| "You're beginning to see the regime look for an exit ramp," said White House Press Secretary Karoline Leavitt on Wednesday when asked about negotiations to end the war in Iran. She was talking about Iran, but it might just as easily have been the US.

The next stage of escalation, should it happen, would be a win for nobody; the US would take out Iran's energy infrastructure, and Tehran would retaliate by doing similar damage to production facilities across the Gulf, meaning energy and food crises for a swathe of the world's population. It's obvious that both sides could use an off-ramp. The question is whether they can find one before it's too late. Stocks have been supported by growing confidence that America is indeed looking for an off-ramp. President Donald Trump's latest ultimatum doesn't expire until after trading ends for the week — a fact that cannot be a coincidence. Markets are likely to spend the rest of the week wavering as they weigh the evidence that Iran, despite its denials, could really make a deal. Trump is prone to exaggeration and contradiction, but he is stoking up a deal so much that it's clear he wants one. To quote Peter Tchir of Academy Securities, the US has a clear Plan A: - Get agreement and enforce it and call it regime change and win (or call it a win).

- Be better prepared (and allow the world to be better prepared) for the resumption of hostilities after the ceasefire.

But when he conducts the same exercise for Iran, he gets questions rather than answers: - Iran has now been attacked twice while "negotiating."

- What can Tehran do in 30 days to offset what the US and the rest of the world can do in 30 days? It would be shocking to see anything less than the biggest restocking of energy products in a month that the world has ever seen. So your economic leverage gets lower.

- Are their own people coalescing around a common enemy? Or is the regime itself being blamed, making its position even more precarious? This could be playing out in either direction.

- What happens to the Revolutionary Guard members if they're not in power after a deal? "To be brutally honest, the consensus view is they will be killed."

- Does Iran believe that there is some amount of "time" where the disruption to global trade (oil and more) causes the US to offer better terms? If there is, it behooves them to prolong the conflict as time is on their side.

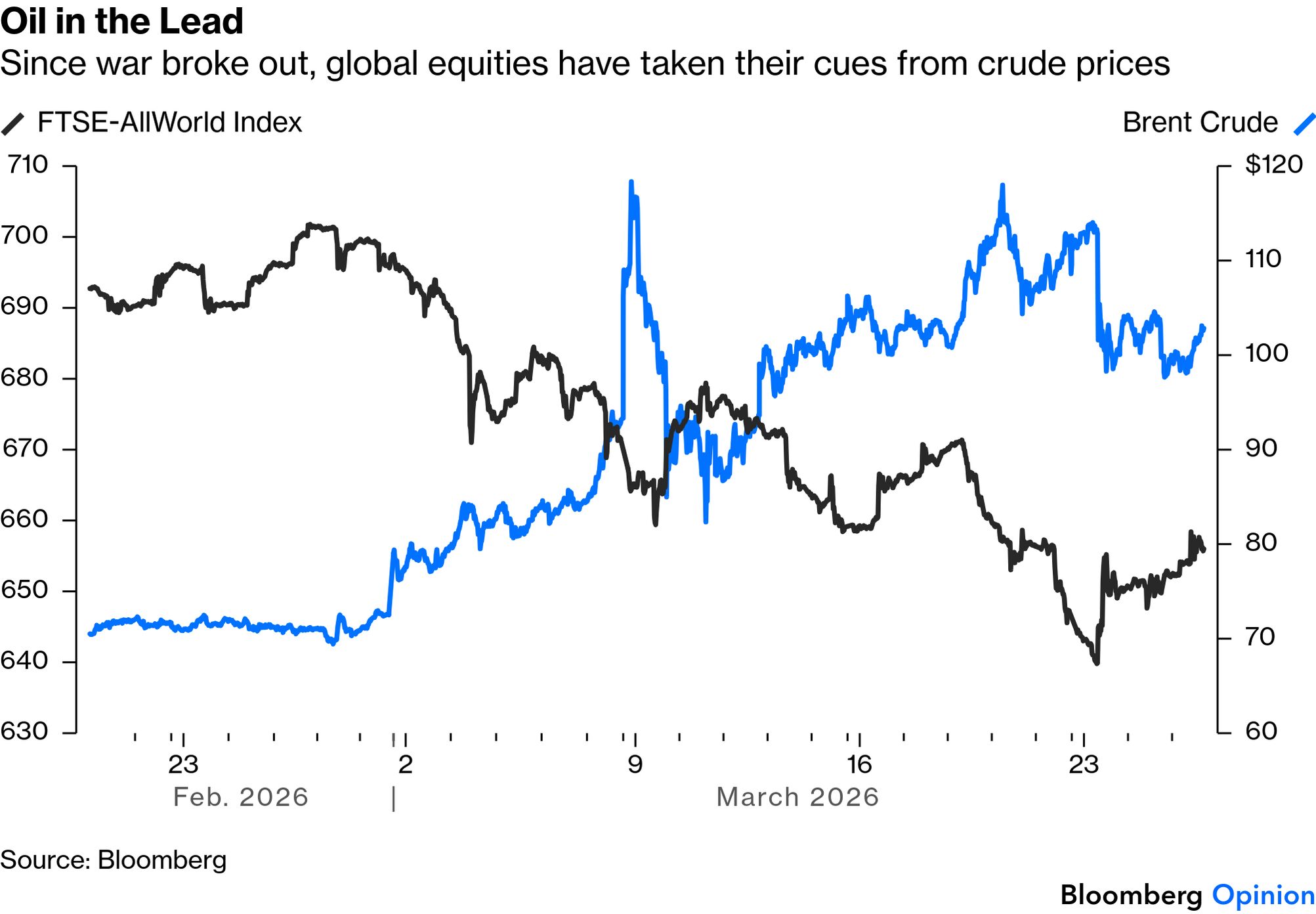

Adding this up, Tchir's instinct is " to fade this rally, because I struggle more to see Iran agreeing." Prediction market bettors think there's no better than a 50-50 chance of a ceasefire by the end of next month. Trump's announcement Monday of a delay to escalation was seen to make a ceasefire significantly more likely, but still no better than a toss-up. Since then, there has been trendless moving around the 50% level: Without a deal, the best available outcome may be for the US somehow to reopen the Strait of Hormuz by military force, which would probably take weeks rather than days — while the energy crisis for much of emerging Asia would deepen. While it's clear Trump doesn't want to escalate, the fact that the US is sending troops to the region, ready for a ground operation, shows it's a possibility. Oil and equity prices are roughly where they were a week ago, plainly driven by Gulf news, and unlikely to break out of their current (wide and jittery) ranges until the ultimatum expires and we have some clarity on a ceasefire. Brent crude has reached back above $100 a barrel several times now, a level that makes nobody in any petroleum-importing country comfortable: The likelihood is that the worst will be avoided (because it usually is), and that that this will be a buying opportunity. That's why the main markets haven't sold off far more. They will do so if Iran and the US can't between them find an exit ramp. The fire around private assets only intensifies. Already, JPMorgan's Jamie Dimon has warned of "cockroaches" in private credit. Now, another of the most revered figures on Wall Street, former Goldman Sachs CEO Lloyd Blankfein, warns Bloomberg of a "fire risk" in private markets. These are strong words, which testify to the alarm. But it's questionable whether anyone should be surprised. There's a strong argument that private credit and equity only look as good as they do because they can hide their volatility. We see public stocks and bonds oscillate in real time; private asset managers get to hold on to our money, and needn't tell us how it's doing until they exit.

Assuming they strike a good deal, this generally means they match the public market return, with much less volatility along the way, and this justifies far higher fees than they could generate for managing an index of public stocks. Is the deal really this good? Another big Wall Street figure, the founder of the AQR quantitative hedge fund group Cliff Asness, coined the term "volatility-washing." In other words, these investments are as volatile as anything else, but don't appear to be because they don't have to own up to it. With the sector now under criticism, Asness' words look prescient — but in a new post he denies that he was making any predictions. The original idea of private assets, and why they were picked up by very long-term investors like the Yale University Endowment under David Swensen, was that they suffered the disadvantage of liquidity. Those who could tolerate illiquidity (like endowments with an infinite time horizon) could therefore expect to profit from their willingness to accept that they might not always be able to get their money in a crisis. Asness contends that in many people's minds, this has been turned on its head: My contention is that today many investors, perhaps most, see the illiquidity as a "feature, not a bug," as it allows them to ignore market turmoil that they are in fact experiencing, but just don't have to acknowledge. That can actually be valuable if it makes you a better long-term investor. But it comes with a cost. A bug is something you get paid to bear through higher long-term returns. A feature is something you pay to receive through lower long-term returns.

That could yet lead to serious trouble should investors need to access their money in a hurry — the sector is altogether bigger than it was the last time this happened in a big way, in 2008. For now, Asness describes private credit's reported volatilities as "silly low compared to reality."

But he also denies predicting the sector's current problems. He didn't attempt to call timing, and was only making a long-term call. If he's right, he says, that means a slow grinding mild or major — again I can't do magnitude — disappointment vs. the past (and BTW, if you think the past was good enough, less might still be OK).

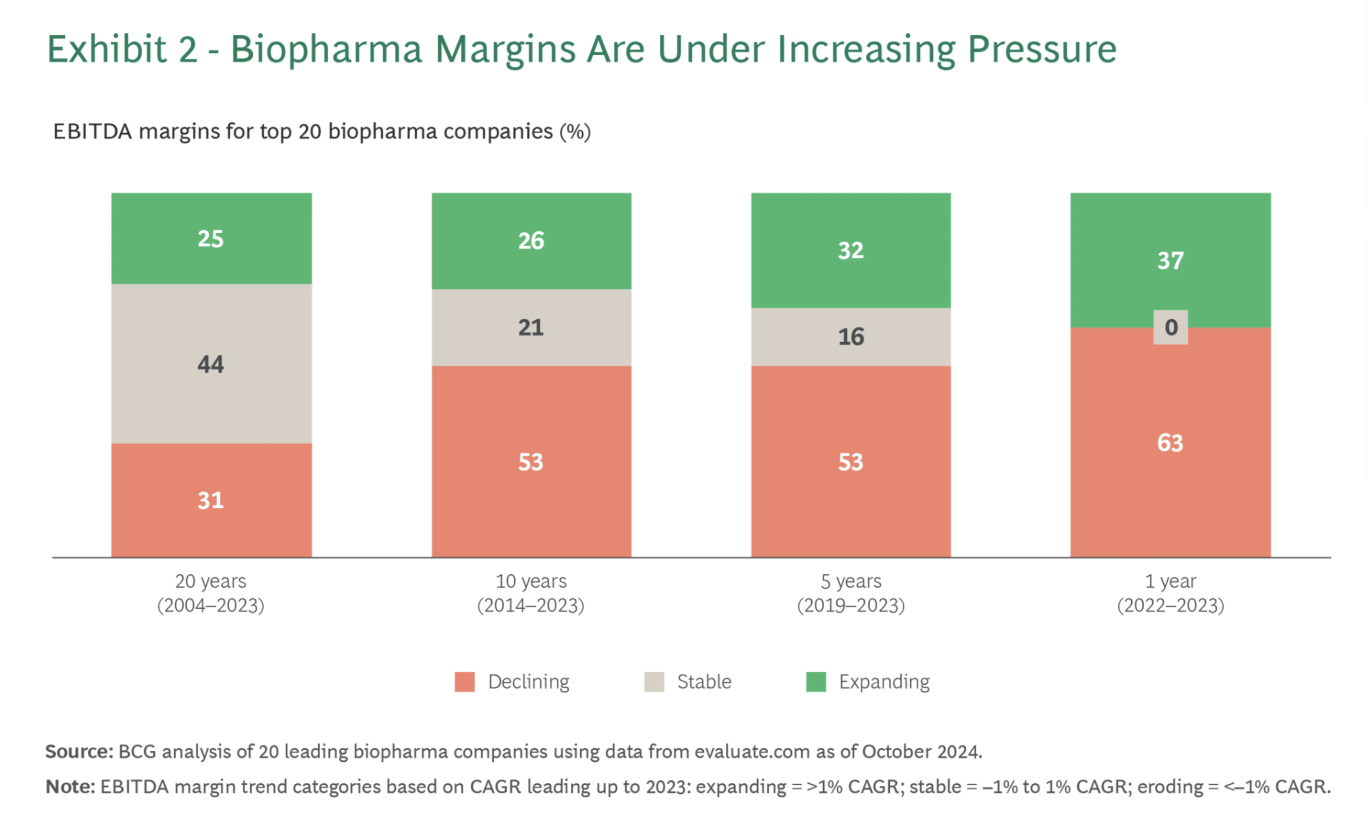

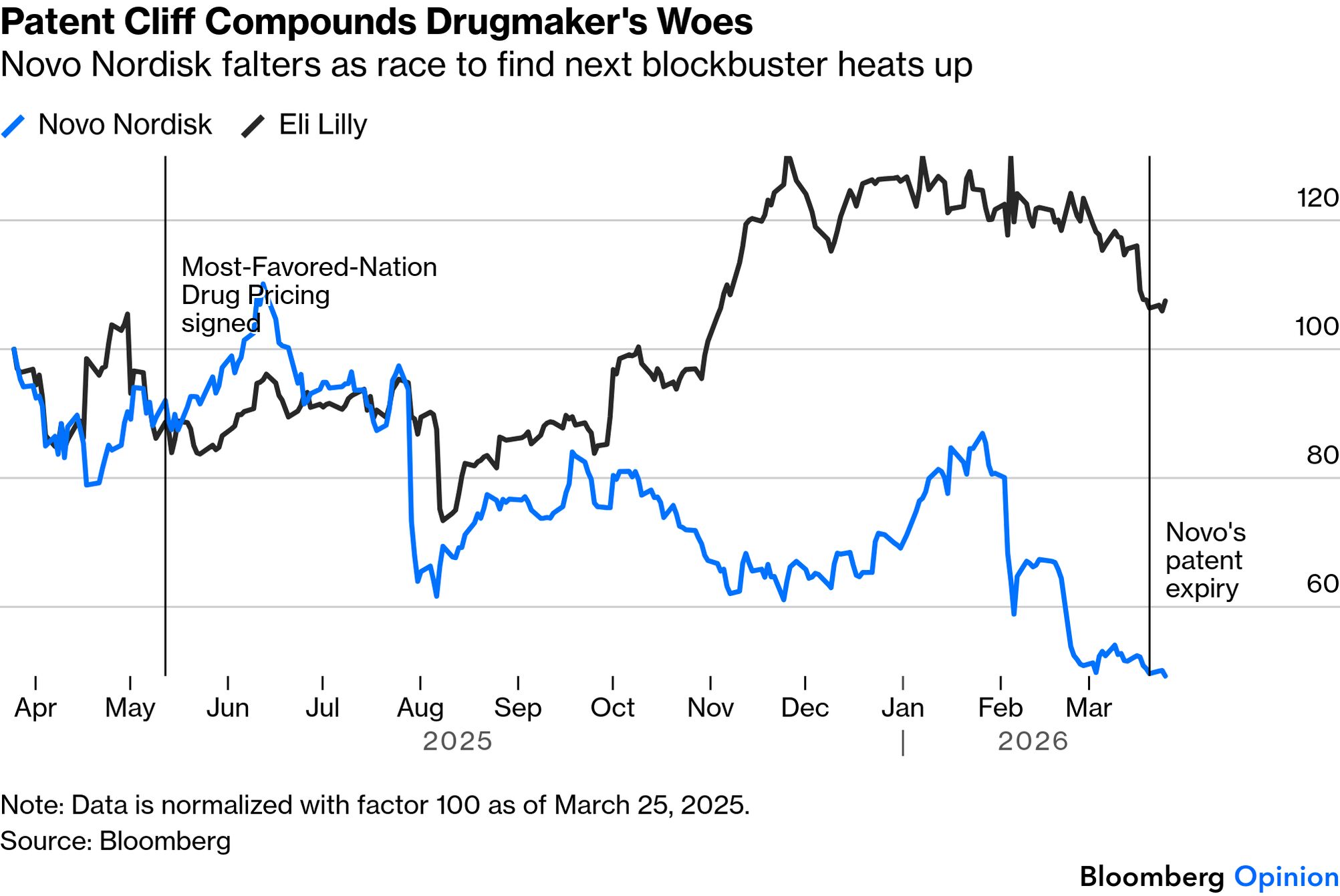

And at present, that will have to count as reassuring. Over the last 21 months, Danish drugmaker Novo Nordisk A/S's market valuation has fallen by nearly $500 billion. That's more than the entire market cap of Costco Wholesale Corp. or Netflix Inc. Over that span, the maker of the blockbuster weight-loss drug Ozempic has gone from Europe's most valuable company to an also-ran. All of this while obesity continues to be a pressing public health concern and demand for its products remains undimmed. The expiration of the company's patent for its obesity and diabetes drugs in notably India and China, which make up about 40% of the world's population, means Novo won't be catching a break any time soon. Lower-cost generics capable of delivering similar outcomes are likely to hit these two countries at prices as low as $14, a fraction of Novo Nordisk's branded offering: Historically, patent cliffs like this have devastated biopharma companies' margins, and investors plainly expect that this time will be no different. Clemens Moller of Boston Consulting Group estimates that by next year, the current wave of expirations will cover drugs worth roughly $150 billion in revenue. While companies have weathered previous cliffs, the stranglehold is not abating. Over the most recent 10- and five-year periods, the share of companies in the sectors with falling margins has jumped to more than 50%:  BCG points out that averages mask big differences between individual companies. Over the last two decades, margins at more than 30% of the world's top 20 biopharma companies have declines, 44% have kept them stable, and 25% have boosted profitability. In many cases, margin expansion has resulted from topline growth driven by individual products, not from controlling costs. That highlights the pressure generic GLP-1s are expected to put on weight-loss and diabetic drug manufacturers: Novo's rivals haven't been spared. Intense competition and Washington's drug-pricing policy are also chipping away at profits. This raises the stakes in the search for new blockbuster drugs. For example, the widely anticipated weight-loss pill cleared the US Food and Drug Administration's last hurdle in December. That should expand access to millions of patients who were previously excluded, either by expense or because they disliked injections. But there's only so much these pills can do for profits, especially compared with their far pricier predecessors. That helps explain the muted response from investors, who may already have priced in the pill's debut. The search for new discoveries continues. Eli Lilly & Co. is trialing a drug that it hopes will be twice as effective as its current flagship Zepbound. Results are due later this year, but Bloomberg Intelligence's Christos Nikoletopoulos says preliminary data suggest it could lead the weight-loss and diabetes segments. Lilly's fortunes could get another tailwind if its weight-loss pill orforglipron, currently under regulatory review in China, gets the green light. Bloomberg News reports that the progress of US-China talks suggests the process is broadly on track. Whether investors are buying into these prospects is another thing. HSBC's Rajesh Kumar suggests that Wall Street is too optimistic on Lilly: Our analysis of the obesity market suggests that prices, more than product features, are a greater driver of market share. Increasing competition from Novo as it fights to regain its foothold in the market is likely in the near term.

Intense competition is good for consumers, but not helpful to investors seeking to capitalize on pharmaceutical breakthroughs. More importantly perhaps, even the forecasts for the eventual revenue generated by the entire market are also slimming down. Analysts expect global obesity-drug revenue to reach about $120 billion by 2032, short of earlier projections by at least $30 billion. —Richard Abbey |

No comments:

Post a Comment