Below is an important message from one of our highly valued sponsors. Please read it carefully as they have some special information to share with you.

Carvana Co. (NYSE: CVNA) is an online retailer for used cars. Since entering the market in 2017, CVNA stock has taken investors on a wild ride. It surged in 2021 as its business model was ideal at a time when "social distancing" entered our collective vernacular.

Table of Contents

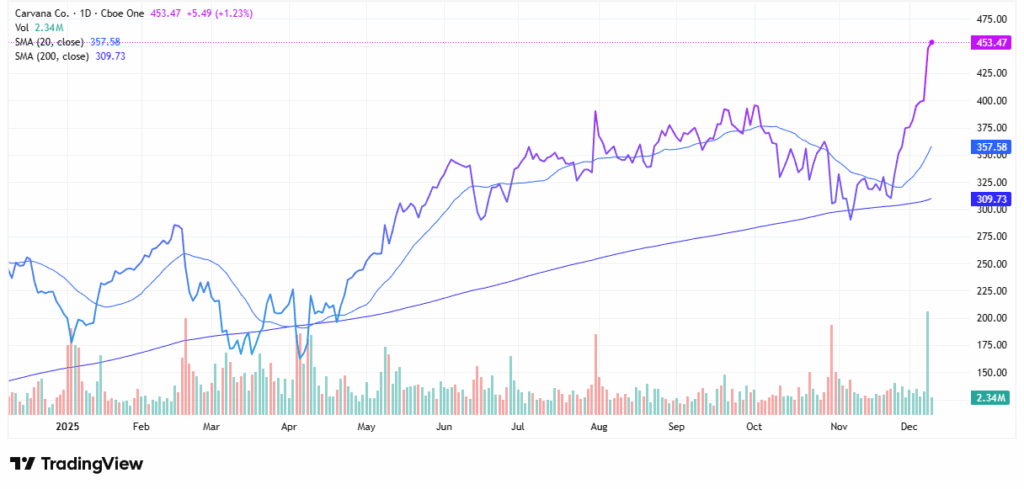

Those gains disappeared quickly. However, since the beginning of 2024, CVNA stock has been in an undeniable uptrend. It made an all-time high earlier this year and blew past that after the announcement that it would be included in the S&P 500.

Keep in mind, CVNA stock won't start trading as part of the S&P 500 until later this month. But it would seem that investors believe that Carvana is headed much higher.

I'm not so sure.

Putting aside any macroeconomic arguments (of which there are a few), CVNA stock has made a parabolic move. That usually means that a pullback is likely in the short term.

The Macroeconomic Concerns

To be fair, Carvana continues to deliver vehicles at a strong pace, and that's not something to dismiss. Unit volumes have rebounded sharply from 2022 lows, and management has made strides in reducing reconditioning bottlenecks, improving logistics routing, and tightening inventory discipline. In other words, operational execution is much better than it was during the company's period of aggressive and unsustainable growth.

But even strong fundamentals can run into a brick wall if the macro environment turns. And the used car market, while stabilizing, remains tied to interest rate policy, employment conditions, and consumer credit health.

Auto loan delinquencies continue to rise, particularly for subprime borrowers. According to recent Federal Reserve data, the 90-day-past-due rate for subprime auto loans is at its highest level since before the 2008 financial crisis. Carvana, by virtue of its volume model, has meaningful exposure to this segment. If consumers in the lower-credit tiers continue to struggle, Carvana's financing arm could see higher default rates and tighter margins—even if unit deliveries remain robust.

High rates also continue to pressure affordability. The average monthly payment for a used vehicle has remained historically elevated. While the Federal Reserve has signaled the potential for rate cuts in 2026, there's little evidence that affordability will normalize quickly. Prices may be softening, but that doesn't automatically translate into healthier buying conditions if financing remains restrictive.

Then there's the broader economic question. The labor market is cooling. Wage growth has slowed. Consumer savings are largely depleted from pandemic-era levels. If unemployment ticks meaningfully higher, discretionary categories (and yes, a vehicle purchase can still fall into that camp) tend to show immediate stress.

Carvana's core strength is built on the rapid turnover of inventory through a frictionless buying experience. That model works best when consumers feel secure, credit flows freely, and used vehicles retain value. If any of those three supports weaken, the bull case becomes harder to justify in the near term.

To this point, Carvana's leadership has been adamant that the company has turned the corner on profitability. And they have—at least on a trailing basis. The shift to a leaner cost structure is real, and investors are right to acknowledge it. But the market is now pricing Carvana as though this profitability inflection is both permanent and insulated from macro risk. That's a tougher assumption to defend.

The Valuation Concerns

The cloudy macroeconomic outlook is why you can't overlook Carvana stock's extended valuation. It's trading at over 7x next year's sales and a price-to-earnings (P/E) ratio of around 104x. That puts it in the category of some of the hottest technology stocks.

And that could be the point. For some investors, the company does fit into the tech stock category. Supporting that thesis is the company's return on invested capital (ROIC) of roughly 25% which would, in general, mean the stock commands a higher multiple.

However, that's only the case if investors believe that the level of ROIC is sustainable. To be fair, this is a dramatic improvement for the company, which was burning cash prior to 2023, and profitability looked like a pipe dream.

Carvana has sharpened its underwriting, optimized reconditioning centers, and materially cut SG&A per unit—all of which have driven ROIC into the range that investors typically associate with mature, quality operators rather than growth-at-all-costs disruptors.

That said, much of the ROIC rebound has been supported by unusually favorable used car pricing dynamics coming out of the pandemic. When used vehicle values were elevated and supply was tight, Carvana squeezed more profit per unit and leaned successfully into high-turn inventory. Now, however, as used car prices continue to normalize and wholesale spreads compress, maintaining a mid-20s ROIC becomes more challenging.

The company also remains tied to auto credit conditions. Carvana finances a significant portion of the cars it sells. Subprime exposure means that if delinquency rates continue to rise, the company may need to tighten credit standards or absorb higher loss provisions. Either path puts pressure on the very return metrics that are supporting the current valuation.

Carvana Stock Looks Extended

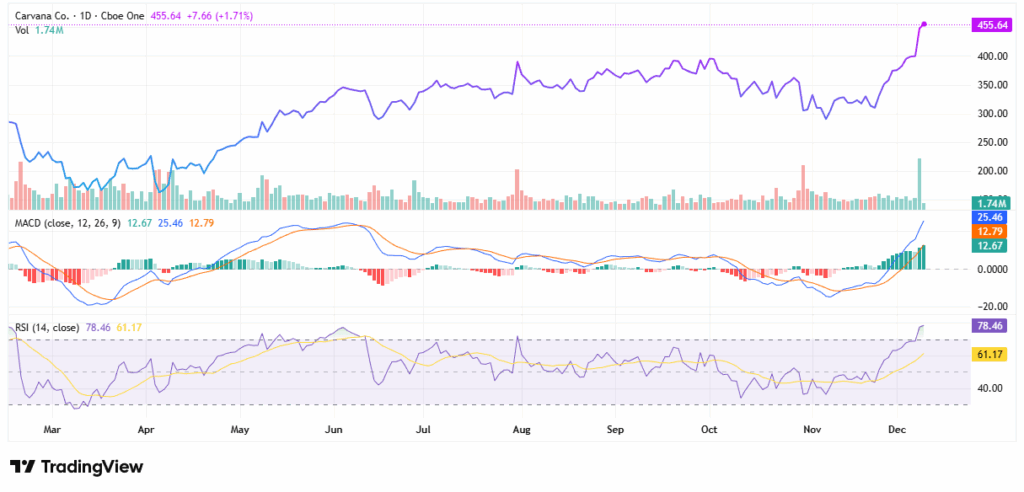

The recent spike in CVNA stock has pushed it well above its short- and long-term moving averages. That's great news if you bought the stock earlier this year, but it's not a guarantee that new highs are coming.

For that, you should consider momentum indicators. And in this case, they're looking a little frothy. The MACD line is solidly green, and the histogram has been expanding. However, a relative strength indicator of approximately 78 places CVNA firmly in overbought territory, suggesting that the next move for the stock is likely to be lower.

That could be good news for investors who believe in the long-term story because you'll get a second chance to start a position. But at what price?

The consensus price target for CVNA stock is $429.04. That's about 5.9% lower than the stock's price on December 9. Analyst sentiment has been mixed since the company's earnings report. That reflects the risk-reward dynamic present in the stock.

The Bottom Line on CVNA Stock

If you believe that the company can continue to deliver growth along with operational efficiency, then CVNA stock may be a good investment. However, it's tough to look past the valuation.

Carvana, at its current multiple, isn't valued like a company that will merely hold its ground. It's valued like one that will continue to improve efficiency even as the macro environment, credit conditions, and used vehicle pricing become less accommodating.

This is a PAID ADVERTISEMENT provided to the subscribers of Daily Options Signals Free Newsletter. Although we have sent you this email, Daily Options Signals and StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above.

Your privacy is very important to us. If you no longer wish to receive email from DailyOptionsSignals.com, please click Unsubscribe.

StockEarnings, Inc 33 SE 4th St, Suite 100, Boca Raton, FL 33432 USA W: 877.6.STOCKS StockEarnings.com

No comments:

Post a Comment