Your Post-Earnings AI Playbook VIEW IN BROWSER

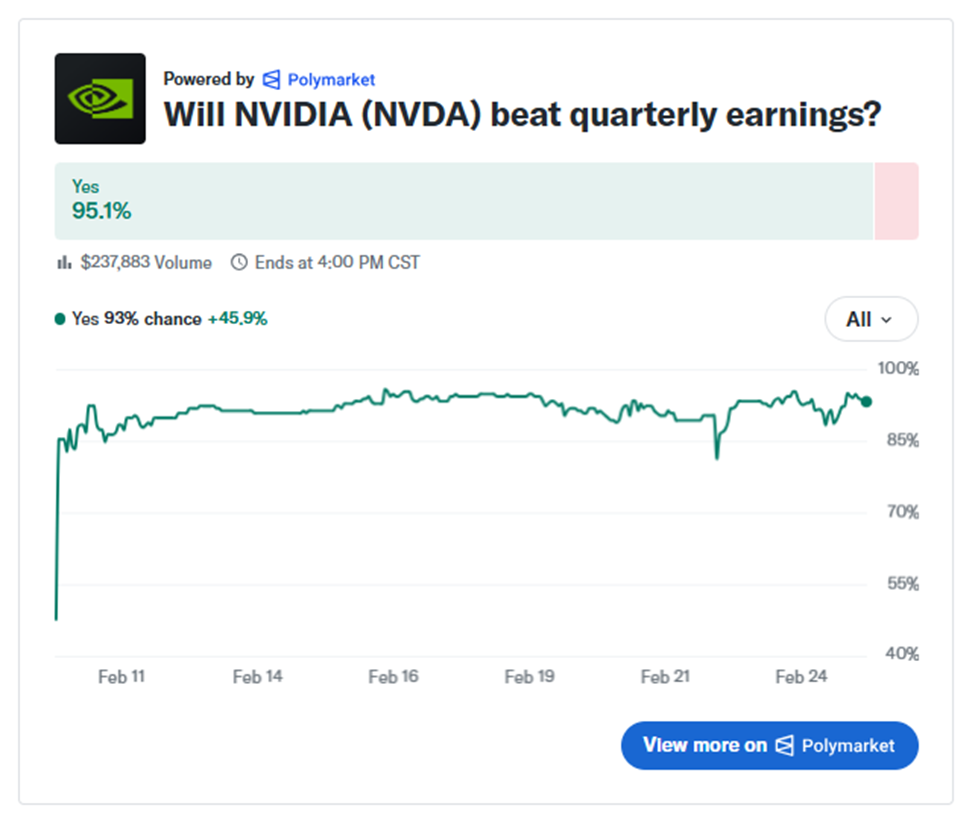

In the 1970s, every Sunday morning on CBS’s The NFL Today, a man named “Jimmy the Greek” would sit beside Brent Musburger and calmly predict the final scores of that afternoon’s games. He never mentioned point spreads. He couldn’t. Sports betting was illegal in most of America. So instead of talking about the line, he’d say something like, “The Raiders will beat the Rams, 31–21.” To the average viewer, that sounded like a straightforward prediction. To anyone who knew the spread, it was something more. If the Raiders were favored by 5 and Jimmy predicted a 10-point win, he wasn’t just picking a winner. He was signaling he thought they’d cover the spread. The people paying attention didn’t need him to say the odds out loud. They could read between the lines. Today, there’s no need for coded language. Betting is legal across much of the country. In fact, you can wager on everything from the Super Bowl to presidential elections to Taylor Swift’s wedding date. And increasingly, markets are putting real-time probabilities on corporate events. This brings us to NVIDIA Corporation (NVDA), which announced earnings after the bell on Wednesday. For years, I’ve called NVIDIA’s report the grand finale of earnings season. In many ways, it’s like the Super Bowl. Everyone’s watching. And plenty of money is riding on the outcome. Heading into this quarter, probability markets were assigning better than a 90% chance that NVIDIA would beat earnings.

When confidence gets that high, the question changes. It’s no longer just whether NVIDIA will “win.” It’s whether it will beat the spread – and by how much. In other words, if expectations are through the roof, what happens when the bar gets raised so high that even excellence isn’t good enough anymore? Now, as I’ll explain in a moment, NVIDIA did more than win. By any traditional measure, it was a blowout quarter. And yet… As I write this, the stock is down nearly 4% – despite beating on revenue, earnings and guidance. This is exactly what I predicted in a recent special presentation. I argued that we’re in the middle of an AI Dislocation – a period when market leadership begins to shift. I also warned that expectations for the mega-cap AI stocks had reached extreme levels. And in that kind of environment, even strong results can trigger selling as capital rotates toward new winners. So, in today’s issue, I’m going to walk through the details of NVIDIA’s earnings and the market’s subsequent reaction. I’ll also discuss why expectations matter more than the headline numbers… and how moments like this can trigger a sharp rotation in the AI trade – creating risk for the obvious names, and opportunity in the overlooked ones. The Earnings Scoreboard Let us start with the facts. NVIDIA reported earnings of $1.62 per share on revenue of $68.1 billion. Wall Street was expecting $1.53 per share on $65.8 billion in revenue. That represents revenue growth of 73% compared with the same quarter a year ago. Data center revenue came in at $62.3 billion, ahead of expectations. And for the current quarter, the company guided revenue to roughly $78 billion. Analysts had been looking for closer to $72.8 billion. By any historical standard, those numbers are extraordinary. I am still amazed that a company of this size can produce accelerating sales and earnings momentum. And it is not happening in isolation. - Super Micro Computer, Inc. (SMCI) is reporting triple-digit sales growth.

- VertivHoldings Co. (VRT) is delivering strong sales and guidance.

- Taiwan SemiconductorManufacturing Co. Ltd. (TSM) recently announced January sales growth of 37%, well above its prior guidance of 30%.

In other words, the demand environment across the AI ecosystem remains powerful. This leads to the question… If the numbers were so strong, why did the stock sell off? So Why Did the Stock Fall? There are several reasons. First, expectations were even higher in some corners of the market. While consensus estimates were around $72.8 billion for the current quarter, some analysts were modeling revenue closer to $80 billion. When expectations drift that high, even a strong beat can feel like a disappointment relative to the most optimistic projections. Second, investors are asking tougher questions about sustainability. Can this level of AI spending continue for years? Will NVIDIA remain as dominant as artificial intelligence shifts from training massive models to running everyday applications? Third, there are ongoing uncertainties in China. Licensing approvals remain fluid, and the company is excluding China data center revenue from certain forecasts. Finally, there is the simple matter of options positioning. NVIDIA is one of the most actively traded stocks in the world. Many investors write covered calls on the stock. Market makers hedge those positions. When you combine heavy options activity with a company of this size, post-earnings price action can become more mechanical than emotional. This is what I mean when I told my followers that “physics” can affect a company of this scale. It takes enormous capital flows to move the needle. None of this changes the fact that NVIDIA is still executing at an extremely high level. The Physics of Expectations When a company becomes one of the largest in the world, perfection gets priced in. The bigger the company, the higher the expectations. And the higher the expectations, the harder it becomes to surprise to the upside in a way that satisfies everyone. That does not mean the growth story is broken. It means the bar keeps rising. NVIDIA’s forward valuation has been compressing because earnings are growing so quickly. That is not the hallmark of a speculative bubble detached from fundamentals. It is the result of extraordinary profit growth. Chief Executive Officer Jensen Huang addressed these concerns directly on the earnings call. He emphasized that customers are already monetizing their artificial intelligence investments. They are generating real cash flow from the computing capacity they are buying. This is not speculation without revenue. This is massive capital deployment backed by visible demand. But while NVIDIA continues to deliver, something else is happening beneath the surface. Stage 1 and Stage 2 The AI Dislocation I have been describing is not about the end of the artificial intelligence boom. It is about leadership rotation within it. Stage 1 of any technological revolution rewards the obvious leaders. The pioneering companies behind the tech. The headline names. The stocks everyone talks about. In artificial intelligence, aside from NVIDIA, it’s the mega-cap hyperscalers. Amazon. Alphabet. Meta. Microsoft. Collectively, those companies are expected to spend roughly $650 billion on AI-related capital expenditures in 2026 alone. That level of spending is phenomenal news for the suppliers building out the data center boom. But for the hyperscalers themselves, it becomes a question of margins and returns. Capital intensity rises. Expectations rise. The bar rises. Stage 2 is when the companies enabling the buildout begin to show faster earnings acceleration than the giants making the headlines and spending all that money. In other words, you want to be where the money is flowing. The power systems. The cooling technology. The semiconductor equipment makers. The networking backbone. The companies NVIDIA and the hyperscalers need to build all those data centers. These businesses often start from smaller bases. Their revenue growth can compound faster. Their earnings momentum can accelerate more dramatically. And when capital begins to rotate, the returns for investors can be significant. The Bottom Line We are in the middle of an AI Dislocation. NVIDIA just proved that demand remains strong. The AI boom is not ending. But the market is shifting. Bottom line, I remain very bullish on NVIDIA over the long term. I believe the stock will be significantly higher in the years ahead. But when expectations for the obvious names reach extreme levels, leadership can shift. And when it does, the biggest percentage gains often come from the companies most investors are not watching. That is why I recently put together a special briefing detailing what’s going on and how investors can position themselves as this AI Dislocation unfolds. If you want to position yourself for the next phase of this boom – instead of chasing yesterday’s winners – I strongly encourage you to go here to watch my free AI Dislocation briefing now. Sincerely, Louis Navellier

Editor, Market 360 The Editor hereby discloses that as of the date of this email, the Editor, directly or indirectly, owns the following securities that are the subject of the commentary, analysis, opinions, advice, or recommendations in, or which are otherwise mentioned in, the essay set forth below: NVIDIA Corporation (NVDA), Super Micro Computer, Inc. (SMCI) and Vertiv Holdings (VRT) |

No comments:

Post a Comment