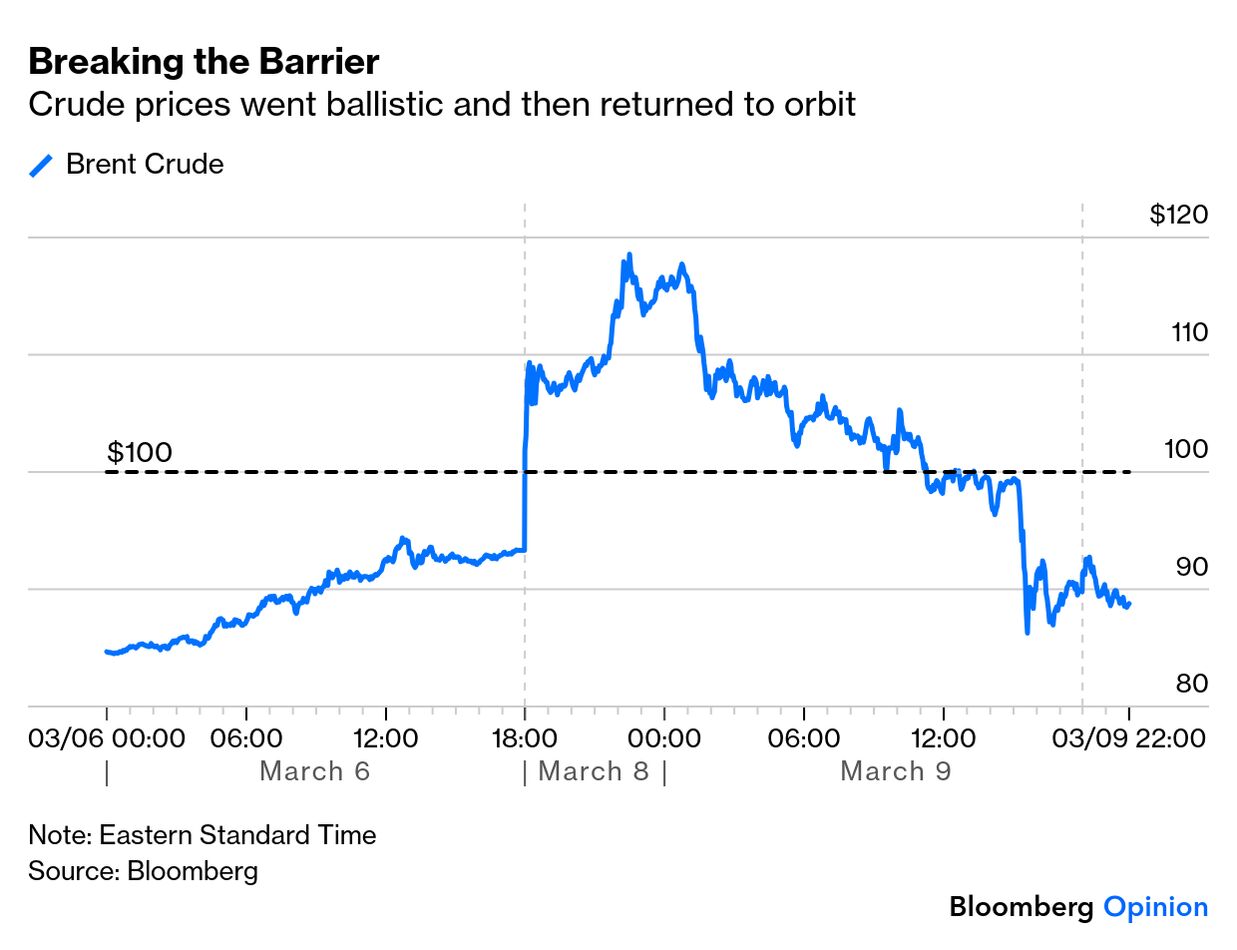

| To get John Authers' newsletter delivered directly to your inbox, sign up here. - So far this week, Brent crude surged from $93.50 to $118.90 — and back to $88.

- President Trump has predicted that the war with Iran will resolve "very soon."

- US stocks gained on this news — the Nasdaq is now higher for the month.

- Asian stocks bounced Tuesday after a serious selloff.

- AND: Putting out the fire with a few songs about oil.

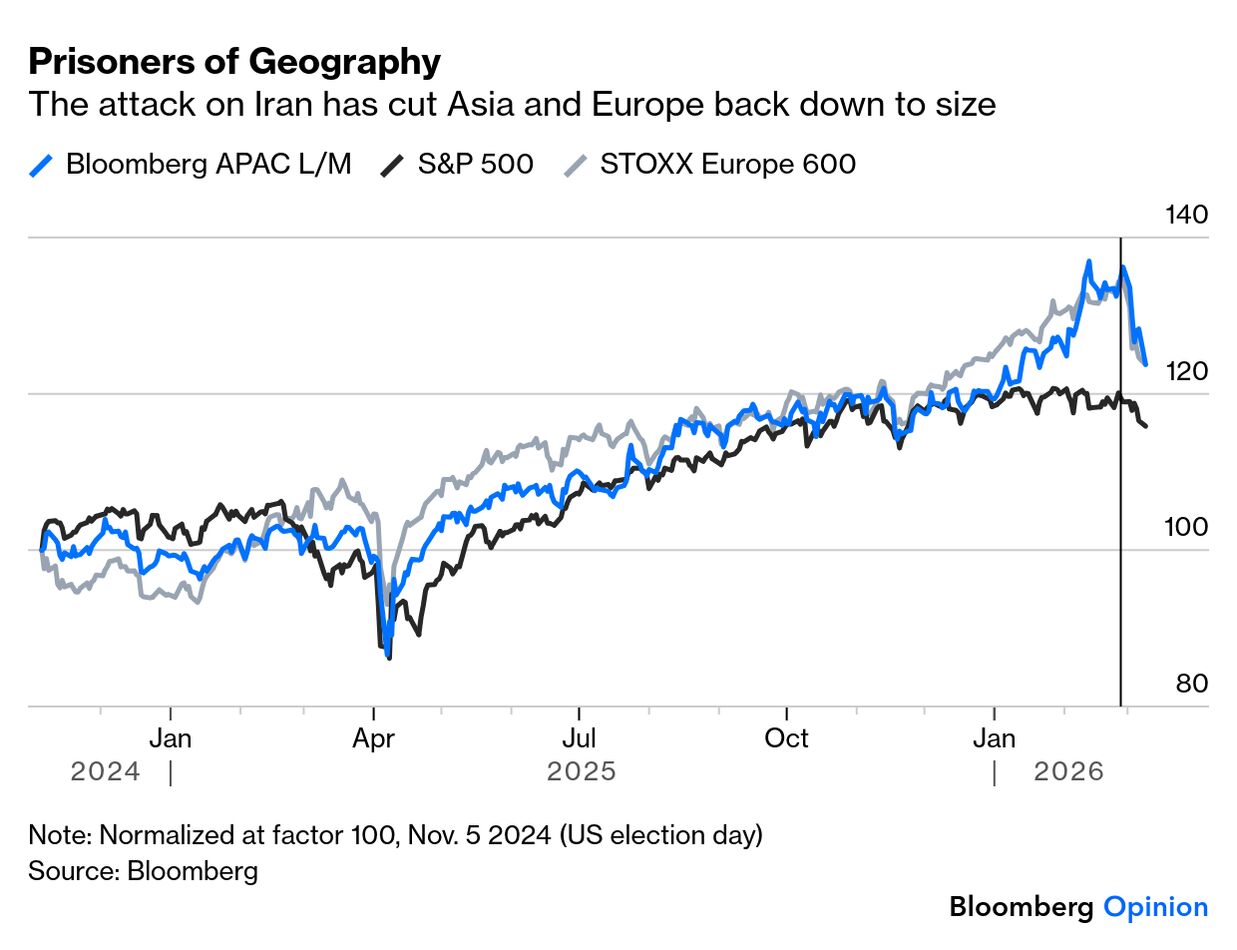

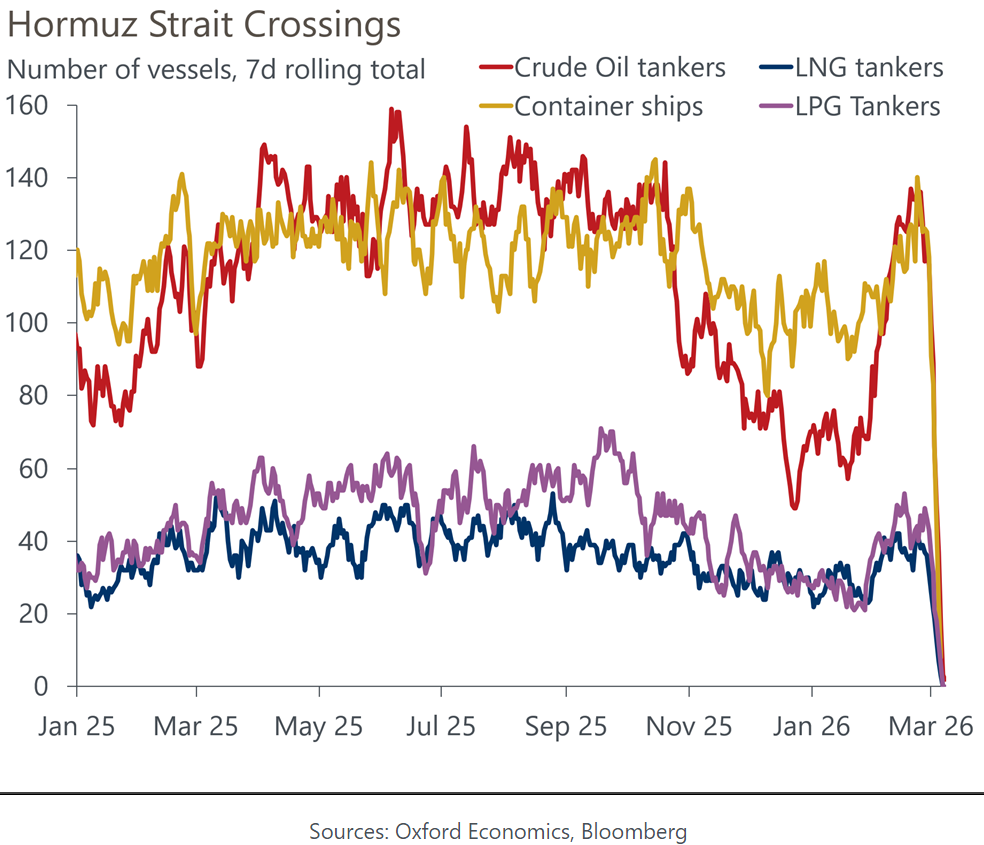

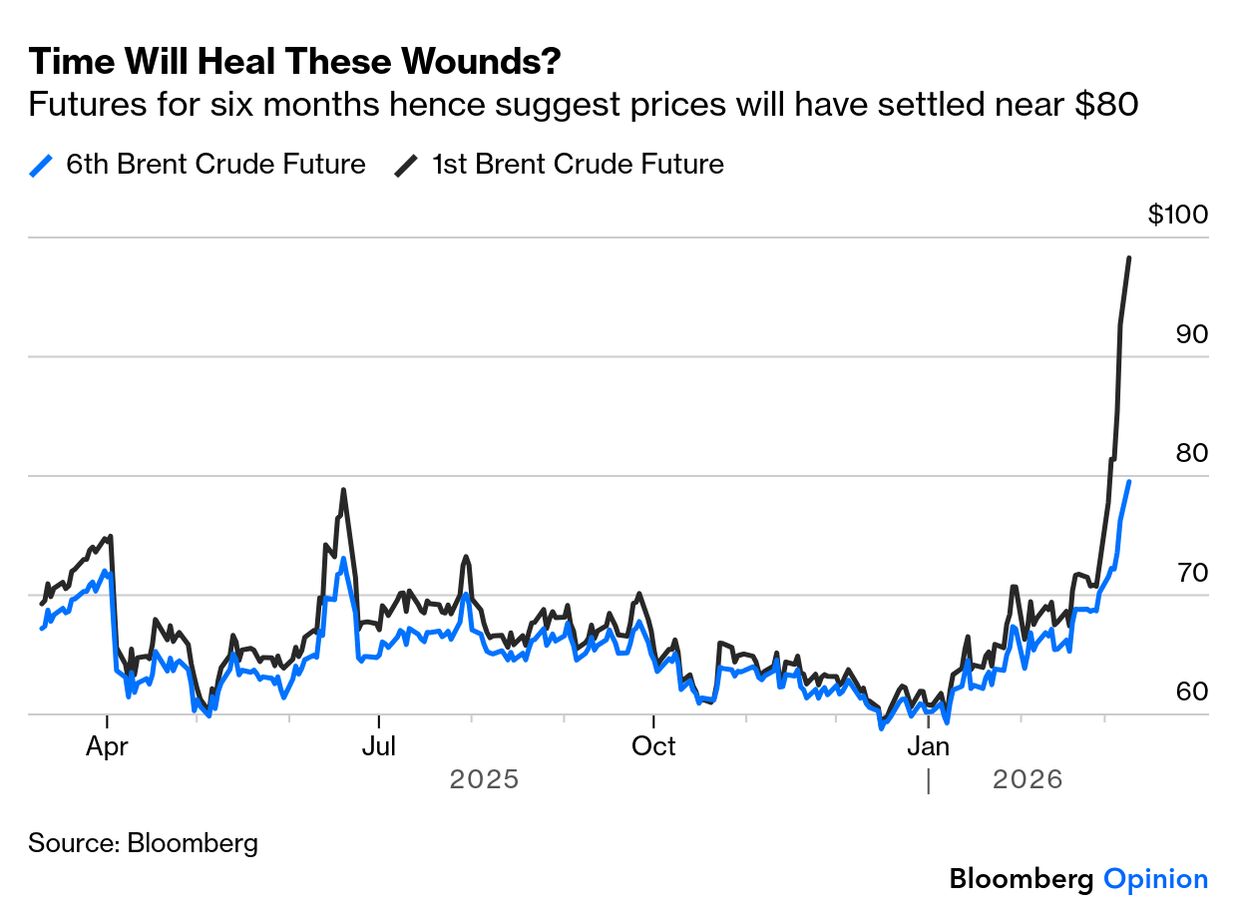

Years go by with less activity in the oil market than we have witnessed in just the first day of this week. The lingering question is whether all's well that ends well. Crude prices surged almost to $120, in a sharper and more sudden rise even than ever occurred in the early days of the Ukraine invasion. Is it more important that traders took the price this high, or that they swiftly thought better of it, and brought it back below $90?  These are unusual events and while they were in part driven by exceptionally volatile news flow, it would be misleading to try to label the chart with events to explain the moves. Iran's choice of the son of the late Ayatollah Ali Khamenei as new supreme leader seemed a bad sign of intransigence to open the day. Reports that the G-7 was prepared to tap oil reserves if needed helped to bring the price under control, and then President Donald Trump's comment that the war would be short prompted the drop to $90. But it's impossible to explain all of the moves with news flow. Sentiment is driving this, and some traders were evidently willing to panic. But it's equally true that they weren't comfortable leaving oil above the landmark of $100. Oil is naturally giving a lead to other markets. Asian exchanges, open when the oil spike was at its worst, took severe damage, while the main US indexes were flat. Overall, the reaction in stocks continues to be surprisingly calm given the extreme goings-on in commodities markets. Geography has asserted itself with Asia and Europe, physically close to the conflict and in need of energy imports, sustaining greater losses than the US, which is neither. But all the last week has done is bring the rest of the world to heel somewhat. Asia and Europe have still outperformed the US since the election of Trump in November 2024: Despite an exceptionally alarming spasm as trading opened Monday in Asia, then, markets remain orderly, and are still not greatly impacted by the terrible events in the Middle East. What would change this? And what if anything would provide a clear signal that it was time to buy? Disruption to oil supply is, we all know, critical to turning a geopolitical shock into a more serious economic event. That has already happened. As this dramatic chart from Oxford Economics demonstrates, trade through the Strait of Hormuz has dried up: The issue is how long supply will stay stoppered up. And markets remained moderately positive on this front, even before Trump's comments were taken as evidence that he did not have the political appetite for a prolonged conflict. The 6th and 1st month futures on Brent crude, covering the price of a barrel at those points into the future, have been trading close together for most of the last year, but now a gap has opened. Futures are still pricing oil to be just around $80 in six months' time (about 10% above its $72 price on the eve of the conflict) — which would be significant, but not the economic game-changer that $120 oil would be: We need to keep following developments on the war and on oil supply. Beyond the duration of the shock, we also need to monitor the impact on central banks and on the macroeconomy. Societe Generale's Manish Kabra lays out the criteria as follows: An exogenous shock lasts beyond a week, but oil spikes usually peak in three months. That's the timeline and only two things matter: 1) shock duration and 2) the Fed's reaction function.

Alternatively, Henry Allen of Deutsche Bank suggests that for a risk-off bear market to follow an oil shock, three conditions need to be met: 1. Large and sustained oil price spike: An oil price spike of at least +50-100% that is sustained over several months.

2. Hawkish policy response: The shock forces a sharp, hawkish pivot from central banks to fight the resulting inflation (e.g. 1979, 2022).

3. Broader macro damage: The shock is big enough to tip an already-slowing economy into recession.

The duration of the shock will reveal itself over time, while the first hard macro data that will include the war's impact are still weeks away. So the chances are that next week's meeting of the Federal Open Market Committee is going to be far more interesting than at one point seemed likely. The Fed is currently in its pre-meeting quiet period, but any indication that it will respond hawkishly will have immediate repercussions. If it gives clear signs that it's more worried about the "stag" side of the stagflation that can follow an oil shock, markets will be that much calmer. Absent clarity on the length of the war, and on the central banks' likely response, it's impossible to say whether the market bottom is in. Monday's extraordinary gyrations in oil settled nothing, beyond showing that there's a lot of residual optimism in the US, which is still taking these events in stride. Credit Where Credit's Due | |

No comments:

Post a Comment