How A 26-Year Old Hacked The "Holy Grail" Of Retirement Accounts & Turned $10,000 Into $1.8 Million In A Year

Hey, it's Tim.

I just finished recording a brand-new interview with a 26-year old who figured out an ingenious way to grow his retirement account.

Sometimes traders turn up their noses at trading inside of a retirement account because you can't short stocks, use margin or trade with any sophisticated options strategies.

You're also limited on how much money you can put into the account so typically these accounts are designed for slow growth over decades.

I grilled him for all the details – including the #1 pattern he looks for and even some of the biggest mistakes he made along the way. You can listen to the conversation at no cost right here…

NFLX Stock Sinks After Company Announces $82.7 WBD Deal

Posted On Dec 05, 2025 by Chris Markoch

Shares of Neftlix Inc. (NASDAQ: NFLX)are down over 3% in midday trading. NFLX stock is now down over 19% in the last three months. The sell-off on a day when the broader market is rising may surprise investors after the company announced its intention to purchase Warner Bros. (NASDAQ: WBD) for $82.7 billion.

Table of Contents

On the surface, this deal looks like game, set, and match for Netflix. The company now gains control over an expansive library of content that includes the DC Universe (e.g., Batman, Superman, Wonder Woman), along with the Harry Potter Wizarding World and the vast HBO library.

However, if you'll indulge a sports metaphor, there are many times when a team makes a free agent signing that looks like a can't-miss deal. Sometimes it works. Other times it becomes apparent why the player was available in the first place.

Bringing it back to Netflix. Was Warner Bros. on sale for a reason? To be fair, $82.7 billion isn't chump change, but it would seem that a content library as I described above would be worth more.

Time will tell. But for now, let's look at some other potential positives and negatives for NFLX stock.

A Case of Back to the Future

The deal gives off echoes of Netflix's past, when it housed almost all syndicated content. Of course, in recent years, the company has become one of the most prolific producers of original content as businesses like Paramount, NBC Universal, and others have brought that content back in-house.

Having WBD's catalog available offers value beyond price. This deal should allow Netflix to negotiate better terms with its advertisers and partners. And let's face it. Netflix will also benefit from a potential subscriber magnet that will make it easier for the company to fund its own original content.

That's not to say Netflix isn't already doing that. The company has forecasted approximately $9 billion in free cash flow (FCF) for the full year 2025. The company also has an operating margin of around 31.3%.

But that's not the same as having $80 billion lying in its couch cushions. Netflix is arranging tens of billions of dollars in bridge loans to finance the cash portion of the deal. That leverage could put a strain on the company's margins in future quarters.

The Death of the Box Office

Another concern that shareholders face is the possibility that the deal will be struck down. You might think that the current administration would be more aligned with such deals. However, reports suggest that top-ranking White House officials have concerns about how much power the combined Netflix-WBD company would have over Hollywood.

For context, many of the WBD franchises are among the few remaining that can still reliably generate multibillion-dollar box office cycles and tentpole momentum for theaters.

In an effort to allay those concerns, Netflix has pledged to honor any contractual agreements for releasing Warner Bros.’ studio films. However, that will only bind the company for so long. The concern is that if Netflix, whose business model prioritizes direct-to-streaming releases and shortened or nonexistent theatrical windows, were to gain control of a legacy studio built on blockbuster scale, it could:

Accelerate the erosion of exclusive theatrical releases

Reduce film-to-theater runs in favor of streaming-first debuts

Compress release windows to drive subscriber growth rather than box office revenue

Shift Warner's big franchises into streaming event content instead of theatrical tentpoles

In a market already struggling with a reduced release calendar, fewer mid-budget films, and ongoing post-strike production lags, the potential pullback of Warner's slate could materially weaken U.S. theater chains, distribution pipelines, and premium formats (IMAX, Dolby, etc.).

Put simply, if a Netflix-owned Warner Bros. prioritizes subscriber growth over box office receipts, the entire theatrical ecosystem could lose one of the last remaining engines of dependable blockbuster volume.

The Netflix Rebuttal – Streaming Has Already Won

The framework for the Netflix counterargument could be summarized as "they call it Netflix and chill" for a reason. That's a bit simplistic, but it's fair to say that the way content is consumed is vastly different. That shift has accelerated in the last five years.

So Netflix will say its biggest competition comes from tech giants like Apple (NASDAQ: AAPL) and Amazon.com Inc. (NASDAQ: AMZN) that are building their own content studios. This will make Netflix more of a media company and less of a tech stock. That could make NFLX stock more attractive to funds and more conservative retail investors.

What to Do with NFLX Stock?

Time will tell. And the story may have as many twists and turns as a Netflix original series. But if you're looking to buy NFLX stock, you may want to wait for a better entry point.

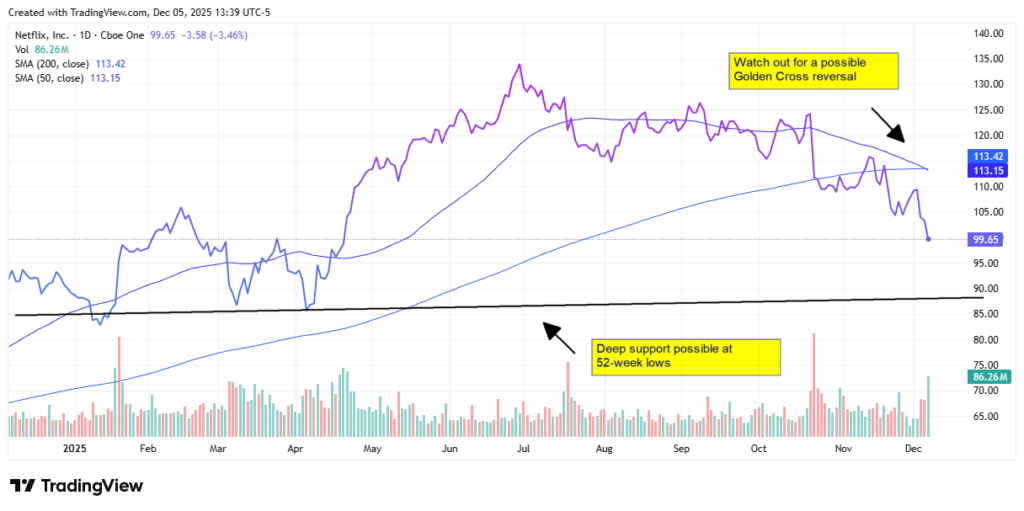

NFLX stock is below its 50-day and 200-day simple moving averages, with the 50-day pointing down toward the 200-day, which is a sign of deteriorating sentiment.

Until the stock can reclaim the 50-day SMA, any rally is best viewed as a counter-trend bounce within a bearish trend.

From a trading perspective, the skew favors:

Short-term: selling strength into the 105–112 zone or using tight stops above the 50-day for any tactical longs.

Medium-term: waiting for either an RSI washout below ~30 plus MACD inflection, or a decisive reclaim of the 50- and then 200-day averages before treating this as anything more than a bounce candidate.

This is a PAID ADVERTISEMENT provided to the subscribers of StockEarnings Free Newsletter. Although we have sent you this email, StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above.

Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click Unsubscribe.

StockEarnings, Inc 33 SE 4th St, Suite 100, Boca Raton, FL 33432 USA W: 877.6.STOCKS StockEarnings.com

No comments:

Post a Comment