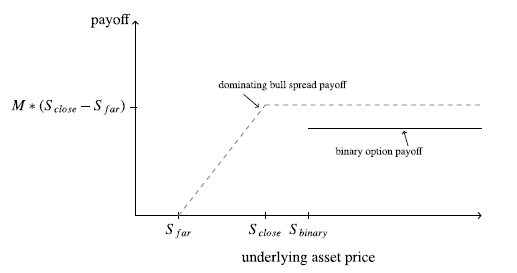

Shh, shh. We have talked a couple of times recently about binary options. Prediction market bets naturally take a binary, yes/no form. Your favorite politician or sports team will win the election or the game, or won't. When prediction markets offer bets that don't naturally take that form — bets like "what will housing prices be in a year," where the obvious form is a contract that goes up 1% for every 1% that housing prices go up — they nonetheless shoehorn them into binary options. I find this aesthetically annoying, but presumably it is easier for the prediction markets as a technological and credit matter. Also, though, while I find them annoying, these binary bets are clearly good marketing, to the point that even traditional financial exchanges, as well as Kalshi and Polymarket, are now offering binary all-or-nothing bets like "will the stock index go up." People like to make simple all-or-nothing binary bets, and to the extent that financial markets are in the business of offering entertaining bets, those are the bets they should offer. (To the extent that financial markets are not primarily in the business of offering entertaining bets, not, but here we are.) Here is "Overvaluing simple bets: Evidence from the options market," by Aaron Goodman and Indira Puri, from the October 2025 issue of the Journal of Financial Economics. The abstract: Analyzing trading behavior in the binary option market for retail investors, we find that market participants purchase binary options although strictly dominant bull spreads are available at lower prices: 15% of S&P index, 19% of gold, and 25% of silver trades violate no-dominance conditions consistently across three different asset classes. Buyers of dominated binaries lose on average 34% of the contract price by forgoing the dominating product. … We show that our results are consistent with retail investors valuing simple, easy-to-understand binary bets.

That is, you can buy a binary option that pays out $100 if some index is above 1,000, and $0 if it's below 1,000. Or you can buy a call spread that pays out at least as much as the binary option in every state of the world, say $0 if the index is below 800, $120 if it's above 900, and a linearly increasing amount in between. The paper has a schematic diagram: The dotted line is always better than the binary payoff. And they find that people pay less for the "dominating bull spread' than they do for the binary, for the pretty obvious reason that the bull spread is complicated, has different (always better) payoffs in different situations, requires you to buy multiple options and do math, etc., while the binary option is just "you make money if yes and you lose your bet if no." That's easier, so people pay more for it. "It simplifies it in a way that everybody can really understand, so it takes out the intimidation factor of the markets." Goodman and Puri are making an academic point — "a theoretically-grounded empirical impetus for research in behavioral finance which goes beyond historically pervasive utility frameworks" — but of course I am more interested in the commercial point. The commercial point is that you should sell people binary options because they will overpay for them. Though Semenova and Goyder report: This is how it works: traders buy contracts that yield $1 each. An option selling for 4 cents represents a 4% probability of an outcome happening. On Wednesday, that was the price on Kalshi for the S&P 500 Index ending the year between 8,000 and 8,200 points — a $2,190 bet pays out almost $44,000. In the options market, one could pay a $2,190 premium to bet on a 8,000/8,200 call spread, giving them the right to cash in if the index exceeds the lower end of the target range. The potential gains are capped at about $20,000 per contract, and investors would need to account for factors such as volatility and time decay that could affect their daily profit and loss. Sounds like the Kalshi call spread is cheaper? If you are arbitraging Kalshi binaries against options-market call spreads I guess you should email me. "Is this securities fraud?" | Because it is my schtick, people often send me fact patterns and ask "is this securities fraud?" Curiously, although my schtick is literally "everything is securities fraud," my answer to these questions is often "no." Most things that don't seem like securities fraud are securities fraud, but some things that do seem like securities fraud aren't. But this is never legal advice. Also people sometimes give ChatGPT fact patterns and ask "is this securities fraud?" Probably don't do that? Here's a TechCrunch article from last week: The $7 million in annual recurring revenue that Cluely co-founder and CEO Roy Lee shared with TechCrunch last summer was a lie, Lee admitted on Thursday on X. Wrote Lee, this "is the only blatantly dishonest thing i've said publicly online, so this is my formal retraction."

Several people sent me Lee's posts on X, which are (as someone posted) "the most @matt_levine coded thing to have ever happened": Lee apparently asked ChatGPT "got a call from some tech crunch reporter asking about revenue. told them 7m arr in reality 6.3m run rate. is this securities fraud," ChatGPT replied "almost certainly not," and Lee posted the exchange with the comment "ngl i was sweating for 2 mins." A verified X account with Elizabeth Holmes's name on it (!?!?!?!!??) replied "I wouldn't trust AI with this one." There are various not-best-practices things here, but I think I agree with ChatGPT? (Really not legal advice!) "Securities fraud" means using "any manipulative or deceptive device" "in connection with the purchase or sale of any security." When I say "everything is securities fraud," I typically clarify that "every bad thing that a public company does can be characterized as securities fraud." People are constantly trading the securities of public companies, so when a public company says something publicly, that will influence the purchase and sale of securities. If the company says something misleading, that is arguably " fraud on the market" that can count as securities fraud. But a private company's shares don't trade continuously; that's what makes it private. A private company will occasionally go out to investors and try to raise money. If it lies to those investors in its offering documents, that's surely securities fraud. If the offering documents are all true, but the company's CEO has gone around lying to reporters about its revenue, that's a harder question. There is no general law against lying to reporters, and in fact people lie to reporters all the time. If the CEO lied to reporters with a plan like "a big magazine will publish a glowing profile of me, and investors will read that profile, and they will want to invest, and then I will go out and raise money from them without lying directly but relying on the glowing profile," then (1) that kind of does sound like securities fraud and (2) it's absolutely part of what got, for instance, Elizabeth Holmes. [10] But if you lie to reporters and then publicly post a "formal retraction" before raising any more money, is that okay? I mean. Don't ask me. Don't ask ChatGPT either. Anyway TechCrunch reports that "in June, Cluely raised a $15 million Series A from Andreessen Horowitz," and the allegedly misleading article came out in July. Maybe it's fine. 'Downright Panic': Traders Tested to Limits on Oil's Wild Monday. Balyasny, Millennium, Point72 Lose Money in Volatile Markets. Anthropic's Standoff With the Pentagon Shakes Up AI Talent Race. Nvidia to Invest in Thinking Machines Lab and Supply AI Chips. The Laid-off Scientists and Lawyers Training AI to Steal Their Careers. Exxon Eyes Texas for Legal Home After 144 Years in New Jersey. Weinstein Is 'Buying Pessimism' With Discount Bids on Private Assets. ( Earlier.) Goldman pitches hedge funds on strategies to bet against corporate loans. Creditors of Wall Street-Backed MFS Claim £1.3 Billion Shortfall. How a British Mortgage Company Became Private Credit's Latest Black Eye. Sturm Ruger Accuses Beretta of Attempting to Gain Control of Company. Lego chief hits out at Danish wealth tax proposal. "The word 'tranche' seems to be having a big moment." Musk-Loving Panama Mayor Wants Him to Tunnel Under the Canal. "Meta has acquired Moltbook, a viral social network designed for AI agents." If you'd like to get Money Stuff in handy email form, right in your inbox, please subscribe at this link. Or you can subscribe to Money Stuff and other great Bloomberg newsletters here. Thanks! |

No comments:

Post a Comment