| Read in browser | ||||||||||||||

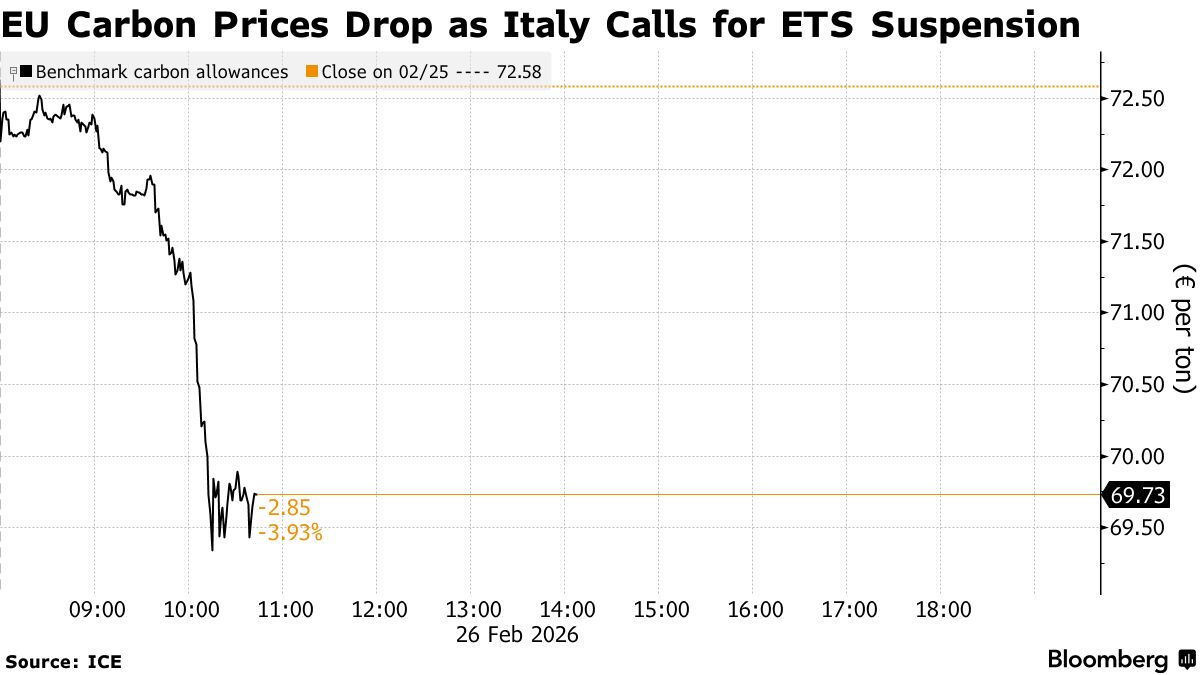

The European Union managed to rally 27 nations behind the world's most ambitious plan to zero out carbon pollution. Now that consensus is fraying. Today's newsletter looks at the heated arguments within the EU over its strict emissions trading system and what lies ahead. Also, billionaire Tom Steyer stopped by Bloomberg's San Francisco office to talk about his gubernatorial run and his plan to lower California energy prices. Someone forward you this newsletter? You can subscribe to the Green Daily for free climate and energy news six days a week. Brewing fightBy John Ainger Italy has launched the biggest attack yet on what many see as the jewel in the crown of the EU's climate policy: its carbon market. Conceived more than two decades ago, the EU's Emissions Trading System, or ETS, has become the key driver of the bloc's decarbonization push as it seeks to become the first climate neutral continent by the middle of this century. Its beauty lies in the fact that it's a market-based instrument that incentivizes companies to adopt new clean technologies, or to pay for each ton of carbon dioxide they eject into the atmosphere. Yet over the past month, some countries have started to question its very existence as they seek quick fixes to stave off growing signs of deindustrialization.  Rome is already preparing a sweeping overhaul of its electricity market that would strip carbon costs from power bills, but this morning industry minister Adolfo Urso went one step further. He slammed the ETS for being "ineffective and "harmful," and called on the European Commission to suspend it until a thorough overhaul has taken place. While such a move is unlikely, it highlights just how much pressure the EU is under from certain quarters to make sure its climate ideals don't get in the way of a harder economic reality. It also underscores a deeper friction within the EU over the best way to make sure that its economy keeps pace with China and the US. After months of delay, the commission is finally due next week to come forward with a "Made in Europe" act that is expected to break with a free-trade mantra that has governed decades of policy. Under the latest draft seen by Bloomberg, it will set strict criteria to favor European firms in public procurement, while obliging some foreign competitors to share technologies and hire locally if they want to operate on the continent. A key question is which countries outside the bloc will be deemed "trusted partners." "We can't invite partners like Canada and India to trade with us and then say we only buy European," Katherina Reiche, Germany's minister for economic affairs and energy, said on Thursday. "We need a made with Europe, not only a made in Europe." Read the full story about Italy's push to suspend Europe's carbon market and subscribe to Bloomberg news for the latest news on the review. Price plunge8% How much European carbon prices slumped after German Chancellor Friedrich Merz said the bloc should be open to revising or delaying the program. Time for a rethink"It is clear that today it is not functioning well for some countries" Emmanuel Macron French President Macron said the EU must reconcile competitiveness with its climate agenda, while urging the bloc to preserve the carbon market. Playing monopolyBy Brian Kahn Tom Steyer wants to start a revolution. Specifically, the billionaire running for California governor is interested in an electricity revolution. California has some of the highest electric bills in the US and a convoluted regulatory framework that has slowed down grid interconnection. That stands in contrast to other places, such as China, which spent a record amount on improving its grid last year and has transmission lines that can transport more energy than any in the US. "We have an electricity revolution going all around the world and for some reason we have legal structures that say we can't participate," Steyer said in a visit to Bloomberg's San Francisco office on Wednesday.  A still from Tom Steyer's campaign announcement. Image: Tom Steyer via X Steyer, a clean tech investor, wants to break up the monopoly three major investor-owned utilities have over the state's energy system, and he's making it a central part of his campaign. "Monopolies always overcharge and they always produce bad service 100% of the time, and that's what's happening here," he said. Expanding competition, he said, will bring down bills and benefit everyday Californians as well as make it more enticing to start a business in the state. He also touted rooftop solar, batteries and artificial intelligence tools to improve grid efficiency as a way to further lower costs. Critics have raised questions about the effectiveness Steyer's approach. They argue that breaking utilities' monopolies wouldn't address the cost of power transmission and distribution, which make up a major portion of energy bills, and that rooftop solar can sometimes drive up costs. There's also the cautionary tale of the early 2000s, when energy prices skyrocketed and rolling blackouts hit California after the state deregulated the electricity market. Bringing down people's bills was a key message as Democrats swept into power in city- and state-level races last year. Largely absent were promises to fix the climate. But Steyer, who ran a climate-focused presidential campaign in 2020, said there are clear connections between affordability and cutting emissions. "We are talking about climate in a way people can relate to," he said. "Health, energy costs, zoning: the things that really matter." Subscribe to the California Edition newsletter for a weekly look at one of the world's biggest economies and its global influence. Courting disasterBy Zahra Hirji President Donald Trump says he wants to shift the responsibility of handling disasters from the federal government to cities and states. But his administration quietly dismantled a division working towards that goal by making the public more prepared for snow, flooding and hurricanes. In a bid to cut costs, the Federal Emergency Management Agency closed the Individual and Community Preparedness Division, or ICPD, and many of its programs last year, according to an internal document seen by Bloomberg News and people familiar with the unit. Victoria Barton, a spokesperson for FEMA, confirmed the agency shut down the division in September as part of an effort to root out "ineffective programs that waste taxpayer money and create bureaucratic red tape."  A FEMA office in Washington, DC. Photographer: Valerie Plesch/Bloomberg A small, low-budget FEMA program, ICPD reached millions of Americans through educational materials and training sessions on how to prepare for and respond to natural disasters. It provided guidance ranging from checklists to identify key personal documents to keep safe during a crisis to formal training on how to locate and rescue people in certain situations before help arrives. "The true first responders are the neighbors — it's neighbors helping neighbors," said Deanne Criswell, President Joe Biden's FEMA chief. "They get the tools and resources and the knowledge from programs that are funded through [ICPD]." Read the full story to find out what else the agency has done with ICPD resources. Subscribe to Bloomberg News for all the latest on how the Trump administration is reshaping disaster response and preparedness. This week's Zero The megalithic entrance to the Kalasasaya mound at Tiwanaku . iStockphoto Societal collapses happen more often than you think, and there's much we can learn from the past to avoid or, at least, delay another one. This week's guest on Zero is Luke Kemp, author of Goliath's Curse, which draws lessons from the rise and fall of societies over 5,000 years of human history. Akshat Rathi asks Kemp whether our current moment — with climate change and AI — makes us uniquely vulnerable to societal collapse or more resilient than we might think. Listen now, and subscribe on Apple, Spotify or YouTube to get new episodes of Zero every Thursday. More from GreenBack in December, the retraction of a key climate report was seen as proof that the economic cost of global warming had been overstated. Now, Norway's wealth fund says its own analysis indicates that would be the wrong conclusion to draw. Scientists from the Potsdam Institute for Climate Impact Research last year took down a paper that had fed into scenarios used by central banks and investors, including Norway's $2.2 trillion wealth fund. The retraction followed criticism from scientists and academics of the paper's methodology, and a formal review ultimately led the paper's authors to acknowledge "substantial" issues. But in Oslo, a team at Norges Bank Investment Management decided to dig further. As part of an ongoing analysis into the potential for climate change to result in portfolio losses, NBIM studied the review of the retracted paper as well as the criticisms of its methodology to arrive at its own assessment. "At the end of this process, we still believe models tend to underestimate physical risk," NBIM said in an email to Bloomberg, referring to the real-world fallout of rising temperatures. Read the full story.  A net-zero alliance has come back from the dead. The Net Zero Asset Managers suspended operations last January. That decision coincided with a mass exodus from net-zero groups, with an equivalent alliance for banks virtually being wiped off the North American map. But the group is back with 250 signatories. Niche Australian metals companies are so hot. Well, one in particular. Lynas Rare Earths, which produces relatively small amounts of critical minerals, has overtaken Australian blue-chip stalwart Qantas Airways by market capitalization. The reason? Concerns about China's supply chain dominance. More from Bloomberg

Explore all Bloomberg newsletters. Follow us You received this message because you are subscribed to Bloomberg's Green Daily newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.

|

Thursday, February 26, 2026

Europe’s carbon market under attack

Subscribe to:

Post Comments (Atom)

I showed everything — You can see it all here

I put everything on the table in my Dark Wire webinar and the replay is still up. But not for long. If you haven...

-

PLUS: Dogecoin scores first official ETP ...

-

Hollywood is often political View in browser The Academy Awards ceremony is on Sunday night, and i...

No comments:

Post a Comment