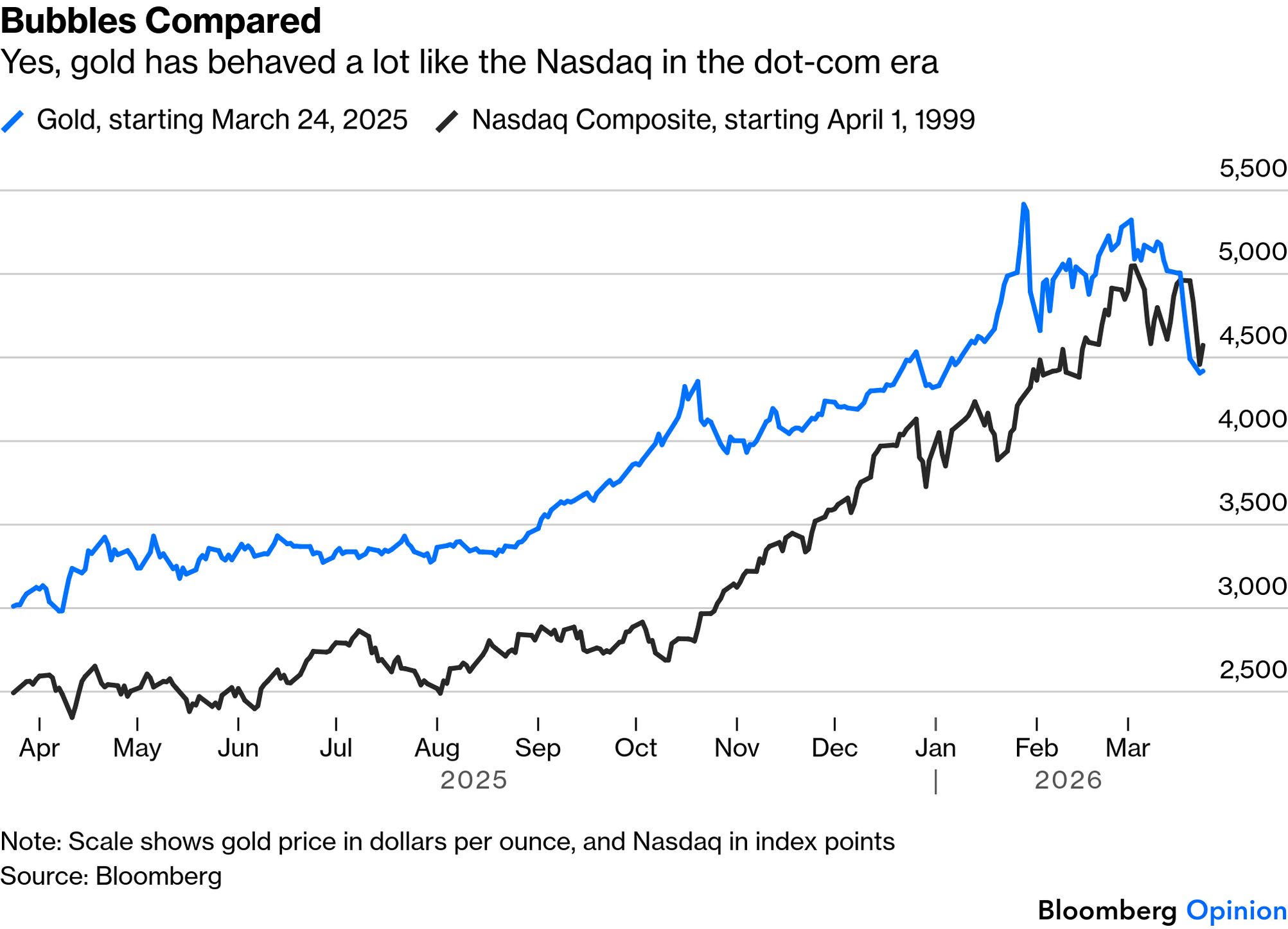

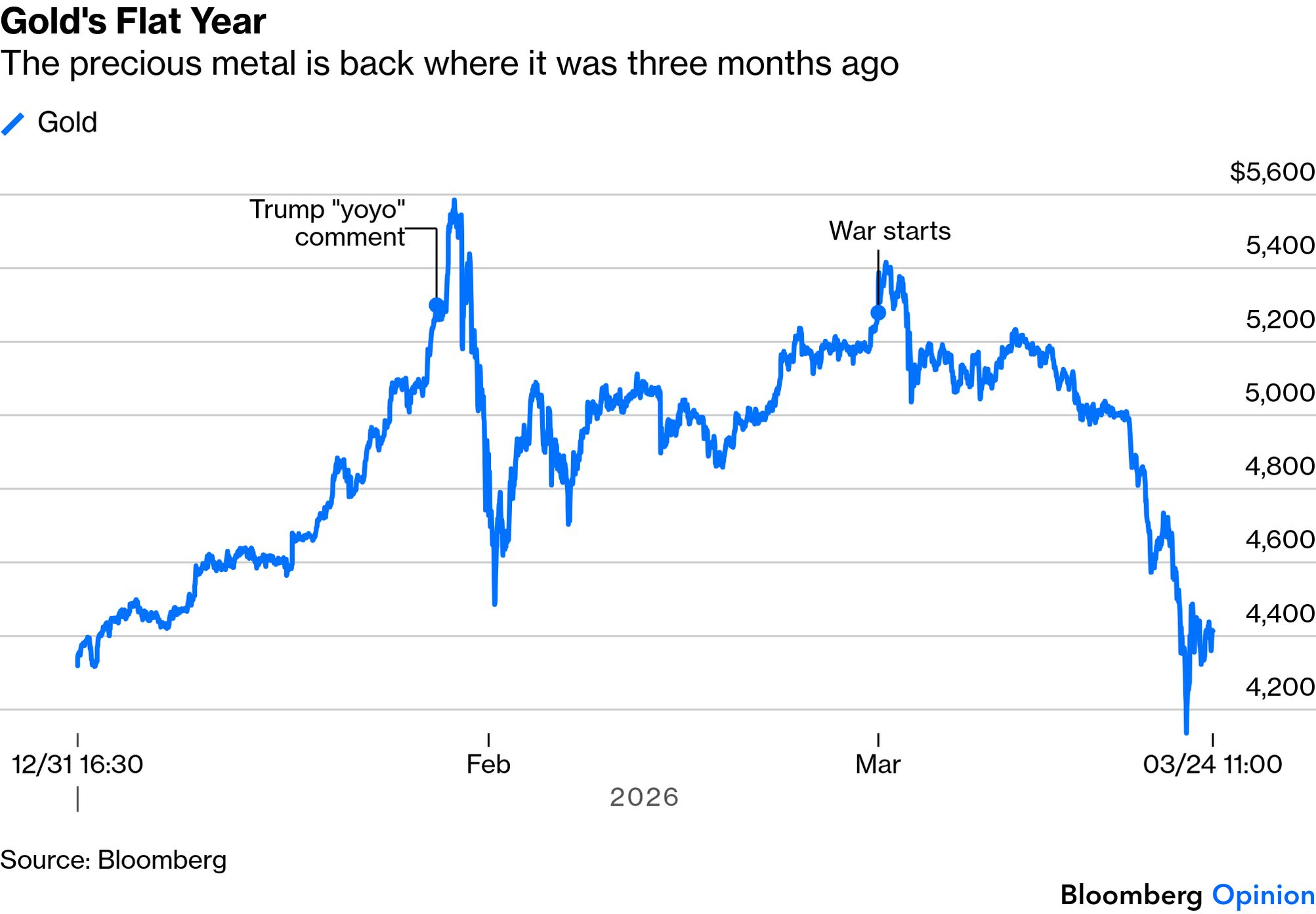

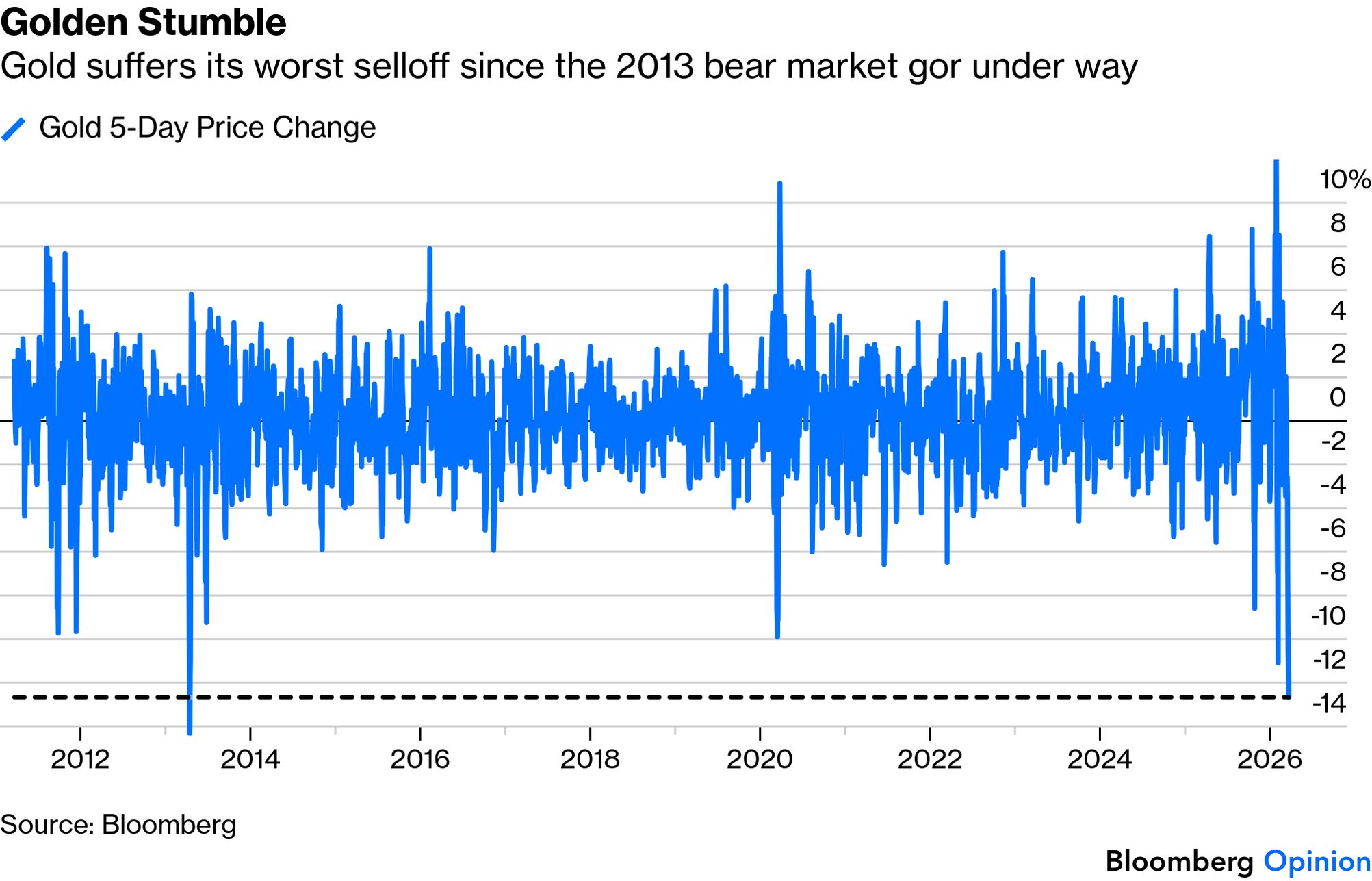

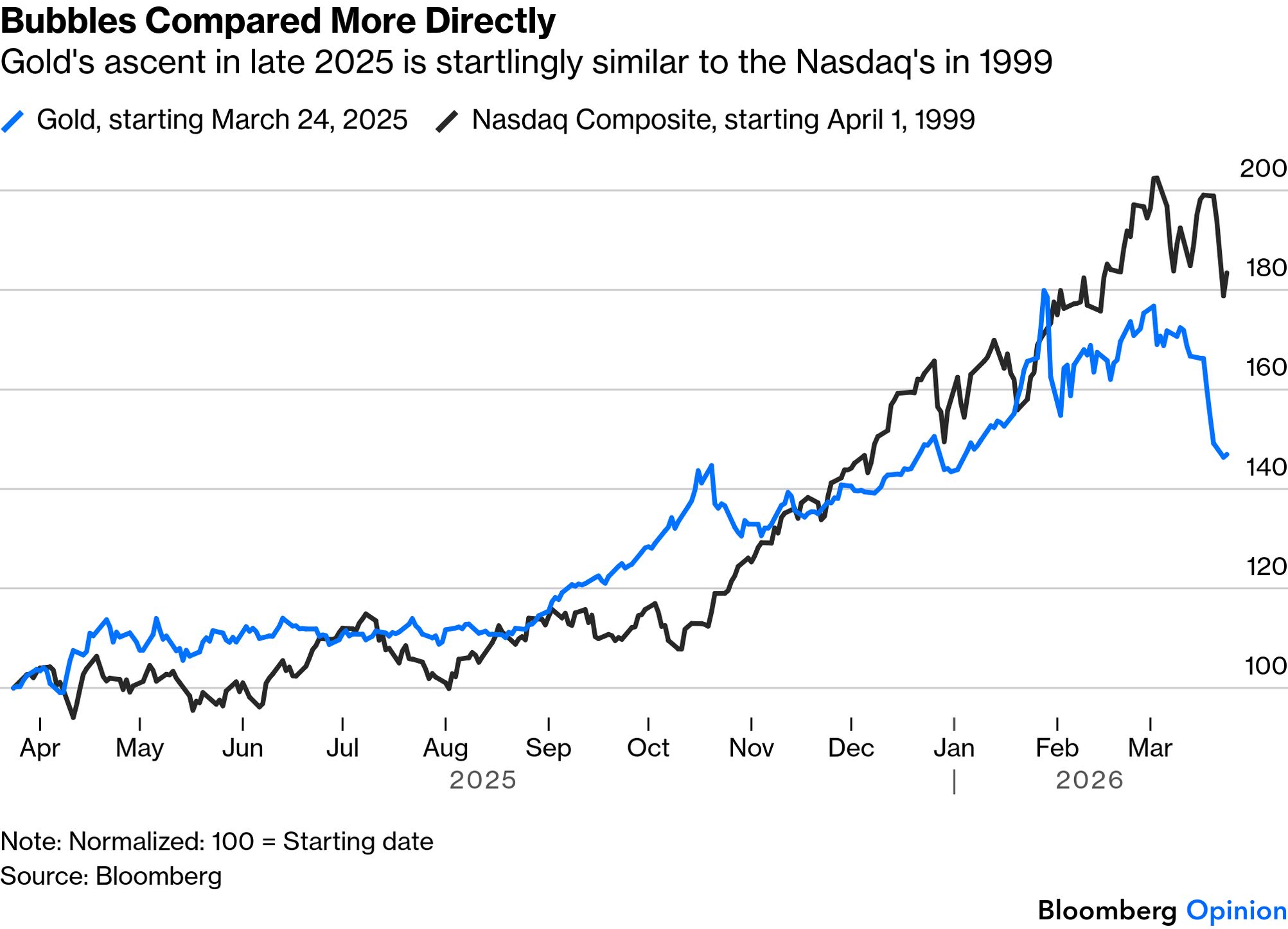

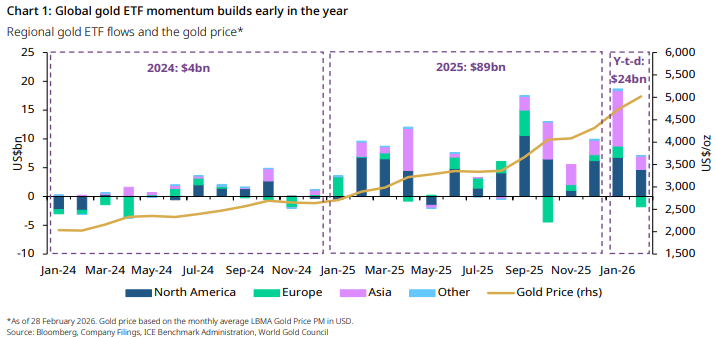

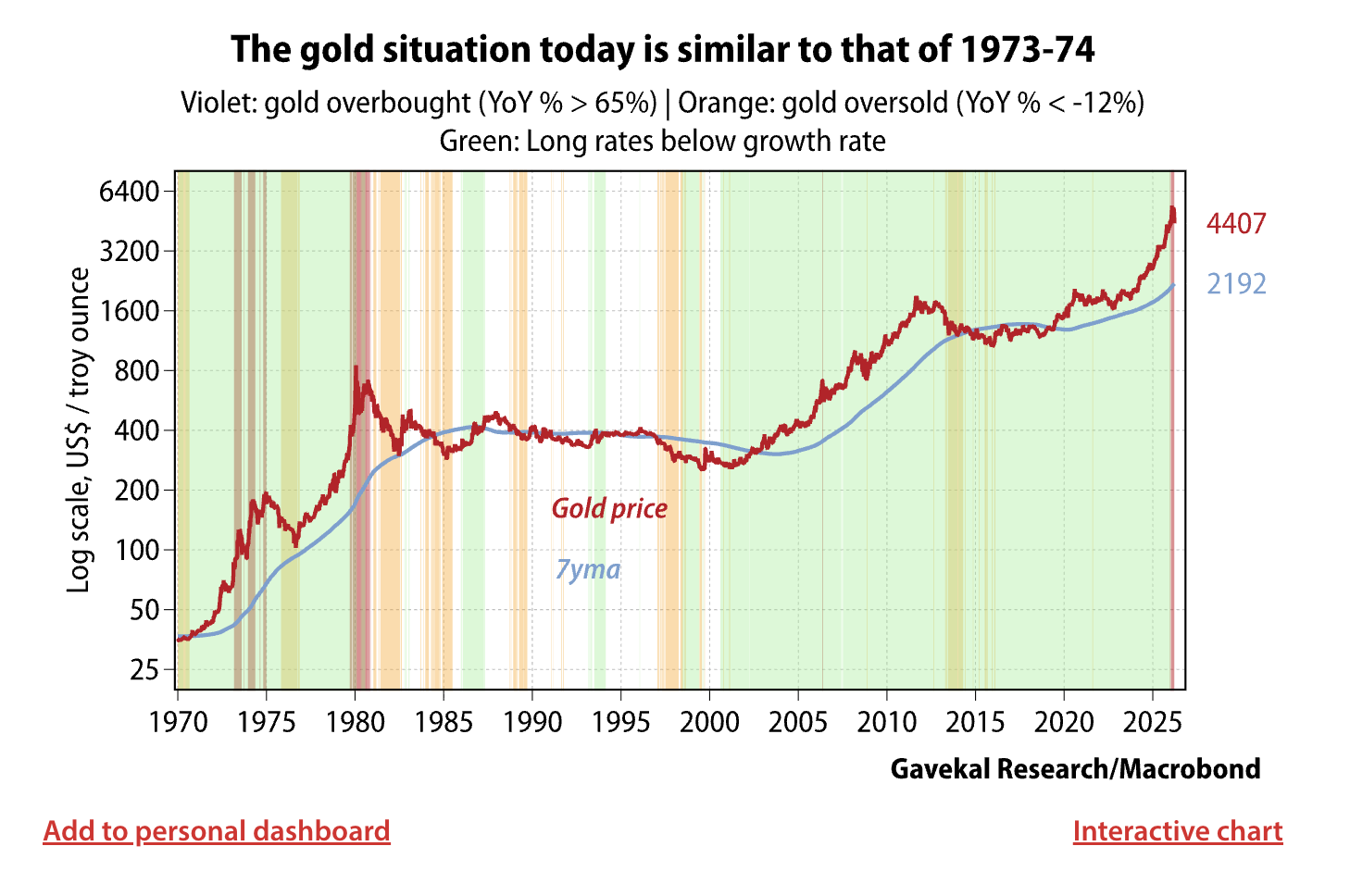

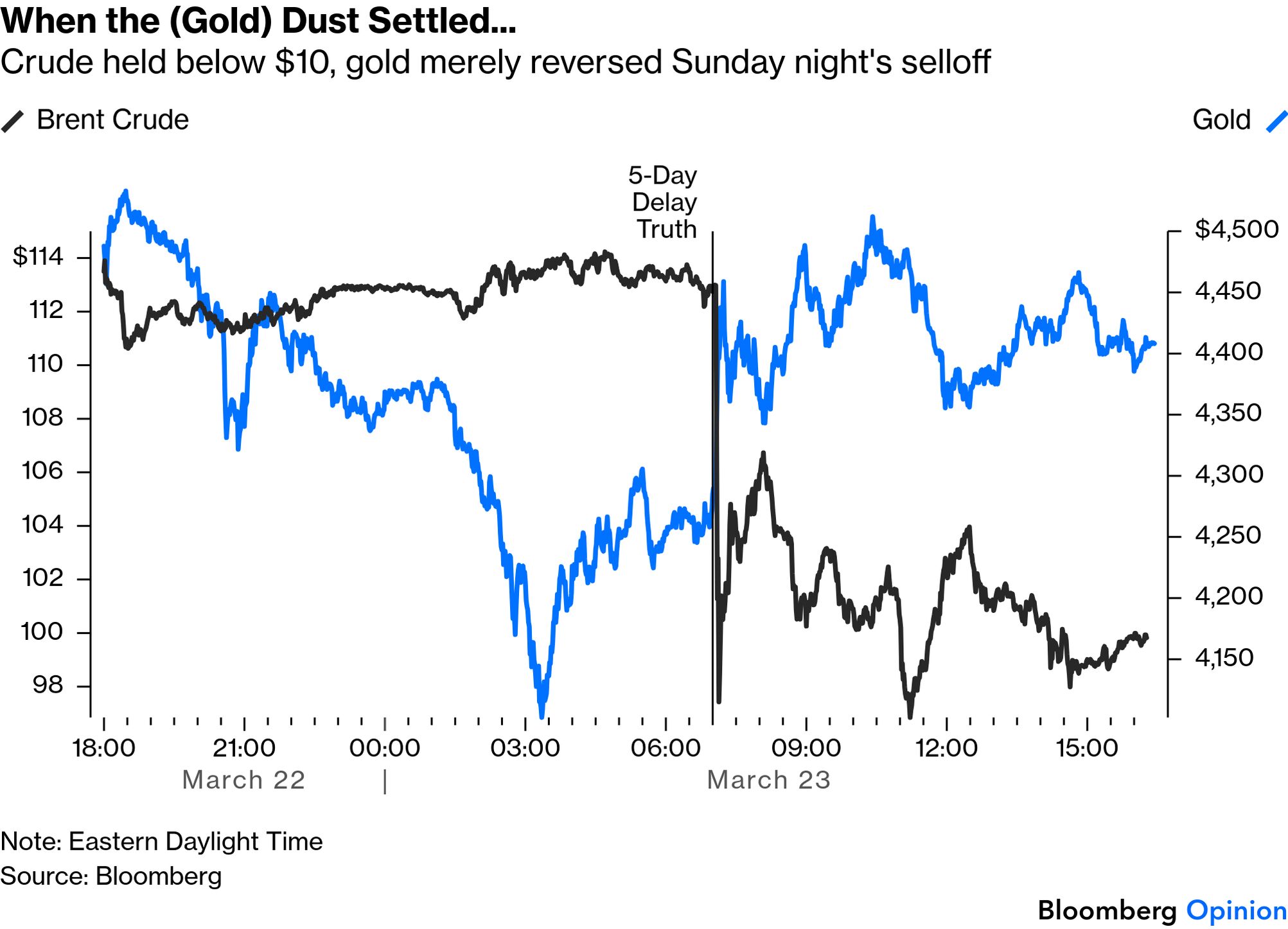

| The war in the Middle East has revealed that gold isn't much of a haven. It's almost exactly the opposite. The metal has lost about a fifth of its value since it surged to an all-time high in late January. At that point it was buoyed by the belief that the US administration was "debasing" its currency, which peaked when President Donald Trump said he was content to see the dollar move "like a yoyo." It also provided a haven from Russia's invasion of Ukraine. This war has been very different. Gold is roughly where it started the year, but only after an epic roller-coaster ride: The selloff from its January intraday peak to the trough earlier this week was an epic 27%, while the week leading up to Trump's post threatening to attack Iranian energy installations was its worst five-day decline since 2013. That discouraging precedent was the start of a lengthy bear market: For gold investors, the question is whether this conflict marks a tectonic shift in the underlying assumptions that have driven its rise (like the bear market of 2013, which came as investors grew to accept that the monetary easing that followed the Global Financial Crisis was not going to cause inflation), or a simple reaction to idiosyncratic factors tied to the war. Gold's trajectory in the last year looks startingly similar to the Nasdaq Composite in the lead-up to the bursting of the dot-com bubble, which offers little comfort:  By coincidence, both the Nasdaq and gold topped shortly after hitting the 5,000 landmark, and the two are shown on the same scale above. If we appease the statistical purists by normalizing them, with both set to 100 a year before their respective peaks, the similarities remain close. Gold has been around for centuries, and the Nasdaq covered a huge list of well-researched public companies. An 80% gain in a matter of months proved madness for the Nasdaq, and there's every reason to think it will be the same for gold: Another similarity with the Nasdaq bubble is that it appears to have dragged in the little guy, retail investors, at the top. Figures from the World Gold Council show record global sales of exchange-traded funds tied to gold in January. Asia, where investors were trying to avoid getting caught up in any downdraft from the dollar's decline, saw particularly enthusiastic buying: The simplest explanation of this selloff then, as Gavekal's Charles Gave and Louis-Vincent Gave note, is that gold was massively overbought in the lead-up to the war. In a period of market dislocation, overbought assets get hurt; people wanted to take profits, of which there were many in gold. The current situation is similar to the early 1970s: sharp price surges followed by sharp corrections, then another sharp rise once the recession was over. Gavekal illustrates this using a log scale: Does this point to a path back for gold once geopolitical tensions ease? The rebound in the price after Trump's decision on Monday to delay planned attacks on Iranian energy infrastructure underscores how eager gold investors are for an off-ramp: But for now, the Gavekal analysts argue that investors have more pressing issues : In this crisis, gold is showing itself not to be an "anti-fragile" asset and has added more volatility to portfolios than most investors likely expected. As such, selling pressure is likely to persist until overall market volatility abates and/or until companies and countries feel comfortable returning to "just in time" inventory management rather than "just in case."

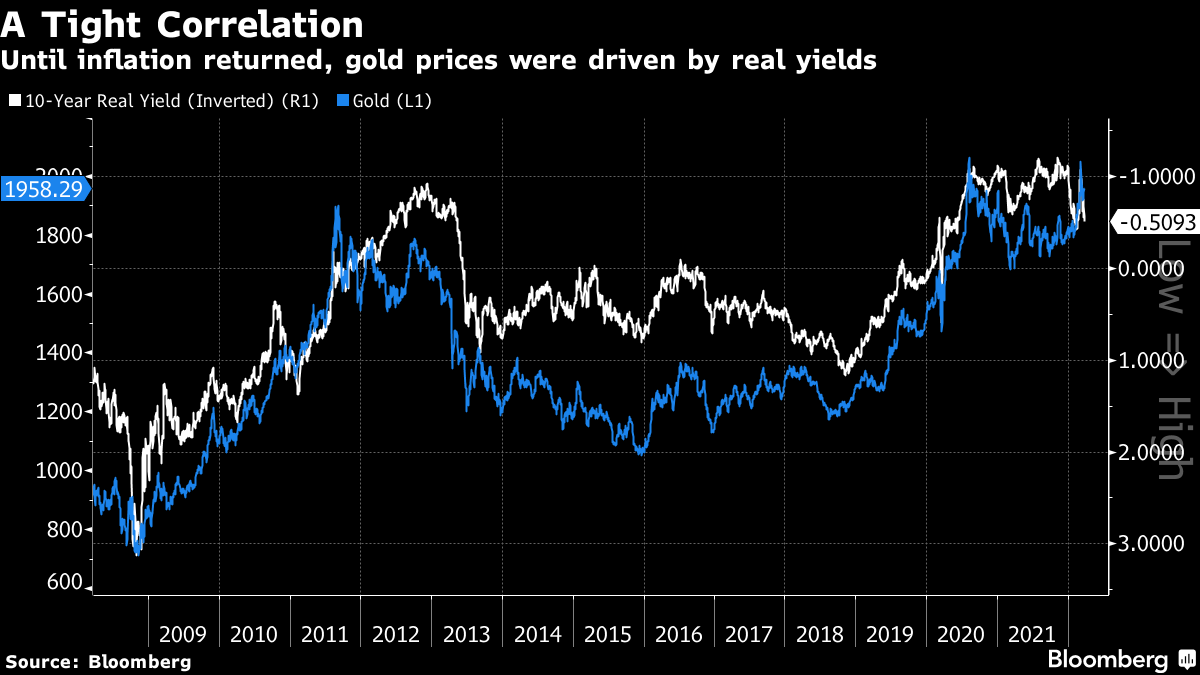

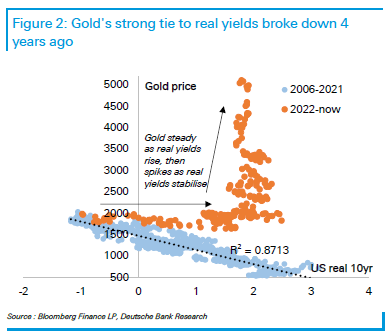

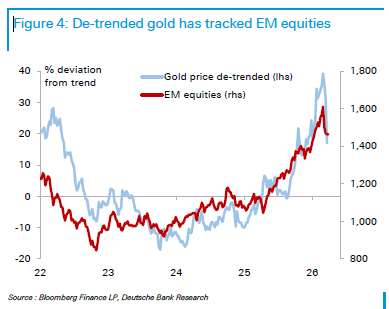

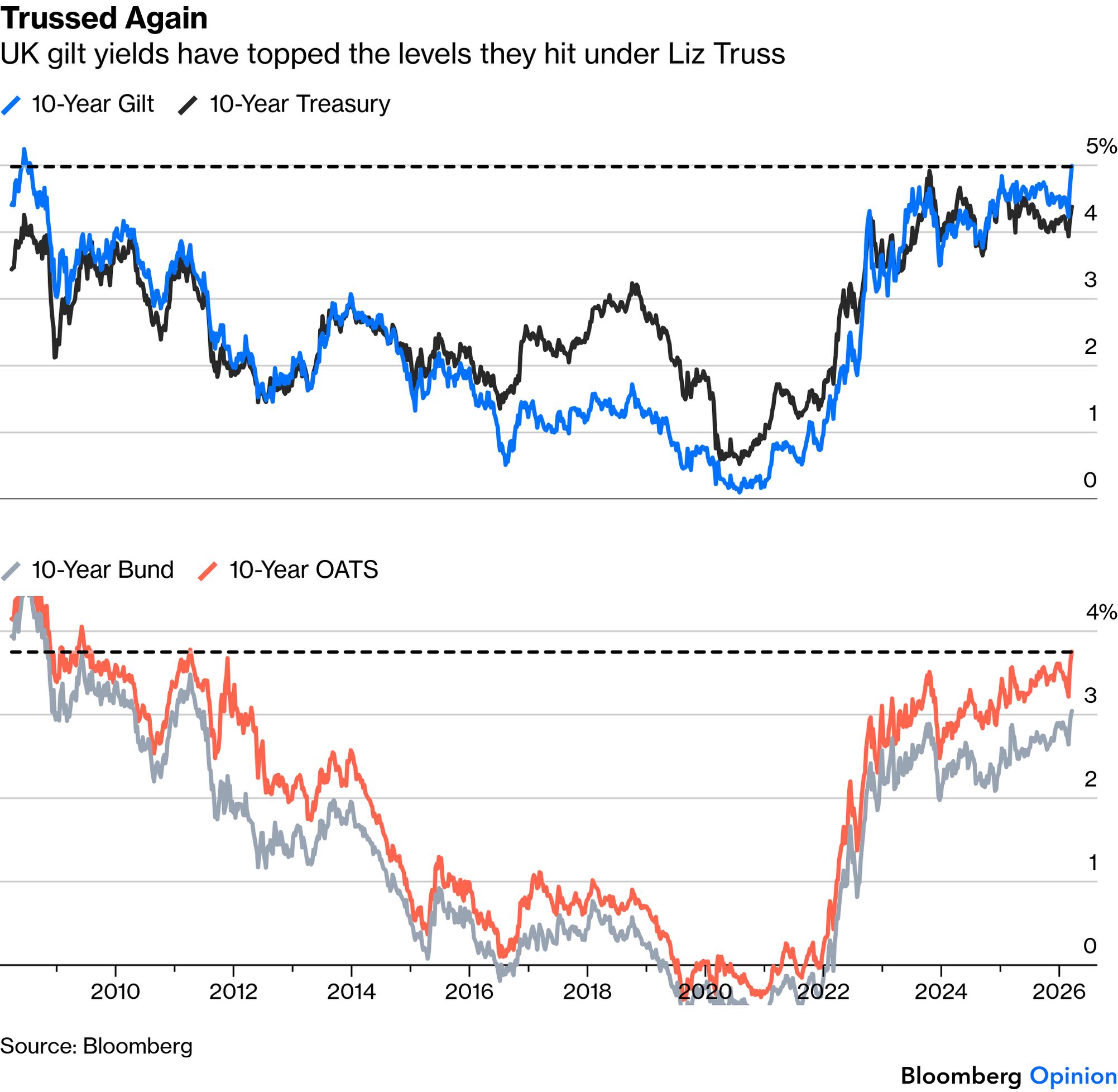

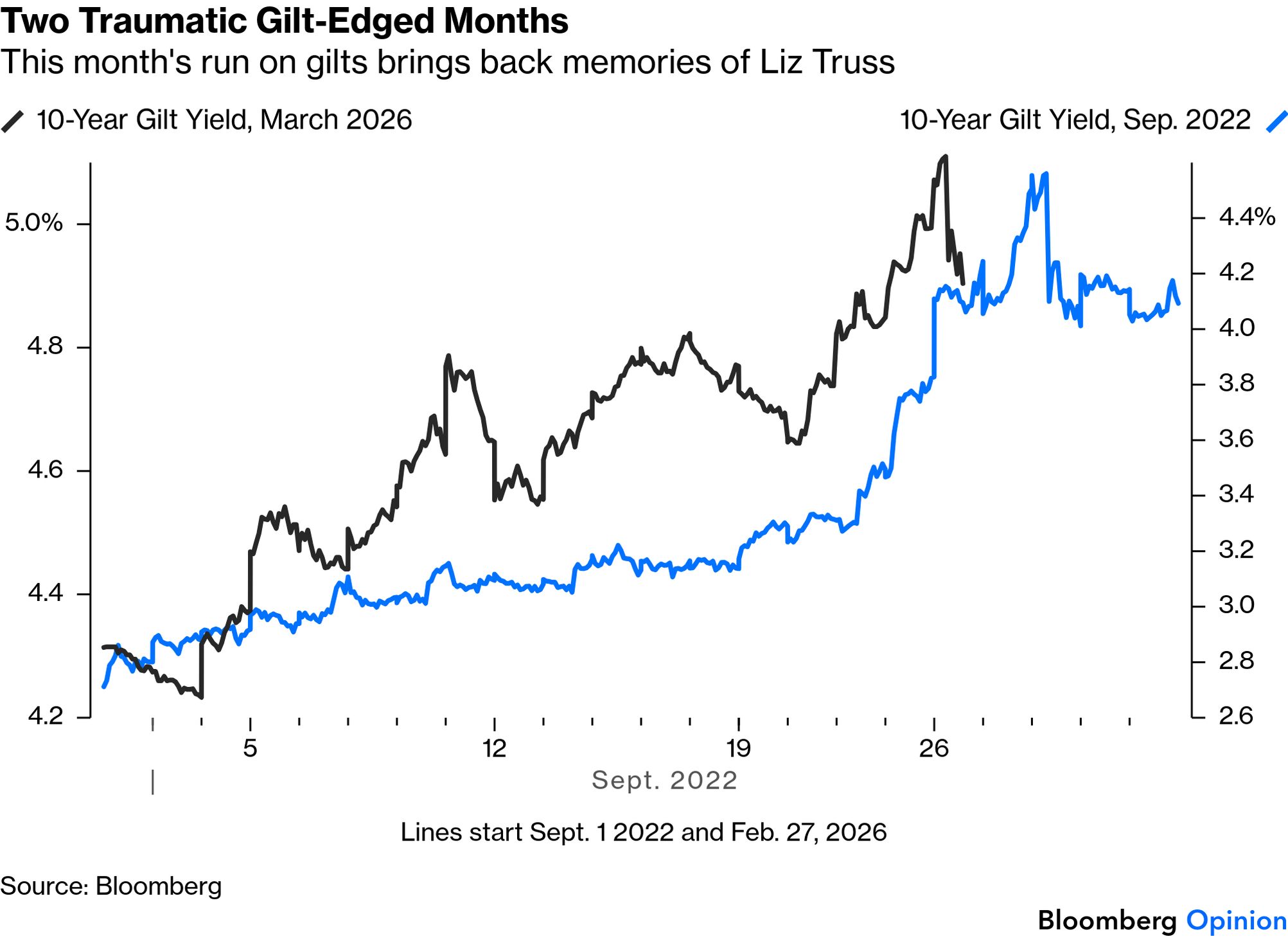

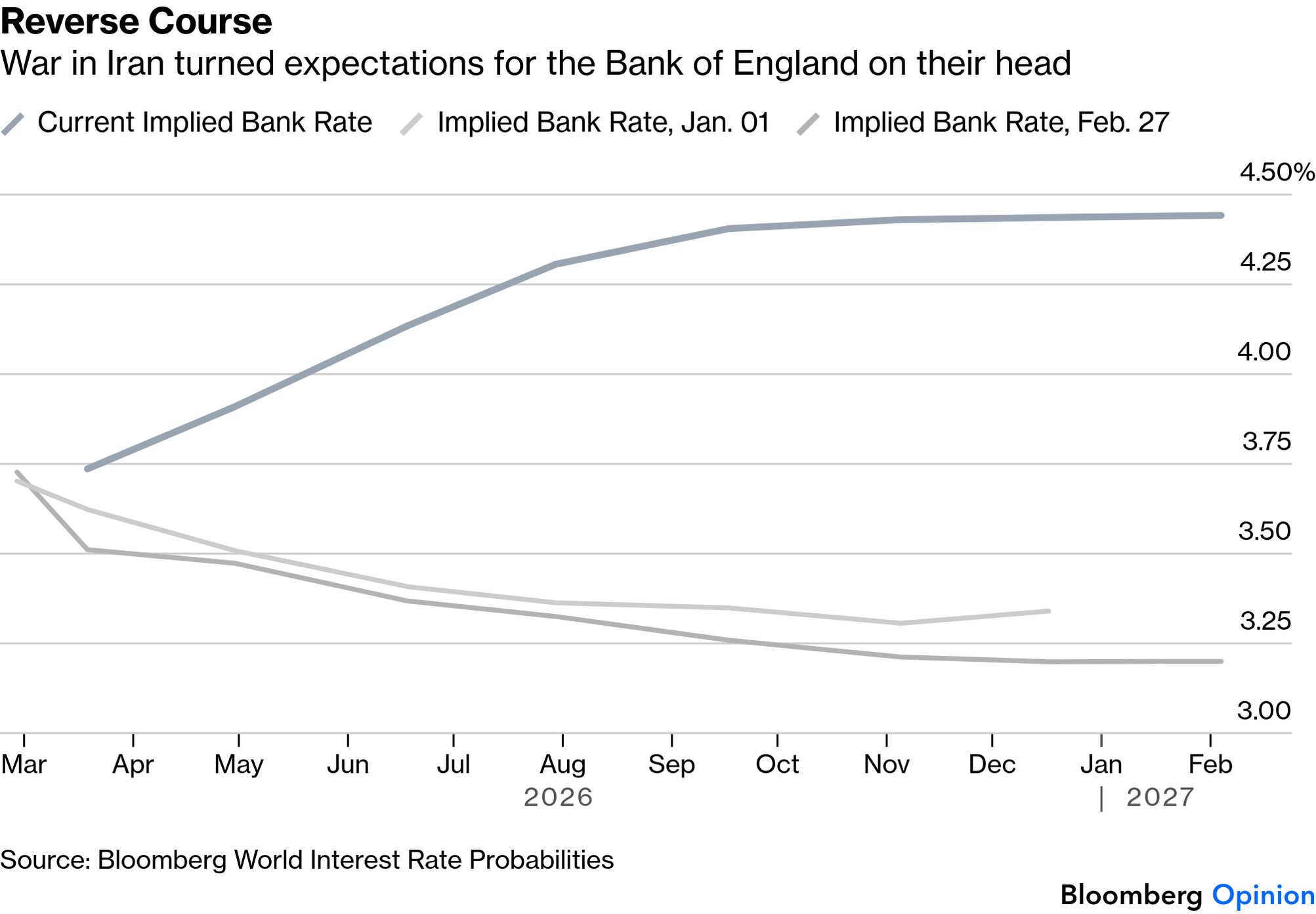

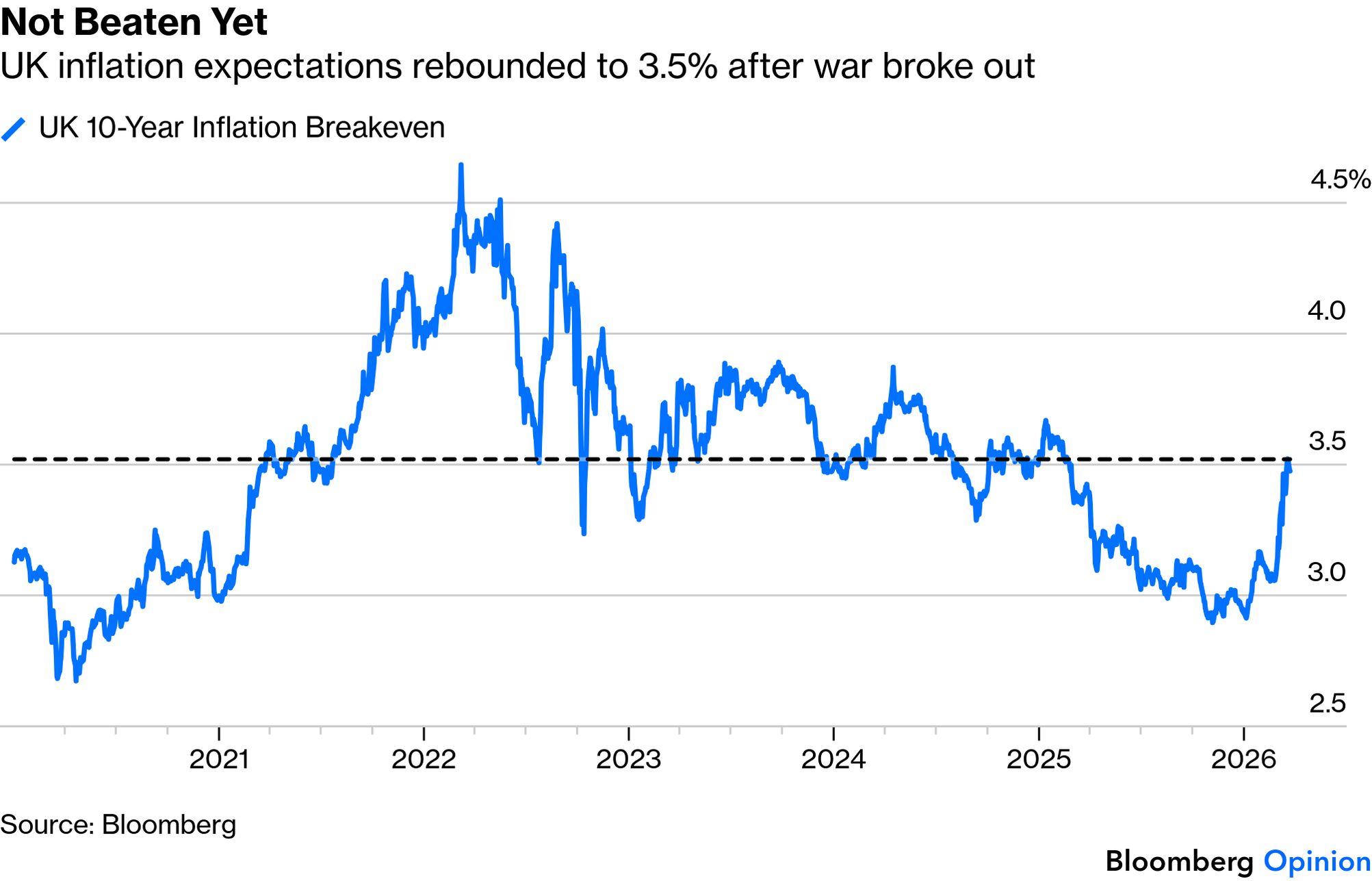

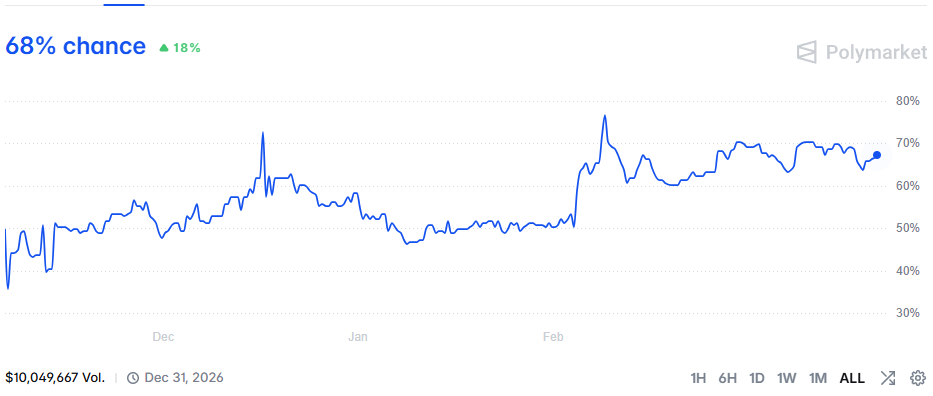

Another argument is that gold investors, like many others, have been flummoxed by the return of inflation. From the GFC through to early 2022, inflation was barely an issue, and gold had a very strong inverse correlation with real yields, illustrated in this chart from the terminal: That correlation disappeared once inflation returned. The difference is dramatic, as illustrated by Deutsche Bank AG's Tim Baker: Instead, over the last few years, the gold price began to move with US nominal yields and, strikingly, with emerging-market stocks — the very antithesis of a haven asset: On that basis, gold's surge over the last six months demonstrated that it had come unmoored from any sensible fundamentals. The shock of the war provided the necessary slap in the face. Another explanation is the change in interest-rate expectations. The war has dampened rate-cut hopes amid surging inflationary pressures. That's not great for the economy, but neither is it good for those who had been eagerly betting on the "debasement" trade. Now that the conflict has left investors in doubt, they are pulling back from gold — even though inflation expectations are rising. The impending arrival of a new Federal Reserve chairman — probably the president's nominee Kevin Warsh — adds a further argument about debasement and excessive easing. New Fed chairs are generally tested by the market, and have to prove their willingness to be tough. For all the pressure to cut from the White House, the pressure in the other direction from markets could be stronger. If gold's strength really was a rational way to hedge against debasement — which is questionable — then that would explain why it has pulled back. A further twist is the dollar, which has an inverse relationship with gold. It has been treated as a haven and has strengthened during the war. A prolonged conflict would likely continue that trend, spelling more trouble for gold. On this account, gold investors are right to feel the ground shift if the war drags on. —Richard Abbey Britain is approaching the 10th anniversary of its fateful decision to "take back control" in the Brexit referendum of 2016. It doesn't feel that way. Of all the developed economies, the UK has suffered more collateral damage than anyone else from the hostilities in Iran. Severing ties with the European Union, still dangerously dependent on Russian energy, and attempting to move closer to the American orbit haven't helped. The problem shows up in the most important market for politicians. The yield on 10-year gilts briefly broke 5% on Monday, before Donald Trump's announcement of a delay to bombing raids prompted a switchback. Rising yields have been universal, but UK yields are now the highest of the developed economies, and they alone have come all the way back to their highs from before the GFC in 2008: That means that the bond market's revolt has gone beyond even the extremes that ended the short premiership of Liz Truss back in 2022. The intensity of the pressure on gilt yields in the last month is distinctly reminiscent of that episode. The speed of the ascent has not been as great, but this is plainly a damaging shift: This revolt, however, is less directly about the government's fiscal plans, and more about the central bank. Expectations have turned 180 degrees since the bombs started falling on Tehran. At that point, the market was pricing at least two 25 basis-point cuts in the Bank Rate by the end of the year. Now it's pricing at least two hikes: That's because inflation expectations have surged, giving the Bank of England little choice but to hike, even with a sluggish economy that otherwise would require cuts: While inflation forecasts have risen in response to this month's jump in crude prices, the UK has a very specific issue. The spread of UK inflation break-evens over US equivalents narrowed last year, as the Labour government tentatively gained confidence on the markets after a bad start. That's over: Politics are also a problem. Betting on prediction markets is fast generating controversy, but needs to be taken seriously, particularly when assessing a situation as well-publicized as the British premiership. Polymarket currently puts the odds that Sir Keir Starmer will be out as prime minister before the end of this year at 68%. That number has been steadily rising. His most likely successors all appear to be to his left, and less to the gilts market's liking: It's hard to disagree with the assessment that Starmer is in deep trouble, even though his party has a big enough majority that there is no need for it to call a general election until 2029. The inaugural opening sketch of the British version of Saturday Night Live skewers the man, and dramatizes his difficulties dealing with Trump. The president then rubbed salt in the wound by posting a link to the skit on social media. Free diplomatic advice: Downing Street should not, repeat NOT, respond by posing the last few dozen times the US version of SNL has lampooned Trump. In the meantime, this looks like a no-win situation. There should be money to be made for investors once Starmer, or his successor, takes back control. But you might have to wait. |

No comments:

Post a Comment